Machine Identity Management Market Size 2026-2030

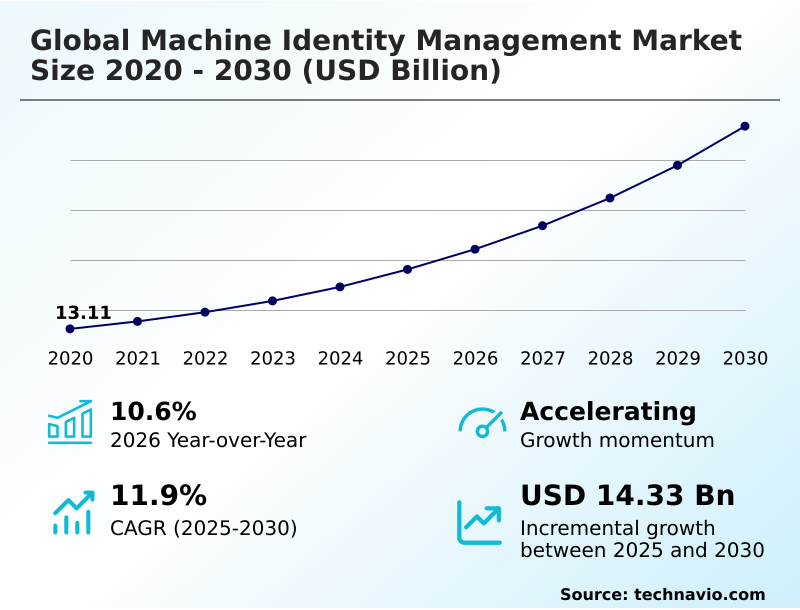

The machine identity management market size is valued to increase by USD 14.33 billion, at a CAGR of 11.9% from 2025 to 2030. Proliferation of cloud computing, containers, and devops practices will drive the machine identity management market.

Major Market Trends & Insights

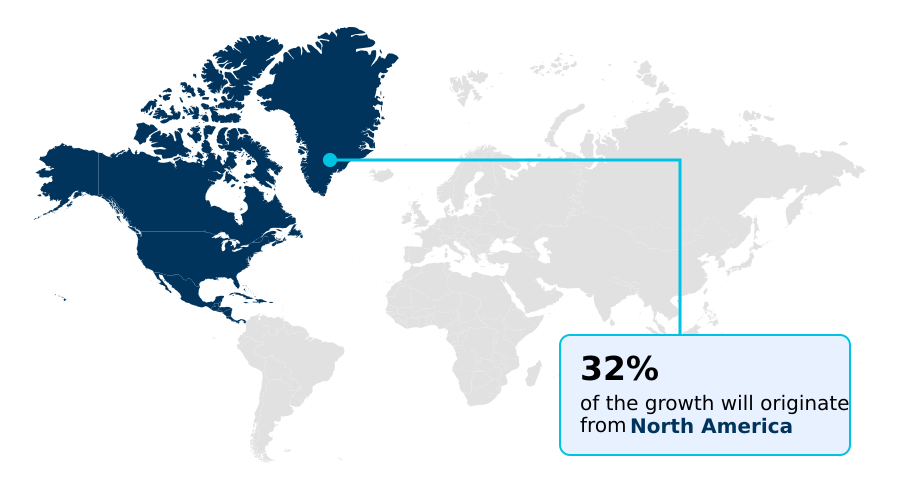

- North America dominated the market and accounted for a 32.5% growth during the forecast period.

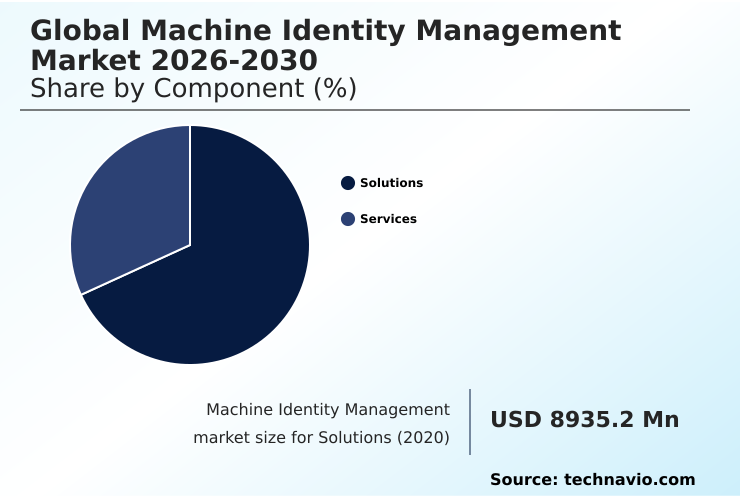

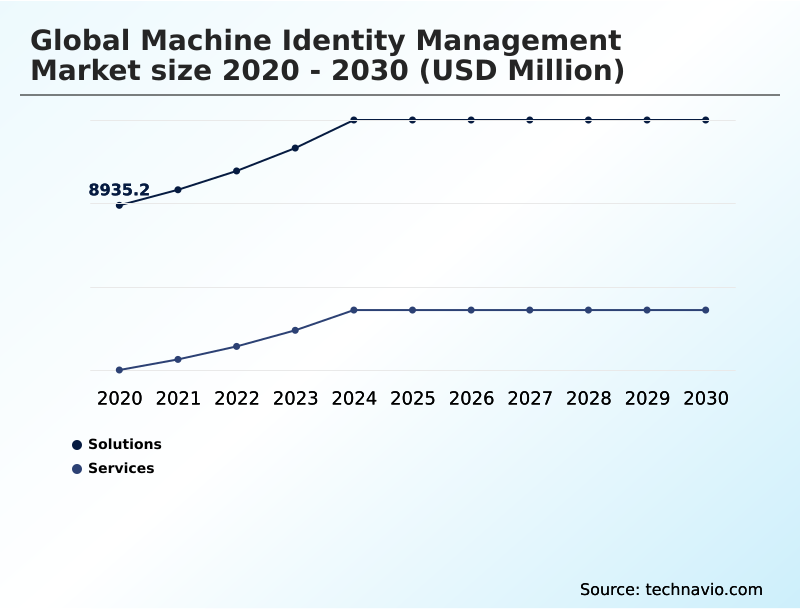

- By Component - Solutions segment was valued at USD 11.40 billion in 2024

- By Deployment - On-premises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 20.28 billion

- Market Future Opportunities: USD 14.33 billion

- CAGR from 2025 to 2030 : 11.9%

Market Summary

- The machine identity management market is undergoing a fundamental shift as digital ecosystems move from human-centric to automated frameworks dominated by non-human identities. This transition is driven by the adoption of agile development and cloud-native architectures, which result in a surge of ephemeral identities for microservices, containers, and APIs.

- The core objective is to apply principles of identity governance, traditionally used for people, to this expanding landscape of machines. For instance, a financial institution implementing an open banking platform relies on thousands of API keys and TLS certificates for secure data exchange with third-party partners.

- Without an automated system for certificate lifecycle management and enforcing access control policies, a single expired certificate or compromised private key could disrupt services or lead to a massive data breach. Addressing this requires a zero trust architecture approach, where every service-to-service authentication is verified, and automated credential rotation is standard practice, ensuring the integrity of all machine-to-machine communication.

What will be the Size of the Machine Identity Management Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Machine Identity Management Market Segmented?

The machine identity management industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Solutions

- Services

- Deployment

- On-premises

- Cloud-based

- Application

- Certificate lifecycle management

- Device authentication

- Secure communication

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The solutions segment is estimated to witness significant growth during the forecast period.

Solutions for machine identity management are evolving from basic tools into sophisticated platforms essential for modern enterprise security. These platforms provide centralized control for discovering, managing, and securing the entire certificate lifecycle management process for all non-human identities.

Core functionality addresses the need for pki automation and crypto-agility, with discovery scans of IT assets, including networks and code repositories, creating a complete and continuously updated inventory.

Through integrations with both public and private certificate authorities, these solutions automate policy-driven requests, secure provisioning, and proactive renewal, reducing manual errors by over 90%.

They are fundamental for workload authentication, enforcing access control policies, and managing ephemeral identities in dynamic settings, providing the secure boot for digital trust and mitigating advanced persistent threats.

The Solutions segment was valued at USD 11.40 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 32.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Machine Identity Management Market Demand is Rising in North America Get Free Sample

The geographic landscape of machine identity management is defined by varying levels of maturity and distinct regional drivers.

North America leads in adoption, accounting for over 32% of incremental growth, fueled by its dense concentration of cloud-native enterprises and a strong push toward DevSecOps, where CI/CD pipeline security is paramount.

In this region, managing ephemeral workloads and securing machine-to-machine communication are top priorities. Europe’s market is heavily influenced by strict regulations like GDPR and NIS2, driving demand for solutions that ensure data sovereignty and provide robust identity federation capabilities.

The APAC region is characterized by rapid digitalization, with many organizations leapfrogging legacy systems, creating a massive need for scalable tokenization and workload identity solutions to secure new IoT and smart city deployments, where machine identities often scale into the billions.

Market Dynamics

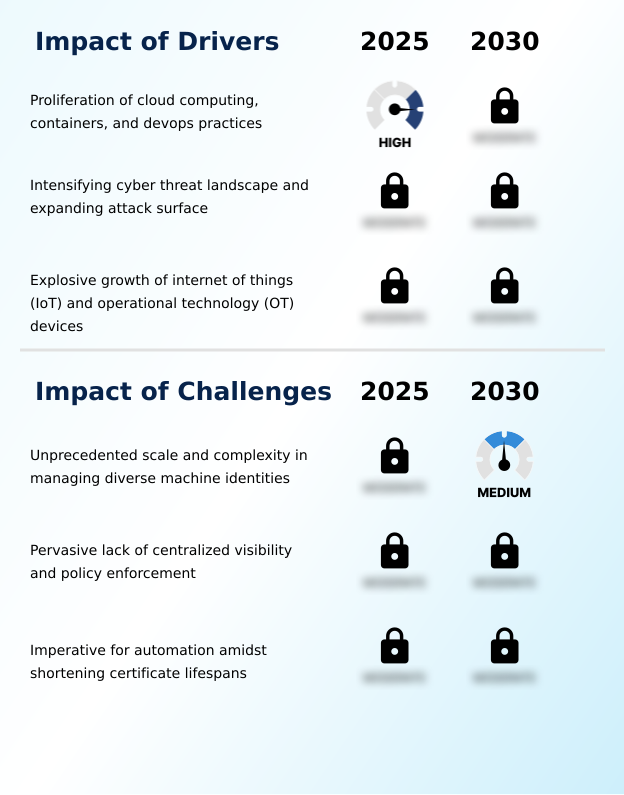

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- As enterprises accelerate digital transformation, the conversation around security is pivoting to address the nuances of machine identities. Effectively managing machine identities in Kubernetes is no longer a niche technical problem but a core business continuity issue.

- The focus is on implementing practical strategies, such as securing DevOps secrets with Vault and establishing a strong role of HSM in PKI strategy to protect cryptographic roots of trust. The rise of serverless computing introduces new complexities, making machine identity for serverless functions a critical area of development.

- For industries deploying IoT at scale, automating certificate management for IoT is essential to prevent widespread vulnerabilities. This is closely tied to the broader security posture, where zero trust for API-driven architectures becomes the default model, requiring robust methods like securing service mesh communication with mTLS.

- Addressing vulnerabilities in SSH key management and protecting code-signing keys securely are foundational tasks that prevent significant breaches. In converged environments, OT security using machine identities is vital for protecting critical infrastructure.

- Beyond technology, the compliance challenges with ephemeral identities are forcing organizations to rethink governance, leading to a greater emphasis on identity governance for non-human users and the ability to prevent certificate-related service outages. This comprehensive lifecycle approach, from the lifecycle of a code signing certificate to automating TLS renewal across multi-cloud environments, underscores the market's maturity.

What are the key market drivers leading to the rise in the adoption of Machine Identity Management Industry?

- The proliferation of cloud computing, containerization, and DevOps practices stands as a key driver for the machine identity management market's growth.

- Market growth is primarily driven by the profound shift to distributed, cloud-native environments where machine identities vastly outnumber human ones, often by a ratio of more than forty to one.

- The proliferation of IoT and OT system security requirements adds billions of new endpoints, each demanding a unique and immutable identity for secure boot processes and trusted communication.

- This explosion of ephemeral identities, created and destroyed in seconds within DevOps workflows and microservices architectures, renders manual management obsolete.

- Consequently, there is immense demand for scalable, agile security solutions that embed directly into the CI/CD pipeline, a concept at the heart of DevSecOps.

- The need for secure remote access and robust secrets management to protect credentials for these non-human identities is a foundational driver across all industries.

What are the market trends shaping the Machine Identity Management Industry?

- The integration with Zero Trust architecture is emerging as a pivotal market trend. It is rapidly establishing itself as a core tenet for modern security frameworks that handle both human and machine interactions.

- Key market trends are centered on the deep integration of machine identities into a zero trust architecture, which is becoming the default security model for modern enterprises. This paradigm shift mandates continuous verification for all service-to-service authentication, making technologies like mutual TLS (mTLS) standard practice.

- The operational tempo has been drastically increased by the industry-wide move to short-lived certificates, with lifespans now commonly at 90 days. This has made automated discovery and automated credential rotation non-negotiable capabilities, with advanced platforms reducing manual renewal efforts by over 95%.

- Furthermore, the application of AI and ML for behavioral analysis allows for the detection of anomalies, such as an API key being used from an unusual location, adding a layer of proactive threat detection and enabling true cryptographic agility.

What challenges does the Machine Identity Management Industry face during its growth?

- The unprecedented scale and complexity of managing diverse and often ephemeral machine identities across hybrid environments present a key challenge to industry growth.

- The foremost market challenge is the sheer scale and complexity of modern digital ecosystems, where security teams often discover that up to 50% of machine identities are unmanaged 'shadow' credentials. This lack of centralized visibility and policy enforcement, stemming from fragmented ownership across networking, development, and infrastructure teams, creates a vast and undefended attack surface.

- Organizations struggle with the secret zero problem, where initial credentials to access secrets management systems are themselves insecure. The pervasive lack of a unified inventory makes it impossible to enforce consistent access control policies or manage the credential lifecycle effectively.

- This is exacerbated by the need for crypto-agility to handle shortening certificate lifespans, a task that becomes nearly impossible without a foundational root of trust and automated, policy-as-code frameworks.

Exclusive Technavio Analysis on Customer Landscape

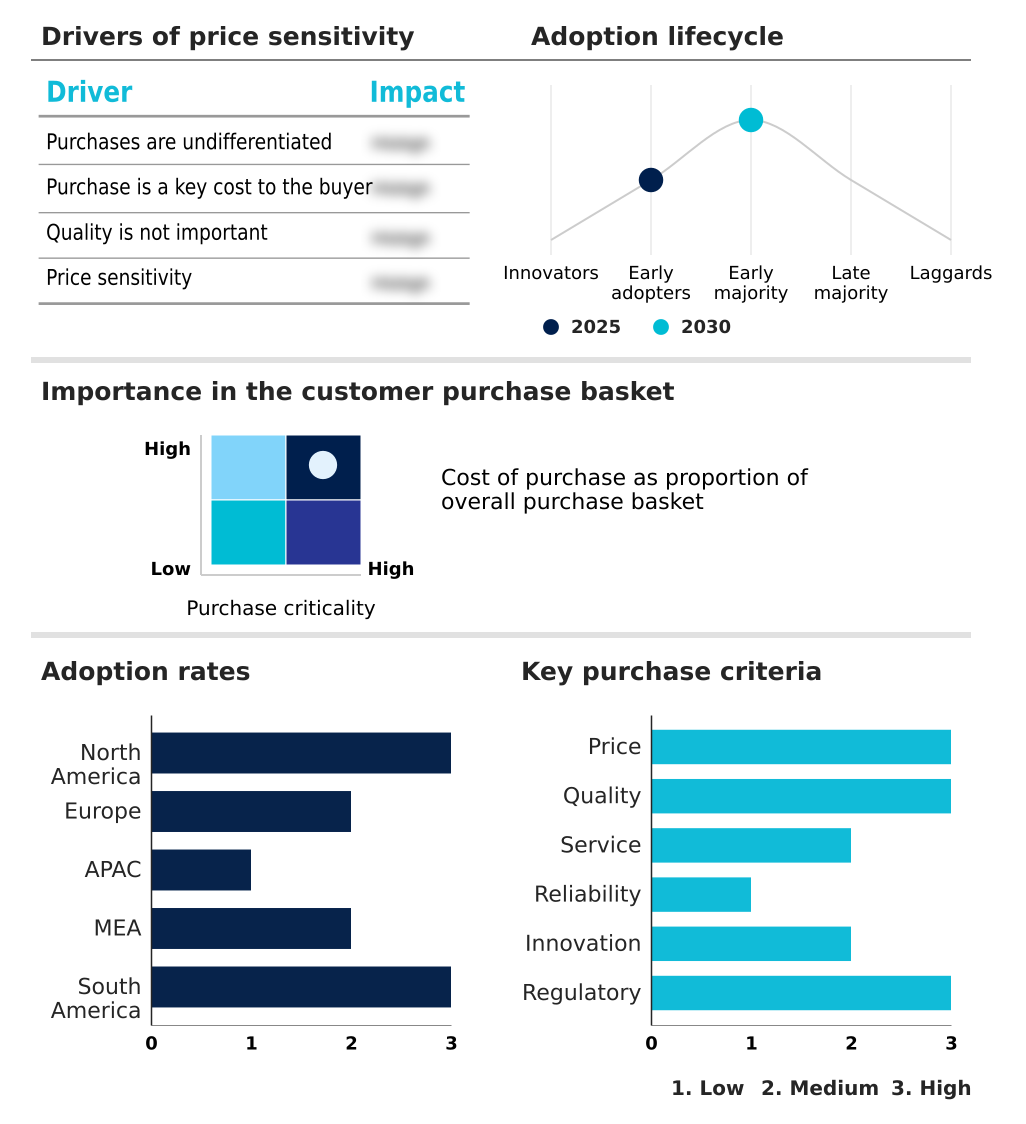

The machine identity management market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the machine identity management market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Machine Identity Management Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, machine identity management market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon Web Services Inc. - Offers comprehensive machine identity management for securing workload identities and authentication across diverse cloud environments, ensuring cryptographic trust from device to data center.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon Web Services Inc.

- AppViewX Inc.

- BeyondTrust Corp.

- Broadcom Inc.

- CyberArk Software Ltd.

- Delinea Inc.

- DigiCert Inc.

- Entrust Corp.

- Fortanix

- GlobalSign Ltd.

- Google LLC

- HashiCorp Inc.

- IBM Corp.

- Keyfactor

- Microsoft Corp.

- Nexus Group

- Okta Inc.

- SailPoint Technologies Inc.

- Thales Group

- Zoho Corp. Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Machine identity management market

- In January, 2025, Microsoft and Telefonica announced a strategic collaboration to integrate artificial intelligence services with regional connectivity solutions, facilitating the secure adoption of digital tools by managing machine identities that enable cloud communication.

- In February, 2025, CyberArk announced a strategic pivot to position machine identity security as its primary growth engine, focusing on public key infrastructure and certificate lifecycle management as core components of zero trust architecture.

- In March, 2025, AppViewX successfully completed the acquisition of Eos, an innovator in AI-native identity control planes, aiming to integrate agentic governance and privileged access controls into its automated certificate management platform.

- In April, 2025, the organizers of Identity Management Day established a global theme focused on achieving parity between human and machine identities, emphasizing the need to protect the automated service accounts driving agentic artificial intelligence.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Machine Identity Management Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.9% |

| Market growth 2026-2030 | USD 14326.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.6% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The machine identity management market is fundamentally reshaping enterprise cybersecurity by addressing the explosive growth of non-human identities. Boardroom-level decisions are now influenced by the operational risks tied to this landscape, particularly as the industry moves toward 90-day certificate lifespans, making budget allocation for robust PKI automation and DevSecOps tooling a critical strategic priority.

- Platforms that provide comprehensive certificate lifecycle management are essential for maintaining service uptime, with successful implementations reducing certificate-related outages by over 90%. The strategic focus is on achieving a unified view of all cryptographic keys and digital certificates, including TLS certificates, SSH keys, API keys, and private keys.

- This involves a zero trust architecture, deep integration into cloud-native platforms, and effective secrets management. Ensuring robust identity governance across microservices and containerization requires advanced solutions that support workload authentication, enforce access control policies, and provide the crypto-agility needed for modern, dynamic environments.

- Ultimately, managing this ecosystem of ephemeral identities is central to mitigating advanced persistent threats and maintaining a secure digital posture.

What are the Key Data Covered in this Machine Identity Management Market Research and Growth Report?

-

What is the expected growth of the Machine Identity Management Market between 2026 and 2030?

-

USD 14.33 billion, at a CAGR of 11.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solutions, and Services), Deployment (On-premises, and Cloud-based), Application (Certificate lifecycle management, Device authentication, and Secure communication) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of cloud computing, containers, and devops practices, Unprecedented scale and complexity in managing diverse machine identities

-

-

Who are the major players in the Machine Identity Management Market?

-

Amazon Web Services Inc., AppViewX Inc., BeyondTrust Corp., Broadcom Inc., CyberArk Software Ltd., Delinea Inc., DigiCert Inc., Entrust Corp., Fortanix, GlobalSign Ltd., Google LLC, HashiCorp Inc., IBM Corp., Keyfactor, Microsoft Corp., Nexus Group, Okta Inc., SailPoint Technologies Inc., Thales Group and Zoho Corp. Pvt. Ltd.

-

Market Research Insights

- Market dynamics are increasingly shaped by the dramatic shift to ephemeral workloads, where machine identities outnumber human users by ratios exceeding forty to one in some automated environments. This has made securing machine-to-machine communication a primary focus. Organizations are adopting identity-aware proxy models and strengthening API security to cope with this scale.

- The industry-wide move to short-lived certificates with 90-day validity periods mandates a high degree of automated certificate renewal to prevent service disruptions, driving demand for platforms that offer crypto-agility. Effective solutions now provide centralized policy enforcement, moving beyond simple credential management to offer true identity-based segmentation, which is critical for implementing least privilege access principles in complex, distributed systems.

We can help! Our analysts can customize this machine identity management market research report to meet your requirements.

RIA -

RIA -