Infertility Treatment Devices Market Size 2024-2028

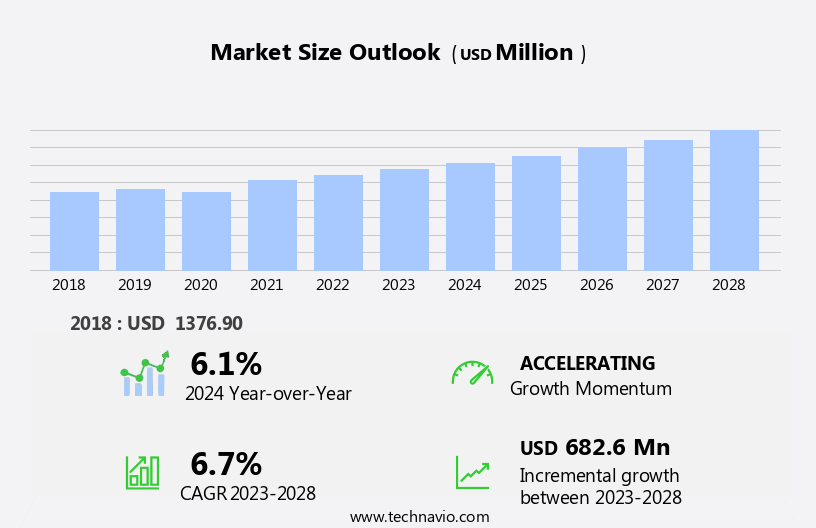

The infertility treatment devices market size is forecast to increase by USD 682.6 billion at a CAGR of 6.7% between 2023 and 2028.

- The market is experiencing significant growth due to several key factors. The prevalence of infertility is on the rise, driven by various lifestyle and health factors. Moreover, an emerging trend of delayed pregnancies among women is leading to a higher demand for infertility treatment devices. However, ethical, legal, and social concerns regarding infertility treatments pose challenges to market growth. These issues include ethical debates around the use of assisted reproductive technologies, legal regulations governing their use, and social stigma surrounding infertility and its treatments. Despite these challenges, the market is expected to continue growing as advancements in technology and increasing awareness of infertility issues drive innovation and demand for effective treatment solutions.

What will be the Size of the Infertility Treatment Devices Market During the Forecast Period?

- The market encompasses a range of diagnostic and assisted reproductive technologies (ART), including in vitro fertilization (IVF), that aim to address infertility issues. The prevalence of infertility, driven by factors such as lifestyle changes, female fertility concerns, and conditions like polycystic ovary syndrome, continues to fuel market growth. ART operations, including fertility clinics, employ advanced technologies like microfluidic chip-based devices for sperm sorting and other procedures. Social and cultural implications, insurance coverage, and mobility constraints influence the market dynamics. Regulatory authorities closely scrutinize patent applications and the safety and efficacy of infertility treatment products. The incidence of infertility, driven by declining fertility rates, fuels the demand for these devices.

- Medical tourism also plays a role, with some individuals traveling to countries with more lenient regulations or lower costs. Assisted reproductive technology continues to evolve, offering new possibilities for those seeking to overcome infertility.

How is this Infertility Treatment Devices Industry segmented and which is the largest segment?

The infertility treatment devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Devices

- Media

- Accessories

- Geography

- Asia

- Singapore

- Thailand

- North America

- US

- Europe

- Rest of World (ROW)

- Asia

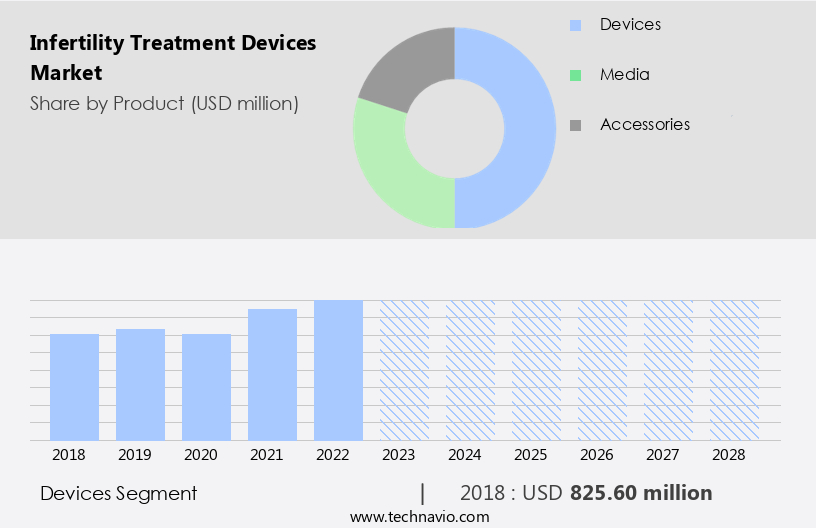

By Product Insights

- The devices segment is estimated to witness significant growth during the forecast period.

The market is driven by several factors, including the rise in infertility prevalence, the success rate of infertility treatment procedures, investments in advanced IVF products, and increasing demand for technologically advanced devices. The devices segment is expected to dominate the market due to these factors, with geographical regions such as North America and Europe leading in market growth. The infertility rate in men and women, growing awareness about assisted reproductive technologies (ART), adoption of advanced technologies by healthcare authorities, and economic stability are key drivers In these regions. Infertility treatment devices, including sperm separation devices, ovum aspiration pumps, sperm analyzer systems, micromanipulator systems, and incubators, are essential tools for ART procedures and are in high demand.

Get a glance at the Infertility Treatment Devices Industry report of share of various segments Request Free Sample

The Devices segment was valued at USD 825.60 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

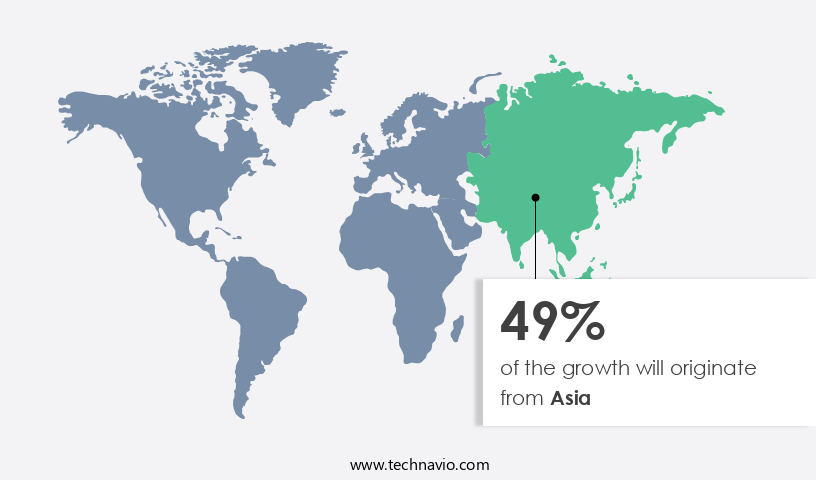

- Asia is estimated to contribute 49% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market in Asia is poised for growth due to several factors, including the rising prevalence of infertility, medical tourism, enhanced healthcare infrastructure, and increasing adoption of advanced technologies. The region's infertility rate is on the rise, attributed to lifestyle changes, the emergence of fertility-related diseases, and escalating stress levels. Infertility treatment devices, such as microfluidic chip-based devices for sperm sorting, are increasingly being adopted in fertility clinics to enhance success rates. Despite ethical and legal concerns regarding surrogacy and embryo transfers, Asia's infertility treatment market is gaining global recognition. The market's growth is further fueled by the availability of less-regulated healthcare systems and the presence of a large pool of skilled medical professionals.

Market Dynamics

Our infertility treatment devices market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Infertility Treatment Devices Industry?

Increase in prevalence of infertility is the key driver of the market.

- Infertility, defined as the inability to conceive after a year of unprotected intercourse, affects approximately 12% of women aged 15-44 In the US. This statistic underscores the significant need for infertility treatment devices, fueling market expansion. Infertility can result from various health conditions and diseases, affecting both males and females. Assisted reproductive technologies (ART), including in vitro fertilization (IVF), have become increasingly common to address infertility issues. The prevalence of infertility is influenced by social and cultural factors, as well as lifestyle choices and medical conditions such as Polycystic Ovary Syndrome (PCOS). Diagnosis and treatment of infertility involve various devices, including sperm separation devices, ovum aspiration pumps, sperm analyzer systems, micromanipulator systems, incubators, cryosystems, imaging systems, and microscopes.

- Fertility clinics, hospitals, clinical research institutes, and specialized centers employ these devices to perform ART operations, ensuring adherence to health standards and maintaining reproductive health. Insurance coverage, mobility constraints, and environmental pollutants can impact the accessibility and affordability of infertility treatments. The success rate of IVF procedures varies, with advancements in technology, such as microfluidic chip-based devices for sperm sorting, contributing to improved outcomes. Market growth is further influenced by regulatory authorities, healthcare expenditures, and the increasing incidence of infertility. Medical tourism also plays a role In the global infertility treatment market. The market for infertility treatment devices is dynamic, with ongoing research and development, patent scrutiny, and declining fertility rates driving innovation and demand.

- The market is expected to continue growing, providing opportunities for companies specializing in ART operations and infertility treatment products.

What are the market trends shaping the Infertility Treatment Devices Industry?

Emerging trend of delayed pregnancies among women is the upcoming market trend.

- Infertility treatment devices refer to technologies and tools used In the diagnosis and treatment of infertility, including assisted reproductive technologies (ART) such as in vitro fertilization (IVF). The prevalence of infertility, driven by factors like age, lifestyle changes, and health conditions, has led to a growing demand for these devices. ART operations, which include sperm separation devices, ovum aspiration pumps, sperm analyzer systems, micromanipulator systems, incubators, cryosystems, and imaging systems, are used in fertility clinics, hospitals, and clinical research institutes to enhance the chances of successful fertility procedures. Environmental pollutants and male infertility are also significant factors driving the market for infertility treatment devices.

- The social and cultural implications of infertility are significant, with many couples facing emotional and financial challenges. Insurance coverage for infertility treatments varies, and mobility constraints can limit access to specialized centers. The success rate of IVF procedures, which is influenced by factors like age, health conditions, and the quality of gametes, is a critical consideration for couples seeking treatment. Regulatory authorities play a crucial role in setting health standards for reproductive health and ART operations. The incidence of infertility is increasing, with conditions like polycystic ovary syndrome (PCOS) being common causes. Microfluidic chip-based devices, such as sperm sorting, are emerging as innovative solutions for improving the efficiency and accuracy of infertility treatments.

- Fertility clinics and healthcare expenditures continue to grow as more couples seek treatment for infertility. Medical tourism is also a significant trend, with couples traveling to countries with more favorable regulations and lower costs for infertility treatments. In conclusion, the market is driven by the increasing prevalence of infertility, the need for advanced technologies to improve the success rate of fertility procedures, and the social and cultural implications of infertility. The market is expected to grow significantly In the coming years, with regulatory authorities playing a crucial role in setting health standards and ensuring the safety and efficacy of infertility treatment devices.

What challenges does Infertility Treatment Devices Industry face during the growth?

Ethical, legal, and social concerns regarding infertility treatments is a key challenge affecting the industry growth.

- The market encompasses various diagnostic and assisted reproductive technologies (ART) used to address infertility issues. These technologies include in vitro fertilization (IVF), sperm separation devices, ovum aspiration pumps, sperm analyzer systems, micromanipulator systems, incubators, cryosystems, imaging systems, and microscopes. The social and cultural implications of infertility treatment are significant, as it raises ethical concerns over procedures such as ART. Issues include semen banking guidelines, surrogacy legality, modes of conceiving, and children's access to genetic backgrounds. Monitoring ART procedures is crucial to prevent ethical exploitation. Infertility treatment devices enable couples facing infertility to manipulate nature and produce children, which some find objectionable.

- Ethical concerns mainly revolve around egg selection, embryo creation, and embryo disposal. Prevalence of infertility, insurance coverage, mobility constraints, and healthcare expenditures influence the market. Environmental pollutants and male infertility also contribute to market growth. The success rate of fertility procedures, such as IVF, and the incidence of infertility further impact market dynamics. Regulatory authorities overseeing health standards and reproductive health play a crucial role in market development.

Exclusive Customer Landscape

The infertility treatment devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the infertility treatment devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, infertility treatment devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Carl Zeiss AG - Our company provides advanced infertility treatment devices for medical professionals, including Oocyte Retrieval Systems. These systems facilitate efficient and safe ovum aspiration during In Vitro Fertilization (IVF) procedures, ensuring optimal results for patients undergoing infertility treatments. The Oocyte Retrieval Systems we offer are designed to enhance the success rate of IVF treatments and prioritize patient safety.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Carl Zeiss AG

- Cook Group Inc.

- DxNow

- Eppendorf SE

- Esco Micro Pte Ltd.

- FUJIFILM Irvine Scientific Inc.

- Genea Biomedx

- Gynotec BV

- Hamilton Thorne Inc.

- IHMedical AS

- IVFtech ApS

- KITAZATO Corp.

- MedGyn Products Inc.

- Merck KGaA

- Rocket Medical Plc

- Shinelife

- The Baker Co.

- The Cooper Companies Inc.

- Thermo Fisher Scientific Inc.

- Vitrolife AB

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market: An In-depth Analysis of Technological Advancements and Market Dynamics the market encompasses a range of innovative tools and technologies designed to diagnose and treat infertility issues. This market is characterized by continuous advancements in assisted reproductive technologies (ART), which have revolutionized the way infertility is addressed. Assisted reproductive technologies, including in vitro fertilization (IVF), have significantly impacted the lives of countless individuals and couples seeking to start a family. These advanced procedures enable the manipulation of gametes (sperm and ova) outside the body to facilitate fertilization. Social and cultural implications of infertility are profound, with individuals and couples facing emotional, psychological, and financial challenges.

Infertility is a complex issue that can be influenced by various factors, such as lifestyle choices, medical conditions, and environmental pollutants. The prevalence of infertility is a growing concern worldwide, with an estimated 15% of couples experiencing difficulty conceiving. Insurance coverage for infertility treatments varies significantly, and mobility constraints can limit access to specialized care. Fertility procedures, such as ovum aspiration pumps, sperm separation devices, and micromanipulator systems, are essential components of ART. These devices enable the precise handling and manipulation of gametes, increasing the chances of successful fertilization. Incubators, cryosystems, imaging systems, and microscopes are other critical devices used in infertility treatment.

These tools ensure optimal conditions for the growth and development of embryos, enhancing the overall success rate of ART procedures. Fertility clinics, hospitals, clinical research institutes, and specialized centers are key players In the market. These institutions invest heavily in research and development, ensuring the latest technologies are available to patients. Health standards and regulatory authorities play a crucial role In the market. Strict regulations ensure the safety and efficacy of these devices, while ongoing research and innovation drive continuous improvements. Female infertility, often linked to conditions such as polycystic ovary syndrome (PCOS), is a significant focus In the market.

Innovations in microfluidic chip-based devices and sperm sorting technologies are helping to address this issue. The success rate of infertility treatments, particularly IVF procedures, has improved significantly over the years. However, challenges such as patent scrutiny, declining fertility rates, and the rising cost of treatments persist. Medical tourism is an emerging trend In the market, with individuals traveling to countries with more favorable regulations and lower costs for treatments. This trend highlights the importance of international collaboration and standardization In the field. In conclusion, the market is a dynamic and evolving industry, driven by technological advancements and the growing need for effective solutions to address infertility issues.

Continuous innovation and collaboration between researchers, clinicians, and regulatory authorities are essential to ensuring the availability of safe, effective, and affordable infertility treatment options for individuals and couples worldwide.

|

Infertility Treatment Devices Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

145 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.7% |

|

Market growth 2024-2028 |

USD 682.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.1 |

|

Key countries |

US, Taiwan, Thailand, Israel, and Singapore |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Infertility Treatment Devices Market Research and Growth Report?

- CAGR of the Infertility Treatment Devices industry during the forecast period

- Detailed information on factors that will drive the Infertility Treatment Devices growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Asia, North America, Europe, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the infertility treatment devices market growth of industry companies

We can help! Our analysts can customize this infertility treatment devices market research report to meet your requirements.

RIA -

RIA -