Hydraulic Accumulators Market Size 2026-2030

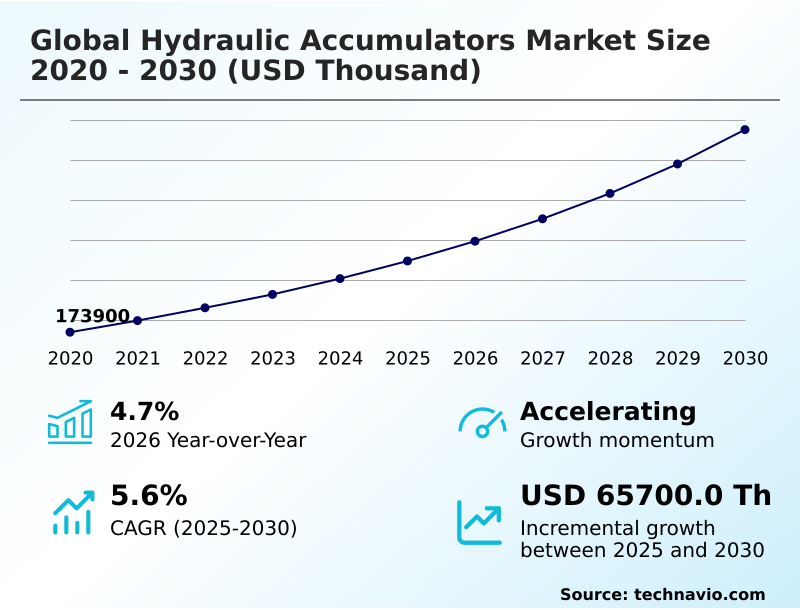

The Hydraulic Accumulators Market size was valued at USD 209.50 million in 2025, growing at a CAGR of 5.6% during the forecast period 2026-2030.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 53.7% growth during the forecast period.

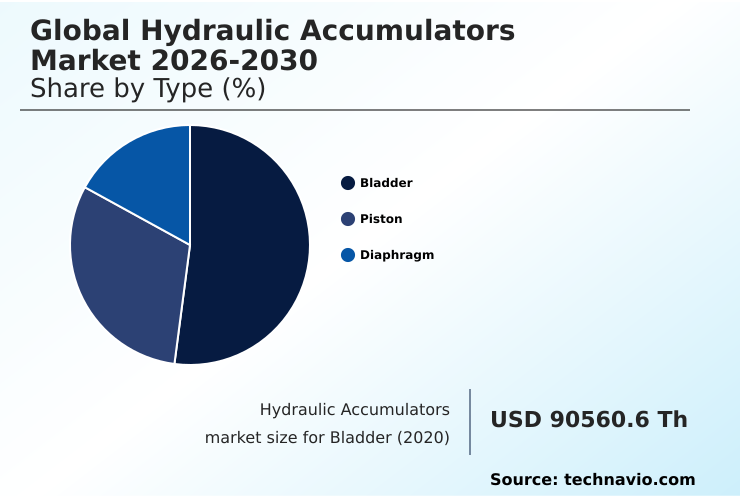

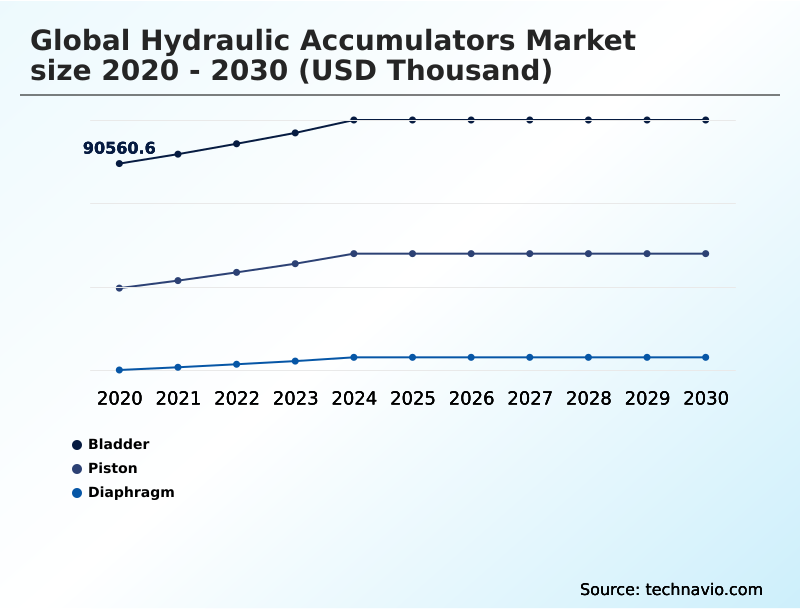

- By Type - Bladder segment was valued at USD 103.43 million in 2024

- By End-user - CM and MH segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024:

- Market Future Opportunities 2025-2030: USD 65.70 million

- CAGR from 2025 to 2030 : 5.6%

Market Summary

- The hydraulic accumulators market is defined by its critical role in enhancing the performance and safety of fluid power systems, where proper energy storage can improve system efficiency by over 15%. In a typical manufacturing scenario, integrating a properly sized accumulator into a hydraulic press circuit reduces energy consumption and minimizes wear on the main pump.

- This is achieved by storing pressurized fluid during low-demand cycles and releasing it to meet peak power needs, a process that can extend the lifespan of primary components by up to 25%. A primary driver is the modernization of aging industrial equipment, as companies seek to replace inefficient legacy systems.

- Conversely, the market faces a significant challenge from the risk of leakage and seal failure, which can lead to costly operational downtime and environmental hazards if not addressed through robust design and predictive maintenance schedules. This balance between performance enhancement and reliability assurance shapes purchasing decisions across end-user industries.

What will be the Size of the Hydraulic Accumulators Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Hydraulic Accumulators Market Segmented?

The hydraulic accumulators industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Bladder

- Piston

- Diaphragm

- End-user

- CM and MH

- Agriculture and forestry

- Oil and gas

- Others

- Product

- Horizontal mounted

- Vertical mounted

- Wall mounted

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

How is the Hydraulic Accumulators Market Segmented by Type?

The bladder segment is estimated to witness significant growth during the forecast period.

The bladder segment's utility in the global hydraulic accumulators market is defined by its rapid response capabilities, with certain designs discharging energy up to 15% faster than other accumulator types.

These devices leverage a flexible elastomer bladder within a pressure vessel to separate gas and fluid, excelling in shock absorption and pulsation dampening.

Their high power density-to-size ratio makes them ideal for mobile equipment where space is a premium, contributing to a 10% reduction in overall system weight in some applications.

Advancements in material science have improved fluid power recovery and resistance to chemical degradation, extending operational life.

Consequently, their role in providing a supplemental or emergency power source ensures system integrity and operational continuity across various industrial settings, driving consistent adoption for applications demanding both speed and reliability.

The Bladder segment was valued at USD 103.43 million in 2024 and showed a gradual increase during the forecast period.

How demand for the Hydraulic Accumulators market is rising in the leading region?

APAC is estimated to contribute 53.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Hydraulic Accumulators Market demand is rising in APAC Request Free Sample

Geographically, the global hydraulic accumulators market exhibits significant divergence, with APAC accounting for over 53% of the incremental growth, a stark contrast to North America's 23.77% share.

This dominance is propelled by countries like China, where the market is valued at over USD 37 billion, fueled by expansive infrastructure projects and a massive manufacturing base requiring high volumes of bladder accumulator and piston accumulator units.

In contrast, adoption in North America is often driven by the need to upgrade aging industrial facilities with more energy-efficient hydraulic systems to enhance hydraulic system reliability.

This regional difference also impacts supply chain strategies; APAC focuses on localized, high-volume production with an emphasis on elastomer bladder technology, while North America prioritizes specialized hydropneumatic accumulator components for sectors like aerospace, where moveable piston design and system pressure stabilization are critical.

What are the key Drivers, Trends, and Challenges in the Hydraulic Accumulators Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Understanding the hydraulic accumulator working principle is fundamental for optimizing industrial and mobile equipment performance, where efficiency gains of up to 15% are achievable with correctly specified systems. The debate over bladder vs piston accumulator often concludes with application-specific needs; bladder types offer faster response, while piston models provide durability under higher pressures.

- Accurate hydraulic accumulator sizing calculation is critical, as an undersized unit can fail to absorb shocks, while an oversized one adds unnecessary cost and weight. For instance, in systems where response time is less critical than high-pressure tolerance, piston accumulators are preferred, leading to a 10% lower failure rate in extreme-duty cycles.

- Maintaining correct hydraulic accumulator precharge pressure is another crucial aspect of operational safety and efficiency. Technicians frequently perform a hydraulic accumulator failure analysis as part of predictive maintenance, a practice that can reduce catastrophic failures and unscheduled downtime. Identifying the symptoms of a bad hydraulic accumulator early, such as sluggish system response or pressure drops, allows for timely intervention.

- This proactive approach to maintenance, which includes learning how to test a hydraulic accumulator effectively, is key to extending equipment life and ensuring reliable operation.

What are the key market drivers leading to the rise in the adoption of Hydraulic Accumulators Industry?

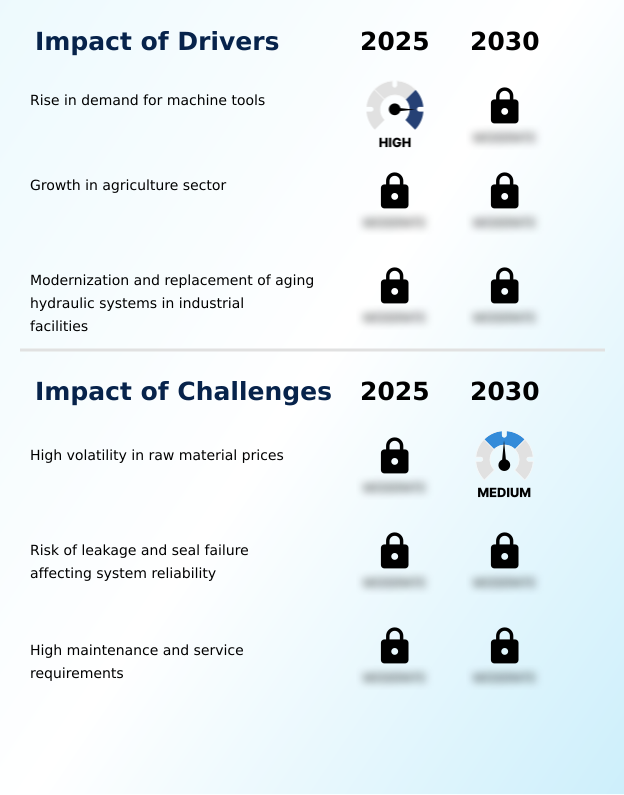

- A key driver for the market is the rising demand for hydraulic accumulators within the machine tools sector.

- The modernization of aging industrial infrastructure is a primary driver, with facilities reporting up to a 20% improvement in energy efficiency after replacing legacy equipment with modern high-pressure hydraulic systems.

- This transition is fueled by the need to enhance system responsiveness and adhere to stricter operational safety standards.

- The expansion of the agriculture sector, where mechanization rates in some regions are growing by 5% annually, also propels demand for reliable fluid power system components.

- In these applications, precise pressure regulation is crucial for optimizing equipment lifespan extension and performance.

- The adoption of advanced accumulators with proper nitrogen gas charging ensures consistent system pressure, supporting the demanding duty cycles of modern industrial hydraulic applications and hydraulic system design.

What are the market trends shaping the Hydraulic Accumulators Industry?

- A prominent market trend is the rapid technological advancement of hydraulic accumulators. This development is primarily focused on enhancing energy efficiency across industrial and mobile applications.

- Technological advancements are driving a significant shift toward smart hydraulic energy storage solutions that can improve overall hydraulic system efficiency by up to 20%. The integration of sensor technology for predictive maintenance integration is a key trend, allowing for real-time monitoring of accumulator performance and reducing unscheduled downtime by over 25% compared to traditional systems.

- This focus on digitalization enables superior pulsation damping and dynamic load management in mobile hydraulic equipment and industrial machinery. As industries prioritize sustainability, the demand for systems capable of advanced energy recovery is increasing. This trend supports the development of more sophisticated motion control systems that offer enhanced hydraulic system stability and operational longevity.

What challenges does the Hydraulic Accumulators Industry face during its growth?

- A significant challenge affecting industry growth is the high volatility in the prices of raw materials required for manufacturing hydraulic accumulators.

- High volatility in raw material costs presents a major challenge, with prices for specialized steel and elastomers fluctuating by as much as 25% in a single year, directly impacting the total cost of ownership for end-users. This price instability complicates production planning and can lead to compromised hydraulic fluid containment if lower-quality materials are substituted.

- Furthermore, the persistent risk of seal failure remains a critical issue, contributing to over 30% of unplanned downtime in certain high-pressure applications. Issues such as improper gas pre-charge, fluid contamination control, and vibration reduction are essential to mitigate leakage compensation problems. Managing these factors is crucial to prevent inconsistent fluid flow consistency and maintain system reliability.

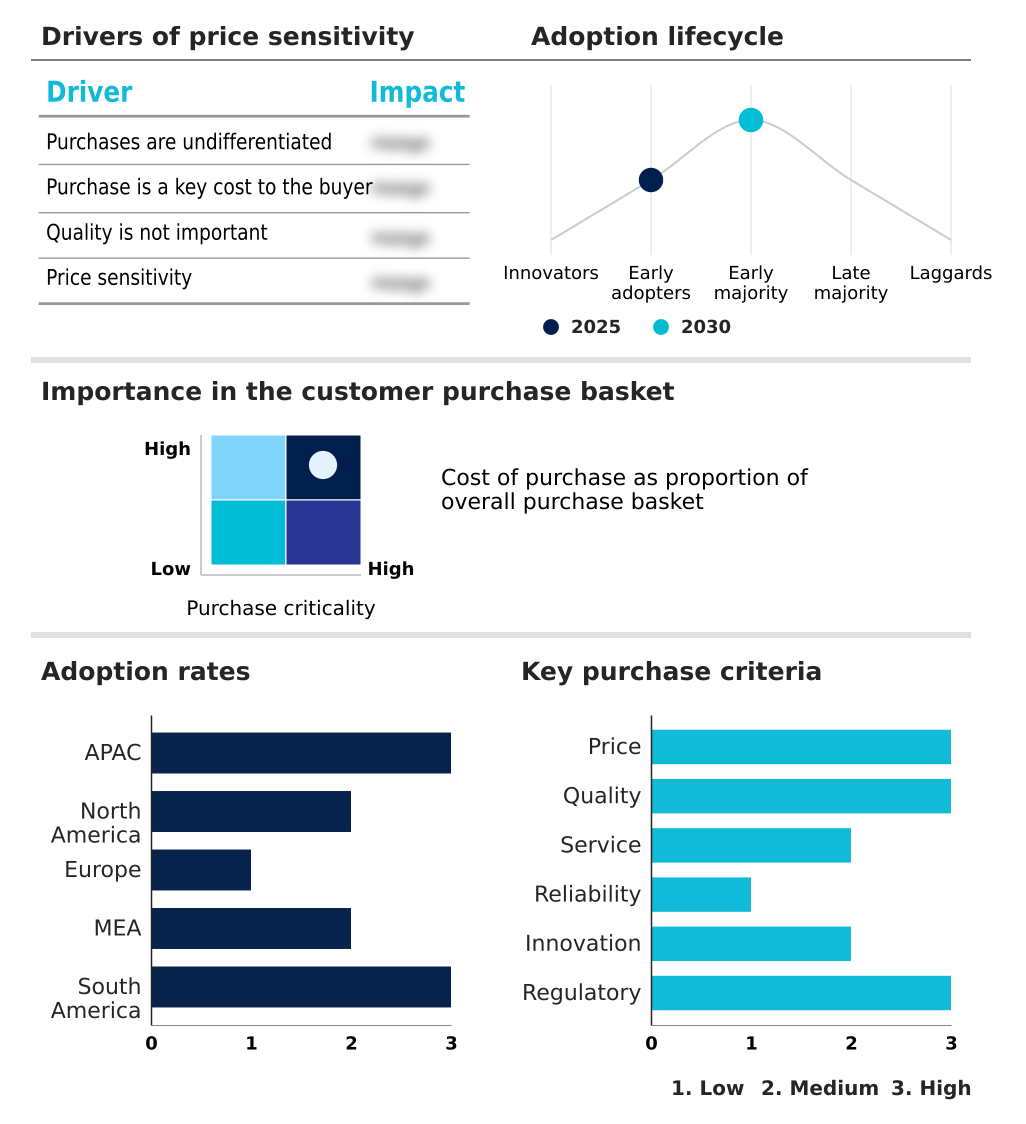

Exclusive Technavio Analysis on Customer Landscape

The hydraulic accumulators market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the hydraulic accumulators market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Hydraulic Accumulators Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, hydraulic accumulators market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accumulators Inc. - Offerings are centered on a diverse range of hydraulic energy storage devices, including bladder, piston, and diaphragm accumulators for varied industrial and mobile applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accumulators Inc.

- Bailey International LLC

- Bucher Hydraulics GmbH

- Danfoss AS

- Freudenberg and Co. KG

- HANNON HYDRUALICS LLC

- HAWE Hydraulik SE

- HYDAC International GmbH

- Hydrapac Italia Inc.

- HYDRO LEDUC SA

- Hydroll Oy

- Parker Hannifin Corp.

- Robert Bosch GmbH

- Roth Hydraulics GmbH

- Servi Group

- Stauffenberg GmbH and Co. KG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Aerospace and Defense industry, the push for lightweight materials to enhance fuel efficiency in next-generation aircraft has increased demand for compact hydraulic accumulators. This directly impacts the market by requiring innovations in designs that reduce component weight without compromising hydraulic system reliability or performance under high-pressure conditions.

- The growing preference for fuel-efficient aircraft and the modernization of aviation fleets are creating new requirements for energy consumption reduction. This trend necessitates the integration of advanced hydraulic accumulators capable of superior energy recovery and dynamic load management, thereby improving the overall hydraulic system efficiency of aerospace platforms.

- Advances in unmanned aerial vehicle (UAV) technology and the development of more complex electronic warfare systems have spurred the need for highly responsive and compact fluid power components. As a result, the market is seeing increased demand for specialized diaphragm and piston accumulators that support the precise motion control systems essential for these advanced defense applications.

- Heightened geopolitical tensions and shifts in international trade agreements have altered supply chain dynamics for critical aerospace components. This has compelled manufacturers to diversify sourcing for high-strength metals and elastomers used in hydraulic accumulators, impacting production costs and necessitating more resilient hydraulic circuit design and logistics planning.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Hydraulic Accumulators Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.6% |

| Market growth 2026-2030 | USD 65700.0 thousand |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.7% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The ecosystem of the global hydraulic accumulators market is a multi-layered value chain, where the construction and material handling (CM and MH) sector represents over 53% of end-user demand. The chain begins with suppliers of raw materials like high-strength steel and specialized elastomers, which are procured by component producers.

- These components are then integrated by system manufacturers, including major industrial players like Robert Bosch GmbH and Parker Hannifin Corp., into complete hydraulic solutions. These solutions are distributed through direct sales and channel partners to end-users in key industries such as agriculture and oil and gas.

- Regulatory bodies influence design by setting safety and environmental standards, while R&D entities drive innovation in areas like energy efficiency and smart monitoring. Piston accumulators, favored for their durability in high-pressure environments, constitute approximately 32% of the market, highlighting a clear preference for robust solutions in demanding applications.

What are the Key Data Covered in this Hydraulic Accumulators Market Research and Growth Report?

-

What is the expected growth of the Hydraulic Accumulators Market between 2026 and 2030?

-

The Hydraulic Accumulators Market is expected to grow by USD 65.70 million during 2026-2030, registering a CAGR of 5.6%. Year-over-year growth in 2026 is estimated at 4.7%%. This acceleration is shaped by rise in demand for machine tools, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Bladder, Piston, and Diaphragm), End-user (CM and MH, Agriculture and forestry, Oil and gas, and Others), Product (Horizontal mounted, Vertical mounted, and Wall mounted) and Geography (APAC, North America, Europe, Middle East and Africa, South America). Among these, the Bladder segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, North America, Europe, Middle East and Africa and South America. APAC is estimated to contribute 53.7% to market growth during the forecast period. Country-level analysis includes China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is rise in demand for machine tools, which is accelerating investment and industry demand. The main challenge is high volatility in raw material prices, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Hydraulic Accumulators Market?

-

Key vendors include Accumulators Inc., Bailey International LLC, Bucher Hydraulics GmbH, Danfoss AS, Freudenberg and Co. KG, HANNON HYDRUALICS LLC, HAWE Hydraulik SE, HYDAC International GmbH, Hydrapac Italia Inc., HYDRO LEDUC SA, Hydroll Oy, Parker Hannifin Corp., Robert Bosch GmbH, Roth Hydraulics GmbH, Servi Group and Stauffenberg GmbH and Co. KG. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for hydraulic accumulators is characterized by intense innovation, with the top five vendors accounting for over 45% of the market share through technological differentiation. Key players such as Robert Bosch GmbH and Parker Hannifin Corp.

- are focusing on developing smart hydraulic systems that integrate advanced sensors for predictive maintenance, a feature that can reduce unscheduled downtime by up to 20%. These developments directly address enterprise demand for greater operational efficiency and automation in sectors like construction and manufacturing.

- The industry's strategic direction is toward creating more integrated solutions that combine hardware with digital control for optimized performance. However, vendors continue to navigate the challenge of high volatility in raw material prices, adapting by optimizing supply chains and exploring alternative materials to maintain cost competitiveness and production stability.

We can help! Our analysts can customize this hydraulic accumulators market research report to meet your requirements.

RIA -

RIA -