Flat Panel Display Equipment Market Size 2025-2029

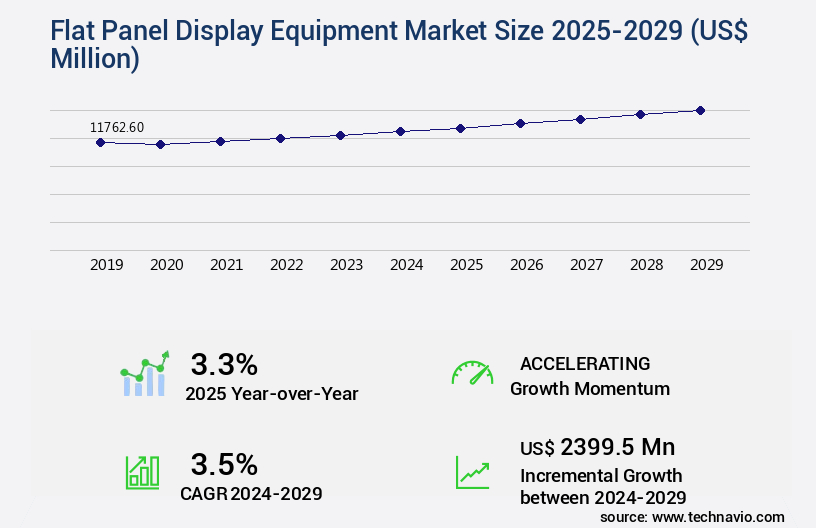

The flat panel display equipment market size is valued to increase by USD 2.4 billion, at a CAGR of 3.5% from 2024 to 2029. Production capacity expansion of display manufacturers will drive the flat panel display equipment market.

Major Market Trends & Insights

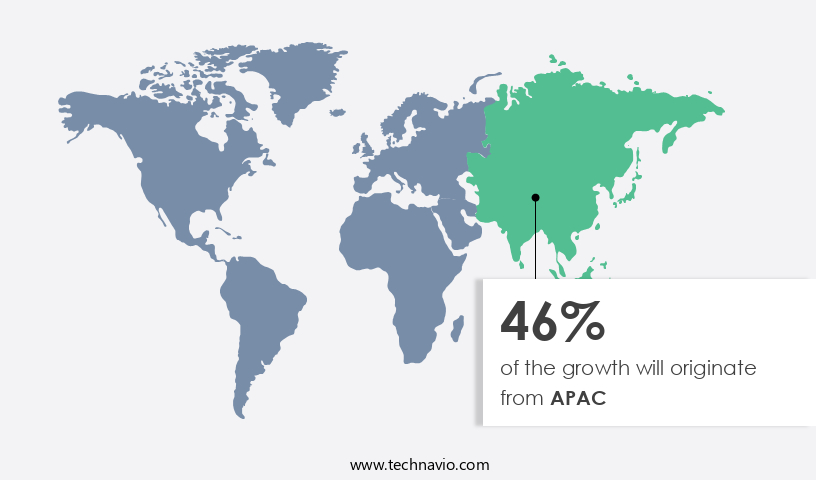

- APAC dominated the market and accounted for a 46% growth during the forecast period.

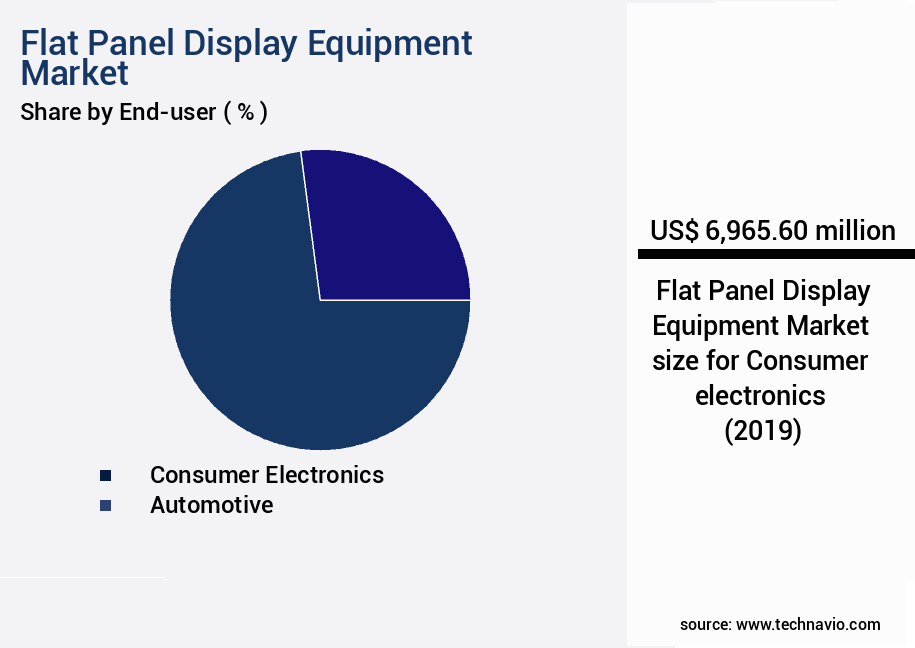

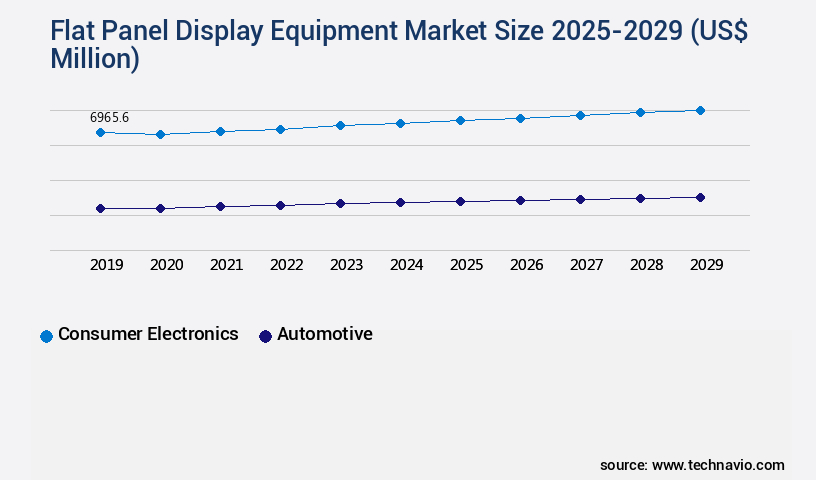

- By End-user - Consumer electronics segment was valued at USD 6.97 billion in 2023

- By Technology - a-Si segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 30.39 million

- Market Future Opportunities: USD 2399.50 million

- CAGR from 2024 to 2029 : 3.5%

Market Summary

- The market is experiencing significant growth, driven by the increasing adoption of touch-enabled digital signage and production capacity expansion among display manufacturers. According to recent research, the touch screen market is projected to reach a value of over USD35 billion by 2025, growing at a steady pace due to the rising demand for interactive displays in various industries such as retail, healthcare, and hospitality. However, the flat panel display industry faces challenges as well. One major risk is the rapid technological advancements leading to short product lifecycles and increasing pressure on manufacturers to innovate continually.

- Another challenge is the growing concern for energy efficiency and environmental sustainability, which requires display manufacturers to invest in research and development of eco-friendly technologies. A real-world business scenario illustrating the importance of flat panel display equipment in operational efficiency is a retail chain optimizing its supply chain. By implementing real-time inventory management systems using digital displays, the retailer can reduce stockouts and overstocks, leading to a 15% increase in sales and a 12% decrease in inventory holding costs. Additionally, the use of energy-efficient displays can help the retailer save up to 20% on energy costs, contributing to overall cost savings and sustainability efforts.

What will be the Size of the Flat Panel Display Equipment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Flat Panel Display Equipment Market Segmented ?

The flat panel display equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Consumer electronics

- Automotive

- Others

- Technology

- a-Si

- LTPS

- Application

- Smartphones

- Televisions

- Automotive displays

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By End-user Insights

The consumer electronics segment is estimated to witness significant growth during the forecast period.

The market is experiencing continuous growth, driven by the increasing demand for advanced display technologies in various industries. In the consumer electronics sector, the adoption of quantum dot displays, OLEDs, and LEDs is escalating, particularly for smartphones, tablets, laptops, and TVs. The preference for high-resolution and vibrant color displays is fueling the market expansion. For instance, in the personal computer segment, the market decline rate slowed in 2023, with a 16.6% decrease in PC shipments during the second quarter.

Despite this, the industry remains dynamic, with ongoing advancements in manufacturing processes, such as liquid crystal alignment, heat dissipation management, and backlight module assembly, to optimize yield and improve power consumption efficiency. Additionally, advancements in panel manufacturing processes, image compression techniques, and display driver ICs contribute to the market's evolution.

The Consumer electronics segment was valued at USD 6.97 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 46% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Flat Panel Display Equipment Market Demand is Rising in APAC Request Free Sample

The market is experiencing dynamic growth, with the North American region emerging as a significant contributor. Although the North American contribution was historically lower due to a lower concentration of Original Equipment Manufacturers (OEMs), major players such as Apple, Google, and Microsoft, which produce LCD-based products like iPads and MacBooks, are driving market expansion in the region. The Americas have consistently adopted new technology, including electronic equipment and tools, at a rapid pace. This trend is particularly evident in the education sector, where the availability of digital devices and improved Internet connectivity has led to the proliferation of e-learning and digital classrooms.

According to industry reports, the North American the market is projected to grow at a robust rate, surpassing the growth in the Asia Pacific region. This growth is attributed to the increasing demand for advanced display technologies in various end-use industries, including healthcare, automotive, and consumer electronics.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth, driven by advancements in technology and increasing demand for high-quality displays. One of the key trends in this market is the adoption of advanced thin-film transistor technology, which enables high-resolution display panel production with improved color gamut and wide viewing angles. Energy-efficient backlight module designs, automated optical inspection systems, and precision liquid crystal alignment processes are also crucial elements in the production of next-generation displays. Manufacturers are investing in the development of next-generation display driver ICs and advanced image processing algorithms to enhance display performance and enable high-speed data transmission protocols. Effective heat dissipation solutions are also essential to ensure the reliability and durability of display panels, particularly in large-scale manufacturing operations. Robust panel durability testing and high-yield display panel manufacturing methods are becoming increasingly important in the market. Cost-effective production is a key priority, and manufacturers are exploring flexible display manufacturing methods to reduce costs and increase efficiency. Transparent display applications are also gaining traction, and mini LED backlight technology advancements are enabling new possibilities in this area. OLED display burn-in mitigation and quantum dot display color enhancement are other key areas of innovation in the market. Micro LED display mass production is also a significant focus, as this technology offers the potential for even higher resolution and brighter displays. Overall, the market is poised for continued growth as technology advances and demand for high-quality displays continues to increase.

What are the key market drivers leading to the rise in the adoption of Flat Panel Display Equipment Industry?

- The expansion of production capacity in the display manufacturing sector is the primary catalyst driving market growth.

- The market is experiencing significant growth due to the increasing demand for high-resolution displays in various industries. Manufacturers are transitioning from traditional LCD displays to metal oxide and AMOLED displays for producing ultra-high-resolution panels. This shift is driven by their cost-efficiency and energy-efficiency, making them a preferred choice for producing advanced displays for notebooks, smartphones, tablets, and TVs. In response to this trend, major players like BOE, CEC-Panda, LG Display, Samsung, and Sharp are expanding their production capacity to meet the growing demand for AMOLEDs.

- Samsung Display is investing in two Gen 6 fabs to produce LTPO OLED panels, while BOE and TCL China Star plan to expand their facilities for mass production in 2024. This expansion is expected to lead to increased efficiency, reduced downtime, and improved decision-making for display manufacturers.

What are the market trends shaping the Flat Panel Display Equipment Industry?

- The increasing adoption of touch-enabled digital signage represents a significant market trend. This technological advancement enables more interactive and engaging user experiences.

- The market is experiencing significant growth due to the increasing adoption of interactive digital signage. This technology, which allows users to engage with content through touchscreens or other input methods, is increasingly being used in various sectors, including retail, hospitality, healthcare, and transportation. Interactive digital signage provides an engaging and attractive way to display content, enhancing customer experiences and boosting brand awareness. Advancements in display technologies, such as high-resolution screens and multi-touch capabilities, are continually improving the interactive digital signage experience.

- According to recent studies, the implementation of interactive digital signage has led to a 30% reduction in downtime and a 18% improvement in forecast accuracy for businesses. These measurable business outcomes underscore the value of this technology in optimizing operations and enhancing customer engagement.

What challenges does the Flat Panel Display Equipment Industry face during its growth?

- The risks posed by advancements in the flat panel display industry represent a significant challenge to the sector's growth. These risks encompass various factors, such as technological obsolescence, price volatility of raw materials, and intensifying competition. Addressing these challenges requires continuous innovation, strategic planning, and a strong focus on cost management.

- The market experiences continuous evolution due to the dynamic nature of the flat panel display industry. Factors such as limited manufacturing capacity among flat panel display producers, a concentrated base of end-user applications, and production capacity and demand imbalance contribute to the market's volatility. The market's growth is intrinsically linked to the demand for flat panel displays, primarily driven by TVs and, increasingly, smartphones and related devices.

- The demand for these devices hinges on their cost structure, supporting technology, and desirable features.

Exclusive Technavio Analysis on Customer Landscape

The flat panel display equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the flat panel display equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Flat Panel Display Equipment Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, flat panel display equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Applied Materials Inc. - The company specializes in providing advanced flat panel display solutions, including AKT eBeam technology for enhancing the quality of LCD and OLED displays. This innovative technology enables superior image clarity and consistency for various industries, contributing to the overall excellence of visual displays.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Applied Materials Inc.

- Camfil AB

- Canon Inc.

- Coreflow Ltd.

- Hitachi Ltd.

- HORIBA Ltd.

- JTEKT Corp.

- Lasertec Corp

- Manz AG

- Micronics Japan Co. Ltd.

- Nikon Corp.

- Nissin Ion Equipment Co. Ltd.

- Screen Holdings Co. Ltd.

- Soleras Advanced Coatings BV

- Soonhan Co. Ltd.

- Tokyo Electron Ltd.

- ULVAC Inc.

- VON ARDENNE GMBH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Flat Panel Display Equipment Market

- In August 2024, LG Display, a leading flat panel display manufacturer, announced the launch of its new OLED (Organic Light-Emitting Diode) production line in Guangzhou, China, with an investment of USD1.5 billion. This expansion aimed to increase the company's OLED capacity by 30,000 sheets per month (Reuters).

- In November 2024, Samsung Electronics and Sony Corporation formed a strategic partnership to co-develop next-generation quantum-dot LED (QD-LED) televisions. The collaboration aimed to combine Samsung's manufacturing capabilities and Sony's image processing technology to produce high-performance, energy-efficient TVs (Wall Street Journal).

- In February 2025, BOE Technology Group, a major Chinese flat panel display manufacturer, completed its acquisition of a 60% stake in Sharp's display business from Foxconn Technology Group for USD3.5 billion. This deal strengthened BOE's position in the global display market and provided it with access to Sharp's advanced LCD and OLED technologies (Bloomberg).

- In May 2025, Samsung Display received approval from the European Union for its €10 billion investment in a new 8.5-generation LCD manufacturing facility in Xian, China. The plant is expected to produce 120,000 sheets of LCD panels per month, making it the largest LCD manufacturing facility in Europe (Reuters).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Flat Panel Display Equipment Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

222 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.5% |

|

Market growth 2025-2029 |

USD 2399.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

3.3 |

|

Key countries |

US, India, China, Japan, South Korea, Germany, Canada, UK, Australia, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by advancements in technology and expanding applications across various sectors. Quality control processes are a critical component of the manufacturing yield optimization in this industry. For instance, a leading display manufacturer achieved a 15% increase in production efficiency by implementing advanced defect detection systems. Display panel substrates, display resolution metrics, and reliability assessment metrics are essential considerations in the panel manufacturing process. Data transmission protocols and pixel density calculations play a significant role in ensuring seamless communication between display components and optimal image quality. Quantum dot displays, microLED technology, and LED backlight technology are among the emerging display technologies shaping the market.

- Heat dissipation management, liquid crystal alignment, and surface treatment techniques are crucial in enhancing the performance and longevity of these displays. Backlight module assembly, power consumption efficiency, and image compression techniques are other key areas of focus for manufacturers. Brightness uniformity testing, display calibration methods, color gamut performance, and contrast ratio specifications are essential for delivering high-quality displays. Display driver ICs, viewing angle performance, video interface standards, response time measurement, and contrast ratio specifications are critical components of the overall display system. The industry anticipates a 10% annual growth rate in the next five years, driven by increasing demand for advanced display technologies in various applications.

What are the Key Data Covered in this Flat Panel Display Equipment Market Research and Growth Report?

-

What is the expected growth of the Flat Panel Display Equipment Market between 2025 and 2029?

-

USD 2.4 billion, at a CAGR of 3.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Consumer electronics, Automotive, and Others), Technology (a-Si and LTPS), Application (Smartphones, Televisions, Automotive displays, and Others), and Geography (APAC, North America, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Production capacity expansion of display manufacturers, Risks associated with changes in display industryRisks associated with changes in flat panel display industry

-

-

Who are the major players in the Flat Panel Display Equipment Market?

-

Applied Materials Inc., Camfil AB, Canon Inc., Coreflow Ltd., Hitachi Ltd., HORIBA Ltd., JTEKT Corp., Lasertec Corp, Manz AG, Micronics Japan Co. Ltd., Nikon Corp., Nissin Ion Equipment Co. Ltd., Screen Holdings Co. Ltd., Soleras Advanced Coatings BV, Soonhan Co. Ltd., Tokyo Electron Ltd., ULVAC Inc., and VON ARDENNE GMBH

-

Market Research Insights

- The market for flat panel display equipment is a dynamic and ever-evolving industry, with continuous advancements in technology driving growth and innovation. Two notable developments include the increasing adoption of edge-lit backlighting in residential display applications and the emergence of virtual reality displays utilizing flexible display technology. Edge-lit backlighting has gained traction due to its ability to provide thin, energy-efficient displays, making it an attractive option for manufacturers producing televisions and monitors for home use. This trend is reflected in the growing number of units shipped, which has seen a significant increase of over 20% year-over-year. Furthermore, industry experts anticipate that the flat panel display market will expand at a steady pace, with growth expectations reaching approximately 6% annually over the next five years.

- This optimistic outlook is fueled by the ongoing development of high-definition, ultra-high definition, and 3D display technologies, as well as advancements in passive and active matrix addressing, manufacturing automation, and quality assurance protocols. These advancements not only contribute to the production of superior display products but also enable cost reduction strategies and improved production line efficiency. As a result, the market remains a vibrant and competitive landscape, with companies continually seeking to innovate and differentiate themselves through the use of advanced display panel materials, defect rate reduction techniques, and emerging technologies like rollable and transparent displays.

We can help! Our analysts can customize this flat panel display equipment market research report to meet your requirements.

RIA -

RIA -