Automotive Vents Market Size 2026-2030

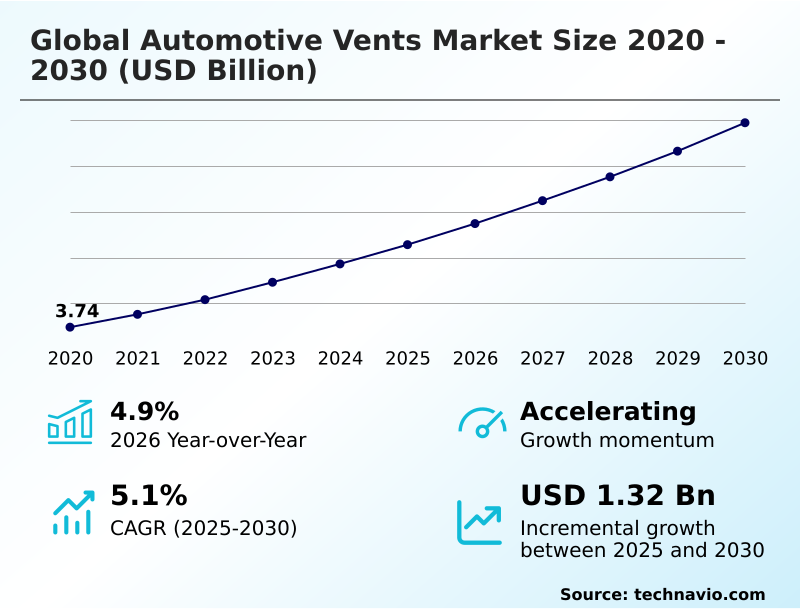

The automotive vents market size is valued to increase by USD 1.32 billion, at a CAGR of 5.1% from 2025 to 2030. Growth of automotive electronics will drive the automotive vents market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 46.8% growth during the forecast period.

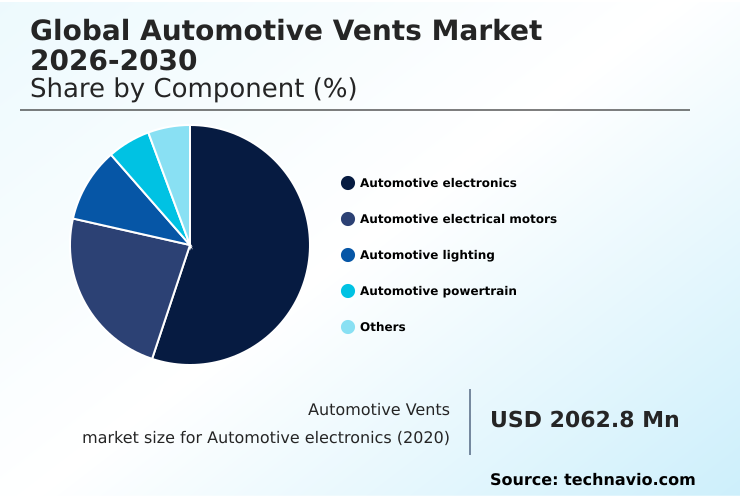

- By Component - Automotive electronics segment was valued at USD 2.46 billion in 2024

- By Type - PTFE materials segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 2.22 billion

- Market Future Opportunities: USD 1.32 billion

- CAGR from 2025 to 2030 : 5.1%

Market Summary

- The automotive vents market is undergoing a significant transformation driven by vehicle electrification and increasing electronic complexity. These components are essential for managing pressure equalization in sealed enclosures, preventing damage from thermal cycling. Advanced eptfe solutions and hydrophobic membranes provide critical ingress protection against moisture and contaminants, a key requirement for electronic control unit protection and ev battery pack venting.

- A typical business scenario involves an OEM designing a new electric SUV for global markets. The engineering team must select screw-in vent plugs and adhesive vents that offer an ip69k protection rating to handle both deep water wading and high-pressure washing. This requires careful material selection, from polypropylene vent housing to specialized oleophobic coatings, to ensure longevity.

- Furthermore, ensuring an emergency degassing function for thermal runaway mitigation is a non-negotiable safety requirement, driving innovation in technologies like dual-stage jet battery venting and reversible metallic quick venting.

What will be the Size of the Automotive Vents Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automotive Vents Market Segmented?

The automotive vents industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

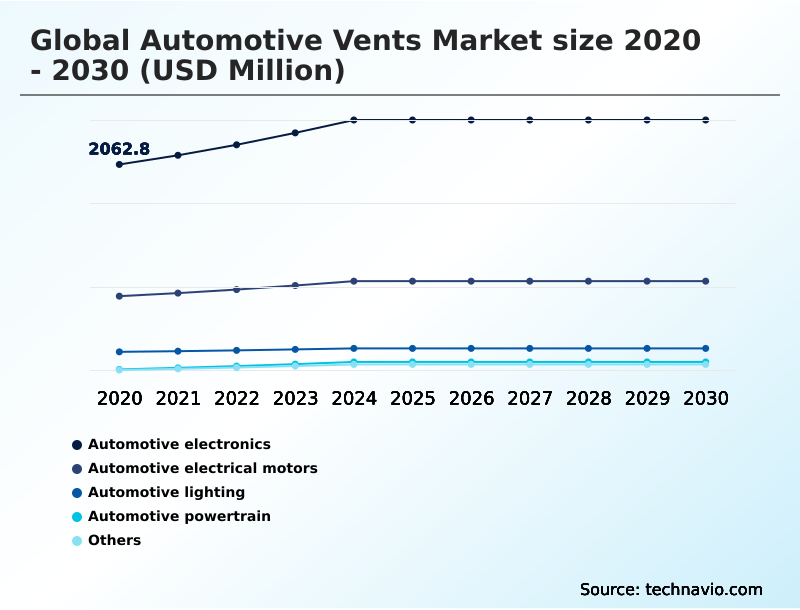

- Component

- Automotive electronics

- Automotive electrical motors

- Automotive lighting

- Automotive powertrain

- Others

- Type

- PTFE materials

- PP materials

- PE materials

- Vehicle type

- Passenger vehicles

- Commercial vehicles

- Others

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- France

- UK

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of World (ROW)

- APAC

By Component Insights

The automotive electronics segment is estimated to witness significant growth during the forecast period.

The automotive electronics segment is expanding rapidly, driving demand for advanced venting solutions. Modern vehicles integrate a dense network of electronic control units that require robust electronic control unit protection.

The shift to electric mobility intensifies this need, particularly for ev battery pack venting to ensure safety and performance through effective thermal runaway mitigation.

Sophisticated components rely on materials like expanded polytetrafluoroethylene (eptfe solutions) to manage pressure equalization during thermal cycling. These vents prevent automotive lighting condensation and ensure powertrain breather solutions function correctly, with oleophobic coatings providing essential protection in harsh environments.

The Automotive electronics segment was valued at USD 2.46 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 46.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Vents Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by the APAC region, accounting for 46.8% of market opportunities, significantly outpacing North America.

This is driven by massive EV production in countries like China, where demand for advanced anti-fogging vents and components for fuel cell stack humidity control is soaring.

European markets prioritize components with a high ip69k protection rating for applications such as charging inlet moisture protection and wiper motor housing protection.

In North America, the focus is on ruggedness for large vehicles, though there is a growing niche for high-tech components like acoustic vent membranes and cabin pressure relief vents in premium and electric models.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The automotive vents market is increasingly focused on providing highly specialized solutions to address complex engineering challenges. The core objective is preventing moisture in ev battery packs, which is crucial for safety and longevity. This has spurred the development of high airflow vents for led headlamps to eliminate condensation and maintain optical clarity.

- For powertrains, oleophobic vents for powertrain components are essential to repel oils while allowing air to pass. The shift to integrated drive units creates demand for effective pressure equalization for e-axle design. As motor technology advances, thermal management for high-speed motors becomes a priority, requiring vents that can handle extreme temperatures.

- Autonomous vehicle development relies on waterproof vents for autonomous sensors and reducing condensation in adas cameras to ensure reliable operation. Key goals include providing dust protection for electronic control units and corrosion prevention in lighting enclosures. The most critical application is providing safety venting for thermal runaway events.

- Suppliers are also developing venting solutions for high-humidity climates and durable vents for commercial vehicles. In a competitive landscape where product lifecycles have been cut by more than half, the ability to rapidly engineer compact vents for integrated e-axles or advanced vents for hybrid powertrains is a key differentiator.

- This extends to chemical resistant vents for fuel systems, vents for off-road vehicle differentials, venting for hydrogen fuel cell stacks, and even smart venting for active thermal control, all while pursuing lightweight vents for ev range extension and managing pressure in sealed enclosures.

What are the key market drivers leading to the rise in the adoption of Automotive Vents Industry?

- The significant growth of automotive electronics is a paramount driver for the global automotive vents market, necessitated by the industry's shift toward connected, autonomous, and electric mobility.

- The accelerated adoption of electric vehicles, with sales growing over 35% annually, is a primary driver. This surge fuels demand for components that manage pressure differentials effectively.

- Innovations like rugged sintered pe vents and durable uhmwpe porous plastics are increasingly used for applications such as hydraulic fluid reservoir vents and transmission breather hose fittings.

- For more critical systems, welded eptfe membranes are specified to prevent headlamp fog prevention and ensure the reliability of fuel tank rollover valves. These advanced membranes are often encased in a resilient polypropylene vent housing to withstand extreme environmental conditions.

What are the market trends shaping the Automotive Vents Industry?

- Advances in membrane technology for automotive vents represent a pivotal market trend. This is driven by the escalating demand for protecting sensitive electronics and electric vehicle components.

- A key market trend is the advancement in material science, with sophisticated hydrophobic membranes and microporous membranes becoming standard for providing robust ingress protection. These innovations are critical for managing the intense effects of thermal cycling in compact systems, which is essential for effective e-axle thermal management and reliable adas sensor protection.

- Furthermore, snap-fit vent assemblies are streamlining manufacturing processes and reducing assembly times by over 15%, enhancing efficiency in applications related to drivetrain pressure management and the protection of sensor enclosure venting.

What challenges does the Automotive Vents Industry face during its growth?

- Volatility in the prices of raw materials for automotive vents poses a significant challenge to the industry, impacting production costs and profit margins for manufacturers.

- A significant challenge arises from the rapid pace of technological change, which shortens product lifecycles and increases R&D costs. As automakers demand solutions for high-voltage battery safety, suppliers must rapidly develop technologies like dual-stage jet battery venting and reversible metallic quick venting, both of which provide a critical emergency degassing function.

- This innovation pressure extends to components like screw-in vent plugs and adhesive vents used for inverter cooling systems and electric motor housing vents. The need to protect sensitive electronics for telematics control unit cooling forces manufacturers to invest heavily in designs that may become obsolete within two to three years.

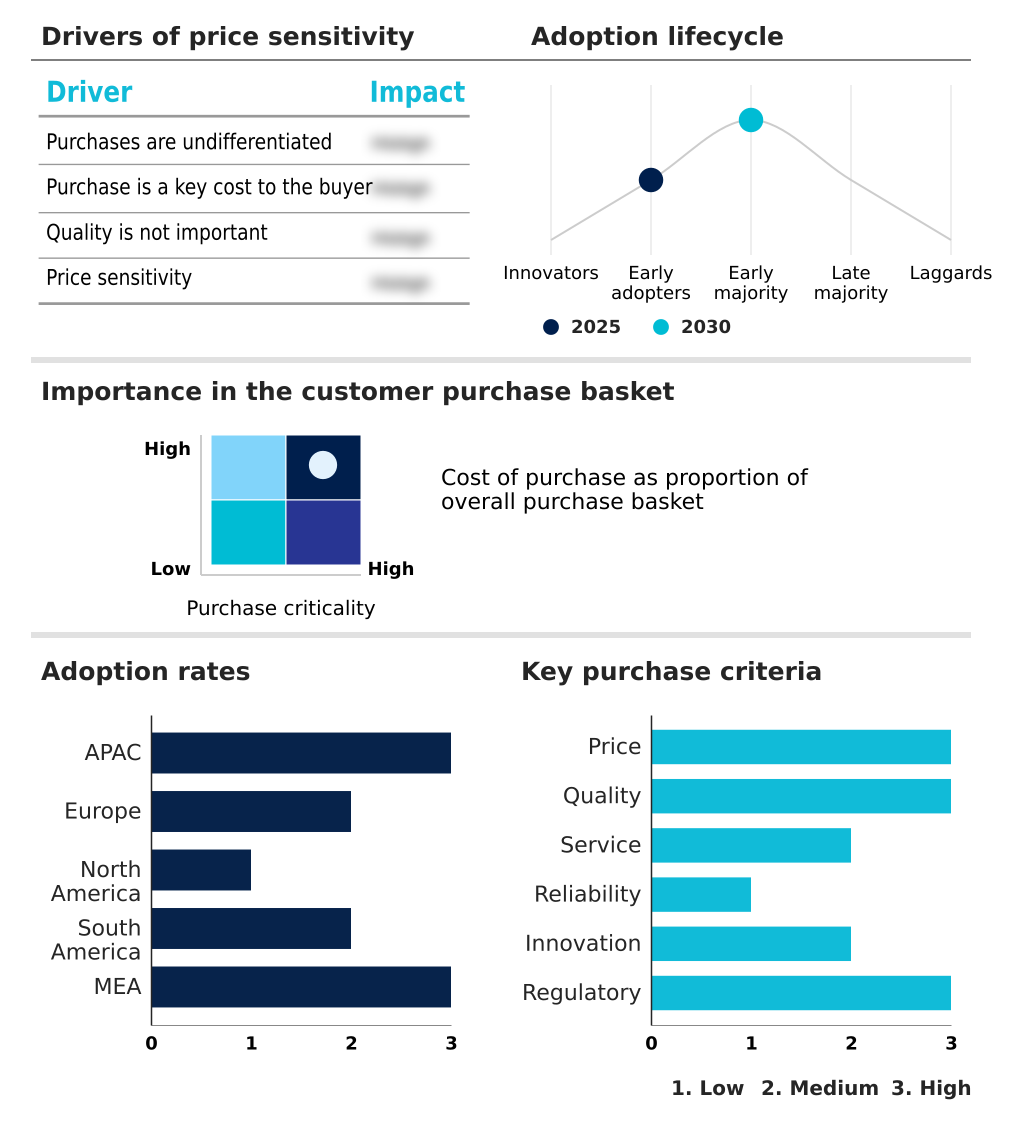

Exclusive Technavio Analysis on Customer Landscape

The automotive vents market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive vents market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Vents Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive vents market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Berghof GmbH - Analysts note the company's focus on specialized fluoroplastic membranes, including Permeaflon automotive vents, serving critical industrial and automation sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Berghof GmbH

- Cascade Engineering

- EBM Papst

- Faurecia SE

- Filtration Group

- Fischerwerke GmbH and Co. KG

- Hangzhou IPRO Membrane Co.

- MAHLE GmbH

- Nifco Inc.

- Novares Group SA

- Parker Hannifin Corp.

- Polystar Technologies LLC

- Porex Corp.

- Shenzhen Milvent Co. Ltd.

- W. L. Gore and Associates

- Weber GmbH & Co. KG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive vents market

- In September 2024, Nifco Inc. broadened its technological scope through a strategic investment in LexxPluss, enhancing its capabilities in automated and robotic solutions.

- In March 2025, Eaton launched an industry-first 3-in-1 battery vent valve, which integrates passive and active venting with a case leak-check mechanism, aligning with the SAE J3277 standard to improve EV battery safety.

- In April 2025, Novares Group SA was acquired by Global Technologies in a move designed to reinforce its industrial capabilities and strategic position in the automotive components market.

- In May 2025, Nitto Denko reported substantial fiscal year 2025 growth, with a 10.8% revenue increase primarily driven by strong demand for its automotive materials and industrial tapes for next-generation mobility.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Vents Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.1% |

| Market growth 2026-2030 | USD 1324.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.9% |

| Key countries | China, Japan, India, South Korea, Indonesia, Australia, Germany, France, UK, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, South Africa, UAE, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The automotive vents market is fundamentally shaped by the industry's shift to electric and software-defined vehicles, a trend compelling boardroom-level strategic pivots toward advanced material science. With EV adoption rates climbing over 35% annually, the focus is on safety and reliability. This necessitates the use of expanded polytetrafluoroethylene (eptfe solutions) and microporous membranes to provide superior ingress protection.

- Key technologies include reversible metallic quick venting and dual-stage jet battery venting, which offer a critical emergency degassing function for thermal runaway mitigation. Boardroom decisions now center on securing supply chains for hydrophobic membranes and components with oleophobic coatings. Designs are evolving to include rugged sintered pe vents made from uhmwpe porous plastics and lightweight polypropylene vent housing.

- Manufacturing employs welded eptfe membranes in snap-fit vent assemblies and adhesive vents to streamline production. The complexity spans from managing pressure equalization during thermal cycling to handling pressure differentials. Solutions range from screw-in vent plugs offering an ip69k protection rating to specialized anti-fogging vents, acoustic vent membranes, and cabin pressure relief vents, demonstrating the market's vast technical scope.

What are the Key Data Covered in this Automotive Vents Market Research and Growth Report?

-

What is the expected growth of the Automotive Vents Market between 2026 and 2030?

-

USD 1.32 billion, at a CAGR of 5.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Automotive electronics, Automotive electrical motors, Automotive lighting, Automotive powertrain, and Others), Type (PTFE materials, PP materials, and PE materials), Vehicle Type (Passenger vehicles, Commercial vehicles, and Others) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growth of automotive electronics, Volatility in raw material prices of automotive vents

-

-

Who are the major players in the Automotive Vents Market?

-

Berghof GmbH, Cascade Engineering, EBM Papst, Faurecia SE, Filtration Group, Fischerwerke GmbH and Co. KG, Hangzhou IPRO Membrane Co., MAHLE GmbH, Nifco Inc., Novares Group SA, Parker Hannifin Corp., Polystar Technologies LLC, Porex Corp., Shenzhen Milvent Co. Ltd., W. L. Gore and Associates and Weber GmbH & Co. KG

-

Market Research Insights

- The market is defined by rapid innovation, driven by an over 30% annual growth in EV adoption and product development cycles compressing from five years to under three. This acceleration mandates advanced solutions for ev battery pack venting and ensuring high-voltage battery safety.

- Demand is surging for specialized components providing electronic control unit protection, preventing automotive lighting condensation, and enabling effective powertrain breather solutions. As vehicles become more complex, managing drivetrain pressure management and e-axle thermal management is critical. This requires sophisticated sensor enclosure venting for adas sensor protection to avoid headlamp fog prevention issues.

- Even conventional components like fuel tank rollover valves, transmission breather hose fittings, and hydraulic fluid reservoir vents are being re-engineered. The scope now includes electric motor housing vents, inverter cooling systems, telematics control unit cooling, and ensuring charging inlet moisture protection.

- Protection for brake fluid reservoir vents, fuel cell stack humidity control, and wiper motor housing protection further highlights the market's expanding technical depth.

We can help! Our analysts can customize this automotive vents market research report to meet your requirements.

RIA -

RIA -