Active Optical Cable Market Size 2024-2028

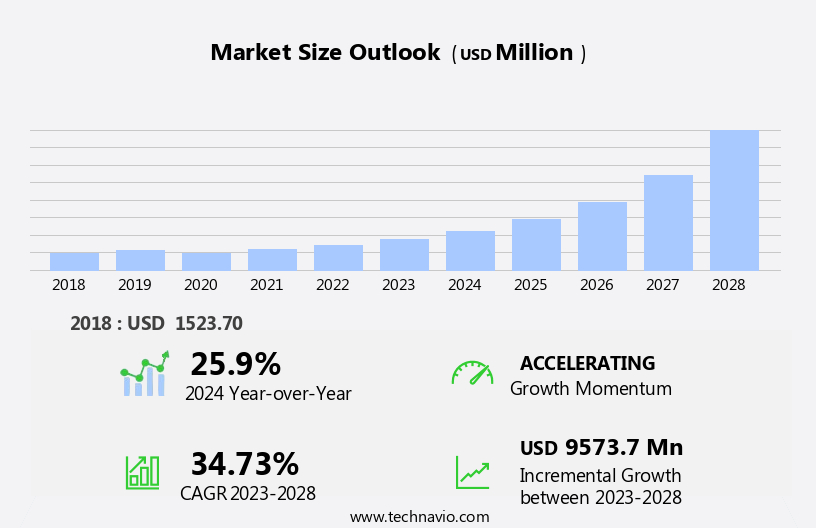

The active optical cable market size is forecast to increase by USD 9.57 billion at a CAGR of 34.73% between 2023 and 2028.

What will be the Size of the Active Optical Cable Market During the Forecast Period?

How is this Active Optical Cable Industry segmented and which is the largest segment?

The active optical cable industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Data center

- Consumer electronics

- High performance computing

- Telecommunication

- Others

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Europe

- Germany

- South America

- Middle East and Africa

- APAC

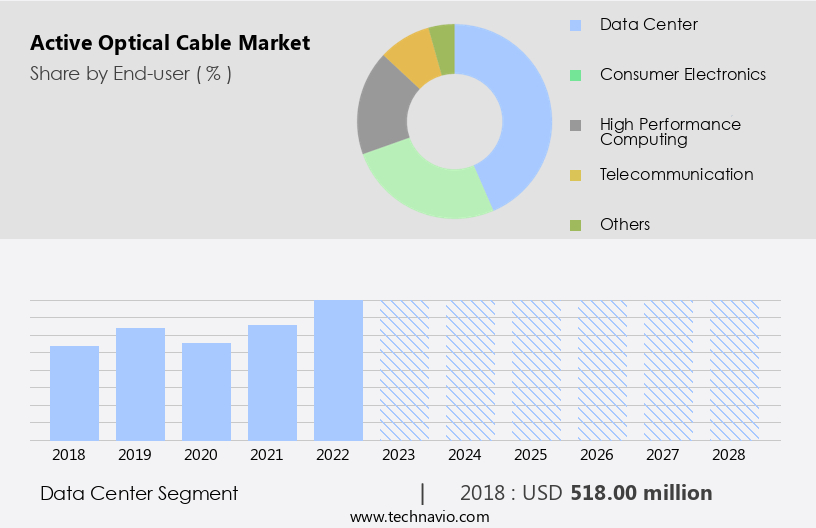

By End-user Insights

- The data center segment is estimated to witness significant growth during the forecast period.

Active optical cables (AOCs) are a crucial component in data center infrastructure, offering high-speed, reliable, and plug-and-play connectivity solutions. The rising trend of data center consolidation, driven by cost savings, enhanced security, and improved efficiency, is fueling the demand for AOCs. Consolidation projects enable enterprises to reduce operating expenses by up to 30%, enhance data security by up to 35%, and improve data transmission efficiency by up to 50%, while reducing power consumption by up to 55%. The shift towards cloud-based services, digitalization, and the deployment of 5G networks are further boosting the demand for AOCs in various sectors, including data centers, high-performance computing, personal computing, digital signage, consumer electronics, and more.

Key segments, such as QSFP, SFP+, and InfiniBand, are expected to dominate the market during the forecast period. AOCs are also gaining traction in industries like military, aerospace, automotive, power plants, oil, gas refineries, telecom, and more, due to their high-performance capabilities and reliability. Technologies like software-defined networking, network-function virtualization, and Ethernet protocols are also driving the market growth.

Get a glance at the Active Optical Cable Industry report of share of various segments Request Free Sample

The Data center segment was valued at USD 518.00 billion in 2018 and showed a gradual increase during the forecast period.

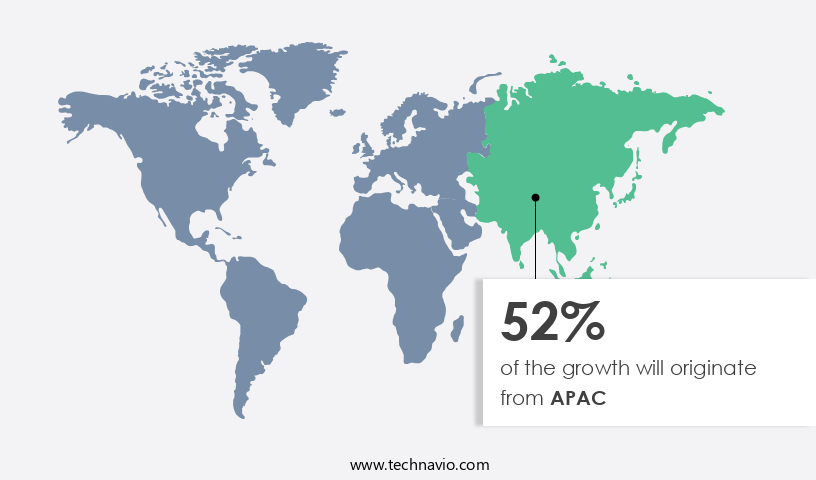

Regional Analysis

- APAC is estimated to contribute 52% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market In the Asia Pacific region is experiencing growth due to the expanding telecom sector and the focus on digitalization in developing countries like India and China. The deployment of active optical cable technology is essential for the smooth functioning of cloud-based services, which are increasingly being adopted. Telecom service providers are investing heavily in active optical cables to meet the growing demand for high-speed data transmission. The market in APAC is anticipated to expand significantly during the forecast period, driven by the increasing need for advanced connectivity solutions in data centers, 5G networks, and various end-user industries, including high-performance computing, personal computing, digital signage, consumer electronics, and professional audio, video applications.

Additionally, sectors such as military, aerospace, automotive, power plants, oil, gas refineries, and telecom are also adopting active optical cable technology for their high-speed data transmission requirements. The technology's advantages, including its smaller form factor, lower power consumption, and higher bandwidth, make it a preferred choice for various applications. Active optical cable is also being used in various industries, including medical imaging, Internet of Things, FTTH, remote radio heads, distributed antenna systems, metro, and long-haul networks, high-resolution displays, televisions, monitors, projectors, gaming consoles, home theatre systems, augmented and virtual reality, and Quad small form-factor pluggable (QSFP), Small form-factor pluggable plus (SFP+), and InfiniBand segments.

The market is expected to continue growing due to the increasing demand for high-speed data transmission and the ongoing digitalization trend.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Active Optical Cable Industry?

Expansion of data centers is the key driver of the market.

What are the market trends shaping the Active Optical Cable Industry?

Adoption of 5G networks is the upcoming market trend.

What challenges does the Active Optical Cable Industry face during its growth?

Complexities involved in wired communication networks is a key challenge affecting the industry growth.

Exclusive Customer Landscape

The active optical cable market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the active optical cable market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, active optical cable market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

3M Co. - Active optical cables are lightweight and flexible solutions engineered for high-performance computing clusters and high-speed servers. These cables offer superior data transfer rates and are routable, making them an ideal choice for data center applications. With their ability to support high bandwidth and low latency, active optical cables are essential for powering today's data-intensive workloads. The technology behind these cables enables longer transmission distances and reduced power consumption compared to traditional copper cables. By delivering unmatched performance and reliability, active optical cables are a crucial investment for organizations seeking to optimize their data infrastructure.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- Amphenol Corp.

- Broadcom Inc.

- Emcore Corp.

- Fujikura Co. Ltd.

- Fujitsu Ltd.

- GIGALIGHT

- Hitachi Ltd.

- International Business Machines Corp.

- II VI Inc.

- Koch Industries Inc.

- Leoni AG

- Lumentum Holdings Inc.

- Optomind Inc.

- SANWA DENKI KOGYO Co.Ltd.

- Sopto Technology Co. Ltd.

- Sumitomo Electric Industries Ltd.

- TE Connectivity Ltd.

- The Siemon Co.

- Yangtze Optical Fibre and Cable Joint Stock Ltd. Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Active optical cables (AOCs) have emerged as a significant alternative to traditional copper cables in various industries due to their ability to provide high-speed data transfer and improved bandwidth efficiency. The market is driven by the increasing demand for cloud-based services, digitalization, and the deployment of 5G networks. AOCs utilize fiber optic technology, which is based on the transmission of light signals through optical fibers. This technology offers several advantages over copper cables, including longer transmission distances, higher bandwidth, and lower power consumption. The QSFP segment, SFP+ segment, and Infiniband segment are key market categories that are expected to witness substantial growth due to their application in high-performance computing, data centers, and telecommunication networks.

The technology behind AOCs comprises several components, including laser diodes, optical fibers, control circuitry, insulating materials, connectors, and housing. The use of photodiodes and telecommunication networks further enhances the capabilities of AOCs, making them suitable for professional audio, video applications, and medical imaging systems. The market for active optical cables is diverse and spans various sectors, including data centers, military, aerospace, automotive, power plants, oil, gas refineries, telecom, and consumer electronics. In the data center sector, AOCs are increasingly being adopted for high-performance computing, personal computing, and software-defined networking applications. In the telecom sector, AOCs are used to build metro, long-haul networks, and remote radio heads, while In the consumer electronics sector, they are used for high-resolution displays, televisions, monitors, projectors, gaming consoles, and home theatre systems.

The market for active optical cables is also driven by the increasing adoption of augmented and virtual reality technologies, which require high-speed data transfer and low latency. The use of AOCs in unmanned aerospace vehicles, satellite communications, and avionics systems is another significant application area that is expected to fuel market growth. The market dynamics of active optical cables are influenced by several factors, including technological advancements, regulatory frameworks, and economic conditions. The ongoing trend towards digitalization and the increasing demand for high-speed data transfer are key growth drivers. However, the market is also facing challenges such as high production costs and the availability of alternative solutions.

In conclusion, the market is a dynamic and growing industry that is driven by the increasing demand for high-speed data transfer and digitalization. The market is expected to witness significant growth In the coming years, with applications spanning various sectors, including data centers, telecom, military, aerospace, and consumer electronics. The technology behind AOCs is continually evolving, with advancements in fiber optics technology, laser diodes, and control circuitry expected to further enhance the capabilities of AOCs.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

145 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 34.73% |

|

Market growth 2024-2028 |

USD 9573.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

25.9 |

|

Key countries |

China, US, Japan, South Korea, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Active Optical Cable Market Research and Growth Report?

- CAGR of the Active Optical Cable industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the active optical cable market growth of industry companies

We can help! Our analysts can customize this active optical cable market research report to meet your requirements.

RIA -

RIA -