Automotive Vacuumless Braking Market 2024-2028

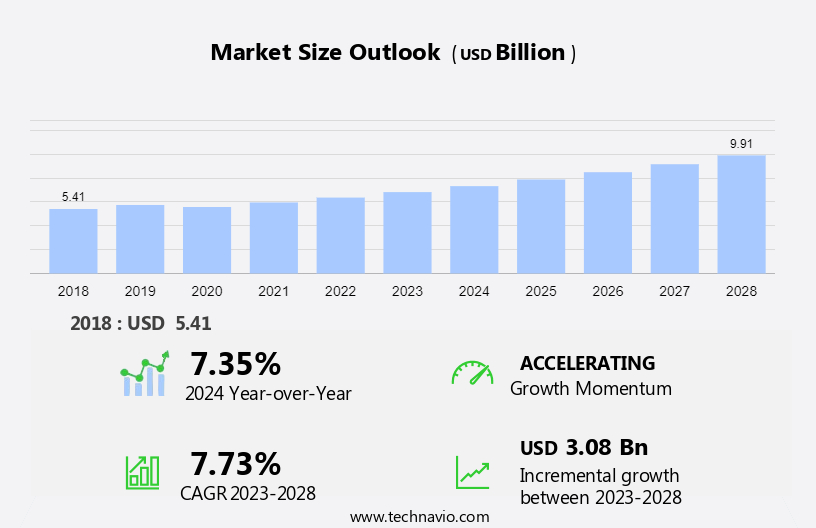

The Automotive Vacuumless Braking Market size is forecast to increase by USD 3.08 billion, at a CAGR of 7.73% between 2023 and 2028. The market growth analysis depends on several factors, including the increase in demand for environmentally sustainable solutions, the rising demand for heavy-duty vehicles in India and Eastern Europe, and the growing need for mandatory safety solutions for heavy-duty vehicles.

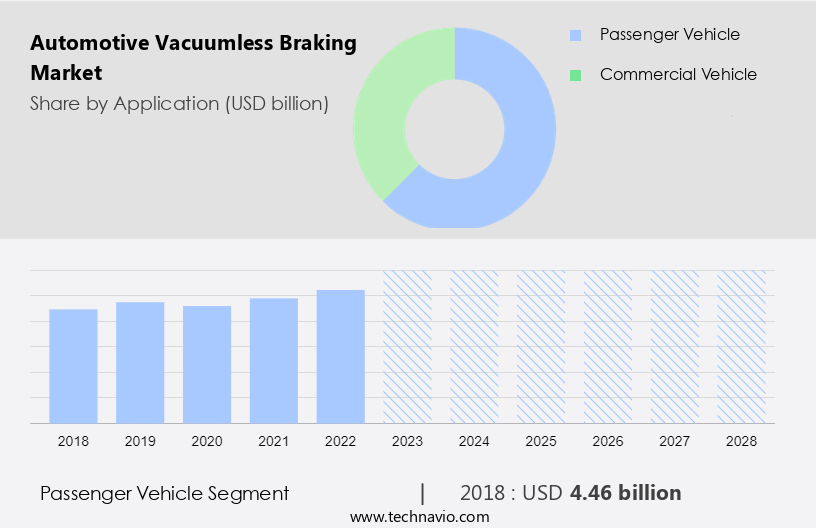

The market research and growth include a comprehensive outlook on the market, offering forecasts for the industry segmented by Application, which comprises passenger vehicle, and commercial vehicle. Additionally, it categorizes End-user into OEM, and aftermarket, and covers Regions, including APAC, Europe, North America, South America, and Middle East and Africa. The market analysis and report provides market size, historical data spanning from 2018 to 2022, and future projections, all presented in terms of value in USD billion for each of the mentioned segments.

What will be the Size of the Market During the Forecast Period?

For More Highlights About this Report, Download Free Sample in a Minute

Market Key Drivers, Trends, and Challenges

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Key Market Driver

Increase in demand for environmentally sustainable solutions is the key factor driving market growth. As the automotive industry grapples with the imperative to reduce its environmental footprint, vacuumless braking systems emerge as a transformative solution. By eliminating traditional vacuum boosters and optimizing braking efficiency, these systems contribute significantly to energy conservation and reduce carbon emissions. The lightweight design of vacuumless braking components not only enhances vehicle fuel efficiency but also aligns with the industry's commitment to lightweight strategies, further curbing greenhouse gas emissions.

Additionally, regulatory pressure for stringent emissions standards globally reinforces the demand for eco-friendly braking technologies, positioning vacuumless braking systems as a key enabler for manufacturers to achieve compliance while bolstering their environmental stewardship credentials. As consumer preferences increasingly pivot toward sustainable automotive solutions, the adoption of vacuumless braking systems not only addresses regulatory imperatives but also aligns with the industry's broader mission of achieving a more environmentally conscious and sustainable transportation ecosystem and, hence, will drive market growth during the forecast period.

Key Market Trends

Integration of vacuumless braking systems with ADAS is the primary trend shaping market growth. Aligning with market trends and analysis, the integration of vacuumless braking systems with advanced driver assistance systems (ADAS) drives market growth. ADAS technologies aim to enhance vehicle safety, providing assistance to drivers and, in some cases, even intervening to prevent or mitigate collisions. Vacuumless braking systems, with their advanced features and improved responsiveness, seamlessly align with and complement the objectives of ADAS, contributing to a safer driving experience.

Moreover, vacuumless braking systems play a pivotal role in these applications by providing a sophisticated braking solution that meets the stringent requirements of modern safety technologies. As the automotive industry continues to progress toward autonomous driving, the integration of vacuumless braking systems with ADAS is expected to play a pivotal role in shaping the future of advanced automotive safety technologies, which will drive market growth during the forecast period.

Major Market Challenge

High implementation costs for integrating advanced braking systems are a challenge that affects market growth. Costs and affordability pose significant challenges to the widespread adoption of vacuumless braking systems in the global automotive market. The initial implementation costs for integrating these advanced braking systems can be relatively high, impacting the production expenses of automakers. These cost challenges may hinder vacuumless braking system adoption, particularly in mass-market and budget-friendly vehicles, where cost-effectiveness is a critical factor.

In addition, one recent example highlighting the cost challenge is the limited integration of vacuumless braking systems in entry-level electric vehicles (EVs). Furthermore, the transition to vacuumless braking systems involves retrofitting existing manufacturing processes and equipment, adding to the overall cost. Manufacturers must strike a balance between incorporating innovative technologies and maintaining competitive pricing to appeal to a broad consumer base. Thus, such factors may impede market growth during the forecast period.

Market Customer Landscape

The market research report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Customer Landscape

Who are the Major Market Companies?

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

- Aptiv Plc: The company offers automotive vacuumless braking that controls and enhances the safety, comfort, and convenience of the vehicle with comfort and convenience functionality through deep power, data, and integration capabilities.

The research report also includes detailed analyses of the competitive landscape of the market and information about 16 market companies, including:

- BorgWarner Inc.

- Brembo Spa

- Continental AG

- Cummins Inc.

- GUD Holdings Ltd.

- Haldex AB

- Hitachi Ltd.

- Knorr Bremse AG

- LSP Innovative Automotive Systems GmbH

- Nabtesco Corp.

- Performance Friction Corp.

- Robert Bosch GmbH

- TSE Brakes Inc.

- Westinghouse Air Brake Technologies Corp.

- ZF Off Highway Solutions Minnesota Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

What is the Largest-Growing Segments in the Market?

The passenger vehicle segment is estimated to witness significant growth during the forecast period. Automakers are concentrating on advancing braking technology for passenger cars to meet the rising demand for ride-hailing and personal use. Developed regions like North America and Europe lead in autonomous car development, with luxury car manufacturers playing a pivotal role.

Get a glance at the market contribution of various segments Download the PDF Sample

The passenger vehicle segment was the largest segment and was valued at USD 4.46 billion in 2018. The growing preference for luxury cars, driven by innovation and early adoption, is propelling the global automotive vacuumless braking market. Electrification of cars and increased disposable income allow customers to pay a premium for technologically advanced vehicles, contributing to the market's positive outlook. The rise of level 2 and level 3 autonomous vehicles further fuels market growth, driven by increasing safety demands and government support for autonomous vehicle development. Thus, such factors are expected to drive the passenger vehicle segment of the market during the forecast period.

Which are the Key Regions for the Market?

For more insights on the market share of various regions Download PDF Sample now!

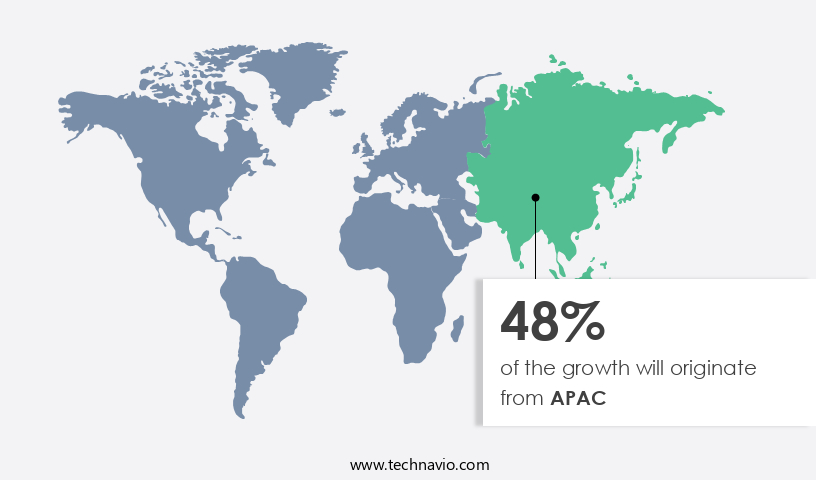

APAC is estimated to contribute 48% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. The APAC region is at the forefront of global automotive innovation, particularly with the adoption of advanced technologies like vacuumless braking systems. Leading economies such as China, India, and Japan are driving this transformation as they actively embrace cutting-edge developments to enhance automotive safety standards. With China and India emerging as significant players in the global automotive market, the region's rapid economic growth increased per capita income, and growing demand for vehicles contribute to the adoption of vacuumless braking, especially in passenger cars. This economic surge also fuels infrastructure development, leading to a heightened demand for commercial vehicles in the region.

Segment Overview

The market report forecasts market growth and forecasting by revenue at global, regional & country levels and provides an analysis of the latest market growth and trends opportunities from 2018 to 2028.

- Application Outlook

- Passenger vehicle

- Commercial vehicle

- End-user Outlook

- OEM

- Aftermarket

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- The U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- South America

- Chile

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

|

Automotive Vacuumless Braking Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

173 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.73% |

|

Market Growth 2024-2028 |

USD 3.08 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.35 |

|

Regional analysis |

APAC, Europe, North America, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 48% |

|

Key countries |

US, China, Japan, South Korea, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Aptiv Plc, BorgWarner Inc., Brembo Spa, Continental AG, Cummins Inc., GUD Holdings Ltd., Haldex AB, Hitachi Ltd., Knorr Bremse AG, LSP Innovative Automotive Systems GmbH, Nabtesco Corp., Performance Friction Corp., Robert Bosch GmbH, TSE Brakes Inc., Westinghouse Air Brake Technologies Corp., and ZF Off Highway Solutions Minnesota Inc. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Automotive Vacuumless Braking Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the growth of the market forecast between 2024 and 2028

- Precise estimation of the market size and its contribution to the market in focus on the parent market

- Accurate predictions about upcoming trends and changes in consumer behavior

- Growth of the market industry across APAC, Europe, North America, South America, and Middle East and Africa

- A thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -