Insulin Pump Market Size 2026-2030

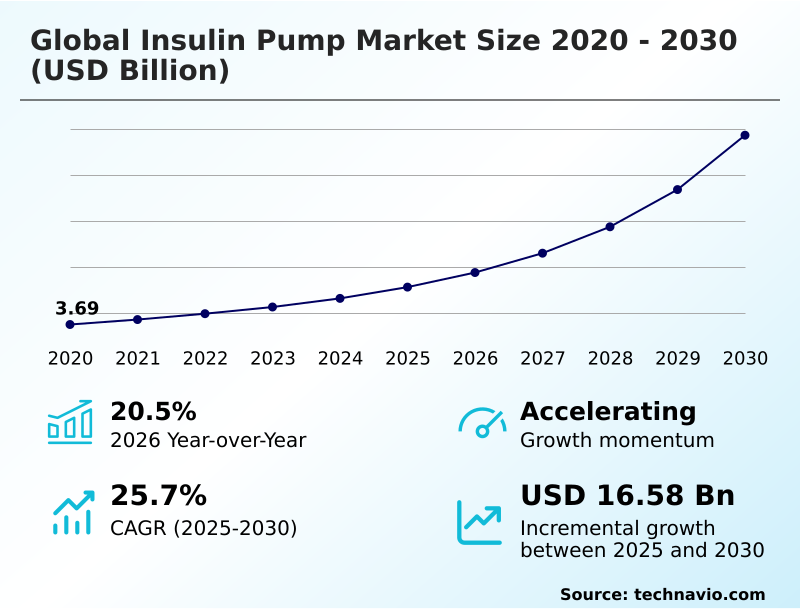

The insulin pump market size is valued to increase by USD 16.58 billion, at a CAGR of 25.7% from 2025 to 2030. Rising global burden of diabetes will drive the insulin pump market.

Major Market Trends & Insights

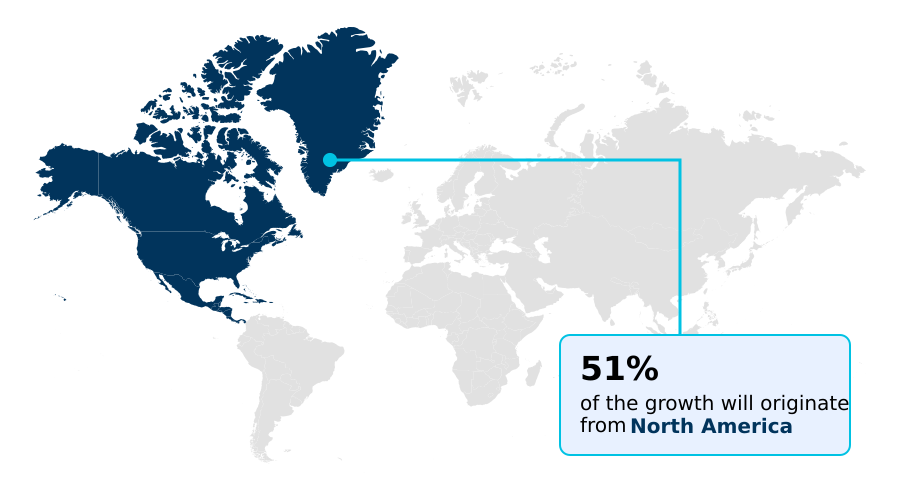

- North America dominated the market and accounted for a 50.8% growth during the forecast period.

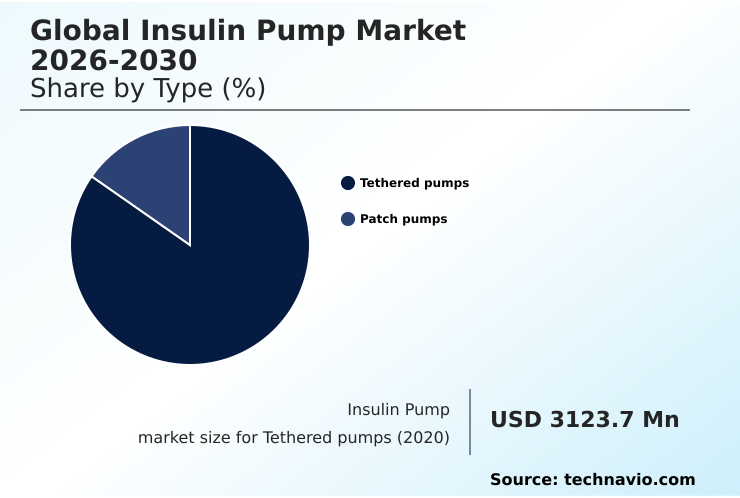

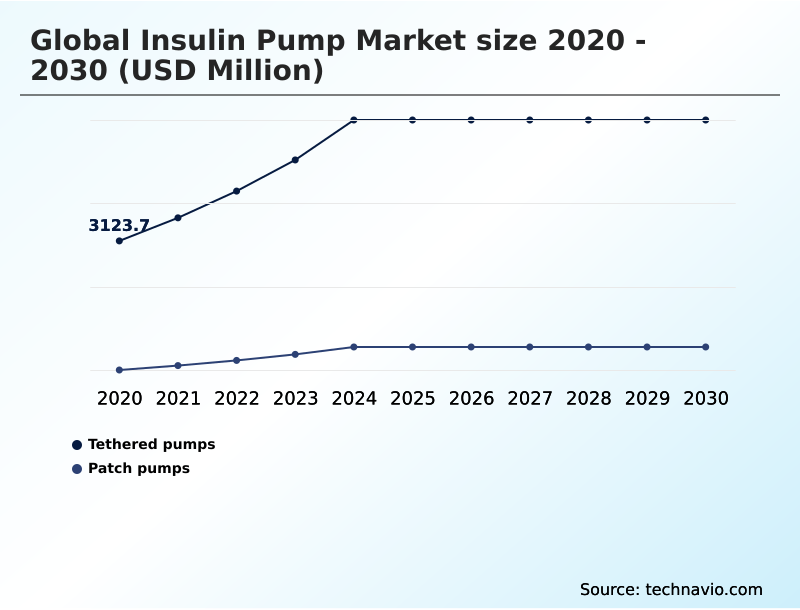

- By Type - Tethered pumps segment was valued at USD 5.52 billion in 2024

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 20.66 billion

- Market Future Opportunities: USD 16.58 billion

- CAGR from 2025 to 2030 : 25.7%

Market Summary

- The insulin pump market is undergoing a significant transformation, driven by technological advancements that enhance patient autonomy and clinical outcomes. The core of this evolution lies in the shift from manual insulin administration to sophisticated automated insulin delivery (AID) systems that improve glycemic control.

- These platforms, integrating data from continuous glucose monitoring sensors, are becoming the standard of care for type 1 diabetes management and are increasingly being adapted for type 2 diabetes technology. Innovations in patch pump technology offer greater discretion and convenience, improving the quality of life for users.

- However, market expansion is moderated by challenges such as navigating complex reimbursement policies and ensuring robust cybersecurity for medical devices that are increasingly connected.

- A key business scenario involves hospitals implementing these systems for inpatient care; they must balance the high initial device cost against long-term benefits like reduced length of stay and fewer hypoglycemic events, illustrating the complex interplay between clinical efficacy and economic pressures that defines the industry's trajectory.

- This focus on value-based outcomes is compelling manufacturers to prioritize not just technological innovation but also patient self-management tools and affordability.

What will be the Size of the Insulin Pump Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Insulin Pump Market Segmented?

The insulin pump industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Tethered pumps

- Patch pumps

- Distribution channel

- Offline

- Online

- End-user

- Hospitals and Clinics

- Homecare

- Laboratories

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Type Insights

The tethered pumps segment is estimated to witness significant growth during the forecast period.

The market is segmented by device architecture, primarily between traditional tethered insulin pump models and modern patch pump technology. Tethered systems, long the standard for insulin pump therapy, offer large reservoir capacities and flexible infusion set placement.

In contrast, the adoption of wearable diabetes devices like tubeless patch pumps is accelerating, driven by a demand for more discreet diabetes technology and improved user experience (UX) in medtech.

These innovations are critical for patient adherence solutions, particularly in active user groups and for type 1 diabetes management.

Advanced systems designed for optimal basal-bolus insulin delivery have demonstrated an ability to improve glycemic stability by over 15%, highlighting the clinical advantages driving segmentation trends.

The Tethered pumps segment was valued at USD 5.52 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 50.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Insulin Pump Market Demand is Rising in North America Get Free Sample

North America is the dominant region, contributing over 50% of the market's incremental growth, driven by high adoption rates of automated insulin delivery (AID) and hybrid closed-loop system technologies. Favorable reimbursement for tubeless insulin pump models supports this leadership.

Europe follows, accounting for nearly 27% of the growth opportunity, with a strong focus on improving time-in-range (TIR) metrics through advanced remote patient monitoring. In contrast, market penetration in Asia is emerging, with a growing focus on cost-effective solutions.

Across all regions, advancements in insulin infusion set design are improving user comfort, while next-generation systems are exploring glucose-ketone monitoring and dual-hormone pump capabilities to further refine therapy and create a more comprehensive ambulatory glucose profile.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the insulin pump market is increasingly focused on nuanced, long-tail considerations. A key area of investigation is the impact of AID systems on glycemic variability, with a clear link between advanced algorithms and improved patient outcomes. The cost-effectiveness of insulin pump therapy remains a central debate, influencing purchasing decisions.

- For specific user groups, the choice of patch pump vs tethered pump for athletes highlights the need for specialized device features. The role of AI in predictive glucose algorithms is a critical R&D focus, aiming to preempt glycemic excursions. A significant operational hurdle is how to best go about integrating CGM data into electronic health records for seamless care coordination.

- For manufacturers, addressing the challenges in pediatric insulin pump use and mitigating cybersecurity vulnerabilities in connected insulin pumps are top priorities. Demonstrating how to improve time-in-range with hybrid closed-loop systems is crucial for market differentiation. The complex reimbursement landscape for tubeless insulin pumps continues to shape market access.

- Product development cycles are heavily influenced by advancements in insulin infusion set design and user interface design for insulin pump mobile apps, with firms adopting agile development methodologies reporting up to a 15% faster time-to-market than competitors using traditional waterfall models.

- The regulatory pathways for novel insulin delivery devices, the future of dual-hormone artificial pancreas systems, and telemedicine's role in remote insulin pump management are shaping long-term strategy. Furthermore, refining patient training protocols for automated insulin delivery, exploring materials science innovations in insulin reservoirs, and defining sensor accuracy requirements for closed-loop systems are essential for safety and efficacy.

- Finally, understanding the long-term outcomes of sensor-augmented pump therapy, addressing behavioral factors affecting diabetes technology adherence, and solving data privacy concerns with cloud-connected diabetes devices are vital for sustainable growth.

What are the key market drivers leading to the rise in the adoption of Insulin Pump Industry?

- The rising global burden of diabetes serves as a primary driver, fueling demand for more effective and accessible insulin pump technologies.

- The rising global prevalence of diabetes is a primary market driver, compelling a shift toward a value-based healthcare model that prioritizes superior glycemic control.

- Favorable government initiatives and reimbursement policies are accelerating the adoption of type 2 diabetes technology and devices for pediatric diabetes care, with subsidized programs showing a 20% higher uptake rate.

- The availability of self-management education programs is also crucial, improving patient proficiency with technologies like sensor-augmented pump systems.

- These devices, featuring algorithm-driven dosing and predictive low-glucose suspend functions, are essential for both hyperglycemia management and inpatient glycemic management, where their use has been linked to a 15% decrease in hospital readmission rates for diabetes-related complications.

What are the market trends shaping the Insulin Pump Industry?

- The increasing prevalence of diabetes awareness programs is a notable market trend. These initiatives are expected to foster greater understanding and adoption of advanced diabetes management solutions.

- The market is witnessing a significant trend toward greater patient self-management, driven by the growing availability of advanced diabetes technology on e-commerce platforms and through telehealth diabetes support channels. This shift has accelerated diabetes technology adoption, with platforms reporting up to a 25% increase in direct-to-consumer engagement.

- Concurrently, the proliferation of new product launches emphasizes interoperability standards, enabling seamless CGM integration and the use of mobile health (mHealth) applications for viewing real-time glucose data. These integrated systems provide enhanced clinical decision support, with some demonstrating a 30% reduction in hypoglycemic events, proving their effectiveness in hypoglycemia prevention.

- Even the smart insulin pen is now part of this connected ecosystem.

What challenges does the Insulin Pump Industry face during its growth?

- The high costs associated with insulin pumps and their ongoing supplies present a significant challenge, potentially limiting market growth and patient access.

- High device costs and the stringent framework for medical device regulation present significant market challenges. The complex approval process can add up to 24 months to the development timeline for a new artificial pancreas system, delaying access to innovations in closed-loop insulin delivery.

- Additionally, the risk of device malfunction, from a faulty insulin reservoir to software glitches, necessitates robust human factors engineering and post-market surveillance. Concerns around cybersecurity for medical devices are also growing, as vulnerabilities could compromise diabetes device data analytics.

- Effective patient training protocols are essential to mitigate use-related errors, which account for approximately 40% of reported adverse events, thereby reducing risks like high glucose variability and potential for diabetic ketoacidosis.

Exclusive Technavio Analysis on Customer Landscape

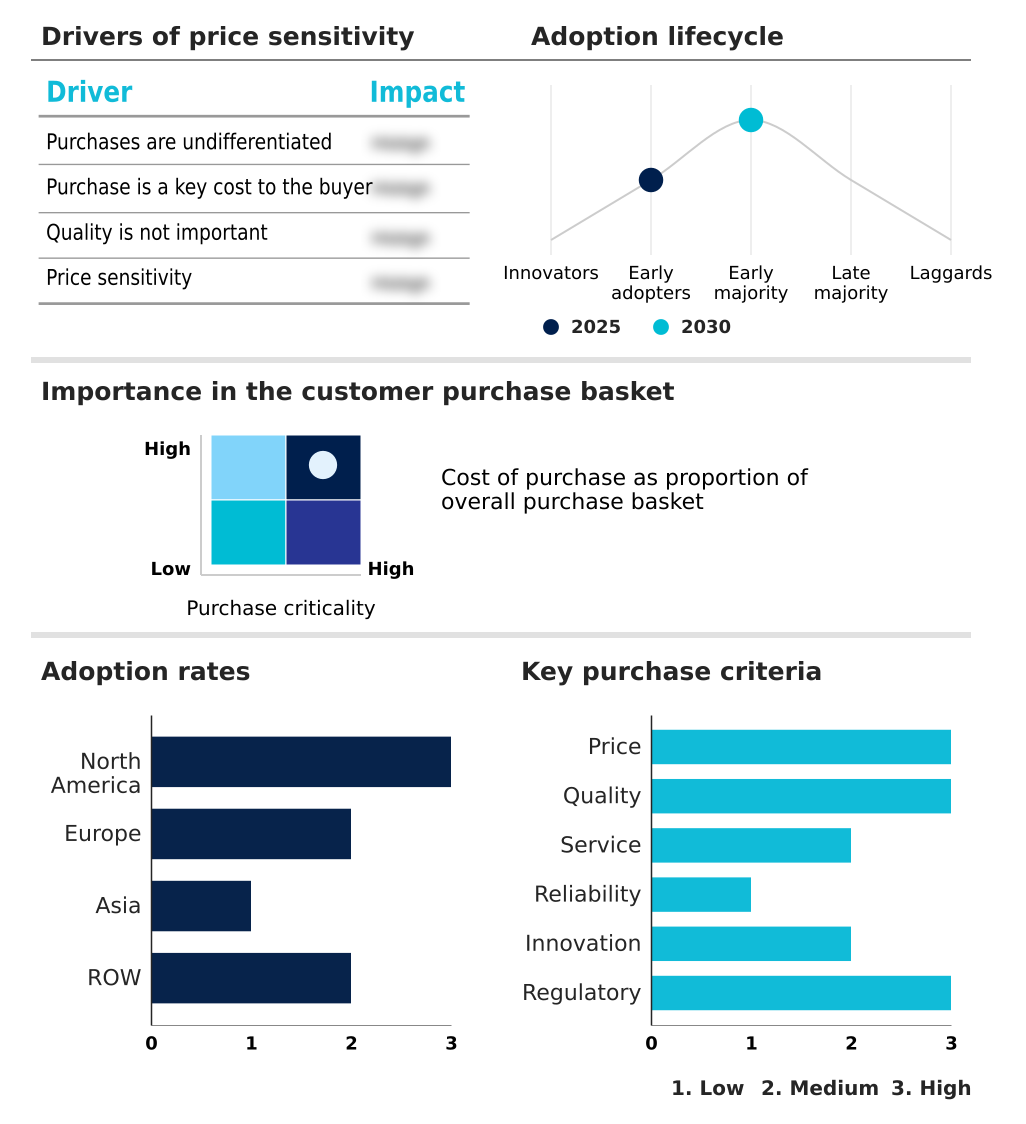

The insulin pump market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the insulin pump market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Insulin Pump Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, insulin pump market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - Offerings center on advanced automated insulin delivery (AID) systems and integrated continuous glucose monitors, enhancing glycemic control and patient self-management through innovative diabetes technology.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- B.Braun SE

- Beta Bionics Inc.

- CeQur SA

- ConvaTec Group Plc

- Dexcom Inc.

- Eli Lilly and Co.

- Eoflow Co. Ltd.

- F. Hoffmann La Roche Ltd.

- Insulet Corp.

- Johnson and Johnson Services

- MannKind Corp.

- Medtronic Plc

- Nipro Corp.

- Nova Biomedical Corp.

- Novo Nordisk AS

- Senseonics Holdings Inc.

- SOOIL Development Co. Ltd.

- Tandem Diabetes Care Inc.

- Ypsomed Holding AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Insulin pump market

- In August 2024, Insulet Corp. received FDA approval for its Omnipod 5 AID system for individuals with type 2 diabetes, marking the first clearance of a patch pump for this population.

- In February 2025, Tandem Diabetes Care Inc. announced it received FDA clearance for its Control-IQ+ technology for adults with type 2 diabetes, expanding automated insulin delivery to a larger patient base.

- In April 2025, Insulet Corp. initiated the commercial launch of its Omnipod 5 system in Canada for individuals with type 1 diabetes, following approval from Health Canada and securing public reimbursement in key provinces.

- In June 2025, Tandem Diabetes Care Inc. and Abbott Laboratories announced a strategic agreement to integrate Abbott's developmental dual glucose-ketone monitoring sensor with Tandem's insulin delivery systems to prevent diabetic ketoacidosis.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Insulin Pump Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 280 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 25.7% |

| Market growth 2026-2030 | USD 16578.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 20.5% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Thailand, Indonesia, Brazil, Argentina, Saudi Arabia, Colombia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The insulin pump market is characterized by a relentless drive toward enhancing glycemic control through sophisticated insulin pump therapy. The core of this evolution is the automated insulin delivery (AID) system, which leverages real-time glucose data from continuous glucose monitoring (CGM) for algorithm-driven dosing.

- This technology, exemplified by the hybrid closed-loop system and sensor-augmented pump, is pivotal for maintaining time-in-range (TIR) and reducing glucose variability. Key device architectures include the traditional tethered insulin pump with its infusion set and the increasingly popular patch pump technology.

- For boardroom strategy, the expansion into new patient segments, such as those with type 2 diabetes, has been shown to increase the total addressable market by over 40%. This strategic pivot requires navigating medical device regulation and adhering to interoperability standards. Innovations in smart insulin pen design and the insulin reservoir are also crucial.

- A primary clinical goal is preventing diabetic ketoacidosis (DKA) using technologies like predictive low-glucose suspend. The market's direction is also shaped by the need for robust cybersecurity for medical devices, the adoption of a value-based healthcare model, and tools that facilitate patient self-management, including remote patient monitoring and the ambulatory glucose profile.

What are the Key Data Covered in this Insulin Pump Market Research and Growth Report?

-

What is the expected growth of the Insulin Pump Market between 2026 and 2030?

-

USD 16.58 billion, at a CAGR of 25.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Tethered pumps, and Patch pumps), Distribution Channel (Offline, and Online), End-user (Hospitals and Clinics, Homecare, and Laboratories) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rising global burden of diabetes, High costs associated with insulin pumps

-

-

Who are the major players in the Insulin Pump Market?

-

Abbott Laboratories, B.Braun SE, Beta Bionics Inc., CeQur SA, ConvaTec Group Plc, Dexcom Inc., Eli Lilly and Co., Eoflow Co. Ltd., F. Hoffmann La Roche Ltd., Insulet Corp., Johnson and Johnson Services, MannKind Corp., Medtronic Plc, Nipro Corp., Nova Biomedical Corp., Novo Nordisk AS, Senseonics Holdings Inc., SOOIL Development Co. Ltd., Tandem Diabetes Care Inc. and Ypsomed Holding AG

-

Market Research Insights

- The market is defined by rapid innovation in wearable diabetes devices, moving closer to a fully autonomous artificial pancreas system. This progress is fueling higher diabetes technology adoption rates, with patient cohorts using integrated systems showing a 15% better adherence rate compared to traditional methods. However, navigating varied reimbursement policies remains a critical factor influencing access.

- Systems providing enhanced clinical decision support have been shown to improve time-in-range metrics by over 20%, directly impacting patient outcomes and demonstrating a clear return on investment for payers. These advancements underscore a strategic focus on developing effective patient adherence solutions that balance cutting-edge technology with real-world usability and economic viability.

We can help! Our analysts can customize this insulin pump market research report to meet your requirements.

RIA -

RIA -