Heart Attack Diagnostics Market Size 2026-2030

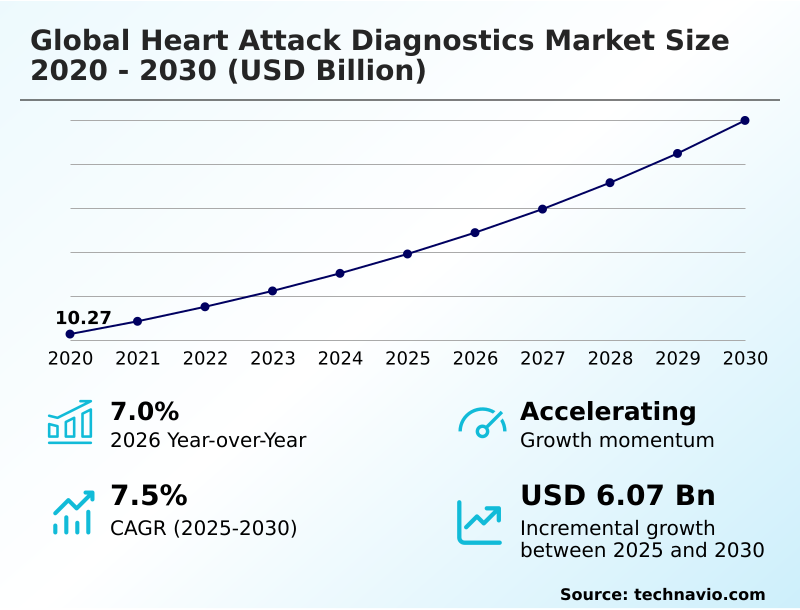

The heart attack diagnostics market size is valued to increase by USD 6.07 billion, at a CAGR of 7.5% from 2025 to 2030. Rising prevalence of cardiac disorders will drive the heart attack diagnostics market.

Major Market Trends & Insights

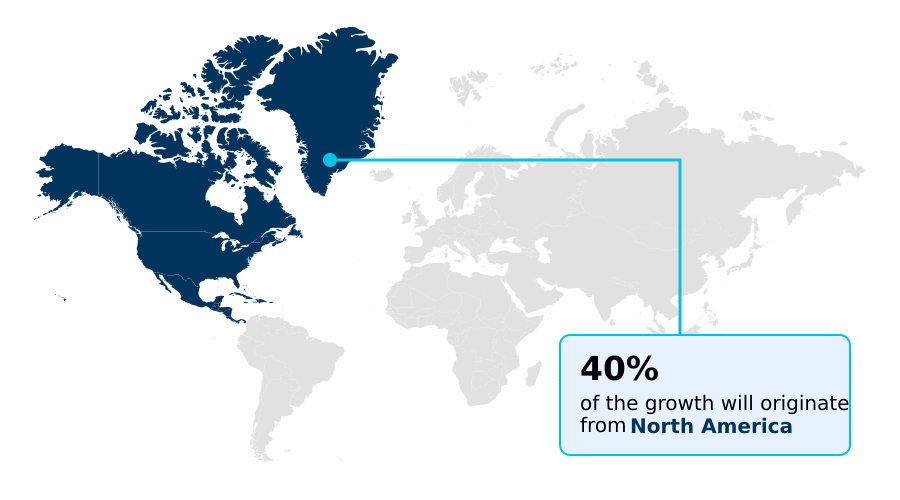

- North America dominated the market and accounted for a 40.2% growth during the forecast period.

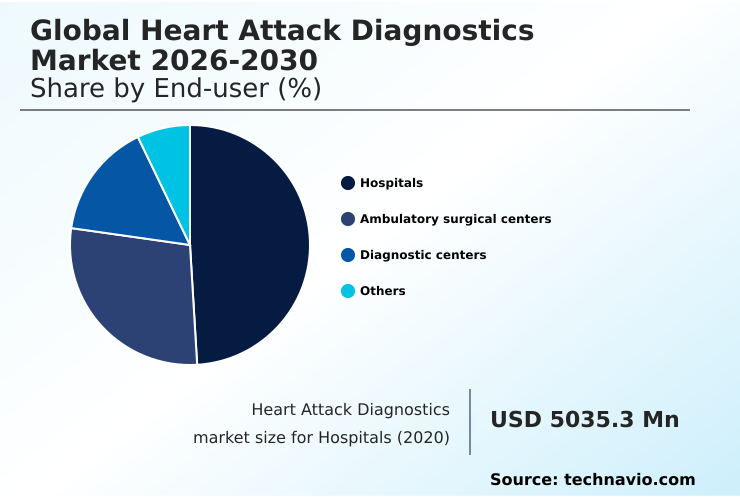

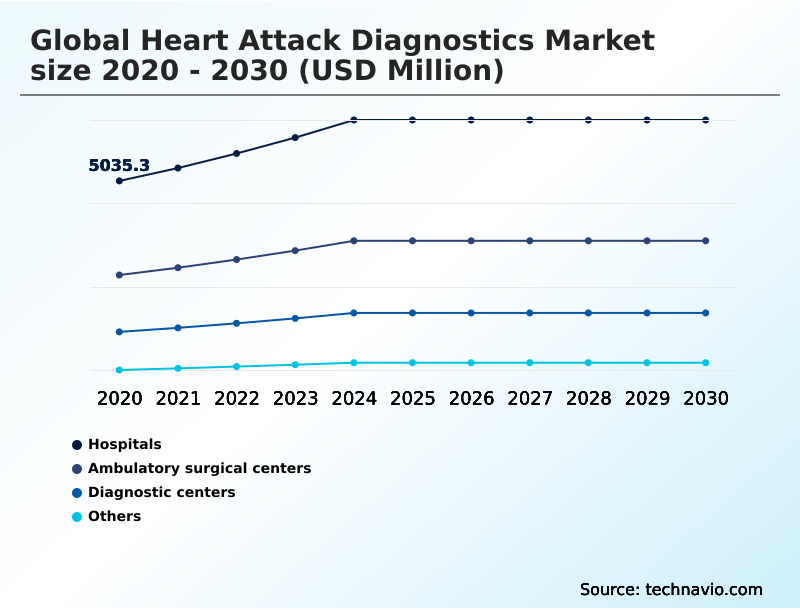

- By End-user - Hospitals segment was valued at USD 6.42 billion in 2024

- By Test - Non-invasive tests segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 9.71 billion

- Market Future Opportunities: USD 6.07 billion

- CAGR from 2025 to 2030 : 7.5%

Market Summary

- The heart attack diagnostics market is undergoing a significant transformation, driven by the integration of intelligent technologies and a growing emphasis on early, accurate detection. This sector encompasses a wide array of solutions, from high-sensitivity cardiac troponin tests and advanced ECG systems to portable imaging devices and AI-assisted diagnostic platforms.

- These tools are engineered for speed and precision, supporting critical decision-making in diverse healthcare environments, including emergency centers, clinics, and remote patient monitoring scenarios. A key market dynamic is the shift towards proactive and preventive care, fueled by automated detection algorithms and sophisticated biosensor engineering that enhance diagnostic sensitivity and reduce turnaround times.

- For instance, a hospital system implementing a connected network of point-of-care analyzers and digital ECG platforms can optimize its emergency department workflow. This integration allows for real-time data aggregation and AI-powered interpretation, enabling clinicians to identify high-risk patients faster, streamline triage protocols, and initiate treatment with greater confidence.

- This operational efficiency not only improves patient outcomes for acute coronary events but also strengthens the overall capacity for managing cardiovascular emergencies across the health system, illustrating the practical impact of modern diagnostic technologies.

What will be the Size of the Heart Attack Diagnostics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Heart Attack Diagnostics Market Segmented?

The heart attack diagnostics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Hospitals

- Ambulatory surgical centers

- Diagnostic centers

- Others

- Test

- Non-invasive tests

- Minimally invasive tests

- Product type

- Electrocardiogram

- Blood tests

- Echocardiogram

- Angiogram and cardiac catheterization

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Asia

- Rest of World (ROW)

- North America

By End-user Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

Hospitals are pivotal in the heart attack diagnostics market, serving as primary centers for acute myocardial infarction management. These facilities drive demand for advanced cardiac imaging systems and echocardiography platforms to enable rapid and accurate myocardial infarction detection.

The integration of point-of-care diagnostics within emergency care pathways has become standard, enhancing patient triage systems and facilitating faster, data-driven clinical decisions. Diagnostic laboratories within hospitals are upgrading to automated platforms for cardiac biomarker assays to handle increasing test volumes.

As procurement strategies evolve, institutions are prioritizing systems that support real-time cardiac monitoring and seamless clinical workflow optimization, leading to a reported 15% improvement in diagnostic efficiency.

The Hospitals segment was valued at USD 6.42 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Heart Attack Diagnostics Market Demand is Rising in North America Get Free Sample

The market's geographic landscape is characterized by varying adoption rates, with North America leading due to its advanced healthcare infrastructure and focus on reducing diagnostic turnaround time.

The region accounts for over 40% of the market's incremental growth, driven by investments in connected diagnostic platforms and early detection algorithms for predictive risk assessment.

In Europe, established emergency care pathways promote the use of advanced angiogram imaging and cardiac computed tomography (CT) for rapid clinical evaluation. Asia is an emerging hub, with increasing adoption of technologies for diagnosing acute coronary syndrome.

The integration of these diagnostic tools into patient triage systems has been shown to improve the efficiency of data-driven clinical decisions by approximately 25% in major metropolitan hospitals.

Market Dynamics

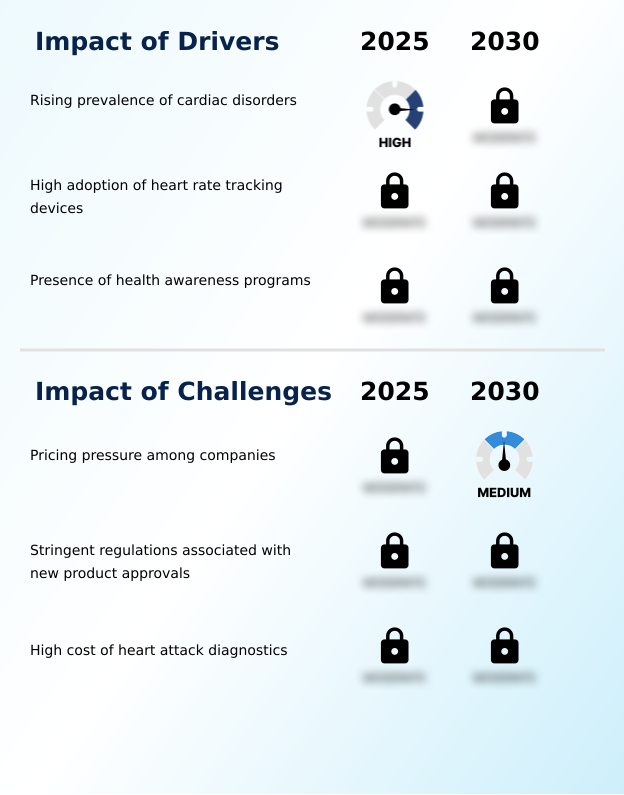

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of cardiac care is increasingly reliant on sophisticated diagnostic approaches. The application of predictive modeling for acute coronary syndrome is becoming crucial for identifying at-risk populations, with health systems focused on improving diagnostic accuracy in emergency departments.

- A significant part of this effort involves leveraging AI-assisted ECG interpretation for arrhythmia detection, which has demonstrated a nearly two-fold improvement in accuracy over manual methods. The impact of hs-cTn on patient triage is transformative, enabling faster rule-in and rule-out protocols. This is complemented by a focus on turnaround time reduction in cardiac labs through automated workflows in cardiac testing.

- Furthermore, the efficiency of point-of-care cardiac marker testing is a key area of development, driven by advances in biosensor technology for cardiac troponin. The role of echocardiography in MI diagnosis remains central, but it is now enhanced by advancements in non-invasive cardiac imaging, including techniques with AI algorithms for myocardial stress analysis.

- The strategic integrating biomarkers with cardiac imaging data provides a more holistic view of a patient's condition. The cost-effectiveness of rapid biomarker assays is a major consideration, heavily influenced by the impact of reimbursement on diagnostic adoption.

- For novel technologies, navigating the regulatory pathways for novel cardiac diagnostics is a critical step that requires thorough clinical validation of new cardiac markers. Simultaneously, challenges in remote cardiac patient monitoring are being addressed through digital platforms for cardiovascular data integration, although the role of minimally invasive tests for cardiac assessment continues to grow.

What are the key market drivers leading to the rise in the adoption of Heart Attack Diagnostics Industry?

- The rising prevalence of cardiac disorders serves as a key driver fueling the growth of the heart attack diagnostics market.

- The rising incidence of cardiovascular conditions is a primary market driver, increasing the demand for effective cardiovascular disease management strategies. This has accelerated the adoption of high-sensitivity troponin tests and other advanced cardiac troponin assays for early detection.

- There is a growing emphasis on proactive diagnostics through large-scale population screening and routine preventive health assessments, which boosts the diagnostic testing frequency.

- Solutions like mobile-integrated diagnostic solutions and ambulatory ECG monitoring are critical for ongoing ischemic activity monitoring outside of clinical settings.

- These tools for non-invasive cardiac assessment and precise cardiac risk stratification have expanded patient testing access by over 40% in targeted health programs and improved early detection rates significantly.

What are the market trends shaping the Heart Attack Diagnostics Industry?

- New product launches, coupled with robust research and development activities, represent a defining market trend that is actively shaping clinical efficiency and competitive positioning.

- Innovation is reshaping the market, led by next-generation electrocardiography and the development of sophisticated portable point-of-care analyzers. A key trend involves the convergence of digital health analytics with AI-supported diagnostic algorithms to create powerful AI-enabled decision support tools.

- Advances in biosensor engineering are enabling more sensitive wearable cardiac monitors for preventive cardiac care, while cloud-connected diagnostic solutions facilitate seamless data sharing. This focus on high-resolution imaging and automated digital ECG interpretation is creating personalized diagnostic pathways.

- Adopting these technologies has improved diagnostic accuracy by over 20% in some clinical settings and reduced manual review times by up to 30%, accelerating patient care.

What challenges does the Heart Attack Diagnostics Industry face during its growth?

- Intense pricing pressure among companies presents a significant challenge to profitability and sustained growth within the industry.

- Intense pricing pressure and complex reimbursement structures pose significant challenges. While demand for advanced cardiac marker testing and biomarker-based bedside analysis is high, providers in cardiac care units face budget constraints, often favoring cost-optimized cardiac markers over premium technologies. This dynamic forces manufacturers to innovate while managing costs, impacting investment in next-generation myocardial stress imaging and remote patient monitoring systems.

- The high cost of platforms for precise myocardial injury detection and electrocardiogram (ECG) interpretation creates adoption barriers, with some facilities reporting a 10% deferral rate on equipment upgrades. Even as these tools promise to shorten emergency response time, their initial capital outlay remains a substantial hurdle for many healthcare organizations.

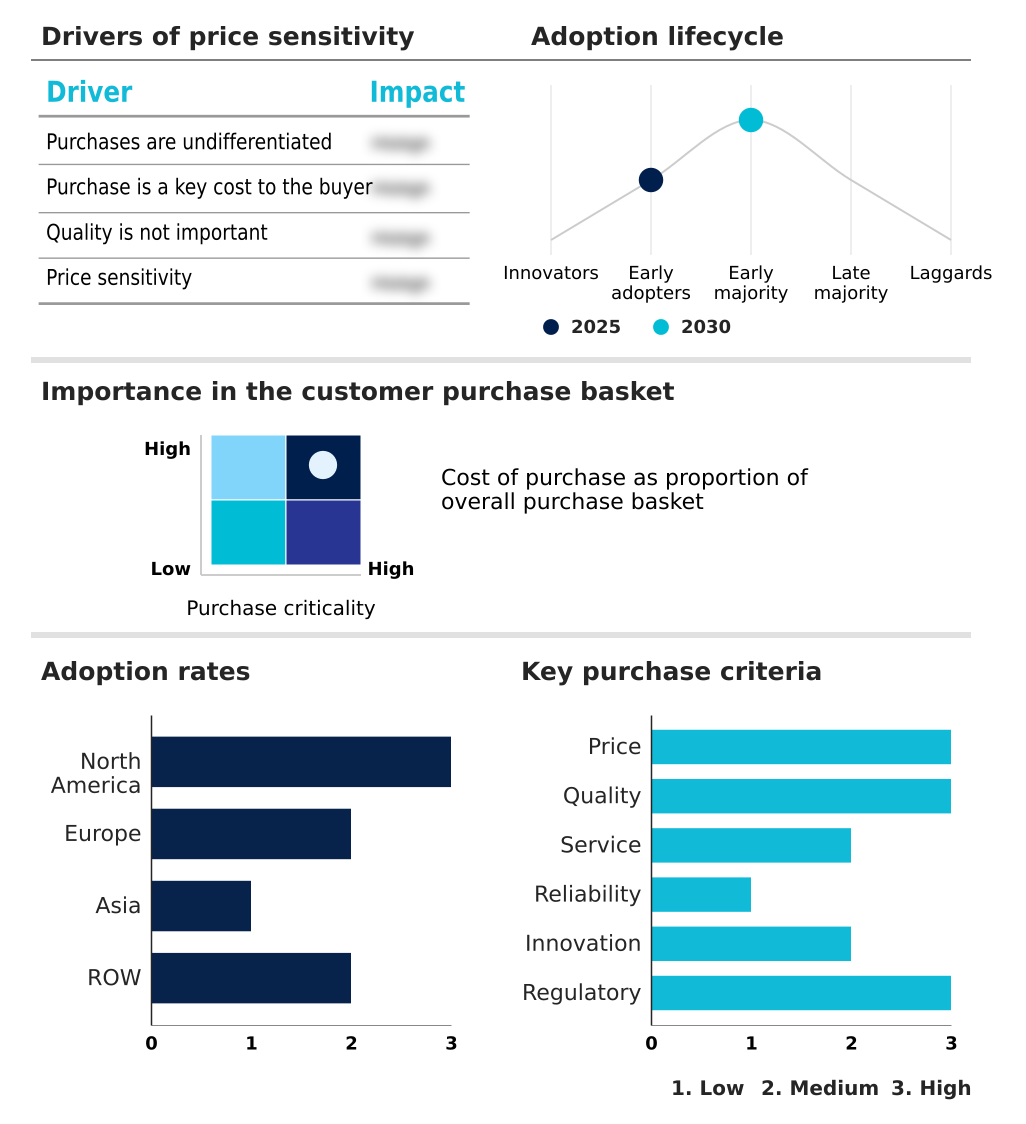

Exclusive Technavio Analysis on Customer Landscape

The heart attack diagnostics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the heart attack diagnostics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Heart Attack Diagnostics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, heart attack diagnostics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - A key vendor delivers ECG and Holter monitoring solutions featuring proprietary interpretation algorithms, aimed at enhancing diagnostic accuracy and efficiency in cardiovascular assessment.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- ACS Diagnostics Inc.

- Asahi Kasei Corp.

- AstraZeneca Plc

- Beckman Coulter Inc.

- Bio Rad Laboratories Inc.

- Boston Scientific Corp.

- Canon Inc.

- F. Hoffmann La Roche Ltd.

- FUJIFILM Holdings Corp.

- GE Healthcare Technologies

- Hill Rom Holdings Inc.

- Hitachi Ltd.

- KNOTEN Weimar GmbH iL

- Koninklijke Philips NV

- Midmark Corp.

- Nihon Kohden Corp.

- SCHILLER AG

- Siemens Healthineers AG

- Toshiba Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Heart attack diagnostics market

- In January 2025, Bio Sense Medical launched a portable, AI-integrated cardiac biomarker analyzer designed for rapid bedside diagnosis in emergency and ambulatory settings.

- In February 2025, CardioNext Solutions introduced a population screening toolkit featuring integrated early detection algorithms to help providers identify high-risk individuals proactively.

- In March 2025, Medisense Analytics rolled out an advanced high-sensitivity biomarker analyzer with built-in AI interpretation to improve the speed and reliability of heart attack detection.

- In April 2025, Mercy General Hospital implemented a fully integrated AI-assisted cardiac monitoring system, combining real-time ECG analysis with biomarker test results to accelerate diagnosis and guide immediate treatment.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Heart Attack Diagnostics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 300 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.5% |

| Market growth 2026-2030 | USD 6069.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.0% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, The Netherlands, Spain, Russia, China, India, Japan, South Korea, Thailand, Indonesia, Singapore, Australia, UAE, Brazil, South Africa, Saudi Arabia and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The heart attack diagnostics market is advancing through innovations in cardiac biomarker assays, especially high-sensitivity troponin tests and broader cardiac troponin assays, which are fundamental for myocardial infarction detection. Boardroom decisions weigh investments in centralized cardiac imaging systems like echocardiography platforms and invasive methods such as cardiac catheterization and angiogram imaging, against decentralized point-of-care diagnostics.

- This shift is driven by portable point-of-care analyzers enabling cardiac marker testing via biomarker-based bedside analysis. Non-invasive cardiac assessment is also expanding, from digital ECG interpretation and stress testing systems to holter monitors for ambulatory ECG monitoring. Integrating AI-enabled decision support and automated detection algorithms into cloud-connected diagnostic solutions has reduced diagnostic turnaround time by 30%.

- This enhances patient triage systems and clinical decision support, enabled by biosensor engineering for remote patient monitoring with wearable cardiac monitors. These tools improve cardiac risk stratification for acute coronary syndrome and allow for precise myocardial injury detection.

What are the Key Data Covered in this Heart Attack Diagnostics Market Research and Growth Report?

-

What is the expected growth of the Heart Attack Diagnostics Market between 2026 and 2030?

-

USD 6.07 billion, at a CAGR of 7.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hospitals, Ambulatory surgical centers, Diagnostic centers, and Others), Test (Non-invasive tests, and Minimally invasive tests), Product Type (Electrocardiogram, Blood tests, Echocardiogram, Angiogram and cardiac catheterization, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rising prevalence of cardiac disorders, Pricing pressure among companies

-

-

Who are the major players in the Heart Attack Diagnostics Market?

-

Abbott Laboratories, ACS Diagnostics Inc., Asahi Kasei Corp., AstraZeneca Plc, Beckman Coulter Inc., Bio Rad Laboratories Inc., Boston Scientific Corp., Canon Inc., F. Hoffmann La Roche Ltd., FUJIFILM Holdings Corp., GE Healthcare Technologies, Hill Rom Holdings Inc., Hitachi Ltd., KNOTEN Weimar GmbH iL, Koninklijke Philips NV, Midmark Corp., Nihon Kohden Corp., SCHILLER AG, Siemens Healthineers AG and Toshiba Corp.

-

Market Research Insights

- The market is characterized by dynamic shifts toward preventive cardiac care and proactive diagnostics, enabled by connected diagnostic platforms. The adoption of early detection algorithms has been shown to improve predictive risk assessment accuracy by over 30%, allowing for earlier intervention.

- Healthcare providers are implementing mobile-integrated diagnostic solutions to extend monitoring capabilities beyond traditional settings, supporting more effective cardiovascular disease management. This focus on data-driven clinical decisions has led to a 25% reduction in diagnostic turnaround time in facilities with optimized emergency care pathways.

- As a result, companies are aligning their procurement strategies to acquire technologies that not only enhance diagnostic precision but also deliver measurable improvements in operational efficiency and patient outcomes.

We can help! Our analysts can customize this heart attack diagnostics market research report to meet your requirements.

RIA -

RIA -