Enjoy complimentary customisation on priority with our Enterprise License!

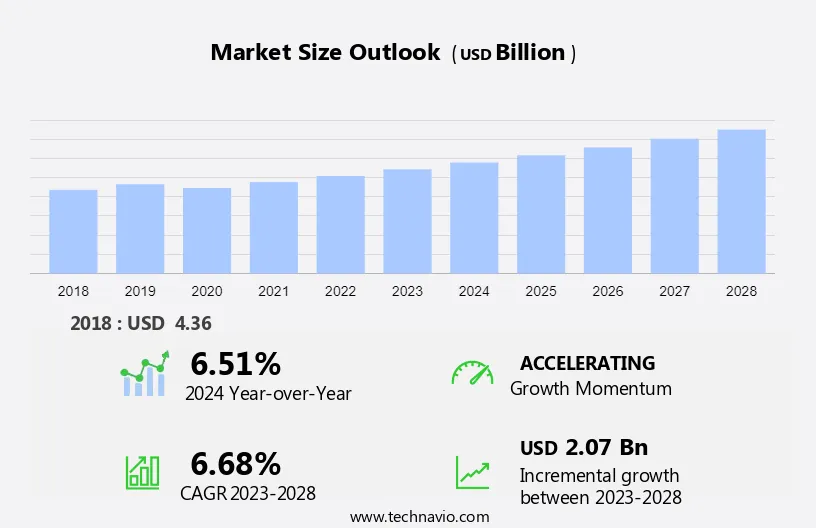

The automotive steering torque sensor market size is forecast to increase by USD 2.07 billion, at a CAGR of 6.68% between 2023 and 2028. Market growth hinges on multiple factors, including widespread EPS system adoption in passenger vehicles (PVs) and light commercial vehicles (LCVs), rising electric vehicle (EV) demand driving the need for automotive steering torque sensors, and the rapid increase in electronic content per vehicle. These dynamics underscore the automotive industry's shift towards advanced electronic systems to enhance vehicle performance and efficiency. With EPS systems becoming ubiquitous in PVs and LCVs, alongside the burgeoning demand for EVs, the automotive sector is experiencing a notable surge in electronic component integration to meet evolving consumer preferences and regulatory standards. The report provides market size, historical data spanning from 2018 - 2022, and future projections, all presented in terms of value in USD billion for each of the mentioned segments.

For More Highlights About this Report, Download Free Sample in a Minute

The market is witnessing remarkable growth driven by advancements in autonomous driving and driver assistance systems for heavy commercial vehicle. These sensors play a critical role in recording and measuring torque within rotating systems, enabling precise collision avoidance systems and optimized turning maneuvers. Utilizing technologies like magnetic sensing, they ensure accurate detection of torsion bar angle and compliance with traffic signs, contributing to safer and more efficient autonomous vehicle operation. Further, autonomous vehicles are revolutionizing the transportation industry, incorporating advanced steering systems and driver assistance systems to navigate turning maneuvers, interpret traffic signs, and ensure safety, particularly in heavy commercial vehicles undergoing electrification. Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Rapidly increasing electronic content per vehicle is the key factor driving the market. Consumer demands and OEM offerings in automotive have expanded to encompass safety, performance, and comfort, necessitating advanced electrification of components over traditional mechanical ones. This shift has propelled the growth of the advanced steering systems like electric power steering (EPS) systems, and electromechanical power steering, surpassing industry growth. With cars viewed as mobility tools, electronic features are vital for product differentiation. Over 90% of car enhancements stem from electronic content, driving the market.

Additionally, Strain gauges play a crucial role in the electronic control unit (ECU) of a vehicle's power steering system, contributing to the integration of autonomous driving technologies and enhancing vehicle safety through automation. If OEMs integrate advanced car features into mid- to low-end models, sensor consumption per car could double. Government regulations mandate features like Advanced driver assistance systems (ADAS), further driving hall-effect sensors demand. These trends will continue to propel market growth during the forecast period.

The rise in demand for wireless connectivity in torque sensors is the primary trend shaping the market. The widespread development of the global economy has pushed the automotive industry across the world to enhance its operational and energy efficiency to cut costs and generate an optimum amount of revenue. To achieve operational and energy efficiency, all processes need to be closely monitored. Wireless systems are used in applications where the conventional torque transducers are not practical due to high shaft speeds, vibrations, and dirty environments.

Additionally, Teledyne Instruments Test Services has developed a non-contact torque sensor to address the challenging application of measuring automotive engine torque. The sensor was developed by customizing and instrumenting the flexplate or flywheel, which connects the engine crankshaft to the torque converter. Owing to the faster adoption of industrial wireless sensor networks (IWSN) in manufacturing industries, it is expected that the demand for wireless torque sensors will increase in the forecast period, which will ultimately drive the market during the forecast period.

Increasing design complexity and escalating manufacturing costs is the major challenge that affects market expansion. Torque sensors are used in a wide range of applications in the automotive industry. Complexity in the design of these sensors is increasing because of the integration of more functions into sensors and the constant and increasing demand from the end-users. Therefore, vendors must focus more on adding new functionalities to microcontroller design to meet the demand from end-users. The increased complexity will increase the cost of the manufacturing process owing to the installation of sophisticated components within the sensors.

Furthermore, industries prefer the miniaturization of components to achieve a reduction in power consumption and the proper utilization of installed space. This miniaturization trend poses a challenge for torque sensor manufacturers, as vendors must develop small sensor-integrated circuits to be incorporated into complex control unit devices. This further increases the complexity of the design of torque sensors. This ultimately results in delays in production schedules and adds to the cost of production, which will be a challenge for market growth during the forecast period.

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market forecast report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report also includes detailed analyses of the competitive landscape of the market and information about 20 market companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

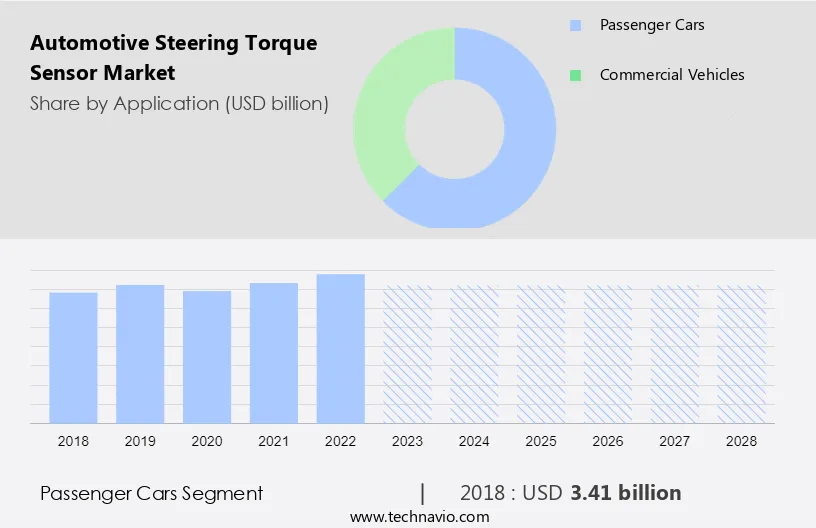

The passenger cars segment is estimated to witness significant growth during the forecast period. The passenger vehicles segment stands as the automotive industry's largest, reflecting economic development, industrial output, and population demographics. With strong demand from developing countries and revived economies, this segment is projected to retain its lead. APAC is anticipated to emerge as a key market, driven by rapid economic growth in the middle class.

Get a glance at the market contribution of various segments Download the PDF Sample

The passenger cars segment was the largest and was valued at USD 3.41 billion in 2018. Further, over time, passenger cars have evolved from mechanically driven to electronically influenced vehicles with advanced safety, security, propulsion, and connectivity features. The market growth hinges on EPS-equipped vehicle sales, fueled by EPS benefits such as improved fuel economy, smaller size, lighter weight, reduced parasitic losses, and lower manufacturing costs, thereby driving market expansion.

For more insights on the market share of various regions Download PDF Sample now!

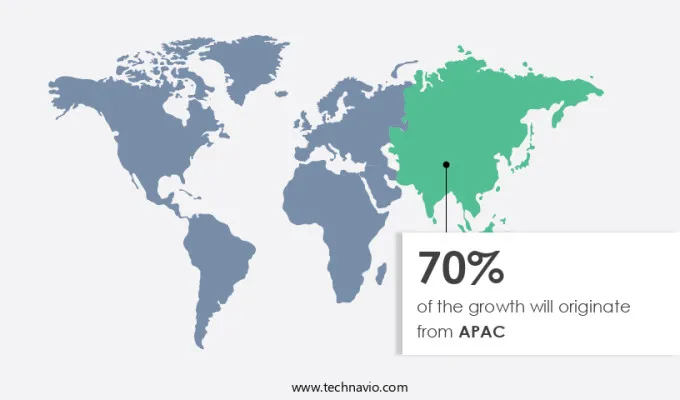

APAC is estimated to contribute 70% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. APAC, led by China, India, Indonesia, and South Korea, boasts one of the world's fastest-growing economies. Improved per-capita income from 2018 to 2019 enhanced consumer purchasing power, driving increased automobile sales. Infrastructure and industrial development expenditures further bolstered commercial vehicle (CV) demand.

Additionally, the region's immense growth potential attracts automotive sensor manufacturers, with APAC expected to see the most significant production volume growth. Establishing a supplier base in APAC offers OEMs cost benefits and fosters collaborative working models, driving sensor market expansion across various automotive applications. China's new fuel consumption standards since 2017, especially with the growing SUV trend, offer substantial EPS market opportunities, while India's increasing PV adoption boosts market growth in the region during the forecast period.

The market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2018 to 2028.

The market is experiencing rapid expansion driven by advancements in electronic control units and motor technology, particularly in hydraulic power steering systems and ESC (electronic stability control) systems. These systems rely on precise torque and angle sensors to enable functionalities such as Steer-by-Wire and modular column-assist EPS system (mCEPS). With the rise of fuel-efficient automobiles and EV adoption, demand for non-contact torque sensors and Surface acoustic wave (SAW) detection technology is surging. Automotive manufacturers and original equipment manufacture (OEM) are increasingly incorporating torque and rotation angle sensors into their vehicles to enhance power steering systems and improve fuel efficiency. This market growth is further fueled by the need for sensor fusion and Adaptive cruise control in modern automotive steering systems, catering to both Heavy-duty (HD) trucks and entry-level cars.

Furthermore, In the market, advancements in pump technology and torque and angle sensor innovations are driving the evolution of Steer-by-Wire systems and UD Active Steering in vehicles. These systems, often integrated with electric motor and hydraulic steering gear, are becoming increasingly popular among automakers to enhance vehicle maneuverability and safety. With rising Vehicle production rates, the demand for reliable Rotating system components and Strain gauge bridges for torque measurement is also growing. Automotive systems equipped with Electric power steering systems and High-Output Electric Power Steering (EPS) system are incorporating sophisticated Accelerometers, Gyroscopes, and Wheel speed sensors to address challenges such as extreme vibrations, Shocks, and Temperature variations.

Additionally, the after market sector is witnessing a surge in demand for innovative solutions like Steer-by-Wire (SBW) systems and Modular column-assist electric power steering (mCEPS) system, catering to both original equipment manufacturers (OEMs) requirements and after market installations. In heavy commercial vehicles, electric power steering (EPS) systems utilize magnetic sensing to record and measure torque, ensuring optimal performance of the rotating system and accurate monitoring of torsion bar angle, particularly in the context of autonomous vehicles.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

179 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.68% |

|

Market growth 2024-2028 |

USD 2.07 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.51 |

|

Regional analysis |

APAC, Europe, North America, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 70% |

|

Key countries |

US, China, Japan, India, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ABB Ltd., Advanced Micro Electronics Co. Ltd., AVL List GmbH, Bourns Inc., DENSO Corp., Eltek Systems, FUTEK Advanced Sensor Technology Inc., HELLA GmbH and Co. KGaA, Hitachi Ltd., Honeywell International Inc., Hottinger Bruel and Kjaer GmbH, Infineon Technologies AG, Kistler Holding AG, Methode Electronics Inc., Novanta Inc., Racelogic, Robert Bosch GmbH, SENSOTEC INSTRUMENTS S.A, TE Connectivity Ltd., and Valeo SA |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements.

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Application

7 Market Segmentation by Type

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.