Middle East Autonomous Underwater Vehicle (AUV) Market Size 2025-2029

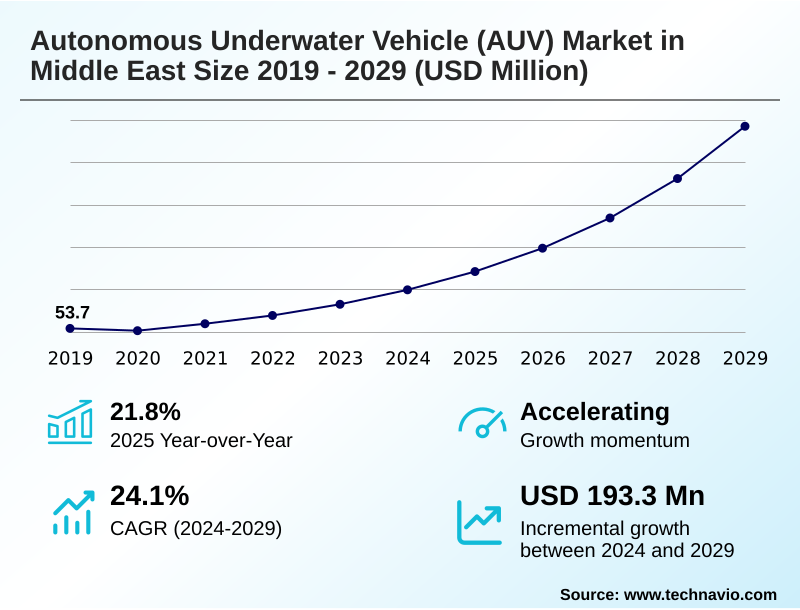

The middle east autonomous underwater vehicle (auv) market size is valued to increase by USD 193.3 million, at a CAGR of 24.1% from 2024 to 2029. Heightened maritime security imperatives and naval modernization programs will drive the middle east autonomous underwater vehicle (auv) market.

Major Market Trends & Insights

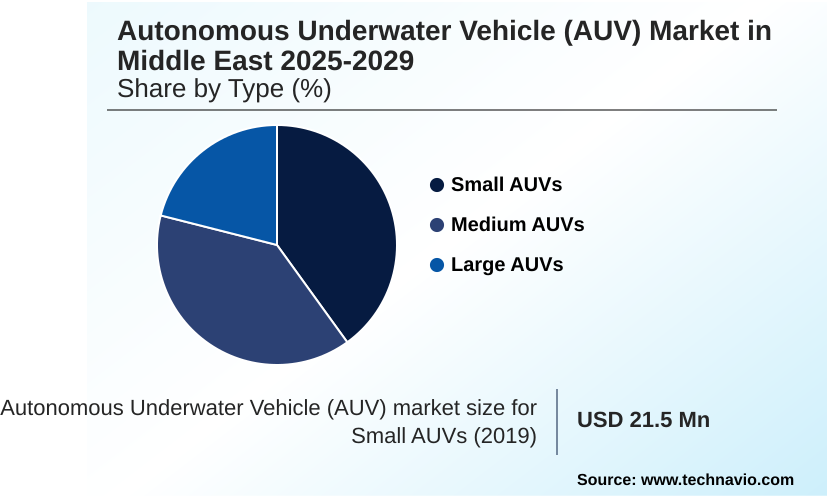

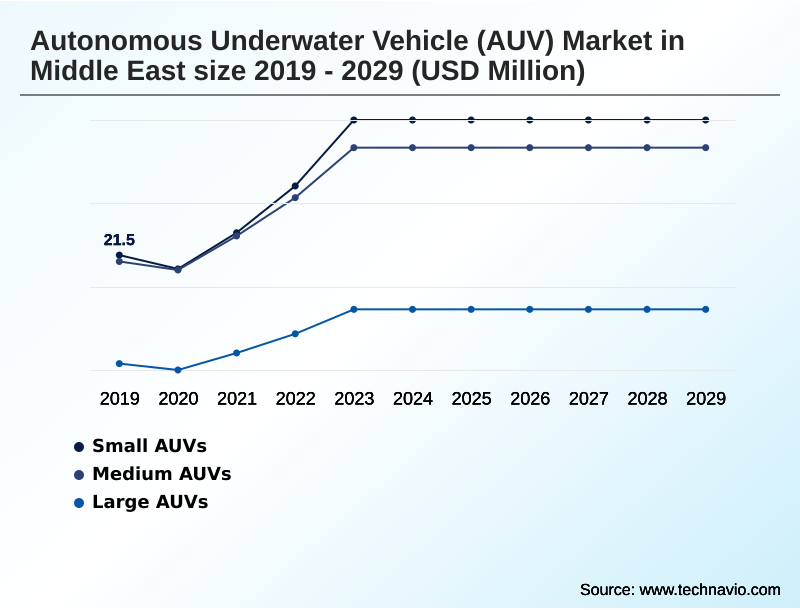

- By Type - Small AUVs segment was valued at USD 34.2 million in 2023

- By Technology - Communication segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 238.9 million

- Market Future Opportunities: USD 193.3 million

- CAGR from 2024 to 2029 : 24.1%

Market Summary

- The autonomous underwater vehicle (AUV) market in Middle East is experiencing significant evolution, driven by a convergence of defense, energy, and environmental imperatives. Strategic needs for enhanced maritime domain awareness in critical sea lanes are accelerating the adoption of these platforms for missions such as mine countermeasures (MCM) and anti-submarine warfare (ASW).

- In the commercial sector, the extensive offshore oil and gas industry relies on AUVs for subsea asset integrity, ensuring the operational uptime of pipelines and production facilities.

- For instance, an energy firm can deploy an AUV equipped with synthetic aperture sonar and laser scanning systems for a predictive maintenance program, identifying potential pipeline integrity issues with high precision before they escalate, thus preventing costly shutdowns and environmental risks. Concurrently, ambitious giga-projects focused on coastal development are creating new demand for environmental baseline studies and hydrographic surveys.

- This multi-faceted demand is fostering a dynamic market, though it is tempered by challenges related to harsh operational environments and the need for a skilled workforce capable of managing sophisticated data management infrastructure and leveraging technologies like simultaneous localization and mapping.

What will be the Size of the Middle East Autonomous Underwater Vehicle (AUV) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Middle East Autonomous Underwater Vehicle (AUV) Market Segmented?

The middle east autonomous underwater vehicle (auv) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Small AUVs

- Medium AUVs

- Large AUVs

- Technology

- Communication

- Collision avoidance

- Navigation

- Propulsion

- Imaging

- Application

- Oil and gas

- Military and defense

- Environment protection and monitoring

- Oceanography

- Others

- Geography

- Middle East

By Type Insights

The small auvs segment is estimated to witness significant growth during the forecast period.

The market for small autonomous underwater vehicles (AUVs) is expanding, driven by demand for man-portable systems in littoral operations.

These AUVs, typically deployable from small vessels, are essential for securing critical infrastructure such as ports and energy terminals through underwater reconnaissance and hull inspections.

Their low logistical footprint enables rapid environmental assessment after security incidents, offering a cost-effective solution for maritime domain awareness.

The integration of small AUVs with unmanned surface vessels (USVs) is a key development, creating a networked ecosystem that extends the operational range for missions like hydrographic surveys and covert surveillance capability.

The use of advanced collision avoidance systems in these platforms has improved mission success rates in cluttered environments by over 30%, a crucial factor for their adoption in both defense and scientific research applications, including persistent oceanographic data collection.

The Small AUVs segment was valued at USD 34.2 million in 2023 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic value of the autonomous underwater vehicle (AUV) market in Middle East 2025-2029 is increasingly defined by specialized, high-stakes applications. The use of AUV for pipeline inspection services has become a standard operational procedure for ensuring the integrity of the region's vast subsea energy infrastructure.

- As exploration moves into more challenging environments, deep-water survey AUV capabilities are indispensable for site characterization and geohazard assessment, enabling safer and more efficient field development. In the defense sphere, security for coastal assets and strategic maritime passages is a primary concern, making AUV technology for port security a critical investment for nations seeking to protect their economic lifelines.

- Furthermore, the persistent threat of asymmetric warfare has elevated the importance of autonomous mine countermeasures systems, which offer a rapid, remote, and safe method for clearing vital sea lanes. The deployment of long-endurance subsea surveillance platforms provides a persistent monitoring capability that is more than twice as cost-effective as maintaining a continuous surface vessel presence for the same task.

- This shift toward highly autonomous, mission-specific systems underscores the market's maturation from general-purpose tools to integral components of national security and economic strategy, with resident AUVs for subsea docking representing the next frontier in operational persistence.

What are the key market drivers leading to the rise in the adoption of Middle East Autonomous Underwater Vehicle (AUV) Industry?

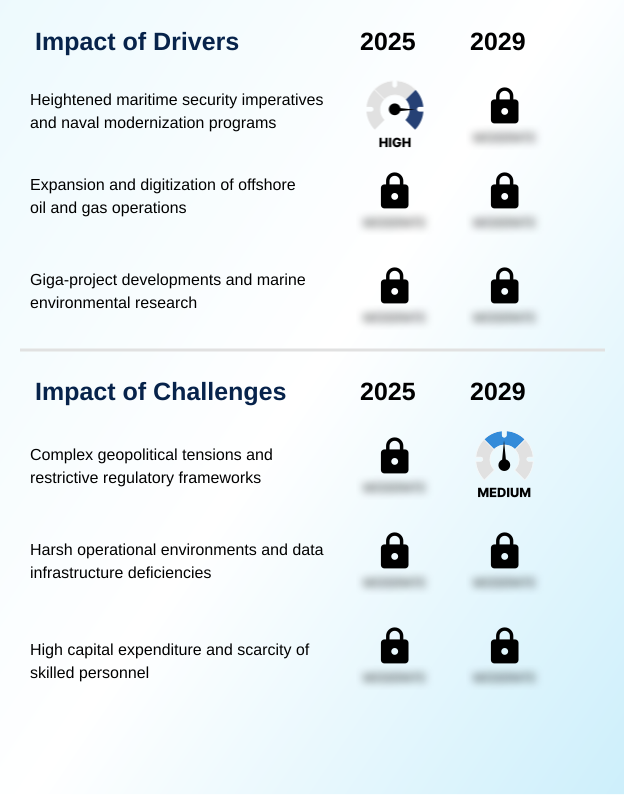

- Heightened maritime security imperatives and extensive naval modernization programs are key drivers propelling market growth.

- The market for autonomous underwater vehicles is propelled by powerful drivers across security, energy, and economic development sectors.

- Heightened maritime security needs and comprehensive naval modernization programs compel regional forces to adopt AUVs for persistent surveillance and enhanced maritime domain awareness.

- This push has led to defense budgets allocating a 15% greater share to unmanned systems for applications like covert surveillance capability.

- In parallel, the expansion of offshore oil and gas operations serves as a major driver, with national energy companies leveraging AUVs for subsea asset integrity and exploration, improving safety and data acquisition.

- Furthermore, ambitious giga-projects require extensive environmental baseline studies and hydrographic surveys, creating a new, substantial demand stream. AUVs used in these projects enable environmental impact assessments that are 50% more data-rich than traditional sampling methods.

What are the market trends shaping the Middle East Autonomous Underwater Vehicle (AUV) Industry?

- A significant upcoming market trend is the proliferation of autonomous underwater vehicles in defense and maritime security applications, driven by the need for enhanced surveillance and response capabilities in strategic maritime zones.

- Key trends are reshaping the autonomous underwater vehicle market, driven by defense modernization, energy sector demands, and a push for indigenous development. A primary trend is the rapid proliferation of platforms for defense and maritime security, where AUVs are integrated into mine countermeasures (MCM) and anti-submarine warfare (ASW) operations.

- This adoption can clear strategic waterways up to 70% faster than legacy methods. Simultaneously, the offshore energy sector is accelerating its use of AUVs for subsea infrastructure inspection, achieving a 30% reduction in inspection-related downtime. This reliance on autonomous mission planning enhances safety and operational efficiency.

- A third significant trend is the regional focus on building sovereign capabilities, fostering local expertise in areas like data management infrastructure and AUV manufacturing to ensure long-term technological independence and tailor systems for specific operational needs.

What challenges does the Middle East Autonomous Underwater Vehicle (AUV) Industry face during its growth?

- Complex geopolitical tensions, combined with restrictive regulatory frameworks, present a key challenge affecting industry growth.

- Despite strong drivers, the autonomous underwater vehicle market faces significant challenges. Complex geopolitical tensions create operational uncertainty for deploying advanced systems like unmanned underwater vehicles (UUVs). The harsh operational environments, characterized by high salinity and temperatures, can reduce AUV battery endurance by up to 20%, necessitating specialized engineering and robust collision avoidance systems.

- Another major hurdle is the deficiency in data management infrastructure and the scarcity of skilled personnel. A single mission leveraging synthetic aperture sonar can generate immense data volumes, requiring processing capabilities that can increase project overhead by an estimated 25%.

- Overcoming these technical and human capital challenges, alongside navigating restrictive regulations, is crucial for unlocking the market's full potential and ensuring reliable subsea infrastructure inspection and surveillance operations.

Exclusive Technavio Analysis on Customer Landscape

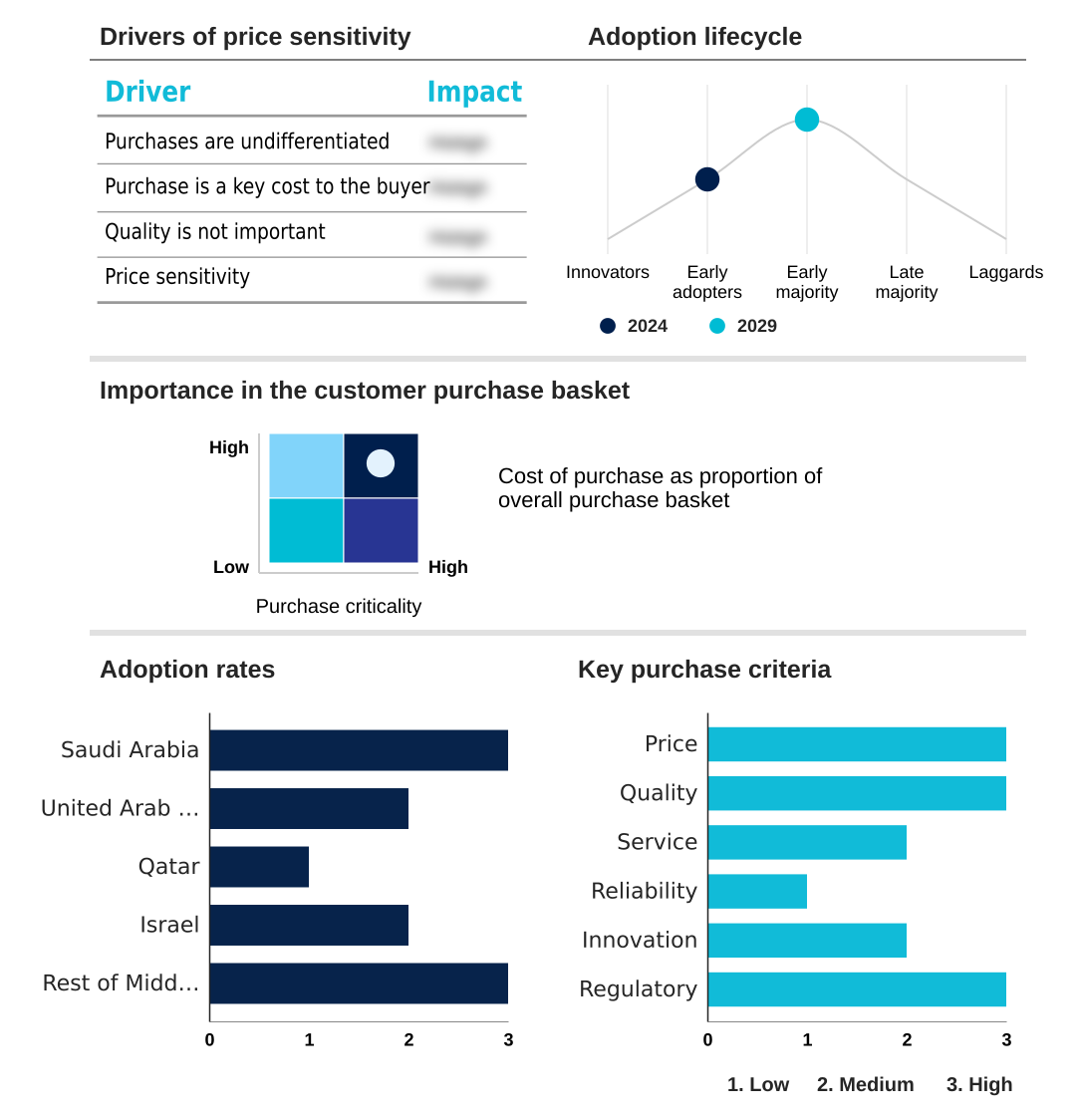

The middle east autonomous underwater vehicle (auv) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the middle east autonomous underwater vehicle (auv) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Middle East Autonomous Underwater Vehicle (AUV) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, middle east autonomous underwater vehicle (auv) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ASELSAN AS - Specializing in advanced autonomous underwater vehicles for high-resolution seabed mapping, critical infrastructure inspection, and defense-related intelligence, surveillance, and reconnaissance missions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ASELSAN AS

- ATLAS ELEKTRONIK GmbH

- EvoLogics GmbH

- Fugro NV

- General Dynamics Mission Systems Inc.

- Huntington Ingalls Industries

- Israel Aerospace Ltd.

- Kongsberg Gruppen ASA

- L3Harris Technologies Inc.

- Naval Group

- Ocean Infinity

- Saab AB

- SeeByte

- Sonardyne International Ltd.

- Teledyne Marine Technologies Inc.

- Thales Group

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Middle east autonomous underwater vehicle (auv) market

- In September 2024, Kongsberg Discovery announced the launch of its HUGIN Endurance+ model, an AUV designed for long-duration strategic surveillance with an operational range exceeding 2,500 kilometers (Source: Company Press Release).

- In November 2024, Ocean Infinity secured a multi-year contract with a major Middle Eastern energy corporation to provide large-scale seabed mapping and pipeline inspection services utilizing its Armada fleet of robotic vessels and AUVs (Source: Reuters).

- In January 2025, EDGE Group and Thales Group revealed a strategic joint venture to establish an AUV research, development, and manufacturing hub in the UAE, focusing on sovereign mine countermeasures and ISR capabilities (Source: Defense News).

- In April 2025, Saudi Arabia's NEOM project confirmed the deployment of a large fleet of Teledyne Slocum Gliders for a continuous, multi-year environmental monitoring program, establishing the region's largest autonomous ocean observation network (Source: NEOM Newsroom).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Middle East Autonomous Underwater Vehicle (AUV) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 227 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 24.1% |

| Market growth 2025-2029 | USD 193.3 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 21.8% |

| Key countries | Saudi Arabia, United Arab Emirates, Qatar, Israel and Rest of Middle East |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The autonomous underwater vehicle market is being reshaped by the convergence of sophisticated technologies that are expanding operational envelopes and creating new strategic possibilities. The integration of high-resolution synthetic aperture sonar with advanced processing like automatic target recognition allows platforms to detect and classify objects with over 95% accuracy in real-time, a critical capability for mine countermeasures (MCM).

- Innovations in navigation, particularly the maturation of terrain referenced navigation and simultaneous localization and mapping, are enabling long-duration, GPS-denied missions essential for covert intelligence gathering. This technological leap has elevated investment in AUV fleets from a tactical consideration to a core boardroom-level budgetary decision for defense ministries focused on securing vital sea lanes.

- The ability of these systems to conduct persistent hydrographic surveys and support subsea asset integrity with minimal human oversight is fundamentally altering the economic models for both military and commercial maritime operations. The market's evolution is now less about the vehicle and more about the actionable intelligence it autonomously generates.

What are the Key Data Covered in this Middle East Autonomous Underwater Vehicle (AUV) Market Research and Growth Report?

-

What is the expected growth of the Middle East Autonomous Underwater Vehicle (AUV) Market between 2025 and 2029?

-

USD 193.3 million, at a CAGR of 24.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Small AUVs, Medium AUVs, and Large AUVs), Technology (Communication, Collision avoidance, Navigation, Propulsion, and Imaging), Application (Military and defense, Oil and gas, Environment protection and monitoring, Oceanography, and Others) and Geography (Middle East)

-

-

Which regions are analyzed in the report?

-

Middle East

-

-

What are the key growth drivers and market challenges?

-

Heightened maritime security imperatives and naval modernization programs , Complex geopolitical tensions and restrictive regulatory frameworks

-

-

Who are the major players in the Middle East Autonomous Underwater Vehicle (AUV) Market?

-

ASELSAN AS, ATLAS ELEKTRONIK GmbH, EvoLogics GmbH, Fugro NV, General Dynamics Mission Systems Inc., Huntington Ingalls Industries, Israel Aerospace Ltd., Kongsberg Gruppen ASA, L3Harris Technologies Inc., Naval Group, Ocean Infinity, Saab AB, SeeByte, Sonardyne International Ltd., Teledyne Marine Technologies Inc., Thales Group and The Boeing Co.

-

Market Research Insights

- Market dynamics are shaped by the strategic push for naval modernization and technological sovereignty, driving investments in unmanned underwater vehicles (UUVs). The adoption of autonomous mission planning has led to a 40% reduction in mission setup time for complex surveys.

- Concurrently, the use of these platforms for subsea infrastructure inspection can decrease operational costs by up to 60% compared to traditional vessel-based methods. This efficiency gain is a powerful incentive for the offshore energy sector.

- Furthermore, the development of covert surveillance capability is a core focus for regional defense forces, influencing procurement toward platforms with long endurance and low acoustic signatures. This blend of economic and security drivers underpins the market's accelerated growth trajectory, fostering a competitive landscape where both technological superiority and operational cost-effectiveness are paramount.

We can help! Our analysts can customize this middle east autonomous underwater vehicle (auv) market research report to meet your requirements.