Inotropic Agents Market Size 2025-2029

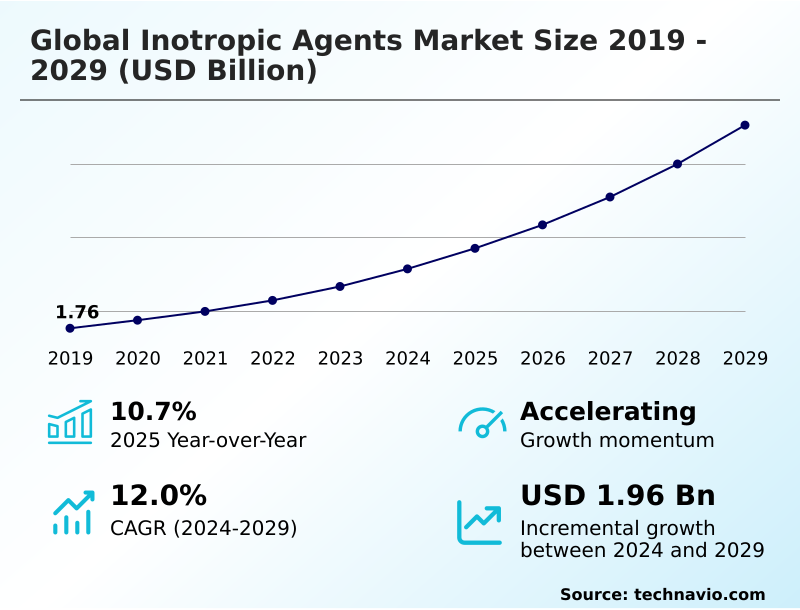

The inotropic agents market size is valued to increase by USD 1.96 billion, at a CAGR of 12% from 2024 to 2029. Increasing prevalence of cardiovascular diseases will drive the inotropic agents market.

Major Market Trends & Insights

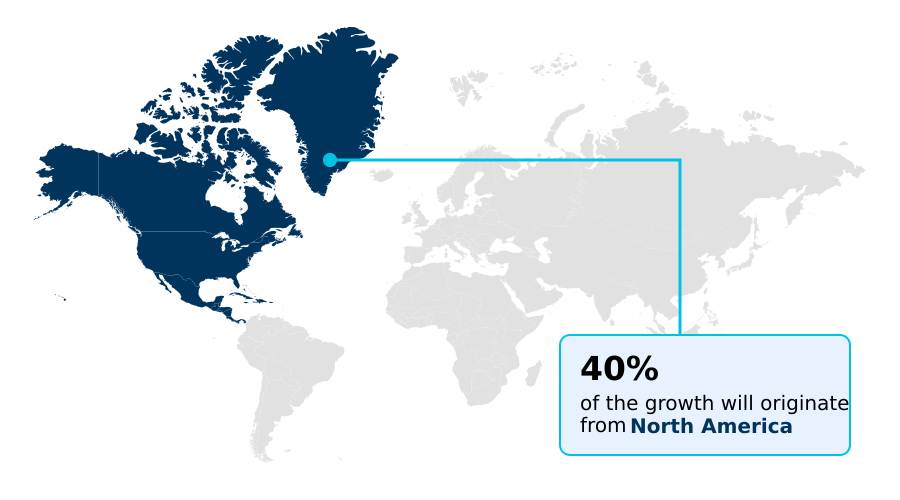

- North America dominated the market and accounted for a 39.6% growth during the forecast period.

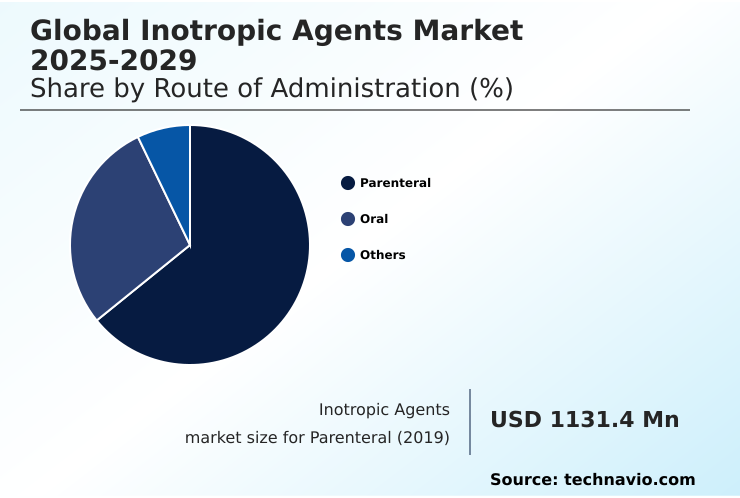

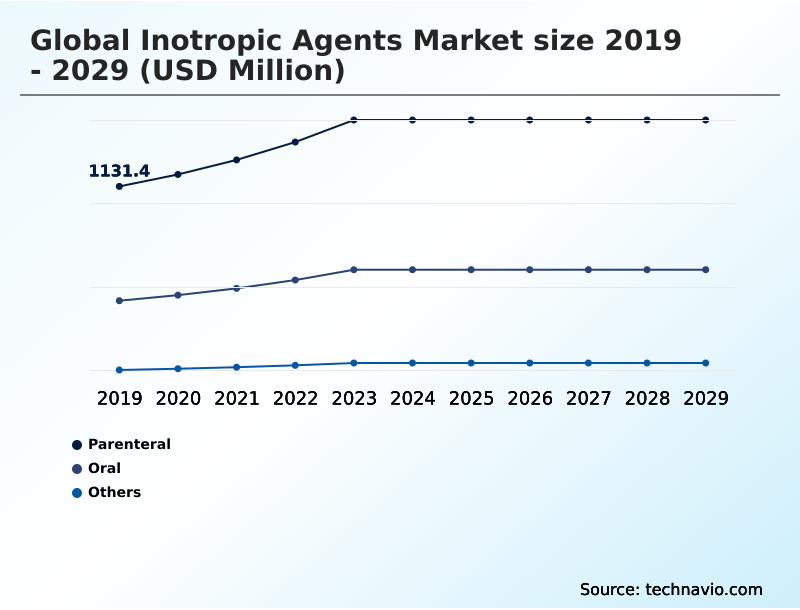

- By Route of Administration - Parenteral segment was valued at USD 1.49 billion in 2023

- By Type - Positive inotropic drugs segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 2.77 billion

- Market Future Opportunities: USD 1.96 billion

- CAGR from 2024 to 2029 : 12%

Market Summary

- The inotropic agents market is shaped by the pressing need for effective therapies to manage cardiac contractility in patients with cardiovascular diseases. The market is primarily driven by the increasing prevalence of heart failure and an aging global population, which expands the patient base requiring hemodynamic support.

- These agents are crucial in both acute settings, for conditions like cardiogenic shock management, and in chronic care. However, the use of traditional positive inotropic drugs and phosphodiesterase inhibitors is often limited by safety concerns, such as increased myocardial oxygen consumption and the risk of ventricular arrhythmias.

- This has spurred a significant trend toward developing novel oral inotropes and cardiac myosin activators with more favorable safety profiles. For instance, a hospital system could implement a protocol for transitioning patients from parenteral inotropes to a new oral agent, aiming to reduce readmission rates and the overall cost of care.

- This shift toward safer, long-term solutions, including outpatient inotropic therapy, is a key dynamic, balanced against competition from non-pharmacological interventions like mechanical circulatory support.

What will be the Size of the Inotropic Agents Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Inotropic Agents Market Segmented?

The inotropic agents industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Route of administration

- Parenteral

- Oral

- Others

- Type

- Positive inotropic drugs

- Negative inotropic drugs

- Others

- End-user

- Hospitals

- Homecare

- Specialty centers

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Route of Administration Insights

The parenteral segment is estimated to witness significant growth during the forecast period.

The parenteral route of administration is central to acute and critical care, where intravenous delivery of parenteral inotropes is indispensable for managing life-threatening conditions.

This method allows for immediate hemodynamic support in cases of cardiogenic shock management and acute decompensated heart failure, where rapid onset and precise dose titration are critical.

Evidence-based treatment protocols guide the use of these potent agents to augment cardiac function while navigating the risk of ventricular arrhythmias.

The clinical necessity for immediate intervention ensures this segment's dominance, with ongoing research focused on novel compounds that offer safer profiles.

For instance, new agents are being developed to improve cardiac efficiency, increasing pumping function by over 15% without a corresponding surge in oxygen demand. This innovation is critical for achieving regulatory approval for cardiovascular drugs in a cautious market.

The Parenteral segment was valued at USD 1.49 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Inotropic Agents Market Demand is Rising in North America Get Free Sample

The geographic landscape of the inotropic agents market is dominated by North America, which accounts for over 39% of the market's incremental growth, driven by high healthcare spending and a sophisticated research ecosystem.

The region's focus is on developing therapies for conditions like hypertrophic cardiomyopathy and improving long-term cardiovascular outcomes. Meanwhile, APAC is the fastest-growing region, fueled by an increasing prevalence of cardiovascular disease and modernizing healthcare infrastructure.

This growth is creating a significant need for effective management of cardiac contractility. In Europe, the market is mature, with a strong emphasis on personalized heart failure management and adherence to stringent clinical trial endpoints for heart failure.

The development of drug-device combination products and subcutaneous infusion systems is a global trend, with neurohormonal antagonists forming a key part of treatment regimens worldwide.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- A critical consideration in the inotropic agents market is the evaluation of safety profiles of novel inotropic agents. Clinicians and healthcare providers must weigh the benefits of new therapies against the potential for adverse events, such as managing arrhythmias from inotropic drugs.

- This is particularly relevant when comparing the role of inotropic agents versus mechanical circulatory support, where the latter may offer better long-term outcomes for specific patient populations despite higher initial costs.

- The development of oral inotropes for chronic heart failure aims to shift the treatment paradigm, potentially reducing the high cost of long-term inotropic therapy, which is often administered in inpatient or specialized homecare settings. For pharmaceutical companies, the challenge is not only demonstrating efficacy but also proving cost-effectiveness to secure favorable reimbursement and market access.

- Strategies focused on reducing mortality with combination therapies are gaining traction, as they can lead to better overall patient outcomes and a stronger value proposition. From a supply chain perspective, a successful oral agent could reduce the logistical complexity associated with infusion therapies by a significant margin, streamlining distribution and patient management.

What are the key market drivers leading to the rise in the adoption of Inotropic Agents Industry?

- The increasing prevalence of cardiovascular diseases, particularly heart failure, is a key driver for the inotropic agents market.

- The inotropic agents market is primarily driven by the increasing global prevalence of cardiovascular diseases, especially heart failure.

- The number of Americans with heart failure is projected to increase to 8.7 million by 2030, creating sustained demand for advanced heart failure treatment.

- This is compounded by a growing aging population, which is more susceptible to conditions requiring cardiac support. Increased healthcare expenditure worldwide is improving access to therapies, including positive inotropic drugs and cardiac glycosides.

- The growing awareness and proactive management of heart failure, supported by the integration of sodium-glucose cotransporter-2 inhibitors and angiotensin receptor-neprilysin inhibitors, are expanding the number of patients under active care.

- This creates opportunities for both acute interventions and long-term palliative care for heart failure, aligning with a push toward patient-centered cardiac care.

What are the market trends shaping the Inotropic Agents Industry?

- A paradigm shift toward novel inotropic agents with improved safety profiles is a key market trend. This is driven by the clinical need to mitigate adverse effects associated with traditional therapies.

- The inotropic agents market is trending toward innovation focused on improving safety and patient convenience. There is a significant push to develop novel agents like cardiac myosin activators and calcium sensitizers that provide therapeutic benefits without the adverse effects of older drugs. This includes the development of ino-lusitropic agents and SERCA2a stimulators, which offer more targeted mechanisms.

- For instance, optimized combination therapy for heart failure has been shown to reduce mortality risk by up to 60%. Another major trend is the shift toward outpatient inotropic therapy and home-based inotropic infusion, facilitated by advanced portable pump technology. This approach improves quality of life and reduces healthcare costs.

- The development of effective oral inotropes remains a key goal, aiming to provide a convenient long-term management option for chronic heart failure patients.

What challenges does the Inotropic Agents Industry face during its growth?

- Stringent regulatory hurdles and the high costs associated with clinical trials present a key challenge affecting industry growth.

- Significant challenges restrain the inotropic agents market, led by stringent regulatory requirements and the high cost of clinical development. The risk-benefit profile assessment for new cardiovascular drugs is rigorous, a legacy of safety concerns with traditional agents like phosphodiesterase inhibitors, which can increase myocardial oxygen consumption. This clinical conservatism creates a high barrier for new entrants.

- For example, thorough pharmacovigilance of cardiovascular drugs is standard practice. Furthermore, there is strong competition from alternative treatments. Advanced mechanical circulatory support, such as left ventricular assist devices, now shows a five-year survival rate of nearly 60% in some trials, presenting a viable alternative to long-term drug therapy.

- The high cost-effectiveness of cardiac therapies is a major consideration for payers, adding another layer of complexity to market access for new, expensive negative inotropic drugs and other agents.

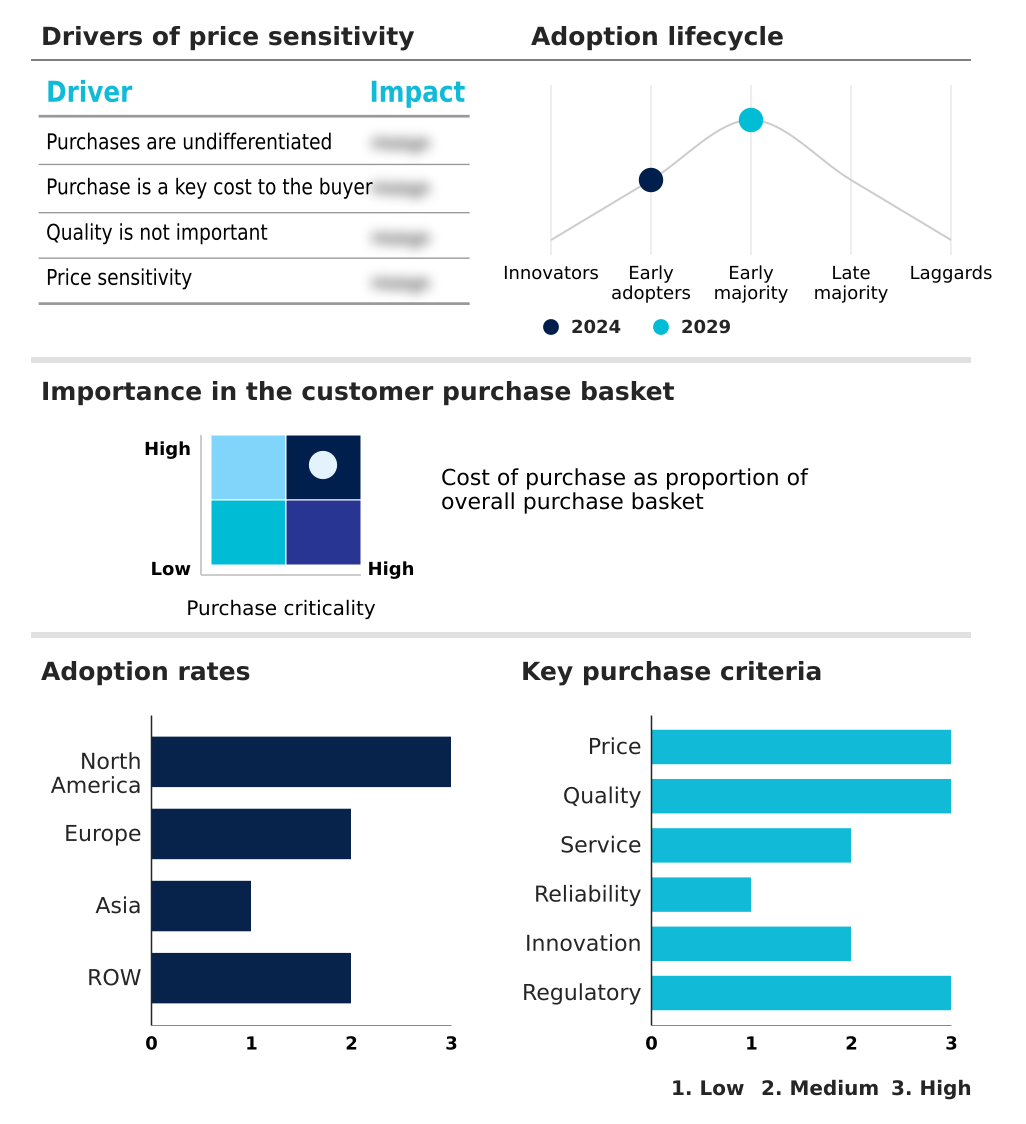

Exclusive Technavio Analysis on Customer Landscape

The inotropic agents market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the inotropic agents market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Inotropic Agents Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, inotropic agents market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbbVie Inc. - Provides formulations to enhance cardiac output and manage hemodynamic instability in severe heart failure, addressing critical care needs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Amgen Inc.

- AstraZeneca Plc

- Aurobindo Pharma Ltd.

- Baxter International Inc.

- Bayer AG

- Boehringer Ingelheim GmbH

- Bristol Myers Squibb Co.

- Cadila Pharmaceuticals Ltd.

- Cipla Inc.

- Eli Lilly and Co.

- GlaxoSmithKline Plc

- Hikma Pharmaceuticals Plc

- Johnson and Johnson Services

- Lupin Ltd.

- Merck and Co. Inc.

- Novartis AG

- Pfizer Inc.

- Sanofi SA

- Viatris Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Inotropic agents market

- In August 2024, Eli Lilly and Co. announced that its drug tirzepatide significantly reduced the risk of worsening heart failure events in adults with heart failure with preserved ejection fraction and obesity.

- In August 2024, Novo Nordisk announced the withdrawal of its FDA filing for Wegovy for heart failure, with plans to resubmit in early 2025 with additional data to support its application.

- In August 2024, Cytokinetics announced its plan to submit a New Drug Application to the FDA for aficamten for symptomatic obstructive hypertrophic cardiomyopathy in the fourth quarter of 2024, following positive trial results.

- In November 2024, the Food and Drug Administration approved BridgeBio Pharma's acoramidis for the treatment of transthyretin amyloid cardiomyopathy, a progressive and fatal heart disease.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Inotropic Agents Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12% |

| Market growth 2025-2029 | USD 1961.6 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 10.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Russia, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Singapore, Thailand, Indonesia, Brazil, Turkey, Saudi Arabia, South Africa, Australia and UAE |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The inotropic agents market is undergoing a significant transformation, moving beyond traditional catecholamines and cardiac glycosides. A key boardroom focus is the strategic investment in novel compounds like cardiac myosin activators and SERCA2a stimulators, which promise enhanced cardiac contractility with lower myocardial oxygen consumption.

- The development of these next-generation parenteral inotropes and oral inotropes is critical, as they aim to provide effective hemodynamic support while minimizing the risk of ventricular arrhythmias. This shift addresses the historical limitations of phosphodiesterase inhibitors and older positive inotropic drugs.

- For instance, clinical trials for ino-lusitropic agents are demonstrating the potential to improve both systolic and diastolic function, a dual benefit that could reduce rehospitalization rates for acute decompensated heart failure by over 20%. The market is also seeing targeted therapies for specific conditions like hypertrophic cardiomyopathy and heart failure with preserved ejection fraction.

- The integration of these agents with foundational therapies, including sodium-glucose cotransporter-2 inhibitors, angiotensin receptor-neprilysin inhibitors, and neurohormonal antagonists, is redefining a complex treatment landscape shaped by competition from mechanical circulatory support and negative inotropic drugs.

What are the Key Data Covered in this Inotropic Agents Market Research and Growth Report?

-

What is the expected growth of the Inotropic Agents Market between 2025 and 2029?

-

USD 1.96 billion, at a CAGR of 12%

-

-

What segmentation does the market report cover?

-

The report is segmented by Route of Administration (Parenteral, Oral, and Others), Type (Positive inotropic drugs, Negative inotropic drugs, and Others), End-user (Hospitals, Homecare, Specialty centers, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing prevalence of cardiovascular diseases, Stringent regulatory hurdles and high clinical trial costs

-

-

Who are the major players in the Inotropic Agents Market?

-

AbbVie Inc., Amgen Inc., AstraZeneca Plc, Aurobindo Pharma Ltd., Baxter International Inc., Bayer AG, Boehringer Ingelheim GmbH, Bristol Myers Squibb Co., Cadila Pharmaceuticals Ltd., Cipla Inc., Eli Lilly and Co., GlaxoSmithKline Plc, Hikma Pharmaceuticals Plc, Johnson and Johnson Services, Lupin Ltd., Merck and Co. Inc., Novartis AG, Pfizer Inc., Sanofi SA and Viatris Inc.

-

Market Research Insights

- The inotropic agents market is shaped by a complex interplay of clinical needs and therapeutic advancements. While the rising incidence of heart failure drives demand, the adoption of new treatments is influenced by their demonstrated value.

- For example, optimized combination therapy for heart failure has been shown to reduce mortality risk by up to 60%, creating a high benchmark for new entrants. Furthermore, advanced heart failure treatment is shifting, with some mechanical circulatory support devices showing a five-year survival rate of nearly 60%, rivaling heart transplantation outcomes.

- This competition pushes the focus toward patient-centered cardiac care and the cost-effectiveness of cardiac therapies, especially for palliative care for heart failure. The development of subcutaneous infusion systems and drug-device combination products reflects a move toward improving quality of life and facilitating home-based inotropic infusion, aligning with modern healthcare's value-based objectives.

We can help! Our analysts can customize this inotropic agents market research report to meet your requirements.

RIA -

RIA -