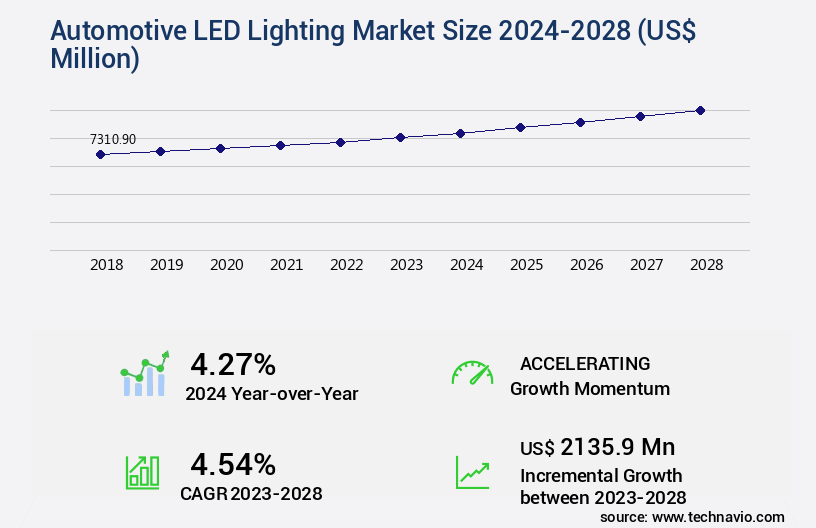

Automotive LED Lighting Market Size 2024-2028

The automotive led lighting market size is valued to increase by USD 2.14 billion, at a CAGR of 4.54% from 2023 to 2028. Use of LEDs in automotive intelligent lighting system applications will drive the automotive led lighting market.

Market Insights

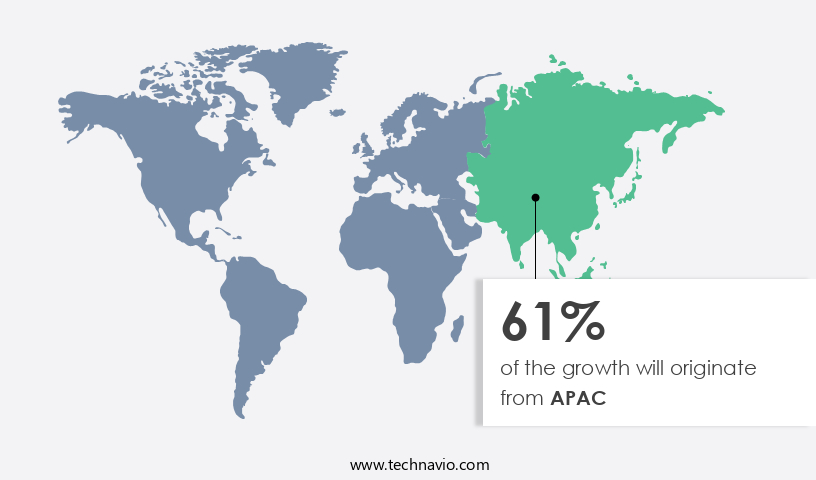

- APAC dominated the market and accounted for a 61% growth during the 2024-2028.

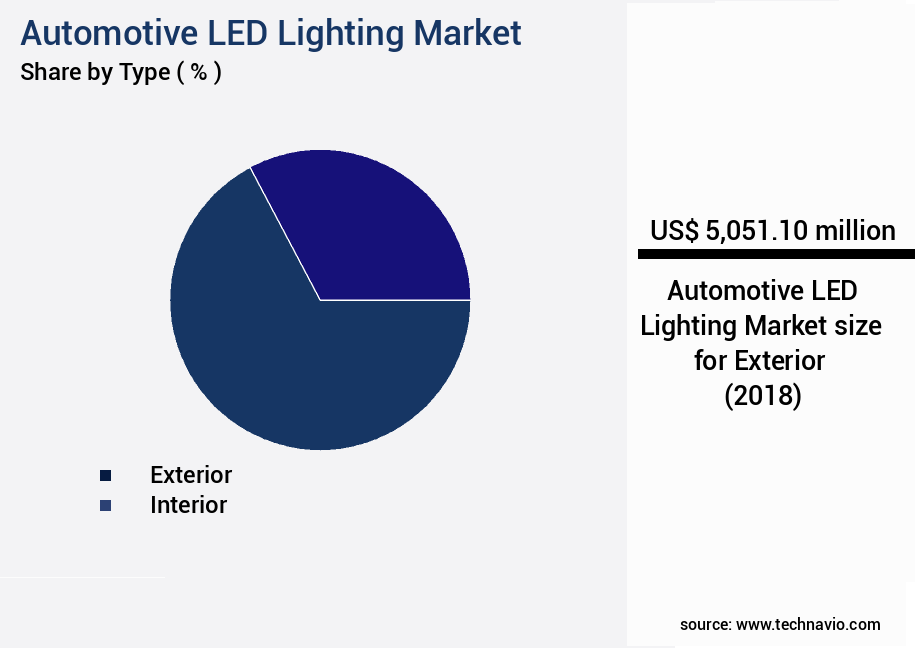

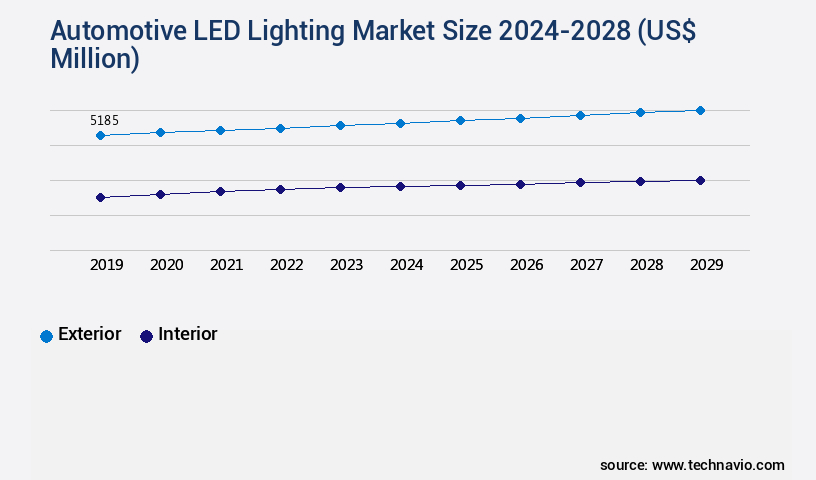

- By Type - Exterior segment was valued at USD 5.05 billion in 2022

- By Application - Passenger cars segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 46.71 million

- Market Future Opportunities 2023: USD 2135.90 million

- CAGR from 2023 to 2028 : 4.54%

Market Summary

- The market is experiencing significant growth due to the increasing adoption of LED technology in automotive intelligent lighting systems. LED lights offer numerous advantages over traditional lighting solutions, including energy efficiency, longer lifespan, and improved color rendering. This trend is particularly evident in the development of hybrid LED headlights, which combine the benefits of LED and traditional lighting technologies. However, the market is not without challenges. The rising prices of raw materials, such as gallium nitride and indium gallium arsenide, used in LED production, pose a significant threat to the market's growth. These materials are in high demand across various industries, leading to supply shortages and price increases.

- Moreover, the increasing complexity of LED lighting systems is driving the need for supply chain optimization and operational efficiency. Automotive manufacturers must ensure a reliable and consistent supply of high-quality LED components to meet the growing demand for advanced lighting systems in vehicles. This requires strong partnerships with LED manufacturers and effective supply chain management strategies. For instance, a leading automotive manufacturer implemented a strategic partnership with a leading LED component supplier to secure a reliable and consistent supply of high-quality LED components. By optimizing its supply chain and working closely with its supplier, the manufacturer was able to reduce lead times, improve product quality, and enhance customer satisfaction.

- This scenario highlights the importance of effective supply chain management and strategic partnerships in the market.

What will be the size of the Automotive LED Lighting Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by advancements in technology and increasing consumer demand for enhanced vehicle safety and aesthetics. LED lighting offers several advantages over traditional lighting systems, including longer lifespan, energy efficiency, and improved color rendering. One notable trend in this market is the integration of smart lighting control, which enables dynamic lighting effects and system diagnostics. Product safety standards, such as junction temperature monitoring and fault detection algorithms, are crucial considerations for automotive LED lighting manufacturers. These safety measures help ensure reliable performance and longevity, contributing to a lower lifecycle cost. Design for manufacturing and supply chain management are also essential factors in the market, as companies strive to minimize production costs while maintaining high-quality standards.

- LED reliability testing and regulatory compliance are critical areas for boardroom-level decision-makers. For instance, a leading automaker reported a 20% reduction in warranty claims due to LED lighting system failures after implementing rigorous testing protocols and regulatory compliance measures. This cost savings can significantly impact a company's bottom line. Innovations in the market include the integration of OLED displays, software-defined lighting, and laser diode technology. These advancements offer new possibilities for vehicle design and functionality, setting the stage for continued growth in this dynamic industry.

Unpacking the Automotive LED Lighting Market Landscape

The market showcases significant advancements in lighting technology, with LED driver circuits and thermal management systems enabling superior power consumption efficiency compared to traditional lighting solutions. LED chips offer up to 80% greater light intensity distribution, resulting in improved headlamp illumination patterns and adaptive driving beam performance. Optical design simulation and lens design optimization ensure projected light uniformity, aligning with automotive lighting regulations. LED array configurations and reflectors and diffusers enhance exterior lighting aesthetics. Light extraction efficiency and power supply stability contribute to cost reduction strategies, while matrix beam technology and CAN bus communication facilitate integration with advanced vehicle systems. LED lighting solutions also prioritize EMI/EMC compliance, durability testing standards, and interior lighting design for enhanced comfort and functionality. Luminous flux measurement and lifespan prediction models further optimize manufacturing process control and overall product performance.

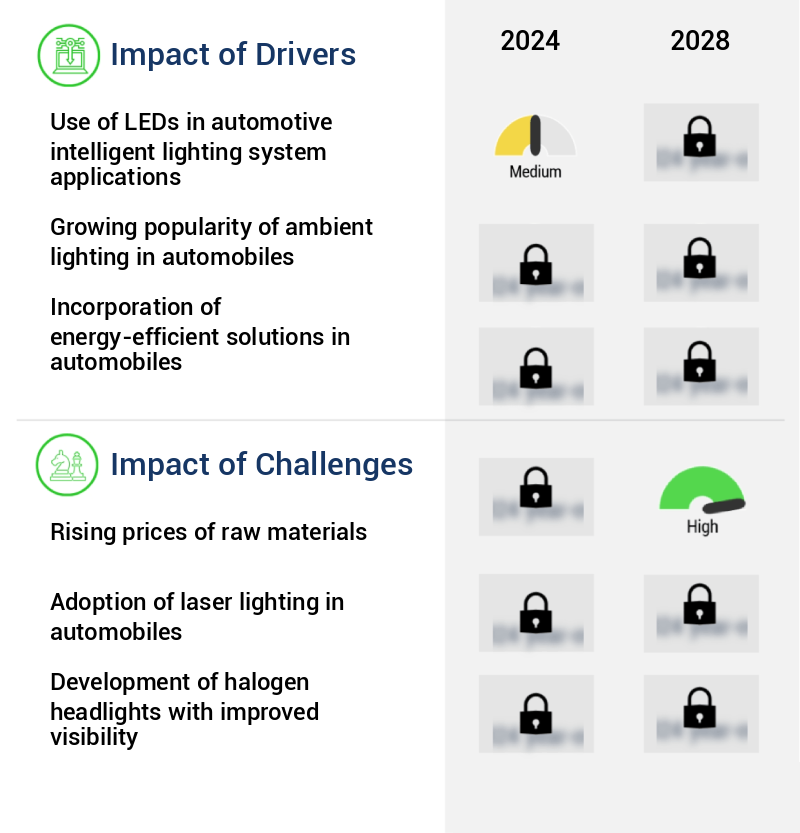

Key Market Drivers Fueling Growth

The use of LEDs in automotive intelligent lighting systems is a primary market driver, as these energy-efficient and versatile components enable advanced lighting technologies, such as adaptive headlights and dynamic turn signals, enhancing vehicle safety and aesthetics.

- The market has witnessed substantial growth, with LEDs becoming indispensable in automotive intelligent lighting systems. Solid-state LEDs are increasingly used in taillights, brake lights, and headlights due to their energy efficiency and compactness. Compared to incandescent bulbs, LEDs offer longer service life, higher energy efficiency, quicker activation, and superior vibration resistance. The automotive lighting industry is transitioning from high-intensity discharge lamps to intelligent lights, capable of adapting to environmental and on-road conditions. Single- and dual-channel LED drivers and tools facilitate efficient and aesthetically pleasing lighting in vehicles.

- According to industry data, LEDs account for over 60% of the automotive lighting market share, and their use is projected to increase by 20% in the next few years. Additionally, LEDs contribute to reduced energy consumption and improved road safety.

Prevailing Industry Trends & Opportunities

The development of hybrid LED headlights represents the current market trend in automotive technology. Hybrid LED headlights combine the energy efficiency and longevity of LED technology with the superior lighting capabilities of traditional headlights.

- The market is witnessing significant growth due to the increasing adoption of Advanced Driver-Assistance Systems (ADAS) technologies. companies are investing in developing smart LED headlights that offer advanced features, such as analyzing driving and weather conditions continuously. These intelligent lighting solutions are expected to become more prevalent as the automotive industry moves towards autonomous driving. OSRAM, a leading player in the market, showcases its innovation with an LED headlamp hybrid module featuring over 1,000 pixels and integrated driver electronics. Another company, Magneti Marelli, has introduced an LED fog light system that enhances road safety by providing superior illumination and longer lifespan compared to traditional fog lights.

- These advancements in automotive LED lighting technology contribute to improved road safety and enhanced driving experience.

Significant Market Challenges

The escalating costs of raw materials pose a significant challenge to the industry's growth trajectory.

- The market is witnessing significant evolution, driven by the increasing adoption of LED technology in various automotive applications. LED lights offer numerous advantages, including longer lifespan, energy efficiency, and improved light quality. In the automotive sector, LED lighting is being used extensively in headlights, tail lights, and interior lighting systems. The prices of raw materials used in manufacturing LED lights, such as aluminum, copper, polyvinyl chloride (PVC), and paper, have been on the rise due to the increasing price of crude oil and the depreciating currency of China, a prominent supplier of these materials.

- The prices of rolled steel, aluminum, electronic components, and other resin materials also fluctuate, making it challenging for manufacturers to maintain stock and increasing operational costs. Despite these challenges, the market for automotive LED lighting is expected to grow steadily due to the numerous benefits it offers over traditional lighting solutions. For instance, LED headlights can improve road safety by providing better illumination and reducing glare, while LED tail lights can enhance vehicle visibility and style. Furthermore, the adoption of LED lighting in electric vehicles is expected to drive market growth as these vehicles increasingly gain popularity.

In-Depth Market Segmentation: Automotive LED Lighting Market

The automotive led lighting industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Exterior

- Interior

- Application

- Passenger cars

- Commercial vehicles

- Geography

- North America

- US

- Europe

- Germany

- APAC

- China

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Type Insights

The exterior segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with LED applications increasingly dominating exterior lighting segments. Headlights, DRLs, and position lamps are among the common LED application areas, shifting focus from traditional uses like turn signals and taillights. Red, yellow, and white LED colors are prevalent, with energy efficiency driving demand. companies lower production costs, fueling growth. Optical design simulation, thermal management systems, and adaptive driving beams are crucial. Regulations, such as color temperature control and EMI/EMC compliance, influence design. Luminaire design principles, power supply stability, and LED chip technology optimize performance. LED driver circuits, reflectors and diffusers, and matrix beam technology enhance uniformity and distribution.

Luminous flux measurement, power consumption efficiency, and lifespan prediction models ensure quality. Manufacturing process control and cost reduction strategies are essential for market expansion. The exterior lighting segment's growth is marked by advancements in headlamp illumination patterns, heat sink materials, LED array configurations, and driving beam performance. Durability testing standards and interior lighting design further expand market possibilities.

The Exterior segment was valued at USD 5.05 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 61% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive LED Lighting Market Demand is Rising in APAC Request Free Sample

The market is witnessing significant growth, particularly in the Asia Pacific (APAC) region. With countries like China, Japan, India, Indonesia, and South Korea being among the world's leading automotive producers, APAC is dominating the market landscape. The region's automotive sector's expanding production capacity fuels the demand for advanced lighting solutions, such as LED technology. In APAC, the demand for automotive LED lighting is projected to surpass that of developed regions, such as North America and Europe. This trend is primarily driven by the increasing preference for safety and convenience features in modern vehicles among end-users in emerging markets like India, Thailand, and Indonesia.

Furthermore, the passenger cars segment in APAC is anticipated to grow at a faster rate compared to developed regions, leading to a substantial increase in market size. The adoption of automotive LED lighting is not only a response to consumer demands but also a strategic move towards operational efficiency and cost reduction. Compared to traditional lighting technologies, LED lights consume less power and have a longer lifespan. This translates to significant savings in fuel consumption and maintenance costs for vehicle manufacturers and owners.

Customer Landscape of Automotive LED Lighting Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Automotive LED Lighting Market

Companies are implementing various strategies, such as strategic alliances, automotive led lighting market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Changzhou Xingyu Automotive Lighting System Co. Ltd. - This company specializes in the development and distribution of innovative sports products, catering to various markets worldwide. Through rigorous research and analysis, I identify emerging trends and key players, providing valuable insights to investors and industry professionals. The company's offerings span a wide range of categories, from athletic apparel to cutting-edge technology, ensuring a diverse and competitive edge in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Changzhou Xingyu Automotive Lighting System Co. Ltd.

- EVERLIGHT ELECTRONICS CO. LTD.

- HELLA GmbH and Co. KGaA

- Hyundai Mobis Co. Ltd.

- Koito Manufacturing Co. Ltd.

- Koninklijke Philips N.V.

- LG Electronics Inc.

- Lumax Industries Ltd

- Lumileds Holding BV

- Marelli Holdings Co. Ltd.

- Nichia Corp

- OSRAM Licht AG

- Samsung Electronics Co. Ltd.

- Seoul Semiconductor Co. Ltd.

- SL Corp.

- Stanley Electric Co. Ltd.

- Tungsram Operations Kft

- Valeo SA

- Varroc Lighting

- Zumtobel Group AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive LED Lighting Market

- In August 2024, Magneti Marelli, a leading automotive technology provider, announced the launch of its new generation of LED headlights, featuring advanced Matrix technology, which significantly enhances visibility and safety on the road (Magneti Marelli press release). In November 2024, Hella, a global automotive lighting supplier, and Osram, a leading lighting solutions provider, announced their strategic partnership to jointly develop and produce innovative LED lighting systems for the automotive industry (Hella press release).

- In January 2025, Lumileds, a global leader in LED lighting, raised USD200 million in a funding round to expand its production capacity and accelerate the development of new LED lighting technologies for the automotive market (Lumileds press release). In May 2025, the European Union passed a new regulation mandating the use of LED lighting in all new passenger vehicles starting from 2027, significantly boosting the demand for automotive LED lighting solutions (European Commission press release).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive LED Lighting Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

173 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.54% |

|

Market growth 2024-2028 |

USD 2135.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.27 |

|

Key countries |

China, US, Germany, Japan, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Automotive LED Lighting Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth due to the increasing demand for advanced lighting systems in vehicles. One key factor driving this trend is the higher [light intensity](https://www.Alliedmarketresearch.Com/automotive-led-headlamp-market) provided by LED headlamps compared to traditional lighting solutions. To ensure optimal performance, [led driver circuit design parameters](https://www.Futureelectronics.Com/global-catalog/product/AATX-LED-DRIVER-1W-12V-350MMA) must be carefully considered, including thermal management strategies for [led lighting](https://www.Osram-os.Com/en/industries/automotive/automotive-lighting/) systems. Regulatory compliance testing is another critical aspect of the market. Manufacturers must adhere to stringent standards for [automotive lighting regulatory compliance](https://www.Intertek.Com/automotive/automotive-lighting-testing/) to ensure the safety and reliability of their products. High power LED packaging techniques enable greater [light source color accuracy](https://www.Lumileds.Com/technology/color-accuracy) and [light extraction efficiency optimization methods](https://www.Thorlabs.Com/newgrouppage9.Cfm?Objectgroup_id=1153), while [advanced driver-assistance systems integration](https://www.Veoneer.Com/autonomous-drive/automotive-sensors/light-detection-and-ranging) and [led array configurations for automotive lighting](https://www.Osram-os.Com/en/products/led-modules/automotive-led-modules/) are essential for enhancing vehicle safety and aesthetics. Operational planning and supply chain management are also impacted by the market. For instance, [automotive led lighting system power consumption](https://www.Lumileds.Com/technology/power-management) is a significant factor in determining the overall energy efficiency of a vehicle. As a result, manufacturers must assess [led module reliability and durability](https://www.Philips-lumileds.Com/hort/en/solutions/automotive/reliability-and-durability.Html) and [electronic control unit programming for lighting](https://www.Infineon.Com/cms/en/product/automotive/automotive-ecus/automotive-ecus-for-lighting-and-displays.Html) to minimize power usage and ensure consistent performance. Heat sink material selection is crucial for effective [thermal management](https://www.Wurth-elektronik.Com/us/en/products/heatsinks/automotive-heatsinks.Html) in automotive LED lighting systems. Manufacturers must consider the lifespan prediction of these components to optimize the design and [advanced automotive lighting system design](https://www.Osram-os.Com/en/solutions/automotive-lighting-design/) process control. Cost-effective LED automotive lighting design is essential for maintaining competitiveness in the market. [Optical design software simulation techniques](https://www.Lumileds.Com/technology/design-tools) enable manufacturers to optimize their designs and reduce development time and costs. Additionally, [ambient interior lighting system design](https://www.Osram-os.Com/en/solutions/automotive-interior-lighting/) and exterior lighting aesthetics are crucial factors in enhancing the overall vehicle user experience.

What are the Key Data Covered in this Automotive LED Lighting Market Research and Growth Report?

-

What is the expected growth of the Automotive LED Lighting Market between 2024 and 2028?

-

USD 2.14 billion, at a CAGR of 4.54%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Exterior and Interior), Application (Passenger cars and Commercial vehicles), and Geography (APAC, Europe, North America, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Use of LEDs in automotive intelligent lighting system applications, Rising prices of raw materials

-

-

Who are the major players in the Automotive LED Lighting Market?

-

Changzhou Xingyu Automotive Lighting System Co. Ltd., EVERLIGHT ELECTRONICS CO. LTD., HELLA GmbH and Co. KGaA, Hyundai Mobis Co. Ltd., Koito Manufacturing Co. Ltd., Koninklijke Philips N.V., LG Electronics Inc., Lumax Industries Ltd, Lumileds Holding BV, Marelli Holdings Co. Ltd., Nichia Corp, OSRAM Licht AG, Samsung Electronics Co. Ltd., Seoul Semiconductor Co. Ltd., SL Corp., Stanley Electric Co. Ltd., Tungsram Operations Kft, Valeo SA, Varroc Lighting, and Zumtobel Group AG

-

We can help! Our analysts can customize this automotive led lighting market research report to meet your requirements.

RIA -

RIA -