Advanced High Strength Steel Market Size 2024-2028

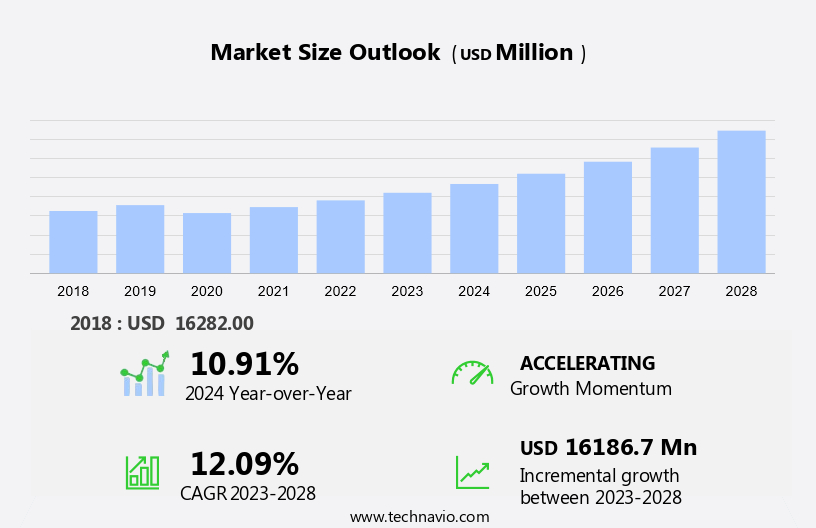

The advanced high strength steel market size is forecast to increase by USD 16.18 billion at a CAGR of 12.09% between 2023 and 2028. The market is experiencing significant growth, driven primarily by the increasing demand for AHSS in the automotive production sector. According to the International Trade Administration, prominent automakers are investing heavily in greenfield projects to expand their production capacity of AHSS. Mechanical properties such as high strength, formability, and lightweight characteristics make AHSS an ideal choice for automotive manufacturers to reduce vehicle weight and improve fuel efficiency. However, the market faces challenges due to the volatile prices of raw materials, particularly iron ore, which can impact the profitability of AHSS producers. The wind energy sector is another emerging application area for AHSS, offering potential growth opportunities. Despite these challenges, the market is expected to continue its upward trajectory, driven by the growing demand for lightweight and fuel-efficient vehicles.

Advanced High-Strength Steels (AHSS) have gained significant attention in various industries due to their superior mechanical properties and weight-reduction capabilities. These steels offer enhanced yield strength and tensile strength, making them ideal for use in lightweight structures, such as rail coach building and automotive parts. The environmental benefits of AHSS are noteworthy, as they contribute to reducing carbon emissions during production and use. Green field investments in advanced high strength steels (AHSS) are crucial for meeting the increasing demand from electric and hybrid vehicles, as companies like Continental Automotive focus on developing third generation steel and aluminum with superior ductility properties and minimum tensile strength. Understanding the nomenclature consideration considerations and each grade's minimum yield strength is essential for ensuring compliance with AHSS specifications and identifying investment pockets in the market. In the construction sector, AHSS is used in active structures, solar heating systems, and roofing systems, leading to energy savings and reduced environmental impact. The steel industry has seen a shift towards third-generation steels, which offer improved mechanical properties and reduced weight.

Furthermore, raw materials, including iron ore prices, play a crucial role in the production of High strength low alloy steels . Regulations governing steel industry emissions continue to evolve, further driving the demand for lightweight and strong AHSS. AHSS grades are used extensively in the automotive industry for manufacturing lightweight components, leading to fuel efficiency and reduced carbon emissions. In the maritime sector, vessel manufacturers use AHSS for building lightweight and strong vessels, ensuring safety and efficiency. Solar panels and other renewable energy systems also benefit from the use of AHSS, as they require lightweight yet strong materials for their construction. Overall, the market for advanced high-strength steels is expected to grow significantly due to their environmental benefits, improved mechanical properties, and weight reduction capabilities.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD Billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Grade Type

- Dual phase

- Complex phase

- Transformation-induced plasticity

- Others

- End-user

- Automobile

- Construction

- Aviation and marine

- Others

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Europe

- Germany

- South America

- Middle East and Africa

- APAC

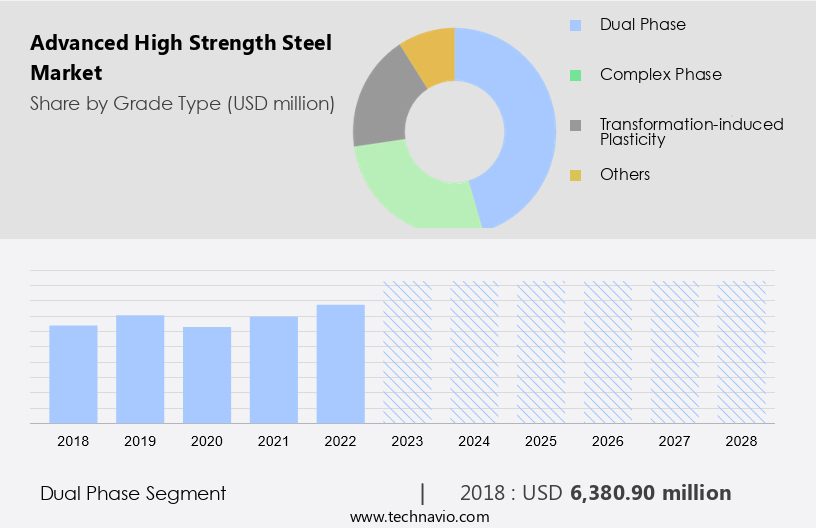

By Grade Type Insights

The dual phase segment is estimated to witness significant growth during the forecast period. It is a class of materials that includes dual-phase (DP steels). Low- to medium-carbon having between 5% and 50% volume fractional martensitic islands that are scattered across a soft ferrite matrix is known as ferrite-martensite dual-phase. There may also be bainite and retained austenite components in addition to martensite; these are typically formed when greater edge stretch formability is sought. Dual-phase has a wide range of strength and ductility due to these changes in microstructure. It is well known to have a high energy absorption capacity. These features make it extremely desirable for automotive applications, especially when combined with a cheap production cost.

Furthermore, It has a high-strain redistribution capacity due to its high-strain hardenability. This translates to better drivability and mechanical qualities (yield strengths) of the completed item that are higher than the blank. In addition, offers a key advantage over traditional HSLA-type materials in the form of bake hardening. The bake hardening effect is an increase in yield strength brought on by the curing temperature of the paint bake cycle, which results in enhanced temperature aging. Such wide benefits are expected to drive the growth of the segment in the global AHSS market during the forecast period.

Get a glance at the market share of various segments Request Free Sample

The Dual phase segment was valued at USD 6.38 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

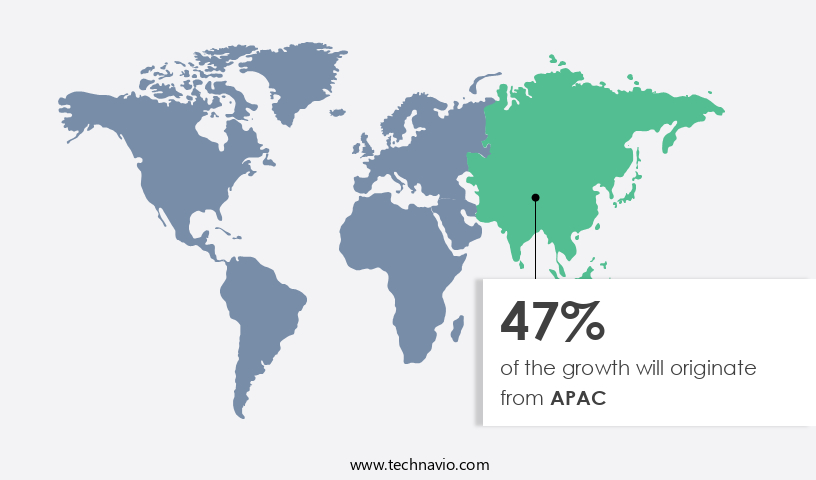

APAC is estimated to contribute 47% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

Advanced High Strength Steel (AHSS) is experiencing significant demand in various industries, particularly in roofing systems and automotive parts. The tech hubs of Silicon Valley and other tech companies are increasingly adopting AHSS due to its weight reduction properties. In the construction sector, APAC is the leading market due to the region's rapid industrialization and infrastructure development. Government investments in countries like China, India, Malaysia, and Vietnam are driving the construction of new roads, residential buildings, bridges, and railways. These projects require sustainable structures, leading to an increased demand for AHSS. Notable projects in the region, such as Oita Stadium, Kamaishi Recovery Memorial Stadium, Shinkansen bullet trains, Central-Wan Chai Bypass-Eastern Corridor Link, Map Ta Phut Industrial Port, and Kyaukpyu Deep Sea Port, have all utilized AHSS in their construction.

Furthermore, the automotive industry is also embracing AHSS for its strength and lightweight properties, resulting in weight reduction and improved fuel efficiency. H2 Green Steel is another emerging trend in the AHSS market, offering a more sustainable production process.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The growing demand for AHSS in automobile industry is the key driver of the market. Advanced High Strength Steel (AHSS), a type of micro-alloyed steel, exhibits a yield strength ranging from 700 to 2,000 N/mm2. This steel is manufactured using the continuous annealing process, which grants it desirable mechanical properties such as strength, toughness, formability, and weldability. The utilization of AHSS is widespread in the automotive, aviation, construction, and energy industries due to its superior mechanical properties and enhanced resistance to atmospheric corrosion compared to conventional carbon steels. In the automobile sector, AHSS is employed to fabricate lightweight and fuel-efficient vehicles. Its application includes the production of frame structures, bumpers, chassis, fuel tank guards, and other automobile components.

Furthermore, the environmental benefits of using AHSS are significant, as it contributes to reducing vehicle weight and subsequently lowers fuel consumption. Moreover, AHSS finds extensive use in rail coach building, offering increased safety and durability. In the energy sector, AHSS is utilized in the manufacturing of solar heating systems and solar panel frames due to its excellent strength-to-weight ratio. Active structures, such as bridges and buildings, also benefit from the use of AHSS, as it enhances their structural integrity and resistance to external forces.

Market Trends

The rising demand in the wind energy sector is the upcoming trend in the market. The global market for Advanced High Strength Steel (AHSS) is witnessing significant growth due to its lightweight properties and the increasing demand for environmental sustainability. AHSS is increasingly being used in various industries, including rail coach building and solar energy, to reduce carbon emissions and promote renewable energy sources. In the rail industry, AHSS is used to manufacture lightweight and durable train components, thereby reducing the overall weight of the train and improving fuel efficiency. Moreover, in the solar energy sector, AHSS is being utilized in the production of solar heating systems and solar panel frames. The environmental benefits of renewable energy sources, coupled with government investments in this sector, are driving the demand for AHSS in solar energy applications.

Furthermore, this growth in renewable energy is further fueling the demand for AHSS in active structures such as wind turbines and solar panel frames. AHSS is also being used in the production of third-generation solar panels, which are more efficient and have a higher power-to-weight ratio compared to traditional solar panels. The use of AHSS in these advanced solar panels not only reduces their weight but also enhances their durability and structural integrity. Overall, the growing demand for renewable energy and the environmental benefits of using lightweight materials are driving the growth of the market.

Market Challenge

The volatile prices of raw materials is a key challenge affecting the market growth. Advanced High Strength Steel (AHSS) is a lightweight and high-performance steel variant, gaining significant traction in various industries due to its environmental benefits and improved structural performance. AHSS is increasingly being used in rail coach building, third-generation solar heating systems, and solar panel manufacturing. The environmental effects of AHSS are noteworthy, as its use leads to reduced fuel consumption and lower carbon emissions. In the rail industry, AHSS is employed in active structures, enhancing safety and durability.

However, the production of AHSS involves the use of crude steel, which is primarily derived from iron ore. The prices of iron ore have been volatile, causing fluctuations in the prices of crude steel and finished AHSS products. Mining disruptions in major iron ore-producing countries like Australia and Brazil have further exacerbated these price swings. Despite these challenges, the demand for AHSS remains strong in industries seeking to improve fuel efficiency, reduce emissions, and enhance structural performance.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Arcelor Mittal - The company offers advanced high-strength steel such as SIRIUS 310S, UR 317LMN, VIRGO 39, UREA 310 MoLN.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ArcelorMittal SA

- Baosteel Group Corp.

- Big River Steel LLC

- China Steel Corp.

- Cleveland Cliffs Inc.

- HBIS Group Co. Ltd.

- Hyundai Motor Group

- JFE Holdings Inc.

- JSW Group

- MSP Steel and Power Ltd.

- Nippon Steel Corp.

- Nucor Corp.

- POSCO holdings Inc.

- Rashtriya Ispat Nigam Ltd.

- SSAB AB

- Steel Technologies LLC

- Tata Steel

- thyssenkrupp AG

- United States Steel Corp.

- voestalpine AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Advanced High-Strength Steels (AHSS) have gained significant attention in various industries due to their superior mechanical properties and weight-reduction capabilities. These steels offer high yield strength and tensile strength, making them ideal for use in automotive parts, rail coach building, and active structures. The market for AHSS is driven by the demand for lightweight components in automotive production and the need for environmental effects mitigation in various industries. AHSS are available in different grades, including dual phase steel and martensitic steels. The mechanical properties of AHSS vary depending on the metallurgical type and specifications. The production of AHSS involves the use of raw materials such as iron ore and silicon, which are subject to international trade administration regulations.

Furthermore, the automotive industry is a significant investment pocket for AHSS, with prominent automakers investing in greenfield projects to increase production capacity. The use of AHSS in automotive parts results in weight reduction, which in turn leads to reduced carbon emissions. The solar heating systems and roofing systems industries also use AHSS for weight reduction and improved strength. The steel industry regulations regarding carbon emissions have led to the development of third-generation steels such as giga steels and ultra-high strength steels. These steels offer even higher strength numbers than AHSS and are used in vessel manufacturing and other applications where extreme strength is required. Informal discussions between tech companies in Silicon Valley and steel manufacturers are ongoing to explore the potential use of AHSS in advanced technologies such as solar panels and other renewable energy applications. The future of AHSS looks promising as the demand for lightweight and strong materials continues to grow.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

189 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 12.09% |

|

Market growth 2024-2028 |

USD 16.18 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

10.91 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 47% |

|

Key countries |

China, US, India, Germany, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ArcelorMittal SA, Baosteel Group Corp., Big River Steel LLC, China Steel Corp., Cleveland Cliffs Inc., HBIS Group Co. Ltd., Hyundai Motor Group, JFE Holdings Inc., JSW Group, MSP Steel and Power Ltd., Nippon Steel Corp., Nucor Corp., POSCO holdings Inc., Rashtriya Ispat Nigam Ltd., SSAB AB, Steel Technologies LLC, Tata Steel, thyssenkrupp AG, United States Steel Corp., and voestalpine AG |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -