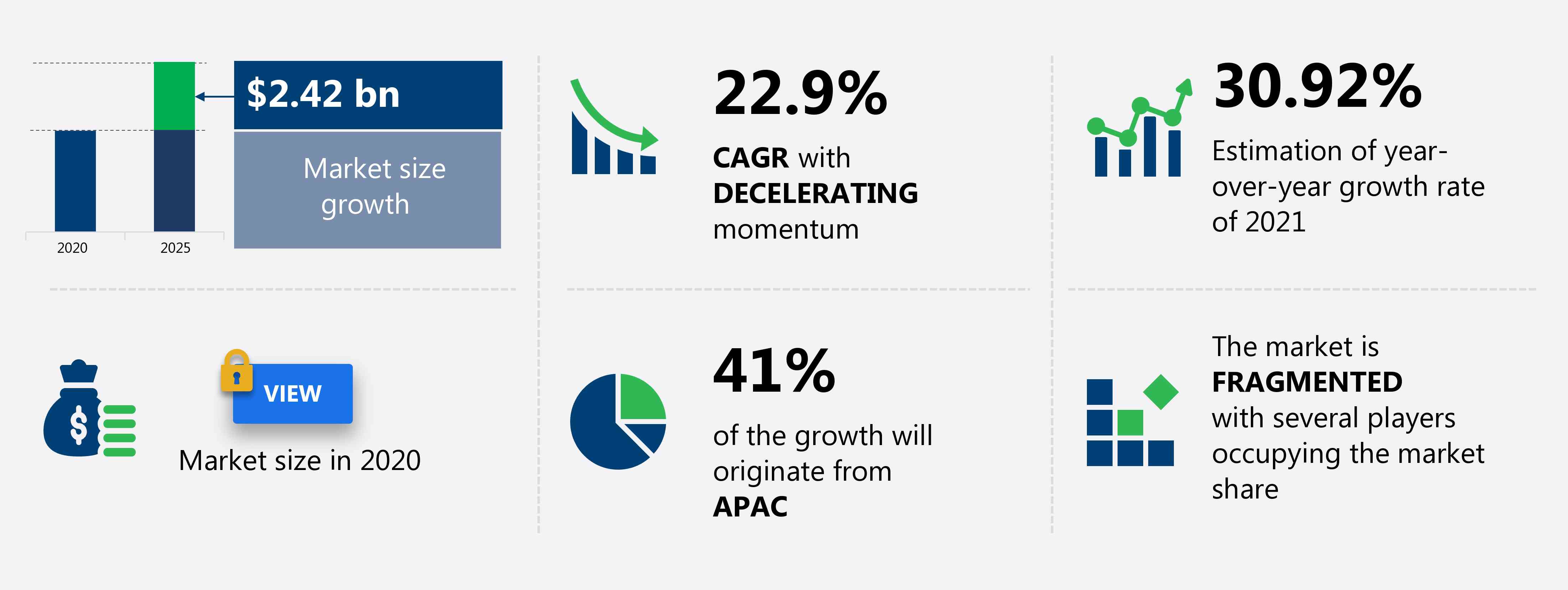

The carrier aggregation solutions market share is expected to increase by USD 2.42 billion from 2020 to 2025, and the market’s growth momentum will accelerate at a CAGR of 22.9%.

This carrier aggregation solutions market research report provides valuable insights on the post COVID-19 impact on the market, which will help companies evaluate their business approaches. Furthermore, this report extensively covers carrier aggregation solutions market segmentation by deployment (femtocell, microcell, metrocell, and picocell) and geography (APAC, North America, Europe, MEA, and South America). The carrier aggregation solutions market report also offers information on several market vendors, including Artiza Networks Inc., Broadcom Inc., Cisco Systems Inc., Huawei Investment and Holding Co. Ltd., Nokia Corp., Qorvo Inc., Rohde and Schwarz GmbH and Co. KG, Telefonaktiebolaget LM Ericsson, Verizon Communications Inc., and ZTE Corp. among others.

What will the Carrier Aggregation Solutions Market Size be During the Forecast Period?

Download the Free Report Sample to Unlock the Carrier Aggregation Solutions Market Size for the Forecast Period and Other Important Statistics

Carrier Aggregation Solutions Market: Key Drivers, Trends, and Challenges

Based on our research output, there has been a neutral impact on the market growth during and after post COVID-19 era. The increase in global mobile data traffic is notably driving the carrier aggregation solutions market growth, although factors such as interoperability issues may impede the market growth. Our research analysts have studied the historical data and deduced the key market drivers and the COVID-19 pandemic impact on the carrier aggregation solutions industry. The holistic analysis of the drivers will help in deducing end goals and refining marketing strategies to gain a competitive edge.

Key Carrier Aggregation Solutions Market Driver

The increase in global mobile data traffic is one of the key factors driving the growth of the global carrier aggregation solutions market. Mobile data traffic is experiencing exponential growth, which is mainly driven by data-capable devices and high bandwidth applications. According to Cisco, over two-thirds of the global population will have access to the internet by 2023. The number of global internet users is expected to increase from 3.9 billion in 2018 to around 5.3 billion in 2023. In addition, the number of devices connected to the IP network is expected to increase from 18.4 billion in 2018 to 29.3 billion in 2023, globally. As a result of these factors, bandwidth demand will begin to exceed supply from macro networks. This will result in poor service quality for customers. A loss in service quality is a challenge for the company, as it is likely to lead to a higher churn rate, resulting in an increase in customer retention costs. To overcome this challenge, carrier aggregation solutions are being deployed in base stations or cell towers, thereby driving the market.

Key Carrier Aggregation Solutions Market Trend

The increased investments in 5G in urban areas will fuel the global carrier aggregation solutions market growth. 5G is the next generation of communication technology, following 4G. On commercialization, 5G will support data download speeds up to 10,000 Mbps. There have been numerous investments in 5G across the globe. For instance, in July 2020, International Business Machines Corp. (IBM) announced its plan to enter into a collaboration with Verizon Business to work together on 5G and edge computing innovation. Similarly, in July 2020, ZTE Corp. announced a collaboration with True Corporation Public Co. Ltd. (True) to build a commercial 5G network in Thailand. Moreover, The transition from 4G LTE to 5G can be achieved through the use of carrier aggregation for the following reasons such as carrier aggregation denotes the concatenation of multiple carriers. This increases the bandwidth and consecutively data rate of the system. LTE R-10 provides support for 5 CCs. As numerous companies are likely to release 5G during the forecast period, investments across all verticals, which include 5G equipment, infrastructure, and deployment techniques will increase. This type of increasing investment in 5G will result in the need for carrier aggregation solutions, thereby driving the market.

Key Carrier Aggregation Solutions Market Challenge

The interoperability issues are a major challenge for the global carrier aggregation solutions market growth. Interoperability is defined as the functioning of separate software and systems to exchange information seamlessly. Carrier aggregation is a part of the LTE-A spectrum; hence, it requires a separate sideband and supporting software to assist in its deployment. Carrier aggregation can be deployed by using a depreciated 4G spectrum. For instance, equipment from Huawei Technologies is incompatible with any gear from Ericsson. Such interoperability issues have delayed the commercialization of such equipment in regions such as Europe. The lack of an ecosystem will also affect its operation, as software upgrades are expensive. Also, differences in interoperability will compel vendors to re-design their equipment, which will further lead to a delay in the deployment of carrier aggregation. This, in turn, will hinder the growth of the market during the forecast period.

This carrier aggregation solutions market analysis report also provides detailed information on other upcoming trends and challenges that will have a far-reaching effect on the market growth. The actionable insights on the trends and challenges will help companies evaluate and develop growth strategies for 2021-2025.

Parent Market Analysis

Technavio categorizes the global carrier aggregation solutions market as a part of the global communications equipment market within the overall global information technology sector. Our research report has extensively covered external factors influencing the parent market growth potential in the coming years, which will determine the levels of growth of the carrier aggregation solutions market during the forecast period.

Who are the Major Carrier Aggregation Solutions Market Vendors?

The report analyzes the market’s competitive landscape and offers information on several market vendors, including:

- Artiza Networks Inc.

- Broadcom Inc.

- Cisco Systems Inc.

- Huawei Investment and Holding Co. Ltd.

- Nokia Corp.

- Qorvo Inc.

- Rohde and Schwarz GmbH and Co. KG

- Telefonaktiebolaget LM Ericsson

- Verizon Communications Inc.

- ZTE Corp.

This statistical study of the carrier aggregation solutions market encompasses successful business strategies deployed by the key vendors. The carrier aggregation solutions market is fragmented and the vendors are deploying organic and inorganic growth strategies to compete in the market.

Product Insights and News

- Artiza Networks Inc. - The company offers various carrier aggregation solutions such as DuoSIM-Advanced Load Tester (DuoSIM-A LT), and DuoSIM-Advanced Functional Tester (DuoSIM-A FT), DuoSIM-Advanced Environmental Simulator (DuoSIM-A ES), and NetPulse.

To make the most of the opportunities and recover from post COVID-19 impact, market vendors should focus more on the growth prospects in the fast-growing segments, while maintaining their positions in the slow-growing segments.

The carrier aggregation solutions market forecast report offers in-depth insights into key vendor profiles. The profiles include information on the production, sustainability, and prospects of the leading companies.

Carrier Aggregation Solutions Market Value Chain Analysis

Our report provides extensive information on the value chain analysis for the carrier aggregation solutions market, which vendors can leverage to gain a competitive advantage during the forecast period. The end-to-end understanding of the value chain is essential in profit margin optimization and evaluation of business strategies. The data available in our value chain analysis segment can help vendors drive costs and enhance customer services during the forecast period.

The value chain of the global communications equipment market includes the following core components:

- Inputs

- Inbound logistics

- Operations

- Outbound logistics

- Marketing and sales

- Service

- Support activities

- Innovation

The report has further elucidated other innovative approaches being followed by service providers to ensure a sustainable market presence.

Which are the Key Regions for Carrier Aggregation Solutions Market?

For more insights on the market share of various regions Request for a FREE sample now!

41% of the market’s growth will originate from APAC during the forecast period. China, India, and South Korea (Republic of Korea) are the key markets for carrier aggregation solutions market in APAC. Market growth in this region will be faster than the growth of the market in regions.

The increase in global mobile data traffic will facilitate the carrier aggregation solutions market growth in APAC over the forecast period. This market research report entails detailed information on the competitive intelligence, marketing gaps, and regional opportunities in store for vendors, which will assist in creating efficient business plans.

COVID Impact and Recovery Analysis

The outbreak of the COVID-19 pandemic in 2020 accelerated the growth of the carrier aggregation solutions market. The growing use of remote access and online connectivity increased the demand for large data capacity for maintaining network resilience, which thereby raised the demand for carrier aggregation solutions. In Japan, data traffic increased by around 30% after February 2020. Likewise, in Thailand and Laos, data traffic increased by 10%-20% after February 2020. In India, the number of broadband subscribers, including both wired and wireless, increased to around 757.6 million in January 2021. Therefore, the rising demand for high-speed data and the increasing data traffic during the pandemic are expected to drive the growth of the market in the region during the forecast period.

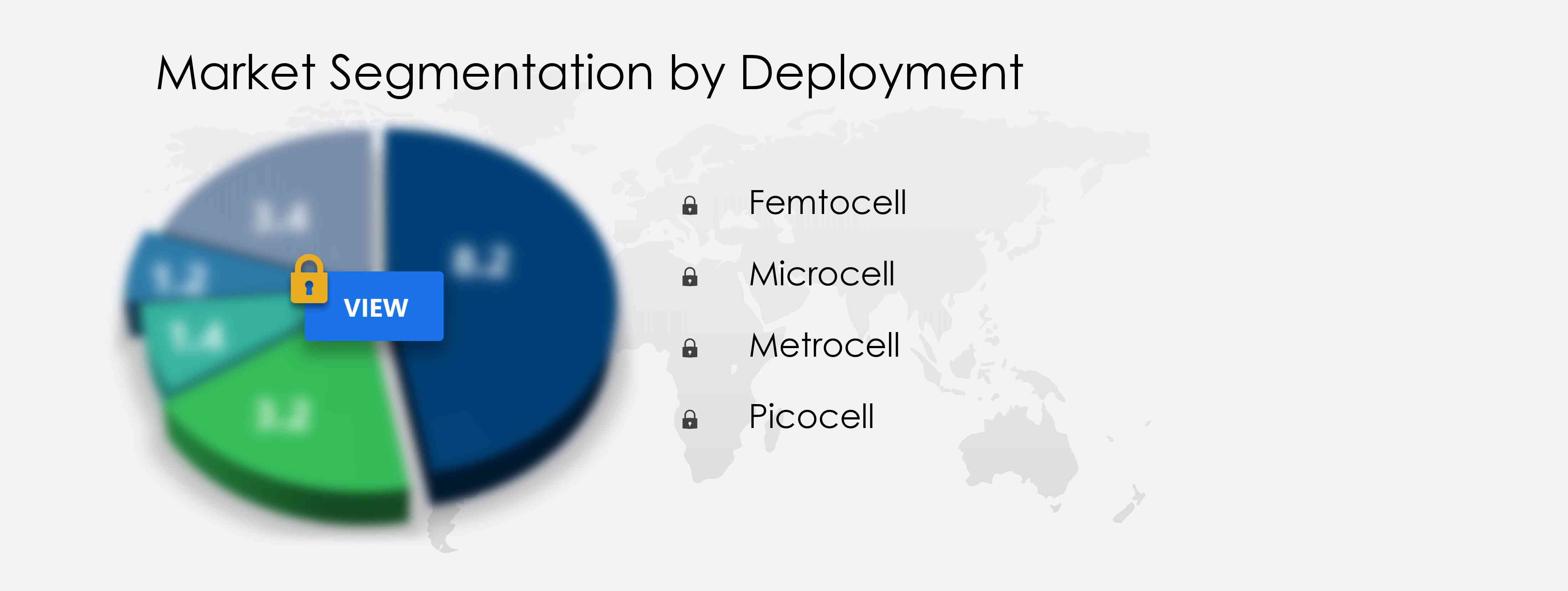

What are the Revenue-generating Deployment Segments in the Carrier Aggregation Solutions Market?

To gain further insights on the market contribution of various segments Request for a FREE sample

The carrier aggregation solutions market share growth in the Femtocell segment will be significant during the forecast period. A femtocell is used to connect to the service provider’s network using a broadband connection (such as DSL or cable). There has been a significant increase in the demand for communications from enterprises, especially for SMEs. Using a femtocell at an enterprise-level helps service providers extend coverage at the cell edge or indoors, allowing higher connectivity.

This report provides an accurate prediction of the contribution of all the segments to the growth of the carrier aggregation solutions market size and actionable market insights on post COVID-19 impact on each segment.

|

Carrier Aggregation Solutions Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

120 |

|

Base year |

2020 |

|

Forecast period |

2021-2025 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 22.9% |

|

Market growth 2021-2025 |

$ 2.42 billion |

|

Market structure |

Fragmented |

|

YoY growth (%) |

30.92 |

|

Regional analysis |

APAC, North America, Europe, MEA, and South America |

|

Performing market contribution |

APAC at 41% |

|

Key consumer countries |

US, China, UK, India, and South Korea (Republic of Korea) |

|

Competitive landscape |

Leading companies, Competitive strategies, Consumer engagement scope |

|

Key companies profiled |

Artiza Networks Inc., Broadcom Inc., Cisco Systems Inc., Huawei Investment and Holding Co. Ltd., Nokia Corp., Qorvo Inc., Rohde and Schwarz GmbH and Co. KG, Telefonaktiebolaget LM Ericsson, Verizon Communications Inc., and ZTE Corp. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Carrier Aggregation Solutions Market Report?

- CAGR of the market during the forecast period 2021-2025

- Detailed information on factors that will drive carrier aggregation solutions market growth during the next five years

- Precise estimation of the carrier aggregation solutions market size and its contribution to the parent market

- Accurate predictions on upcoming trends and changes in consumer behavior

- The growth of the carrier aggregation solutions industry across APAC, North America, Europe, MEA, and South America

- A thorough analysis of the market’s competitive landscape and detailed information on vendors

- Comprehensive details of factors that will challenge the growth of carrier aggregation solutions market vendors

We can help! Our analysts can customize this report to meet your requirements. Get in touch

RIA -

RIA -