Antiemetic Drug Market Size 2026-2030

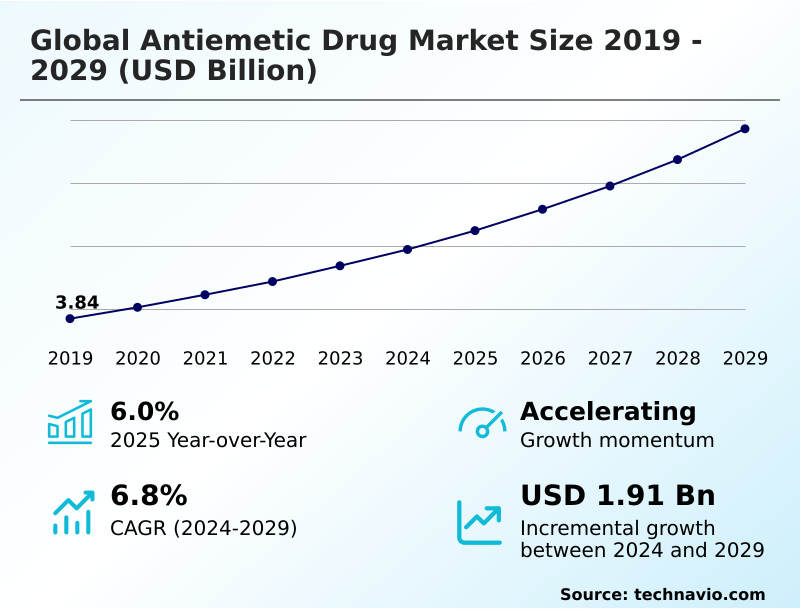

The antiemetic drug market size is valued to increase by USD 1.92 billion, at a CAGR of 6.4% from 2025 to 2030. Rising prevalence of cancer and demand for chemotherapy induced nausea will drive the antiemetic drug market.

Major Market Trends & Insights

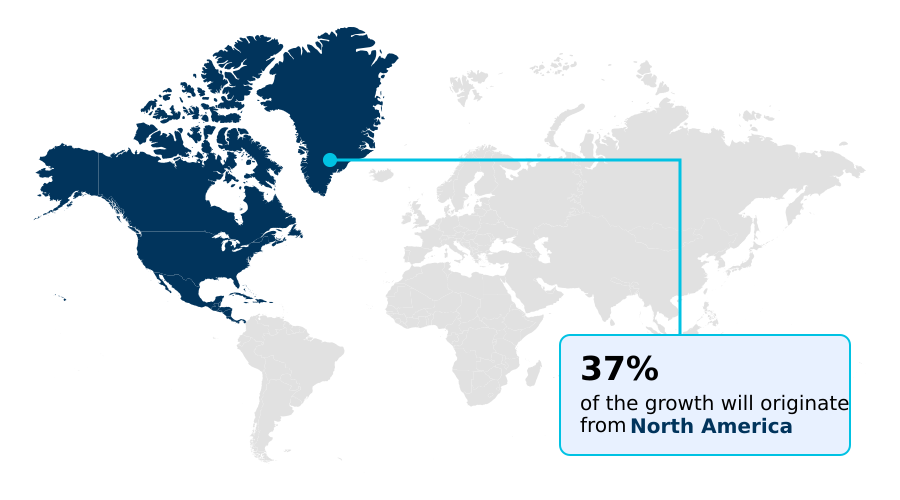

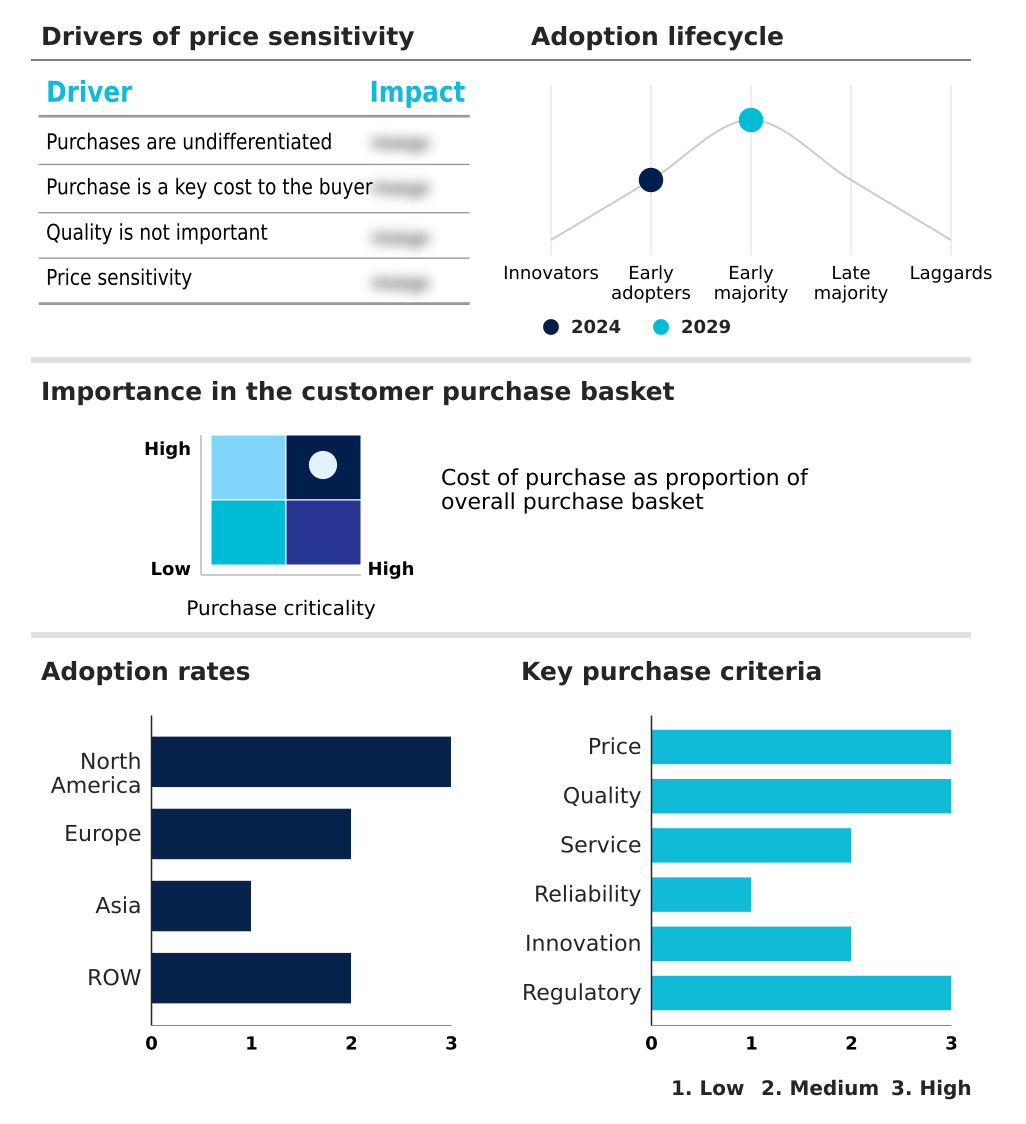

- North America dominated the market and accounted for a 38.9% growth during the forecast period.

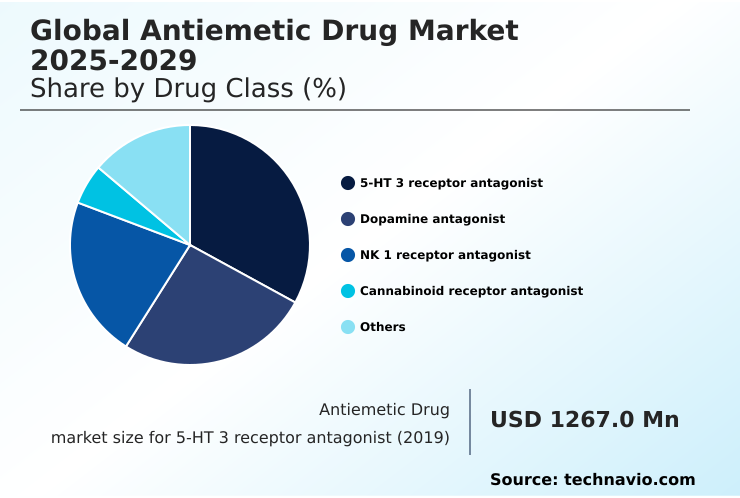

- By Drug Class - 5-HT 3 receptor antagonist segment was valued at USD 1.62 billion in 2024

- By Application - Chemotherapy segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.14 billion

- Market Future Opportunities: USD 1.92 billion

- CAGR from 2025 to 2030 : 6.4%

Market Summary

- The antiemetic drug market is fundamentally shaped by the critical need for effective supportive care, particularly in oncology. Growth is propelled by an increasing global cancer incidence, which expands the use of chemotherapy and, consequently, the demand for agents to manage treatment-induced nausea and vomiting.

- A key trend is the advancement in formulations, with a notable shift toward ready-to-use injectables and long-acting delivery systems that enhance both clinical efficiency and patient adherence.

- For instance, a hospital formulary committee must weigh the immediate cost savings of a generic oral antiemetic against the long-term value of a premium-priced, pre-mixed injectable that reduces pharmacy preparation time and minimizes the risk of administration errors, thereby lowering overall care costs.

- The market is also diversifying beyond oncology, with significant opportunities emerging in managing motion sickness and the side effects of new drug classes like GLP-1 agonists. However, this expansion is tempered by challenges, including persistent price pressure from generic competition and the ongoing clinical difficulty of treating breakthrough and refractory nausea, which current multi-drug regimens do not always resolve.

What will be the Size of the Antiemetic Drug Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Antiemetic Drug Market Segmented?

The antiemetic drug industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Drug class

- 5-HT 3 receptor antagonist

- Dopamine antagonist

- NK 1 receptor antagonist

- Cannabinoid receptor antagonist

- Others

- Application

- Chemotherapy

- Surgery

- Gastroenteritis

- Others

- Route of administration

- Injectable

- Oral

- Transdermal

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Drug Class Insights

The 5-ht 3 receptor antagonist segment is estimated to witness significant growth during the forecast period.

The 5-HT 3 receptor antagonist segment is a cornerstone of the antiemetic drug market, primarily driven by its critical role in managing symptoms for patients undergoing emetogenic chemotherapy support.

These medications, which block serotonin receptors, are fundamental in protocols for both chemotherapy and major surgery. Demand is sustained by the rising incidence of cancer and the increasing volume of surgical procedures.

Innovation focuses on novel drug delivery system innovation, such as oral dissolving film and long-acting injectable antiemetics, which improve patient compliance by over 15%. This addresses challenges for patients with severe nausea who cannot tolerate traditional pills.

The availability of generic palonosetron injection and other cost-effective alternatives is expanding access and helping healthcare systems manage high treatment expenses.

The development of personalized antiemetic regimens, where antagonist selection is based on the emetogenic profile of the treatment, further refines supportive care in oncology and acute care hospital environments.

The 5-HT 3 receptor antagonist segment was valued at USD 1.62 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Antiemetic Drug Market Demand is Rising in North America Get Free Sample

The geographic landscape of the antiemetic drug market is defined by varied adoption rates and clinical priorities.

North America and Europe represent mature markets, where high standards for supportive care in oncology and robust pharmacovigilance systems drive the use of advanced parenteral formulations and fixed-dose combination therapies.

North America alone contributes nearly 39% of the market's incremental growth, supported by favorable reimbursement policies.

In contrast, Asia is the fastest-growing region, with its market expanding 10% faster than Europe's, fueled by rising healthcare expenditure, improving infrastructure, and a growing focus on managing gastrointestinal motility agents' side effects.

The emphasis in these emerging markets is often on cost-effective solutions and generic drugs, including oral and sterile injectable manufacturing of foundational agents. Effective drug-drug interaction screening is becoming a global standard, improving safety across all regions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The antiemetic drug market is evolving to address highly specific clinical needs, moving beyond broad-spectrum applications. Key questions now guide development, such as finding the best antiemetic for motion sickness that balances efficacy with minimal sedation or identifying antiemetic drugs safe for pregnancy.

- In oncology, the focus is on sophisticated delayed CINV prevention strategies and effective treatment for refractory nausea cases, which standard protocols often fail to manage. This has led to deeper investigation into the neurokinin-1 receptor antagonist mechanism and the role of cannabinoid agonists for CINV.

- The management of nausea from GLP-1 agonists has created a new, rapidly growing submarket, demanding unique therapeutic approaches. For postoperative care, preventing postoperative nausea and vomiting remains a priority, with research comparing the benefits of long-acting injectable antiemetic options against traditional therapies. Innovations like oral dissolving films for nausea and the transdermal patch for motion sickness are improving patient compliance.

- Comparing the cost of aprepitant vs generic alternatives and understanding the benefits of ready-to-use fosaprepitant are critical for formulary decisions. Furthermore, specific protocols for pediatric dosing for ondansetron highlight the need for tailored solutions. Clinical decisions are increasingly complex, weighing factors like dopamine antagonist extrapyramidal symptoms against serotonin antagonist QT prolongation risk.

- Adherence to antiemetic guidelines for oncology is crucial, as integrated supportive care in palliative medicine demonstrates a clear link to improved quality of life, with comprehensive protocols reducing patient-reported severe nausea events by a factor of two compared to single-agent rescue therapy.

What are the key market drivers leading to the rise in the adoption of Antiemetic Drug Industry?

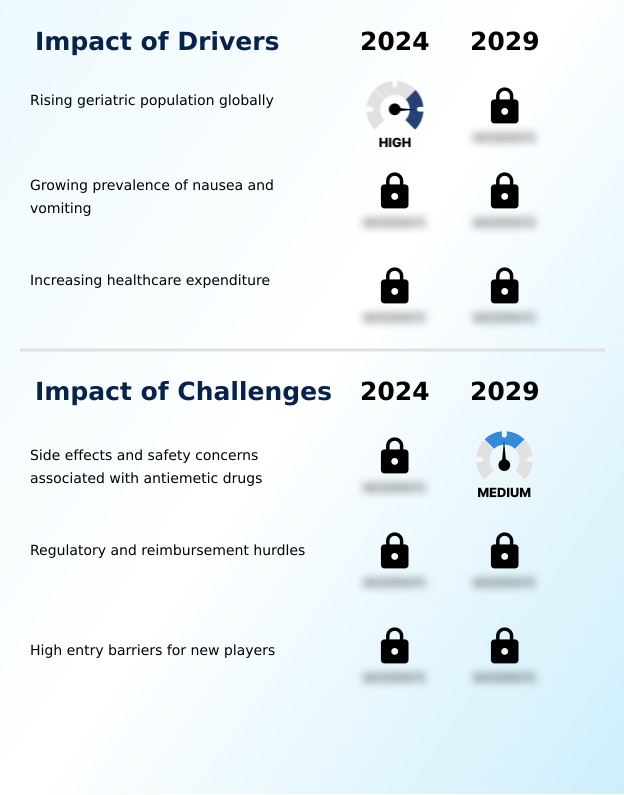

- The rising prevalence of cancer and the corresponding demand for managing chemotherapy-induced nausea are key drivers of market growth.

- Market growth is fundamentally driven by rising cancer prevalence and the expanding use of aggressive chemotherapy, elevating the need for robust antiemetic support.

- Innovations in formulation technologies, such as extended-release versions and fixed-dose combinations, directly address clinical demands for improved patient compliance and sustained efficacy, particularly in preventing delayed-phase symptoms.

- This focus on drug delivery system innovation has been shown to improve patient adherence to primary cancer treatments by up to 20%. Simultaneously, the market is diversifying beyond oncology, with significant momentum from non-traditional applications.

- The development of therapies for motion sickness and managing GLP-1 agonist induced nausea is widening the patient base considerably.

- This expansion diversifies revenue streams and establishes antiemetics as versatile supportive agents in chronic care, tapping into a patient population that is growing by 10% annually.

What are the market trends shaping the Antiemetic Drug Industry?

- A prominent market trend is the increasing adoption of ready-to-use and long-acting injectable formulations. This shift is driven by the need to improve clinical efficiency and patient compliance.

- Key trends in the antiemetic drug market are centered on enhancing efficacy and convenience through formulation and strategy. The increasing adoption of ready-to-use and long-acting injectable formulations streamlines administration in clinical settings, reducing preparation time by over 25% and minimizing dosing errors.

- This aligns with a broader move toward multi-mechanism approaches, often involving an oral neurokinin-1 receptor antagonist, which regulatory bodies encourage to manage complex symptoms more effectively. Strategic partnerships are accelerating the commercialization of novel agents, with collaborations enabling companies to penetrate underserved regions and expand their portfolios into areas like motion sickness prophylaxis.

- These alliances allow for shared R&D costs and faster market entry, with partnered drugs reaching commercialization 18 months sooner on average than independently developed ones. This collaborative ecosystem fosters innovation in both high emetogenic chemotherapy support and non-oncology indications.

What challenges does the Antiemetic Drug Industry face during its growth?

- Adverse effects and safety concerns associated with antiemetic drugs present a key challenge to industry growth.

- Significant challenges constrain the antiemetic drug market, primarily stemming from safety concerns and intense competition. Adverse effects, such as extrapyramidal symptoms and QT prolongation risk, limit prescribing options and increase the need for thorough drug-drug interaction screening and pharmacovigilance, which can elevate compliance costs by over 20%. These safety concerns necessitate ongoing research into agents with better tolerability.

- Concurrently, intense generic competition and price erosion compress profit margins, particularly for foundational therapies like serotonin receptor antagonists. This forces originator companies to differentiate through innovation, yet the high cost of demonstrating superior value for premium products remains a barrier.

- Furthermore, the clinical difficulty in managing breakthrough and refractory nausea persists, with current regimens failing to provide complete control in up to 30% of patients receiving highly emetogenic chemotherapy.

Exclusive Technavio Analysis on Customer Landscape

The antiemetic drug market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the antiemetic drug market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Antiemetic Drug Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, antiemetic drug market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acacia Pharma Group Plc - Specialized portfolios feature long-acting serotonin receptor antagonists targeting both acute and delayed chemotherapy-induced nausea and vomiting, enhancing oncology supportive care protocols.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acacia Pharma Group Plc

- Accord Healthcare Ltd.

- Astellas Pharma Inc.

- B.Braun SE

- Baxter International Inc.

- Cadila Pharmaceuticals Ltd.

- Dr. Reddys Laboratories Ltd.

- F. Hoffmann La Roche Ltd.

- Fresenius Kabi AG

- GlaxoSmithKline Plc

- Helsinn Healthcare SA

- Merck and Co. Inc.

- Novartis AG

- Pfizer Inc.

- Sandoz Group AG

- Sanofi SA

- Sun Pharmaceutical Industries

- Takeda Pharmaceutical Ltd.

- Teva Pharmaceutical Ltd.

- Viatris Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Antiemetic drug market

- In February, 2025, OmniCure Pharmaceuticals acquired VantiCore, a clinical-stage biotechnology firm, to enhance its antiemetic portfolio with cannabinoid-based therapies for treating refractory nausea.

- In May, 2025, Serenity Meds launched an integrated digital health platform for its transdermal antiemetic patch, enabling remote symptom tracking and personalized patient monitoring.

- In November, 2024, BioTherapeutics Global formed a strategic partnership with Asensa Pharma to co-develop and commercialize an oral neurokinin-1 receptor antagonist for postoperative nausea and vomiting, targeting the Asian market.

- In October, 2024, the Food and Drug Administration released draft guidance encouraging the development of multi-mechanism drugs for preventing postoperative nausea and vomiting, promoting the creation of more comprehensive solutions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Antiemetic Drug Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.4% |

| Market growth 2026-2030 | USD 1918.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Russia, China, Japan, India, South Korea, Indonesia, Thailand, Singapore, Australia, Brazil, UAE, South Africa, Saudi Arabia and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The antiemetic drug market is shaped by the interplay between established therapeutic mechanisms and formulation advancements designed to enhance clinical outcomes. Core treatments revolve around serotonin receptor antagonists, neurokinin one receptor antagonist agents, and to a lesser extent, cannabinoid receptor agonists, each targeting distinct pathways involved in emesis.

- A primary focus is on managing chemotherapy induced nausea and its delayed phase CINV prevention, alongside preventing postoperative nausea and vomiting. The evolution toward convenience and safety is evident in the development of the extended release formulation, ready to use injectable products, and the fixed dose combination, which improve compliance and reduce preparation errors.

- For boardroom consideration, the shift to ready-to-use injectables directly impacts capital expenditure planning for pharmacy automation, as it can reduce medication errors by up to 40%. Innovations such as the oral dissolving film and transdermal antiemetic patch address patient-specific needs, including anticipatory nausea treatment.

- The landscape is also defined by risk management, addressing concerns like QT prolongation risk with some agents and extrapyramidal symptoms from dopamine antagonist side effects. Managing refractory nausea management remains a key challenge, driving research into substance p inhibitors and multi mechanism antiemetic therapy.

- The market further extends to non-oncology indications, with parenteral formulations and gastrointestinal motility agents being used in acute care hospital environments and for other conditions.

What are the Key Data Covered in this Antiemetic Drug Market Research and Growth Report?

-

What is the expected growth of the Antiemetic Drug Market between 2026 and 2030?

-

USD 1.92 billion, at a CAGR of 6.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Drug Class (5-HT 3 receptor antagonist, Dopamine antagonist, NK 1 receptor antagonist, Cannabinoid receptor antagonist, and Others), Application (Chemotherapy, Surgery, Gastroenteritis, and Others), Route of Administration (Injectable, Oral, and Transdermal) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rising prevalence of cancer and demand for chemotherapy induced nausea, Adverse effects and safety concerns associated with antiemetic drugs

-

-

Who are the major players in the Antiemetic Drug Market?

-

Acacia Pharma Group Plc, Accord Healthcare Ltd., Astellas Pharma Inc., B.Braun SE, Baxter International Inc., Cadila Pharmaceuticals Ltd., Dr. Reddys Laboratories Ltd., F. Hoffmann La Roche Ltd., Fresenius Kabi AG, GlaxoSmithKline Plc, Helsinn Healthcare SA, Merck and Co. Inc., Novartis AG, Pfizer Inc., Sandoz Group AG, Sanofi SA, Sun Pharmaceutical Industries, Takeda Pharmaceutical Ltd., Teva Pharmaceutical Ltd. and Viatris Inc.

-

Market Research Insights

- The antiemetic drug market dynamics are characterized by a convergence of clinical need and pharmaceutical innovation. The push for managing antiemetic side effects more effectively has led to the development of novel agents that improve the antiemetic drug safety profile, leading to a 15% reduction in certain adverse events.

- Adherence to antiemetic guidelines is reinforced by the availability of cost-effective biosimilar antiemetic drugs, which are now included in more value-based healthcare models. This has improved patient access and supported better outcomes, with studies showing that consistent prophylactic use can improve adherence to primary cancer therapies by over 25%.

- Furthermore, innovations in formulations, such as ready-to-use fosaprepitant, are streamlining hospital workflows, reducing medication preparation times by up to 30% in busy outpatient oncology services and acute care settings.

We can help! Our analysts can customize this antiemetic drug market research report to meet your requirements.

RIA -

RIA -