Cast Polymer Market Size 2024-2028

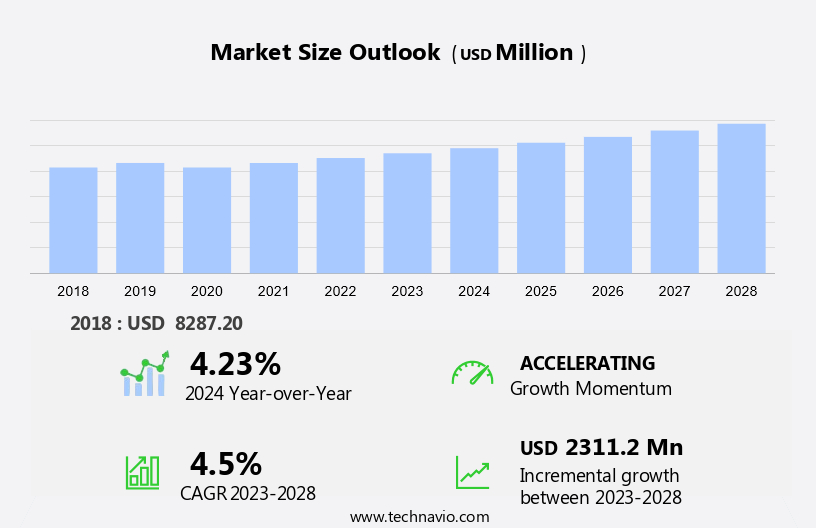

The cast polymer market size is forecast to increase by USD 2.31 billion at a CAGR of 4.5% between 2023 and 2028. The market is experiencing significant growth due to the increasing demand for this material in various applications, including countertops, shower receptors, fireplace surrounds, bathtubs, window sills, and floor tiles. One key driver of this growth is the rising population in urban areas, leading to an increased need for durable and affordable building materials. These benefits have led to their widespread use in various industries, including infrastructure, concrete blocks, construction, roof tiles and automotive. Additionally, cast polymer's ability to mimic the look and feel of natural materials, such as marble and granite, makes it an attractive alternative to traditional materials. However, the market faces challenges from substitutes like concrete, which offer lower costs but may not provide the same level of durability and aesthetic appeal as cast polymer. To stay competitive, market players must focus on innovation and improving the production efficiency of cast polymer products. By doing so, they can continue to meet the growing demand for this versatile material while maintaining a competitive edge. In summary, the market is witnessing increased adoption due to its durability, affordability, and aesthetic appeal, but faces competition from substitutes. Innovation and production efficiency are crucial for market players to remain competitive and meet the growing demand.

What will be the Size of the Market During the Forecast Period?

Cast polymer is a type of engineered material used extensively in various industries, particularly in building construction. This material is known for its high durability properties and scratch resistance, making it a popular choice for countertops, shower receptors, fireplace surrounds, and other applications. Cast polymer is produced by combining calcium carbonate and resins. The calcium carbonate provides the material with the desired aesthetic qualities, such as those found in natural marble, granite, and other natural stones. The resins offer the material its strength and durability. Solid surface products, which include cast polymer, have gained significant traction in the market due to their versatility and ease of maintenance.

Additionally, these products are used in both residential and non-residential sectors, including bathroom sinks, shower bases, vanity tops, and more. The market is driven by several factors, including the increasing demand for low-maintenance materials in building construction and the growing preference for aesthetically pleasing and durable materials. Additionally, the ability to produce cast polymer in various colors and textures, including cultured marble, cultured granite, and cultured onyx, has expanded its applications and appeal. Cast polymer's high durability properties make it an attractive alternative to natural stones like marble and granite. While natural stones have their unique beauty, they require regular maintenance and are susceptible to scratches and stains.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

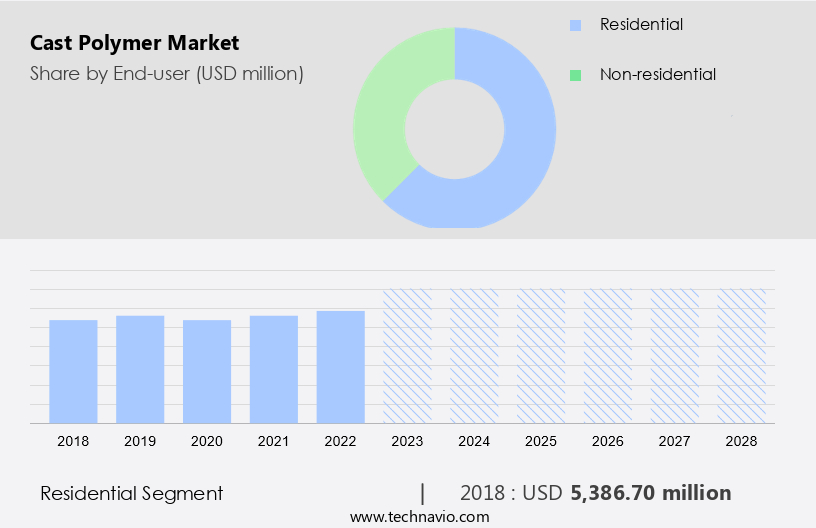

- Residential

- Non-residential

- Geography

- APAC

- China

- India

- Europe

- Germany

- UK

- North America

- US

- Middle East and Africa

- South America

- APAC

By End-user Insights

The residential segment is estimated to witness significant growth during the forecast period. The residential sector represents a significant portion of The market, with a substantial market share attributed to this application. In the United States, cast polymer products are increasingly preferred for residential applications due to their versatility, durability, and attractive appearance. These advantages have led to a growth in demand for cast polymer products in various residential applications, including countertops, vanity tops, sinks, bathtubs, shower receptors, window sills, and floor tiles.

Furthermore, cast polymers are favored for their resistance to damage and discoloration, making them a popular alternative to natural stone. The ongoing trend of home renovation and remodeling projects, coupled with the rising number of new residential constructions, is expected to fuel the growth of the market in the residential sector. Cast polymer's molding capabilities enable the creation of intricate designs and patterns, making them an excellent choice for molding accents and fireplace surrounds. In summary, the market in the United States is poised for growth, driven by the increasing popularity of these products in residential applications.

Get a glance at the market share of various segments Request Free Sample

The residential segment was valued at USD 5.39 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

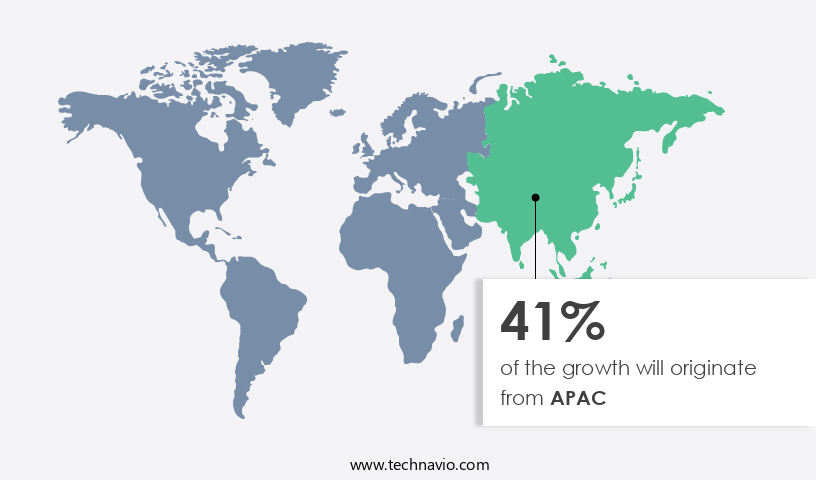

APAC is estimated to contribute 41% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The Asia Pacific (APAC) region dominates The market due to the expanding utilization of this material in both residential and non-residential sectors. The industrialization progress of major nations, including China and India, as well as the growth of manufacturing industries, have boosted the demand for cast polymers in APAC. Cast polymers, also known as engineered stones, are derived from calcium carbonate and resins.

Additionally, their usage has gained traction due to their durability, low maintenance, and aesthetic appeal. In the residential sector, cast polymers are extensively used for countertops, flooring, and wall cladding. In the non-residential sector, they are employed in the construction of commercial buildings, hospitals, and educational institutions. The market in APAC is expected to continue its growth trajectory due to these factors. The Market encompasses a wide range of applications, including countertops for kitchens and bathrooms, shower receptors, fireplace surrounds, bathtubs, window sills, gelcoats, floor tiles, pigments, and molding accents.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The rising population in urban regions is the key driver of the market. The global population is projected to reach 6 billion in urban areas by 2045, representing a significant increase from the current figure. Urbanization is crucial for economic growth, as cities contribute to over 80% of the world's GDP. However, managing this growth effectively is essential to meet the increasing demand for affordable housing, efficient transportation systems, and necessary infrastructure. Moreover, providing essential services and creating employment opportunities are vital to accommodate the expanding urban population. Despite the benefits, urbanization poses challenges. High costs of raw materials, such as natural marble and granite, can hinder the construction industry's growth. Furthermore, shipping delays can add to the expenses, impacting the timely completion of projects.

To mitigate these issues, the use of alternative materials, like cast polymers, can offer cost savings and ease shipping logistics. Cast polymers are gaining popularity due to their versatility, durability, and cost-effectiveness. They can be tinted to mimic the appearance of natural materials like marble and granite, making them an attractive alternative for construction projects. As urbanization continues to accelerate, the demand for cast polymers is expected to increase, offering potential growth opportunities for manufacturers and suppliers. In conclusion, urbanization's economic benefits are substantial, but managing its growth effectively is crucial to address the challenges posed by increasing demand for affordable housing, infrastructure, and services. Utilizing cost-effective alternatives like cast polymers can help mitigate the high costs of raw materials and shipping delays, ensuring the timely completion of projects and contributing to the long-term growth of urban areas.

Market Trends

An increasing adoption of cast polymer products is the upcoming trend in the market. The market for cast polymer products, including cultured marble, cultured granite, and cultured onyx, is experiencing significant growth due to their superior scratch resistance and high durability properties. These attributes make cast polymer products an attractive alternative to natural stones in various applications. In the non-residential sector, the demand for cast polymer products is increasing due to their resistance to biological contamination, making them ideal for use in hospitals and schools. Moreover, cast polymer products offer high durability properties and scratch resistance, making them a popular choice for various applications, such as whirlpool baths, vanities, enclosure sets, wall panels, colorants, and lavatories.

Also, the affordability and availability of cast polymer products in various colors, sizes, and types have led to their increased adoption in remodeling and construction activities. Cast polymer products are replicas of natural stones, created by combining a specific blend of polyester resin, catalyst, fillers, and pigments to meet strength requirements and provide the durability benefits that consumers expect from composite materials. The versatility and popularity of cast polymer products have made them a preferred choice in commercial, industrial, residential, and medical applications. Their beauty and strength make them an excellent option for creating visually appealing and long-lasting surfaces. With the continuous advancements in technology and manufacturing processes, the future of the market looks promising.

Market Challenge

The threats from substitutes such as concrete is a key challenge affecting the market growth. The usage of cast polymers is experiencing significant growth in various commercial applications, particularly in the manufacturing of vanity tops for bathrooms and kitchens. This trend is driven by the material's cost-effectiveness and widespread availability compared to other construction materials such as steel and certain specialty polymers. Cast polymers are composed primarily of resins, fillers, and additives, making them a versatile alternative for various applications. In the realm of commercial construction, cast polymers have gained popularity for their suitability in the production of window sills and shower bases. Their resistance to water and chemicals makes them an ideal choice for these applications, ensuring low maintenance activity and durability.

Furthermore, the recyclability of industrial wastes, such as fly ash, slag, waste glass, and even ground vehicle tires, as substitutes for cement or aggregate in cast polymer production, adds to their environmental appeal. In the US market, the demand for cast polymers is on the rise due to their cost-effective nature and ease of use. Their versatility in various applications, including vanity tops, window sills, and shower bases, makes them a preferred choice for commercial projects. Cast polymers offer a sustainable solution by utilizing industrial wastes as substitutes for traditional cement and aggregate components. This not only reduces the overall cost but also contributes to a more eco-friendly construction industry.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

AGCO Corp: The company offers cast polymers such as Granite, Limestone, Marble, Quartzite, Semi Precious Stones, Soapstone, Alkemi, Curava, Durat, PaperStone, and IceStone.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aristech Surfaces LLC

- BLANCO GmbH and Co. KG

- Bradley Corp.

- Breton S.p.A.

- Caesarstone Ltd

- Compac

- Cosentino SA

- DuPont de Nemours Inc.

- Eastern Surfaces

- J M Huber Corp.

- Kaneka Corp.

- Kingkonree International China Surface Industrial Co. Ltd.

- Link Composites Pvt. Ltd.

- Oppein Home Group Inc.

- Swan Corp.

- The RJ Marshall Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is witnessing significant growth due to the increasing demand for solid surface products in both residential and non-residential sectors. These products, including countertops, shower receptors, fireplace surrounds, bathtubs, window sills, floor tiles, molding accents, whirlpool baths, vanities, enclosure sets, and wall panels, offer high durability properties and scratch resistance. The use of calcium carbonate, resins, and natural stone in the production of cast polymers contributes to their mechanical properties, making them suitable for various applications. Solid surface products, such as cultured marble, cultured granite, and cultured onyx, are gaining popularity due to their affordability and versatility compared to natural marble, granite, and other natural stones.

However, the high cost of raw materials and the ongoing issue of raw material shortages and shipping delays pose challenges to market growth. The market is segmented into residential and non-residential sectors, with commercial applications accounting for a significant share. Maintenance activity and building construction are the primary end-users. The market is expected to continue growing, driven by increasing demand for solid surface products in various applications.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

143 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market Growth 2024-2028 |

USD 2.31 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Regional analysis |

APAC, Europe, North America, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 41% |

|

Key countries |

China, US, Germany, India, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

AGCO Corp., Aristech Surfaces LLC, BLANCO GmbH and Co. KG, Bradley Corp., Breton S.p.A., Caesarstone Ltd, Compac, Cosentino SA, DuPont de Nemours Inc., Eastern Surfaces, J M Huber Corp., Kaneka Corp., Kingkonree International China Surface Industrial Co. Ltd., Link Composites Pvt. Ltd., Oppein Home Group Inc., Swan Corp., and The RJ Marshall Co. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -