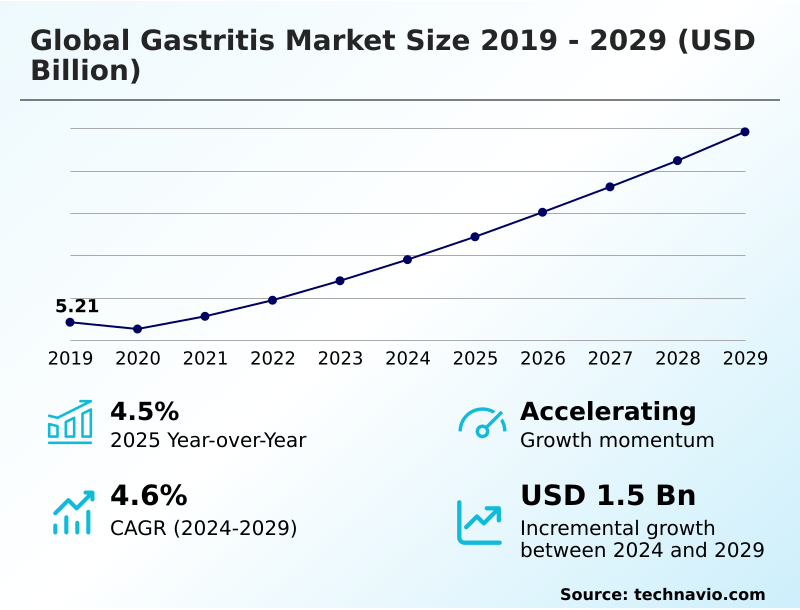

Gastritis Market Size 2025-2029

The gastritis market size is valued to increase by USD 1.50 billion, at a CAGR of 4.6% from 2024 to 2029. Pervasive helicobacter pylori infection and detrimental lifestyle factors will drive the gastritis market.

Major Market Trends & Insights

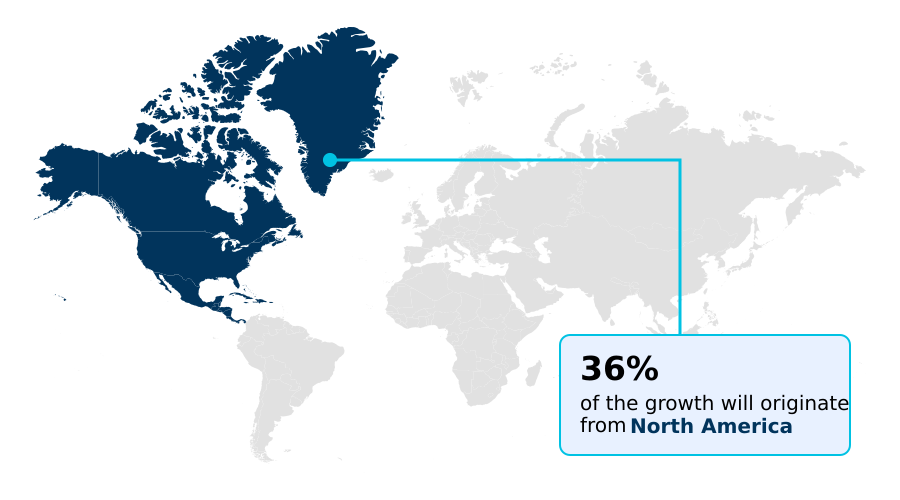

- North America dominated the market and accounted for a 36.1% growth during the forecast period.

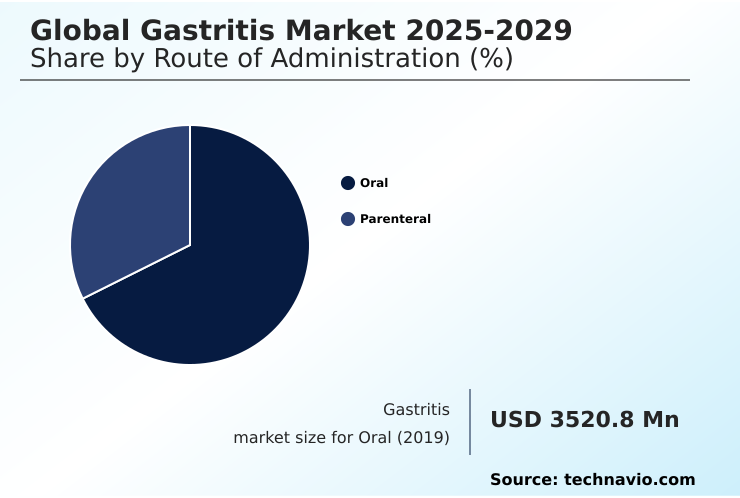

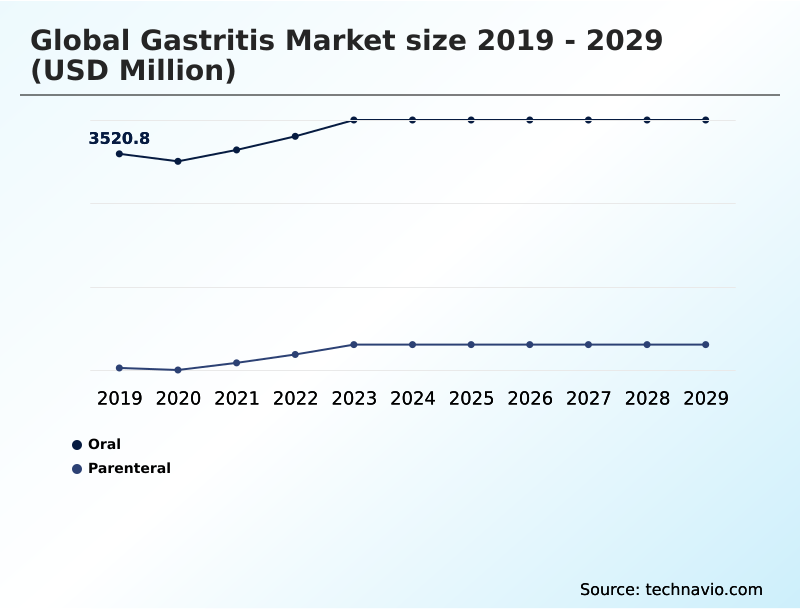

- By Route of Administration - Oral segment was valued at USD 3.81 billion in 2023

- By End-user - Hospitals and clinics segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 2.25 billion

- Market Future Opportunities: USD 1.50 billion

- CAGR from 2024 to 2029 : 4.6%

Market Summary

- The gastritis market is defined by a dynamic interplay between persistent epidemiological factors and continuous technological innovation. A primary driver is the high global prevalence of helicobacter pylori infection, the main cause of chronic gastritis, which creates a vast and sustained need for effective treatments.

- This need is amplified by modern lifestyle choices and the widespread use of nonsteroidal anti-inflammatory drugs, particularly in aging populations. The therapeutic landscape is currently undergoing a significant transformation to address the critical challenge of antibiotic resistance, which has diminished the efficacy of long-standing regimens.

- As a result, pharmaceutical firms are strategically pivoting R&D investment away from legacy proton pump inhibitors toward novel mechanisms, such as potassium-competitive acid blockers like vonoprazan, and more robust combination therapies.

- Concurrently, the diagnostic segment is advancing with the integration of ai-assisted endoscopy, which enhances the detection of precancerous conditions like chronic atrophic gastritis and improves overall patient outcomes by enabling earlier, more accurate interventions.

What will be the Size of the Gastritis Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Gastritis Market Segmented?

The gastritis industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Route of administration

- Oral

- Parenteral

- End-user

- Hospitals and clinics

- Specialty centers

- Homecare settings

- Type

- Acute gastritis

- Chronic gastritis

- Erosive gastritis

- Non-erosive gastritis

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Route of Administration Insights

The oral segment is estimated to witness significant growth during the forecast period.

The market is segmented by offerings, including diagnostics and therapeutics, and by end-users, such as hospitals, specialty centers, and homecare.

The oral administration route dominates the global gastritis market, valued for its convenience, which is a critical factor for patient adherence to complex, multi-drug regimens.

While parenteral administration is reserved for acute scenarios like severe gastrointestinal bleeding, the vast majority of treatments for gastric inflammation and dyspeptic symptoms are oral. These include h2 receptor antagonists and other acid-suppressing agents that promote mucosal healing.

However, the symptomatic overlap with other conditions complicates diagnosis. The development of more tolerable oral rescue regimens is a key focus, as patient adherence to some multi-day therapies can be low, impacting treatment efficacy for many individuals.

The Oral segment was valued at USD 3.81 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

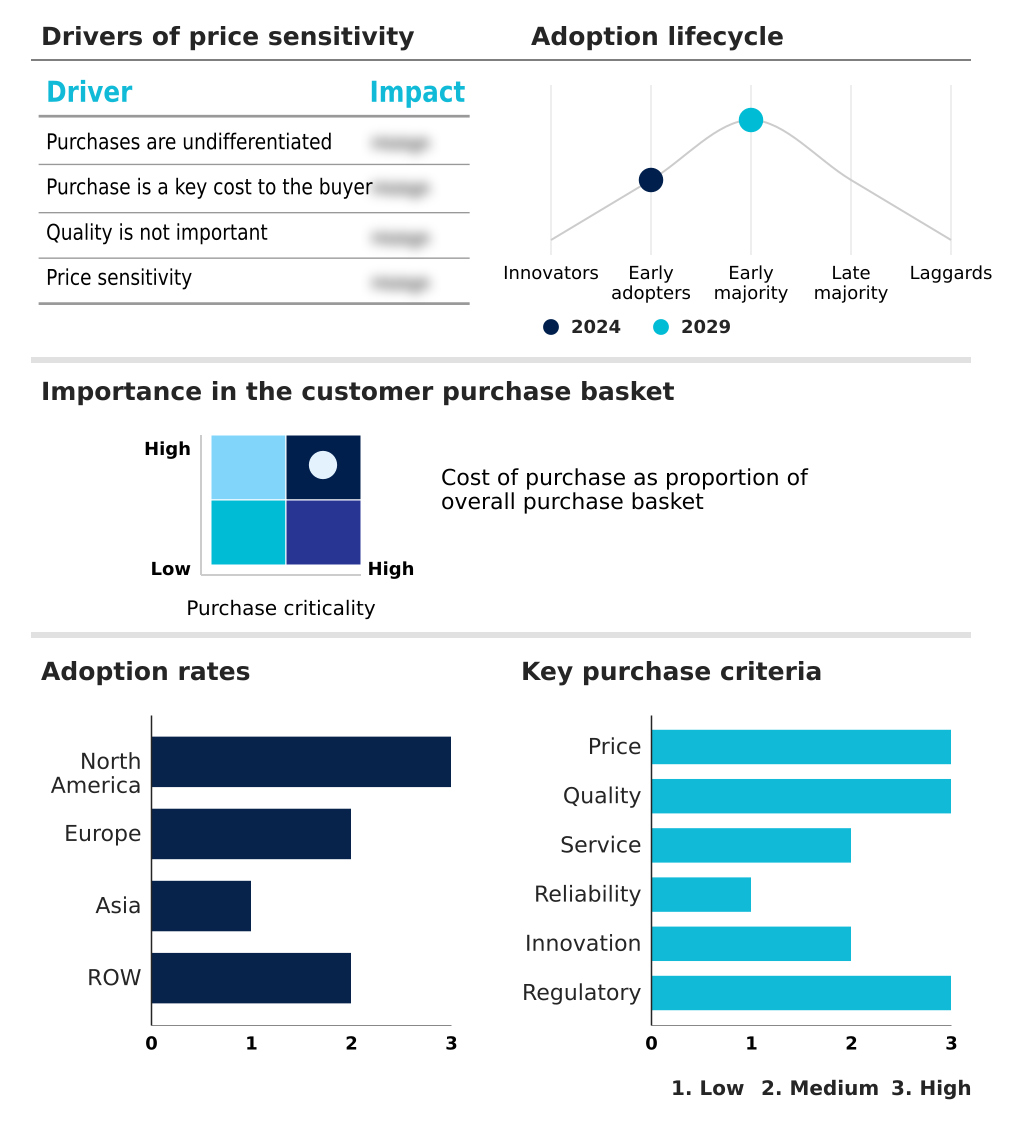

North America is estimated to contribute 36.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Gastritis Market Demand is Rising in North America Get Free Sample

The global gastritis market exhibits distinct regional dynamics, with North America leading in value and Asia poised for the fastest growth.

North America is set to contribute approximately 36% of the market's incremental growth, driven by high healthcare spending and rapid adoption of innovative therapies like vonoprazan and advanced upper gi procedures.

However, Asia is forecast to expand at a rate approximately 43% faster than Europe, fueled by the high prevalence of helicobacter pylori infection and a growing focus on gastric cancer prevention.

This has created a substantial demand for cost-effective, non-invasive diagnostic methods, including the urea breath test and stool antigen test, to support mass screening initiatives.

In this region, a well-defined test and treat strategy is essential for managing chronic atrophic gastritis and reducing the long-term healthcare burden, pushing a shift from legacy proton pump inhibitors to more effective eradication solutions.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the gastritis market is increasingly complex, forcing companies to weigh the benefits of pursuing novel therapeutic targets for gastritis against the realities of the generic ppi market impact on innovation. The efficacy of vonoprazan vs ppi has set a new benchmark, compelling a re-evaluation of R&D pipelines.

- Simultaneously, the challenge of managing nsaid-induced erosive gastritis remains a consistent revenue driver. Companies are focusing on the ai-assisted diagnosis of atrophic gastritis and improving endoscopy for precancerous lesion detection. Another key area is overcoming the challenges in functional dyspepsia diagnosis. For acute care, parenteral ppi for acute gi bleeding is a staple, but the focus is shifting to prevention.

- The push for better non-invasive h.pylori testing accuracy and effective antibiotic stewardship in gastritis treatment is reshaping diagnostics. In chronic care, staging chronic gastritis histologically is crucial. Firms must also address concerns over long-term ppi use adverse effects and consider the cost-effectiveness of h.pylori eradication.

- The development of pediatric h.pylori treatment protocols and methods for treating clarithromycin-resistant h.pylori are high-priority needs. There is also a renewed interest in the gut microbiome role in gastritis and the role of h2 blockers in gastritis. Ensuring patient compliance with quadruple therapy, like bismuth quadruple therapy for h.pylori, and preventing stress-related mucosal disease are also vital for improving outcomes.

- This landscape demands a balanced portfolio, where investment in next-generation therapies is offset by efficient lifecycle management of established products.

What are the key market drivers leading to the rise in the adoption of Gastritis Industry?

- Market growth is significantly driven by the pervasive nature of Helicobacter pylori infections, compounded by detrimental modern lifestyle factors.

- Market expansion is primarily fueled by the high global prevalence of helicobacter pylori infection, which is a leading cause of peptic ulcer disease and requires effective acid-suppressive therapies.

- This driver is intensified by the widespread use of nonsteroidal anti-inflammatory drugs (NSAIDs), particularly among the growing elderly population with significant comorbidity management needs, which can damage the gastric mucosal barrier.

- In high-risk patients, the use of stress ulcer prophylaxis is standard, but the sheer volume of NSAID users creates a sustained demand for gastroprotective agents.

- The market is also sustained by the continuous need for effective first-line treatment and rescue regimens, with recent pharmacovigilance studies shaping prescribing habits.

- This confluence of infectious disease and lifestyle-related factors ensures a persistent and expanding patient base requiring intervention to manage gastric acid secretion and prevent long-term complications.

What are the market trends shaping the Gastritis Industry?

- The market is witnessing a paradigm shift in H. pylori eradication therapy. This change is primarily driven by the escalating challenge of antibiotic resistance.

- Key market trends are centered on technological and therapeutic advancements to address clinical shortcomings. The integration of ai-assisted endoscopy is revolutionizing endoscopic diagnostics, with deep learning models demonstrating the ability to diagnose h. pylori infection from images with up to 90% accuracy. This enhances the potential for personalized therapy by identifying subtle mucosal changes.

- In therapeutics, the introduction of the potassium-competitive acid blocker class is reshaping h.pylori eradication therapy, especially for refractory cases. The development of streamlined regimens like amoxicillin dual therapy and potent alternatives such as rifabutin-based triple therapy offers new options where traditional treatments fail.

- This innovation extends to digital pathology, where AI algorithms can analyze histologic slides, improving diagnostic consistency and workflow efficiency by over 20% in some settings.

What challenges does the Gastritis Industry face during its growth?

- A key challenge affecting industry growth is the escalating rate of antibiotic resistance in Helicobacter pylori.

- A primary market challenge is the rise of antimicrobial resistance, which has led to clarithromycin resistance rates exceeding 30% in some regions and has rendered standard bismuth quadruple therapy less effective. This necessitates rigorous antibiotic resistance surveillance to guide treatment for both erosive gastritis and non-erosive gastritis.

- The challenge is compounded by the significant diagnostic ambiguity created by functional dyspepsia, a disorder of gut-brain interaction that mimics gastritis symptoms in up to 75% of dyspeptic patients. This overlap often leads to an inefficient test-and-treat strategy and inappropriate prescribing.

- Furthermore, the market faces pressure from generic price decay of legacy drugs and growing de-prescribing initiatives, which require a shift in strategy from established players toward innovation in both therapeutics and histologic analysis to maintain growth.

Exclusive Technavio Analysis on Customer Landscape

The gastritis market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the gastritis market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Gastritis Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, gastritis market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - Key offerings include proton pump inhibitors for managing acid-related symptoms and therapies designed to mitigate NSAID-induced gastric damage and complications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- AbbVie Inc.

- AstraZeneca Plc

- Cipla Inc.

- Dr Reddys Laboratories Ltd.

- GlaxoSmithKline Plc

- Johnson and Johnson Services

- Lupin Ltd.

- Medtronic Plc

- Novartis AG

- Otsuka Pharmaceutical Co Ltd.

- Perrigo Co. Plc

- Pfizer Inc.

- QIAGEN N.V.

- Sanofi SA

- Takeda Pharmaceutical Ltd.

- Teva Pharmaceutical Ltd.

- Zydus Lifesciences Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Gastritis market

- In August 2024, a pivotal systematic review concluded that AI-based technologies significantly outperform human experts in diagnosing various gastritis types, signaling increased investment in AI-assisted endoscopy platforms by companies like Medtronic Plc.

- In September 2024, the American College of Gastroenterology released new clinical guidelines recommending 14-day bismuth-based quadruple therapy, a move that directly reshapes the product and marketing strategies of firms like AbbVie Inc. and Takeda Pharmaceutical Ltd.

- In November 2024, Takeda Pharmaceutical Ltd. presented research at the American College of Gastroenterology annual meeting demonstrating that its 10-day vonoprazan-based regimen was significantly more effective than standard 14-day omeprazole therapy for H. pylori eradication.

- In January 2025, Teva Pharmaceutical Ltd. launched a new generic version of a leading proton pump inhibitor in Europe, intensifying price competition and expanding patient access to affordable gastritis treatments.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Gastritis Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.6% |

| Market growth 2025-2029 | USD 1502.4 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 4.5% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Russia, China, Japan, India, South Korea, Indonesia, Thailand, Singapore, Australia, Brazil, South Africa, UAE, Saudi Arabia and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The gastritis market is undergoing a fundamental realignment driven by the clinical necessity to overcome high antibiotic resistance. This shift is forcing a strategic pivot in product development and boardroom budgeting, moving away from legacy treatments. The declining efficacy of standard therapies has rendered many first-line protocols obsolete, creating a market imperative for innovation.

- Consequently, there is a pronounced focus on advancing more robust therapeutic options, such as bismuth quadruple therapy and novel agents like vonoprazan, a potassium-competitive acid blocker. The development of amoxicillin dual therapy and rifabutin-based triple therapy further diversifies treatment for resistant infections.

- This therapeutic evolution is complemented by advancements in diagnostics, including ai-assisted endoscopy and more precise histologic analysis for conditions from non-erosive gastritis to erosive gastritis. The management of peptic ulcer disease and gastrointestinal bleeding relies on effective acid-suppressive therapies and a clear understanding of the gastric mucosal barrier.

- This complex environment, where treatment failure rates for older regimens can exceed 20% in some regions, demands that companies prioritize investment in clinically superior solutions to maintain market relevance.

What are the Key Data Covered in this Gastritis Market Research and Growth Report?

-

What is the expected growth of the Gastritis Market between 2025 and 2029?

-

USD 1.50 billion, at a CAGR of 4.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Route of Administration (Oral, and Parenteral), End-user (Hospitals and clinics, Specialty centers, and Homecare settings), Type (Acute gastritis, Chronic gastritis, Erosive gastritis, and Non-erosive gastritis) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Pervasive helicobacter pylori infection and detrimental lifestyle factors, Escalating antibiotic resistance in helicobacter pylori

-

-

Who are the major players in the Gastritis Market?

-

Abbott Laboratories, AbbVie Inc., AstraZeneca Plc, Cipla Inc., Dr Reddys Laboratories Ltd., GlaxoSmithKline Plc, Johnson and Johnson Services, Lupin Ltd., Medtronic Plc, Novartis AG, Otsuka Pharmaceutical Co Ltd., Perrigo Co. Plc, Pfizer Inc., QIAGEN N.V., Sanofi SA, Takeda Pharmaceutical Ltd., Teva Pharmaceutical Ltd. and Zydus Lifesciences Ltd.

-

Market Research Insights

- Market dynamics are shaped by a strategic pivot toward value-based outcomes and technological integration. The introduction of novel therapeutic agents is a key factor, with newer regimens demonstrating the ability to reduce treatment duration by nearly 30% compared to traditional therapies, significantly lowering the overall cost of care and improving patient adherence.

- The integration of deep learning models into diagnostics is also transforming care, with studies showing AI-assisted platforms can improve the detection of high-risk mucosal changes by over 15%, facilitating a more effective test and treat strategy. This focus on personalized therapy and more effective first-line treatments is critical for managing refractory cases and avoiding costly repeat procedures.

- As the market contends with the symptomatic overlap between organic gastritis and functional dyspepsia, the emphasis on precise non-invasive diagnostic methods is increasing, driving demand for advanced urea breath tests and stool antigen tests to ensure appropriate and cost-effective patient management pathways.

We can help! Our analysts can customize this gastritis market research report to meet your requirements.

RIA -

RIA -