Commercial Aircraft Airframe Materials Market Forecast 2024-2028

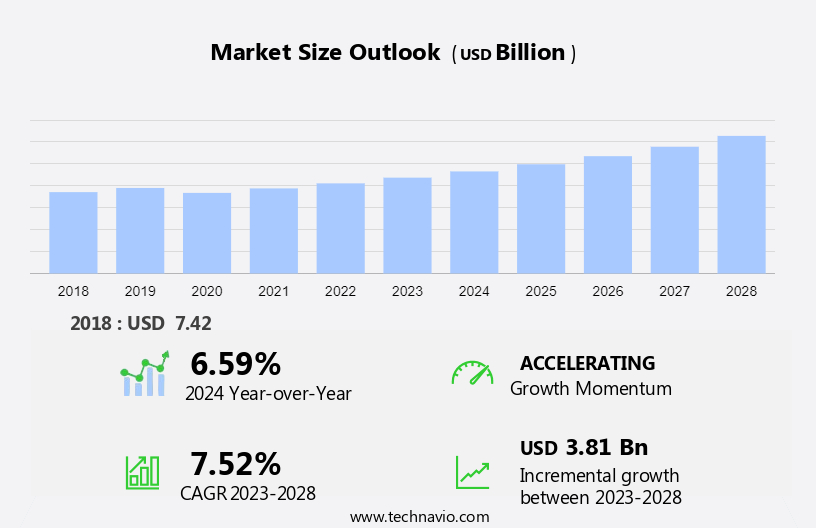

The commercial aircraft airframe materials market size is forecast to increase by USD 3.81 billion, at a CAGR of 7.52% between 2023 and 2028.

Market growth hinges on various factors including rising air travel demand, expanded air routes, and increased utilization of composites in commercial aircraft airframes. The surge in demand for air travel underscores the need for more efficient and reliable aircraft, driving advancements in materials like composites. With the expansion of air routes, airlines seek to cater to growing passenger needs, fostering the continuous evolution of the aviation industry towards greater efficiency and sustainability. Our report examines historical data from 2018 - 2022, besides analyzing the current and forecasted market scenario.

Moreover, the market in North America is driven by leading manufacturers like Boeing, Bombardier, and Embraer, renowned for their commercial aircraft and business jets. Moreover, the region benefits from fleet expansions by airline operators, who are increasingly opting for newer aircraft over older ones. This preference fuels demand for commercial airframe components. Arconic Corp provides a range of commercial aircraft airframe materials, while BASF SE offers various materials including Elastollan Thermoplastic Polyurethane and Ultrason PES for airframe applications.

Market Forecasting and Size

Market Forecast 2024-2028

To learn more about this report, Request Free Sample

Market Dynamic

The market is driven by a myriad of factors such as superior performance properties required to withstand harsh conditions and accommodate newer aircraft designs. The emergence of low-cost carriers and the growth of emerging economies spur demand, while aerospace companies navigate challenges like travel restrictions and supply chain disruptions. With composites gaining popularity and aluminum alloy segments dominating, the market faces complexities in regulatory compliance and meeting stringent safety standards amidst rapid technological advancements and increasing demand from both civil and military sectors. Our researchers studied the market research and growth data for years, with 2023 as the base year and 2024 as the estimated year, and presented the key drivers, trends, and challenges for the market.

Key Market Driver - Increasing demand for air travel

The surge in passenger and cargo demand drives increased utilization of aircraft fleets, necessitating more frequent maintenance, repair, and overhaul (MRO) activities. Factors such as the growth of the middle class in emerging economies like China, India, and Brazil have substantially expanded the pool of air travelers. Rapid urbanization also contributes, as more people migrate to cities seeking better opportunities and quality of life, increasing demand for air travel. The major aircraft manufacturing companies include Boeing 737MAX, Malaysian Airlines, Ethiopian Airlines, Airbus etc.

Additionally, advancements in aviation technology, aircraft design, and airline route networks have made air travel more convenient, affordable, and accessible. The proliferation of low-cost carriers, airline alliances, and new routes further enhances connectivity between cities and regions, stimulating air travel demand. Some of the superior materials that are included in the manufacturing of the passenger air travel segment include aluminum alloy segment, steel, and iron. This increased demand results in higher utilization of aircraft, prompting more frequent flights and longer operating hours, thus accelerating the need for commercial aircraft airframe materials. Hence, such factors are driving the market growth during the forecast period.

Significant Market Trends - Rising adoption of carbon fiber-reinforced plastic composites in aircraft components

The rising trend in the global market is the increasing use of carbon fiber-reinforced polymer (CFRP) composites in different aircraft components. In addition, CFRP composites are used because of their exceptional strength-to-weight ratio, which is critical for improving airplane performance and fuel efficiency. Furthermore, this lightweight feature not only reduces the overall weight of airplane components but also significantly reduces fuel consumption and emissions, which aligns with the aviation industry's growing emphasis on environmental sustainability.

Moreover, CFRP composites provide design flexibility, allowing for the creation of complex and aerodynamic structures. In addition, this flexibility enables airplane manufacturers to optimize component design, resulting in higher efficiency and aerodynamics. Furthermore, the corrosion-resistant nature of CFRP composites fuels the durability of airplane components, lowering maintenance and operational costs over the aircraft's life cycle. Hence, such factors are driving the market growth during the forecast period.

Major Market Challenge - Volatility in raw material prices

The prices of raw materials that are utilized for the production of commercial aircraft airframe materials are volatile. In addition, the high demand-to-supply ratio, high taxes, duties and additional tariffs, and production disruptions in metal ore-mining countries can lead to an increase in raw material prices. Furthermore, such scenarios have been pushing airplane original equipment manufacturers (OEMs) to procure raw materials before the scheduled production to keep the price and product mix at controllable levels.

Moreover, airplane OEMs and their suppliers are also on the lookout for additional substitution opportunities to reduce the cost and amount of materials required for the construction of individual airframe components, such as fuselages, doors, and wings, among others. In addition, raw material costs account for a major share of the total expenditure incurred by commercial airframe component manufacturers. Therefore, any unanticipated fluctuations in raw material prices put pressure on these manufacturers, as an abrupt or unforeseen price rise can affect their overall profit margins. Hence, such factors are hindering the market growth during the forecast period.

Market Segmentation by Type, Material and Geography

Type Segment Analysis:

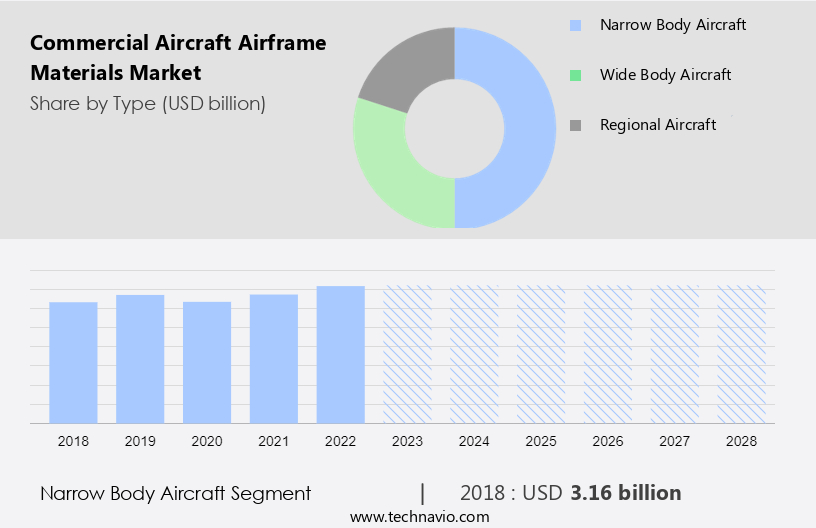

The narrow body aircraft segment is estimated to witness significant growth during the forecast period. Narrow-body aircraft segments have a single aisle inside the cabin, and the passengers are seated in two axial groups. In addition, this segment has a twin-engine setup, which is integrated into the wings to provide thrust. Furthermore, the demand for such aircraft is driven by the efficiency-focused operations of aircraft carriers in emerging and developed economies, where average load factors and seasonality play vital roles in determining their profit margins.

Customised Report as per your requirements!

The narrow body aircraft segment was the largest segment and was valued at USD 3.16 billion in 2018. Moreover, the procurement of new aircraft is increasing the demand for aircraft airframe modifications to match the specifications and themes of airline operators. In addition, low-cost carriers (LCCs) are adding seats to ensure optimum revenue per flight. Furthermore, in this regard, several carriers have reconfigured their fleet to include more seats and reduce the size of lavatories. Furthermore, JetBlue Airways Corp. (JetBlue) is increasing the seating capacity of its A320s from 150 seats to 162. Hence, such factors are fuelling the growth of this segment which in turn drives the market growth during the forecast period.

Material Segment Analysis:

Based on the material, the market has been segmented into aluminum alloys, titanium alloys, composites, and steel alloys. The aluminum alloys segment will account for the largest share of this segment. Aluminum alloy segments are mainly recognized for their exceptional strength-to-weight ratio, corrosion resistance, and versatility, making them a preferred choice in aerospace applications. In addition, this segment is further categorized based on different types of aluminum alloys, each catering to specific industry needs. Moreover, generally, 2000 series alloys are one of the most important types of alloys used in the aerospace industry, especially in the construction of wings and fuselage. Furthermore, due to the benefits of aluminum, companies offering aluminum alloys are focusing on expanding their manufacturing facilities. Hence, such factors are fuelling the growth of this segment which in turn drives the market growth during the forecast period.

Regional Analysis

For more insights on the market share of various regions Download Sample PDF now!

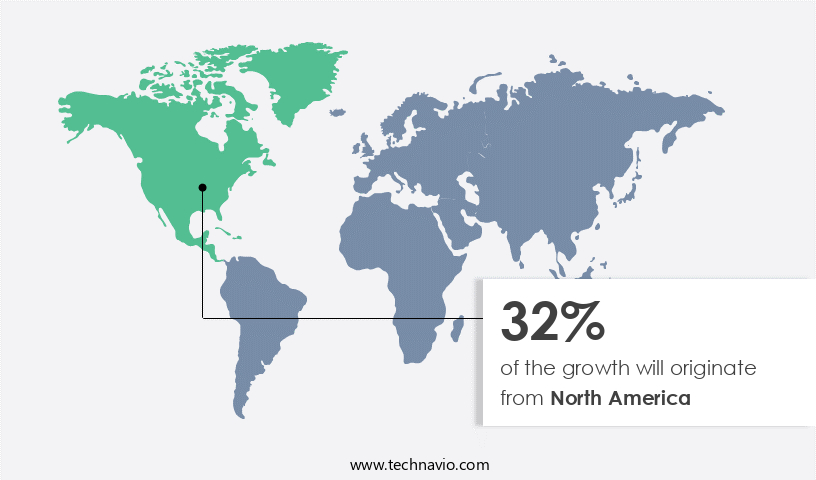

North America is estimated to contribute 32% to the growth by 2028. Technavio's analysts have provided extensive insight into the market forecasting, detailing the regional trends and drivers influencing the market's trajectory throughout the forecast period. Several companies such as Boeing often engage in research and development (R&D) projects with manufacturers of commercial airframe components and these companies are mainly based in North America. In addition, the US is witnessing a continuous flow of investments into the development of advanced airframe components that can be integrated into modern commercial aircraft such as the Boeing 787.

Moreover, although Canada accounts for a considerable share of the regional market in focus, the market is primarily dominated by the US. In addition, a large number of these aircraft will translate into higher investments in the market in focus. Furthermore, the Boeing Company, headquartered in Chicago, develops a number of patents related to airframe components that are used in its commercial aircraft. Hence, such factors are driving the market growth in North America during the forecast period.

Who are the Major Market Companies?

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Constellium SE: The company offers commercial aircraft airframe materials such as rolled and extruded aluminium products for key structural aircraft applications including fuselage and wing skins, ribs, spars, doublers, stiffeners, window frames, bulkheads, floor structures, seat tracks, and various other internal structure components.

We also have detailed analyses of the market’s competitive landscape and offer information on 20 market companies, including:

ATI Inc., DuPont de Nemours Inc., Hexcel Corp., Honeywell International Inc., Huntsman International LLC, Kaiser Aluminum Corp., Materion Corp., Mitsubishi Motors Corp., Norsk Titanium AS, SGL Carbon SE, Solvay SA, Southwest Aluminum (Kunshan) Co. Ltd., Tata Sons Pvt. Ltd., Teijin Ltd., thyssenkrupp AG, Toray Industries Inc., and VSMPO AVISMA Corp.

Technavio market forecast the an in-depth analysis of the market and its players through combined qualitative and quantitative data. The analysis classifies companies into categories based on their business approaches, including pure-play, category-focused, industry-focused, and diversified. Companies are specially categorized into dominant, leading, strong, tentative, and weak, based on their quantitative data analysis.

Segment Overview

The market analysis and report forecasts market growth by revenue at global, regional & country levels and provides a market growth analysis of the latest trends and growth opportunities from 2018 to 2028.

- Type Outlook

- Narrow body aircraft

- Wide body aircraft

- Regional aircraft

- Material Outlook

- Aluminum alloys

- Titanium alloys

- Composites

- Steel alloys

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- The U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- South America

- Chile

- Argentina

- Brazil

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

Market Analyst Overview

The Market is influenced by several factors that shape its dynamics and growth trajectory. Superior performance properties of materials are essential, especially considering the harsh conditions commercial aircraft encounter during operation. With the introduction of newer airplane models like the Boeing 737MAX and advancements in the UAV market, there's a growing demand for aerospace materials in the global aerospace industry. Additionally, factors like technological advancements, rising demand, and favorable government policies contribute to market growth.

However, challenges such as supply chain disruptions, policy uncertainty, and competing technologies like fossil fuels and nuclear energy pose significant obstacles. Environmental concerns, including carbon emissions and noise pollution, also impact market dynamics. Overcoming these challenges requires regulatory support, innovative manufacturing processes, and sustainable practices to address growing consumer awareness and demand for eco-friendly products. While the market holds growth prospects driven by efficiency and effectiveness in manufacturing, addressing limitations like infrastructure constraints and limited awareness remains crucial for sustainable growth.

Moreover, the Market is characterized by a competitive landscape with established players and new entrants vying for market share. Understanding industry patterns, market movements, and geographical regions is essential for stakeholders to make well-informed decisions and capitalize on industry growth potential in key segments like wide-body airplane.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

170 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.52% |

|

Market Growth 2024-2028 |

USD 3.81 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.59 |

|

Regional analysis |

North America, Europe, APAC, Middle East and Africa, and South America |

|

Performing market contribution |

North America at 32% |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Arconic Corp., ATI Inc., BASF SE, Constellium SE, DuPont de Nemours Inc., Hexcel Corp., Honeywell International Inc., Huntsman International LLC, Kaiser Aluminum Corp., Materion Corp., Mitsubishi Motors Corp., Norsk Titanium AS, SGL Carbon SE, Solvay SA, Southwest Aluminum (Kunshan) Co. Ltd., Tata Sons Pvt. Ltd., Teijin Ltd., thyssenkrupp AG, Toray Industries Inc., and VSMPO AVISMA Corp. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the growth of the market between 2023 and 2028

- Precise estimation of the market growth and trends and its contribution to the market in focus on the parent market

- Accurate predictions about upcoming market trends and analysis and changes in consumer behavior

- Market growth and forecasting across North America, Europe, APAC, Middle East and Africa, and South America

- A thorough market analysis and report of the market’s competitive landscape and detailed information about companies

- Comprehensive market report analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -