Cutting Tool Inserts Market Size 2026-2030

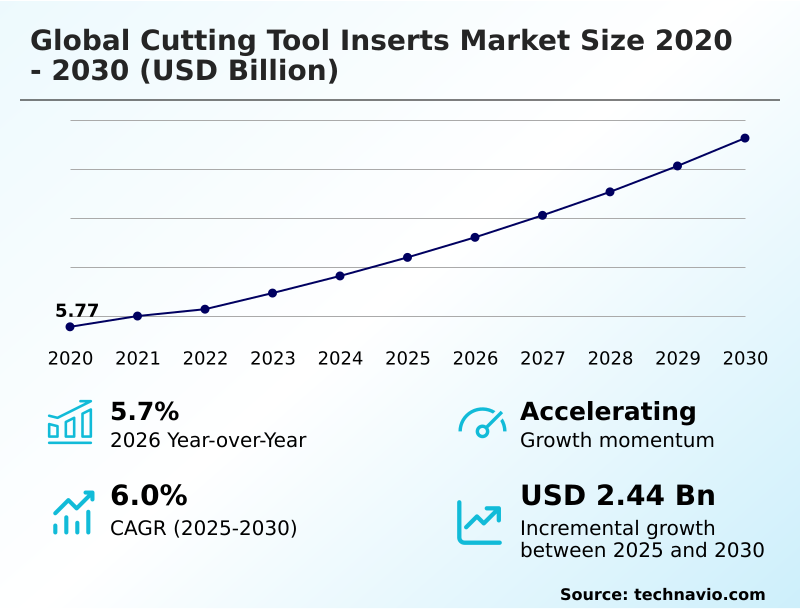

The cutting tool inserts market size is valued to increase by USD 2.44 billion, at a CAGR of 6% from 2025 to 2030. Advancements in coating technologies and substrate innovations will drive the cutting tool inserts market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 57.6% growth during the forecast period.

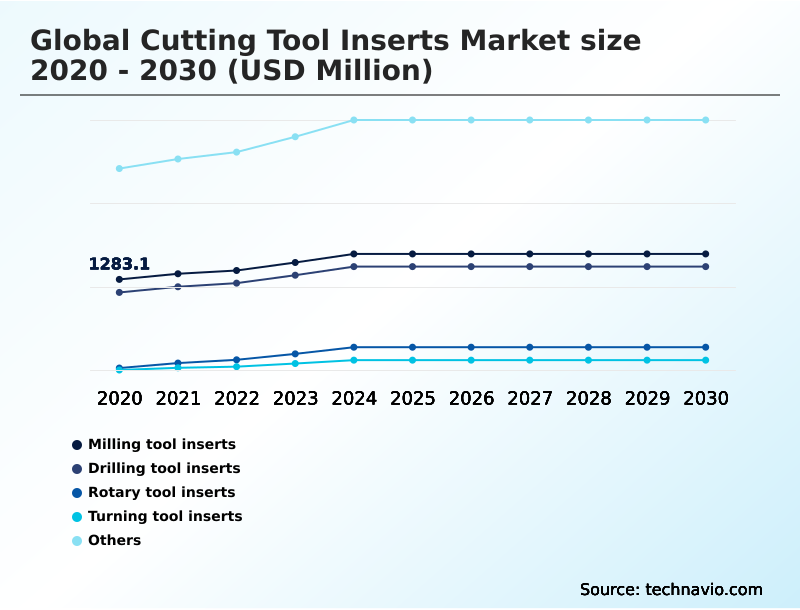

- By Application - Milling tool inserts segment was valued at USD 1.49 billion in 2024

- By Type - Carbide tool inserts segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.86 billion

- Market Future Opportunities: USD 2.44 billion

- CAGR from 2025 to 2030 : 6%

Market Summary

- The cutting tool inserts market is fundamentally shaped by the industrial pursuit of higher efficiency and precision. Innovations are centered on material science, particularly the development of advanced carbide inserts, ceramic inserts, and cermet inserts, enhanced by PVD coatings and CVD coatings to achieve superior wear resistance and thermal stability.

- The aerospace sector's demand for tooling capable of handling heat-resistant superalloys (HRSA) drives the creation of specialized grades like whisker-reinforced ceramics, while the automotive shift to electric vehicles requires solutions for lightweight materials. A key challenge is the raw material price volatility of elements like tungsten.

- To counteract this and a persistent manufacturing skills gap, a modern machine shop might implement tool wear monitoring and a digital twin for machining process simulation. This strategy supports lights-out manufacturing, ensures process reliability, and optimizes tool life, thereby improving operational efficiency and reducing dependency on manual oversight.

What will be the Size of the Cutting Tool Inserts Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Cutting Tool Inserts Market Segmented?

The cutting tool inserts industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Milling tool inserts

- Drilling tool inserts

- Rotary tool inserts

- Turning tool inserts

- Others

- Type

- Carbide tool inserts

- CBN inserts

- Ceramic inserts

- Others

- Product type

- Metal machining

- Plastic machining

- Woodworking

- Composite materials

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- Italy

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Application Insights

The milling tool inserts segment is estimated to witness significant growth during the forecast period.

The milling tool inserts segment is driven by the increasing design complexity in the aerospace, automotive, and die and mold industries. These inserts must withstand intermittent cutting forces, requiring superior substrate toughness and coating adhesion.

The market is shifting towards high feed milling and shoulder milling solutions that offer versatility. There is a demand for inserts with complex micro-geometries and reinforced cutting edges to improve process security by over 15% in unattended machining operations.

Key innovations in this area include advanced PVD coatings and cermet inserts for enhanced performance. The integration of vibration-dampening features and optimized chip gullet designs are now standard requirements, particularly for machining hard materials and achieving high-quality surface integrity.

The Milling tool inserts segment was valued at USD 1.49 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 57.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cutting Tool Inserts Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the global cutting tool inserts market 2026-2030 is led by the APAC region, which accounts for over 57% of the incremental growth opportunity, fueled by large-scale industrial upgrades.

In this region, a focus on high-volume production drives demand for solutions that ensure consistent chip control.

In contrast, Europe is defined by its focus on precision engineering and sustainability, with manufacturers widely adopting dry machining techniques to achieve energy efficiency improvements of 15%.

This has spurred the development of green tools and a transparent product carbon footprint (PCF) system.

North America's market is shaped by the aerospace sector and the automotive transition to EVs, creating strong demand for PCD tooling for aluminum battery housings and inserts for monolithic components, reflecting a focus on high-performance, specialized applications.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Addressing complex manufacturing challenges is central to the evolution of the cutting tool inserts market. The difficulty of machining heat-resistant superalloys with ceramics is being met with new insert grades that offer superior performance and reliability. In parallel, the adoption of CBN insert grades for hard turning continues to displace traditional grinding, offering faster cycle times and better geometric control.

- The automotive industry's pivot to electric vehicles is creating a new set of requirements, with a focus on PCD tooling for aluminum battery housings and effective strategies for lightweight composite material drilling. This shift underscores the need for advanced tooling that can handle abrasive and non-ferrous materials efficiently.

- Across all sectors, sustainability in cemented carbide production is now a strategic priority, compelling manufacturers to innovate in recycling and material sourcing. The need to improve process development is also critical; firms adopting digital twin for machining process simulation report a reduction in new process development time that is twice as fast as traditional trial-and-error methods.

- This digital approach is key to optimizing chip control in stainless steel, implementing advanced coatings for dry machining applications, and reducing tool wear in composite machining. Furthermore, it helps manufacturers manage the intricacies of high-pressure coolant for deep-hole drilling and select the optimal PVD coating for high-speed steel turning, ensuring efficiency and cost-effectiveness.

What are the key market drivers leading to the rise in the adoption of Cutting Tool Inserts Industry?

- Advancements in coating technologies and substrate innovations are key drivers of the market, enabling higher machining speeds and improved tool performance.

- Market growth is significantly driven by advancements in coating technologies and the demands of high-performance industries.

- The resurgence of the aerospace sector, for example, is increasing the need for specialized inserts for heat-resistant superalloys (HRSA), with optimized ceramic grades enabling a 50% increase in cutting speeds over traditional carbide.

- In the automotive sector, the pursuit of efficiency is fueling the adoption of high-speed machining. This, combined with an advanced PVD coating, can double the number of components produced per cutting edge through superior tool life optimization.

- Furthermore, these coating innovations are critical enablers of dry machining and minimum quantity lubrication (MQL), strategies that can reduce coolant-related operational costs by nearly 100%, aligning with both economic and environmental objectives.

What are the market trends shaping the Cutting Tool Inserts Industry?

- The accelerated development and adoption of high-performance materials and advanced coating technologies is a significant trend. This is reshaping the capabilities and efficiency of cutting tool inserts across manufacturing sectors.

- Key market trends are centered on digitalization and the imperative of a circular supply chain. Leading manufacturers are now achieving recycled content ratios of over 80% in select product lines, creating a new benchmark for sustainability.

- Concurrently, the adoption of smart tooling is accelerating, with tool wear monitoring systems reducing premature insert changes and saving up to 20% in annual consumable costs. This is complemented by the use of a digital twin for machining process simulation, a technology that has been shown to improve first-part-right rates by over 15%.

- This digital ecosystem, which includes high-performance grades for strategic industries, is crucial for enabling lights-out manufacturing and enhancing process reliability without constant human intervention. The evolution towards a data-driven approach is reshaping how tool life optimization and inventory management are handled.

What challenges does the Cutting Tool Inserts Industry face during its growth?

- Raw material price volatility and supply chain insecurity present a key challenge affecting industry growth, particularly concerning the supply of tungsten and cobalt.

- The market faces significant challenges from raw material price volatility and the ongoing manufacturing skills gap. Geopolitical concentration of key materials like tungsten can lead to price fluctuations exceeding 30% during volatile periods, directly impacting production costs and the viability of just-in-time manufacturing. This supply chain insecurity is a major constraint.

- Furthermore, the skills deficit means that suboptimal tool application by inexperienced operators can reduce material removal rates by as much as 40% compared to benchmarks. This inefficiency is compounded by the structural shift to electric vehicles, which reduces demand for the heavy-duty roughing grades used in traditional engine manufacturing, altering the market's historical volume base.

- These factors necessitate a strategic focus on recycling, automation, and workforce training to ensure long-term stability and growth.

Exclusive Technavio Analysis on Customer Landscape

The cutting tool inserts market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cutting tool inserts market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cutting Tool Inserts Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cutting tool inserts market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ARCH Cutting Tools - Provides a portfolio of high-performance cutting tool inserts, featuring advanced carbide and ceramic grades, for optimizing precision machining across multiple industrial sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ARCH Cutting Tools

- Asahi Diamond Industrial Ltd.

- B.R. Meccanica Italy

- CERATIZIT SA

- Element Six UK Ltd.

- ILJIN Diamond Co. Ltd.

- International Metalworking Co

- ISCAR Ltd.

- Kennametal Inc.

- Knight Carbide Inc.

- KYOCERA Corp.

- LOVEJOY Tool Co. Inc.

- Mitsubishi Materials Corp.

- NACHI FUJIKOSHI Corp.

- Sandvik AB

- Seco Tools AB

- Sumitomo Corp.

- Tungaloy Corp.

- Tyrolit Schleifmittelwerke KG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cutting tool inserts market

- In October 2024, Sandvik announced the acquisition of Buffalo Tungsten Inc. to strengthen its regional supply chain resilience and secure upstream raw material supply for its cemented carbide products.

- In September 2024, Kennametal Inc. introduced the KCP25C steel turning grade, featuring its proprietary KENGold coating technology to enhance wear identification and maximize cutting edge utilization.

- In September 2024, the Ceratizit Group introduced a Product Carbon Footprint (PCF) classification system, providing customers with detailed data on carbon emissions associated with specific carbide grades.

- In April 2025, NTK Cutting Tools launched the SX9 ceramic grade, a silicon nitride-based insert engineered with high fracture resistance for the rough machining of gray cast iron.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cutting Tool Inserts Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 310 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6% |

| Market growth 2026-2030 | USD 2439.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.7% |

| Key countries | China, Japan, India, South Korea, Taiwan, Indonesia, Germany, Italy, France, UK, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Egypt and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The cutting tool inserts market is defined by a relentless drive for operational efficiency through advancements in material science and surface engineering. The foundation of the market remains carbide inserts, CBN inserts, and ceramic inserts, which are continually enhanced with sophisticated PVD coatings and CVD coatings to push performance boundaries.

- A significant boardroom-level trend is the focus on sustainability in cemented carbide production, where the use of recycled carbide to create green tools is now a key factor in supply chain risk mitigation and ESG compliance.

- Technologically, innovations such as functionally graded substrates, whisker-reinforced ceramics, and nanostructured coatings are critical for machining difficult materials like heat-resistant superalloys (HRSA) and for enabling high-speed machining. The adoption of advanced cermet inserts for finishing operations has demonstrated a 30% reduction in cycle times.

- Concurrently, the growth in electronics and electric vehicles has amplified the importance of PCD inserts and DLC coating for processing non-ferrous and composite materials, with specialized tooling like indexable drilling inserts and exchangeable tip solutions becoming standard.

What are the Key Data Covered in this Cutting Tool Inserts Market Research and Growth Report?

-

What is the expected growth of the Cutting Tool Inserts Market between 2026 and 2030?

-

USD 2.44 billion, at a CAGR of 6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Milling tool inserts, Drilling tool inserts, Rotary tool inserts, Turning tool inserts, and Others), Type (Carbide tool inserts, CBN inserts, Ceramic inserts, and Others), Product Type (Metal machining, Plastic machining, Woodworking, and Composite materials) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Advancements in coating technologies and substrate innovations, Raw material price volatility and supply chain insecurity

-

-

Who are the major players in the Cutting Tool Inserts Market?

-

ARCH Cutting Tools, Asahi Diamond Industrial Ltd., B.R. Meccanica Italy, CERATIZIT SA, Element Six UK Ltd., ILJIN Diamond Co. Ltd., International Metalworking Co, ISCAR Ltd., Kennametal Inc., Knight Carbide Inc., KYOCERA Corp., LOVEJOY Tool Co. Inc., Mitsubishi Materials Corp., NACHI FUJIKOSHI Corp., Sandvik AB, Seco Tools AB, Sumitomo Corp., Tungaloy Corp. and Tyrolit Schleifmittelwerke KG

-

Market Research Insights

- Market dynamics are shifting from general-purpose tooling to specialized solutions focused on measurable outcomes. Enhanced process reliability in high-value component manufacturing is leading to scrap reductions of up to 25%. Concurrently, tool life optimization strategies in abrasive material applications are extending insert longevity by over 40%, directly impacting cost per part reduction.

- The focus on consistent chip control and thermal stability has become critical for enabling lights-out manufacturing, which has been shown to improve operational uptime by more than 15%. This transition highlights a move toward data-driven performance where the selection of cutting tool inserts is tied to specific gains in productivity, waste reduction, and automation efficiency.

We can help! Our analysts can customize this cutting tool inserts market research report to meet your requirements.

RIA -

RIA -