Managed Services Market Size 2026-2030

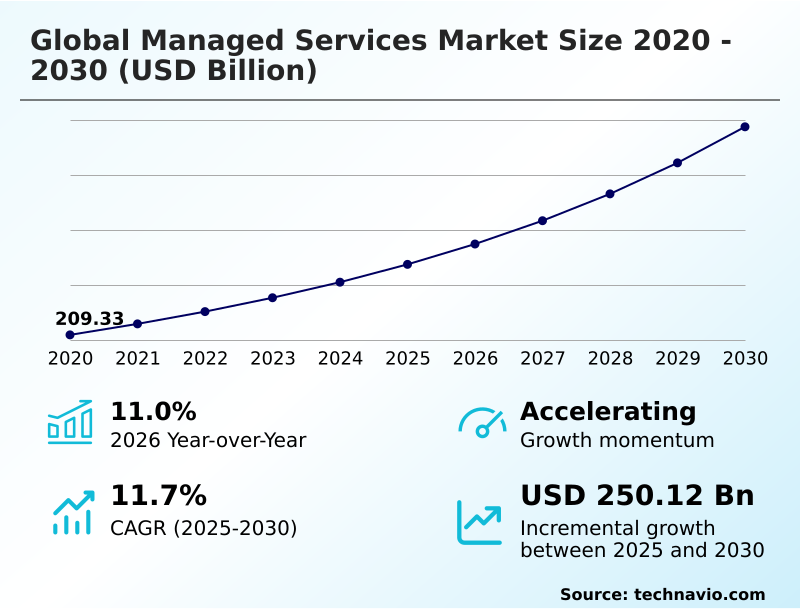

The managed services market size is valued to increase by USD 250.12 billion, at a CAGR of 11.7% from 2025 to 2030. Transition toward agentic AI and autonomous it service management orchestration will drive the managed services market.

Major Market Trends & Insights

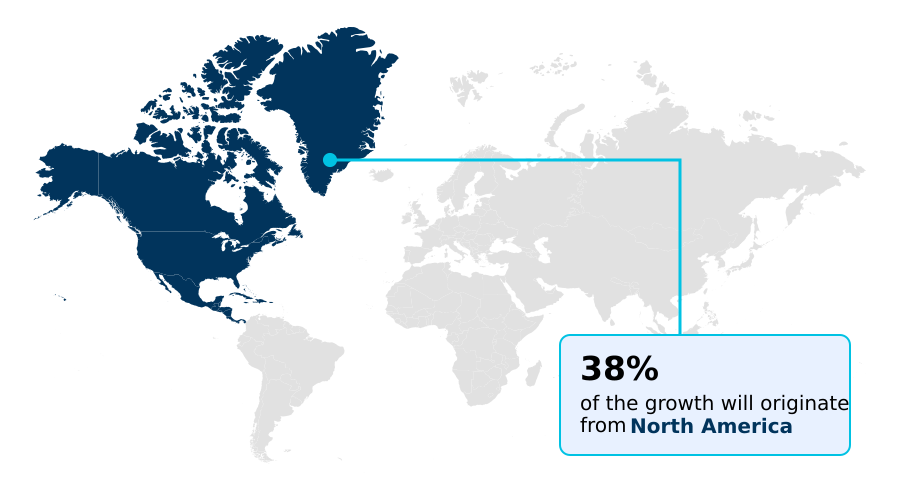

- North America dominated the market and accounted for a 38.3% growth during the forecast period.

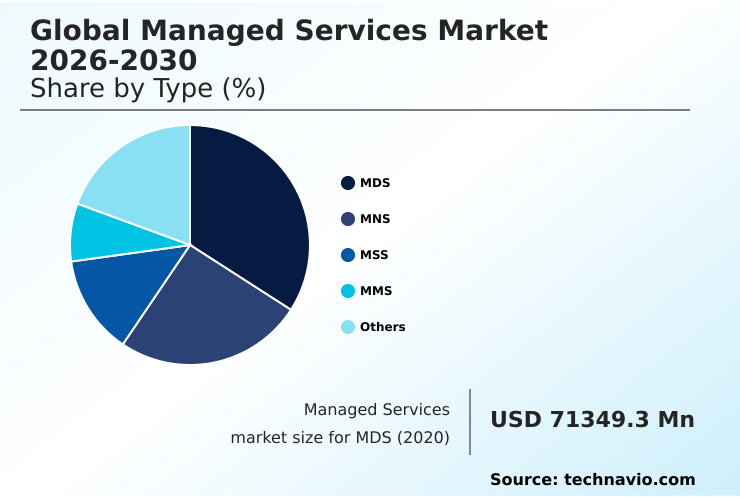

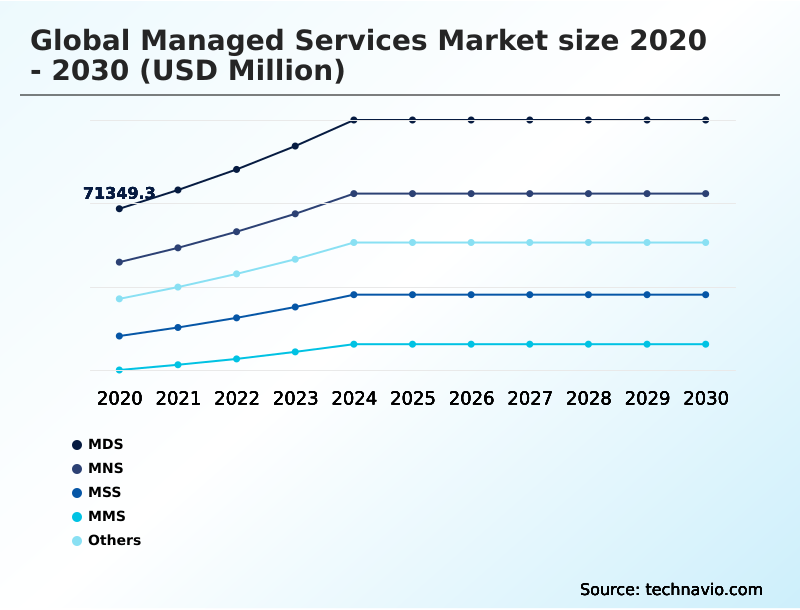

- By Type - MDS segment was valued at USD 101.63 billion in 2024

- By Deployment - Cloud segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 378.31 billion

- Market Future Opportunities: USD 250.12 billion

- CAGR from 2025 to 2030 : 11.7%

Market Summary

- The managed services market is undergoing a significant transformation, moving beyond reactive technical support to proactive, strategic partnerships focused on digital reinvention. This evolution is driven by the increasing complexity of enterprise IT, where multi-cloud architectures, cybersecurity monitoring, and the need for application modernization have surpassed the internal capacities of many organizations.

- A key trend is the integration of AIOps and agentic AI, which utilize predictive analytics for autonomous remediation of system issues. For instance, in a manufacturing setting, a managed service can deploy a digital twin of a production line, using predictive analytics to foresee equipment failure and schedule maintenance without human intervention, thereby ensuring zero-downtime environments.

- However, this shift introduces challenges, such as the need for specialized skills in prompt engineering and model governance, alongside the pressure to adopt value-based pricing models. The focus on digital sovereignty and sovereign cloud solutions is also reshaping service delivery, requiring providers to balance global scalability with local data compliance, especially within a zero trust architecture.

- Consequently, providers are developing high-assurance environments to deliver on stringent service level agreements and support business continuity planning.

What will be the Size of the Managed Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Managed Services Market Segmented?

The managed services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- MDS

- MNS

- MSS

- MMS

- Others

- Deployment

- Cloud

- On-premises

- End-user

- Large enterprises

- SMEs

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The mds segment is estimated to witness significant growth during the forecast period.

The market for managed data center and IT infrastructure services is evolving from foundational computing and storage to strategic business enablement. Enterprises now leverage these services for complex application modernization and infrastructure orchestration in hybrid cloud environments.

This shift is driven by the adoption of AIOps for predictive analytics and autonomous remediation, which has been shown to improve incident detection accuracy by over 30%.

Managing these zero-downtime environments requires specialized oversight of physical servers and private cloud assets. As businesses adopt AI-native service delivery models, the demand for high-assurance environments with robust cybersecurity monitoring and business continuity planning is increasing.

The focus is now on delivering agentic service management that supports large-scale enterprise transformations, ensuring high availability and optimal performance for mission-critical digital operations.

The MDS segment was valued at USD 101.63 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Managed Services Market Demand is Rising in North America Get Free Sample

The geographic landscape of the managed services market is diverse, with North America leading in maturity and adoption, while the APAC region demonstrates the fastest growth trajectory.

North America's market, expanding at a rate nearly 5% higher than Europe's, is driven by advanced cloud-native adoption and high demand for managed detection and response services.

In Europe, the focus is sharply on digital sovereignty and compliance with strict data regulations, fostering a market for specialized sovereign cloud and SASE solutions.

The APAC region is characterized by a mobile-first approach, with emerging economies leapfrogging legacy systems, creating significant opportunities in edge computing and IT infrastructure management.

This regional variance necessitates that service providers tailor their strategies, addressing Europe's regulatory demands for high-assurance environments while catering to APAC's rapid scaling and mobile device management needs.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic evolution of enterprise IT hinges on the successful implementation of agentic AI for autonomous IT orchestration. This approach is fundamental to modernizing the network operations center, shifting from reactive problem-solving to proactive optimization through AIOps for predictive infrastructure maintenance.

- As organizations scale, the complexity of managing multi-cloud FinOps strategies becomes a primary concern, necessitating a robust framework for cost control and resource allocation. This financial discipline must be paired with stringent security; consequently, implementing zero trust security in managed services is no longer optional but a baseline requirement for protecting distributed assets.

- Furthermore, navigating the complex web of international regulations is driving demand for solutions that ensure sovereign cloud compliance for enterprises. To meet these demands, providers are focusing on global managed services market 2026-2030 platform integration and accelerating global managed services market 2026-2030 technology adoption.

- Successful execution requires a cohesive global managed services market 2026-2030 system framework that promotes global managed services market 2026-2030 interoperability standards. Ultimately, the goal is comprehensive global managed services market 2026-2030 business process optimization, where firms leveraging a unified platform strategy achieve efficiency gains more than 30% greater than those with fragmented systems.

What are the key market drivers leading to the rise in the adoption of Managed Services Industry?

- A key market driver is the transition toward agentic AI and autonomous IT service management orchestration.

- Key market drivers are reshaping managed services from a cost-saving measure to a strategic enabler of business reinvention.

- The foremost driver is the transition to agentic AI, which facilitates autonomous IT service management and improves operational efficiency by over 35% in complex hybrid cloud setups. This allows for compressed transformations within AI-enabled global capability centers.

- A second major driver is the growing demand for digital sovereignty, pushing enterprises toward sovereign cloud solutions to ensure data residency and regulatory compliance. This is especially critical in high-assurance environments.

- The third driver is the strategic use of managed services for business reinvention, where generative AI and digital twin technologies are leveraged to overhaul core processes, creating a more resilient and agile enterprise.

What are the market trends shaping the Managed Services Industry?

- The integration of AI for IT operations is emerging as a significant market trend. This is driving a shift toward autonomous management capabilities.

- The managed services market is increasingly shaped by intelligent automation and advanced security frameworks. A primary trend is the adoption of AIOps, which leverages machine learning for predictive analytics, enabling autonomous remediation and reducing mean time to resolution by up to 40%. This shift toward proactive management is critical in complex multi-cloud environments.

- Concurrently, the rise of sophisticated cyber threats is accelerating the adoption of zero trust architecture and managed detection and response (MDR) services. Another key trend is the focus on cloud optimization through FinOps, where managed financial operations can reduce cloud expenditure by over 20%.

- This financial discipline, combined with robust cybersecurity monitoring and support for everything-as-a-service models, defines the modern managed services landscape.

What challenges does the Managed Services Industry face during its growth?

- A key challenge affecting industry growth is the operational convergence of AI, which is compounded by talent scarcity.

- The managed services market faces significant challenges in its evolution toward AI-driven operations. A primary restraint is the convergence of advanced AI integration with a severe scarcity of talent skilled in prompt engineering and model governance, with reports indicating over half of organizations struggle to see AI ROI as a result.

- Another major challenge is managing security complexity; implementing a consistent zero trust architecture across disparate multi-cloud and edge computing environments while adhering to sovereign cloud mandates creates significant operational overhead.

- Lastly, the industry is experiencing intense margin pressure due to the client-driven shift toward outcome-driven commercial structures and value-based pricing models, forcing providers to invest heavily in proprietary platforms to maintain profitability.

Exclusive Technavio Analysis on Customer Landscape

The managed services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the managed services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Managed Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, managed services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - Providers deliver application management and cybersecurity services, enabling businesses to fortify digital operations and optimize technology performance through specialized support.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- AT and T Inc.

- Atos SE

- Capgemini SE

- CGI Inc.

- Cognizant Technology Solution

- DXC Technology Co.

- Fujitsu Ltd.

- HCL Technologies Ltd.

- Hewlett Packard Enterprise Co.

- IBM Corp.

- Infosys Ltd.

- Kyndryl Inc.

- NTT DATA Corp.

- Rackspace Technology Inc.

- ScienceSoft USA Corp.

- Tata Consultancy Services

- Tech Mahindra Ltd.

- Unisys Corp.

- Wipro Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Managed services market

- In June 2025, NWN Holdings announced the strategic acquisition of InterVision Systems to bolster its position in the AI-powered managed services sector, integrating advanced AWS-based artificial intelligence and customer experience solutions.

- In March 2025, Globalgig introduced its Premier SSE Management solution, a managed Secure Service Edge platform built on Palo Alto Networks Prisma Access, combining 24/7 security operations center support with deep network intelligence.

- In November 2025, Capgemini completed the acquisition of Cloud4C, a move aimed at enhancing its automation-driven and AI-enabled managed services, particularly for complex SAP migrations and enterprise cloud transformations.

- In May 2026, IBM launched the general availability of IBM Sovereign Core, a software platform designed to help managed service clients build and operate AI-ready sovereign environments with verifiable control over data and infrastructure.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Managed Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 317 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.7% |

| Market growth 2026-2030 | USD 250121.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 11.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The managed services market is fundamentally reshaping enterprise operations by embedding intelligence into its core. The convergence of AIOps and agentic AI is enabling a transition from manual oversight to autonomous, self-healing systems.

- Boardroom decisions are now heavily influenced by the need for digital sovereignty, compelling the adoption of sovereign cloud solutions and a stringent zero trust architecture to mitigate geopolitical and cyber risks. In this landscape, providers are leveraging generative AI and digital twin technologies for advanced application modernization and infrastructure orchestration across complex multi-cloud and edge computing environments.

- Core offerings now center on proactive IT infrastructure management and continuous cybersecurity monitoring, with managed detection and response (MDR) and SASE becoming standard. Expertise in prompt engineering and model governance is a key differentiator.

- The strategic application of predictive analytics within these frameworks has been shown to reduce critical system incidents by over 35%, solidifying the value of proactive, intelligence-driven managed services in achieving operational resilience and promoting workload rightsizing with a focus on endpoint protection and identity governance.

What are the Key Data Covered in this Managed Services Market Research and Growth Report?

-

What is the expected growth of the Managed Services Market between 2026 and 2030?

-

USD 250.12 billion, at a CAGR of 11.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (MDS, MNS, MSS, MMS, and Others), Deployment (Cloud, and On-premises), End-user (Large enterprises, and SMEs) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Transition toward agentic AI and autonomous it service management orchestration, Operational convergence of AI and talent scarcity

-

-

Who are the major players in the Managed Services Market?

-

Accenture Plc, AT and T Inc., Atos SE, Capgemini SE, CGI Inc., Cognizant Technology Solution, DXC Technology Co., Fujitsu Ltd., HCL Technologies Ltd., Hewlett Packard Enterprise Co., IBM Corp., Infosys Ltd., Kyndryl Inc., NTT DATA Corp., Rackspace Technology Inc., ScienceSoft USA Corp., Tata Consultancy Services, Tech Mahindra Ltd., Unisys Corp. and Wipro Ltd.

-

Market Research Insights

- The market is defined by a rapid shift toward intelligent automation and strategic value, with outcome-driven commercial structures replacing traditional contracts. This move toward AI-native service delivery is compelling providers to build AI-enabled global capability centers. Firms leveraging autonomous IT service management report up to a 40% reduction in mean time to resolution, demonstrating clear ROI.

- Concurrently, the adoption of everything-as-a-service models supports business continuity planning and enhances financial flexibility. As enterprises undergo compressed transformations, the ability to deliver on service level agreements through advanced security information and event management and disaster recovery as a service is critical.

- These dynamics show a market where FinOps-driven cloud optimization can reduce cloud spend by 25%, proving the tangible benefits of strategic managed partnerships.

We can help! Our analysts can customize this managed services market research report to meet your requirements.

RIA -

RIA -