Minimally Invasive Surgical Instruments Market Size 2025-2029

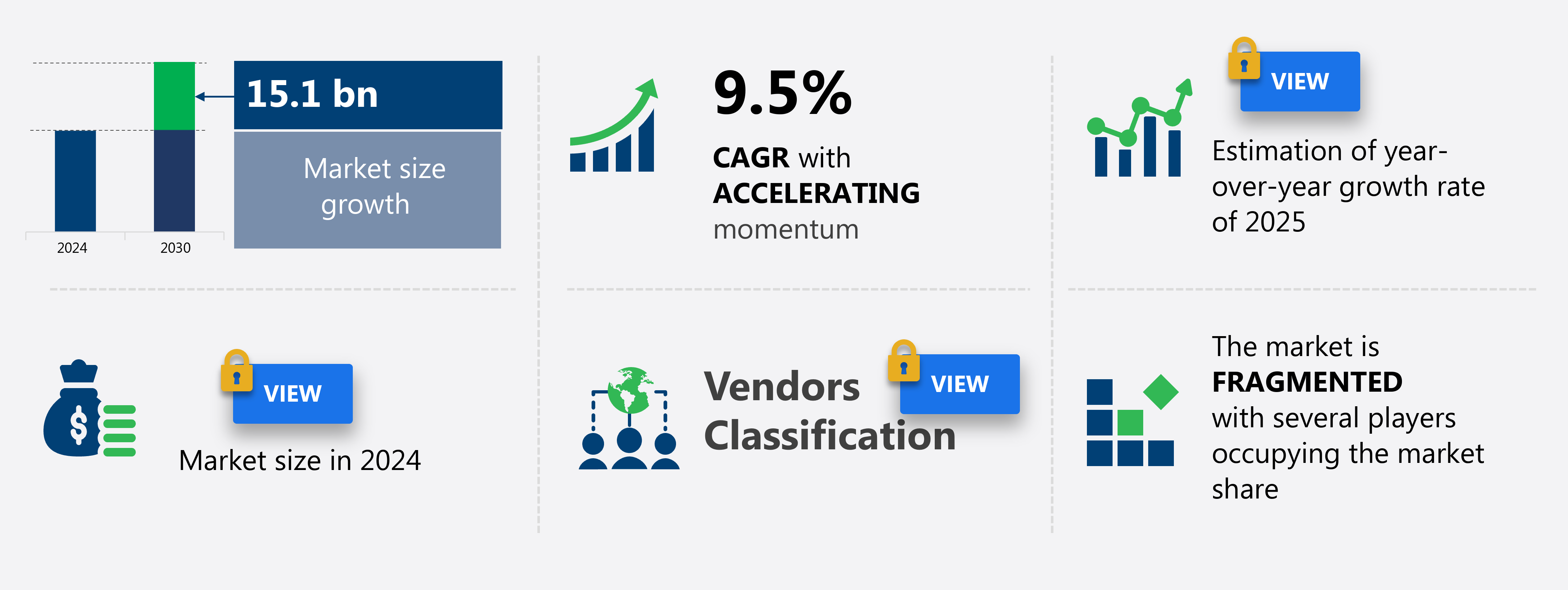

The minimally invasive surgical instruments market is forecasted to grow significantly, reaching approximately USD 49.6 billion by 2029, exhibiting a CAGR of 9.5% during the forecast period. This growth reflects increasing demand for less invasive surgical options and technological advancements.

The global minimally invasive surgical instruments market is primarily driven by the benefits of MIS procedures, including reduced patient trauma, lower infection risks, and quicker recovery times, leading to reduced healthcare expenditures. The increasing acceptance of surgical robots and their integration into minimally invasive surgeries further fuels market expansion. Growing product approvals and new product launches by key market players also create robust opportunities for market growth. As the geriatric population increases and chronic diseases become more prevalent, the demand for minimally invasive surgeries is expected to rise significantly. The market is witnessing continuous innovation, particularly in cardiac, orthopedic, ophthalmic, neurological, and oral surgical procedures, enhancing surgical precision and patient safety. The introduction of novel MIS products is enabling complex procedures previously deemed unsuitable for minimally invasive techniques.

To access the full market forecast and comprehensive analysis, Buy Now

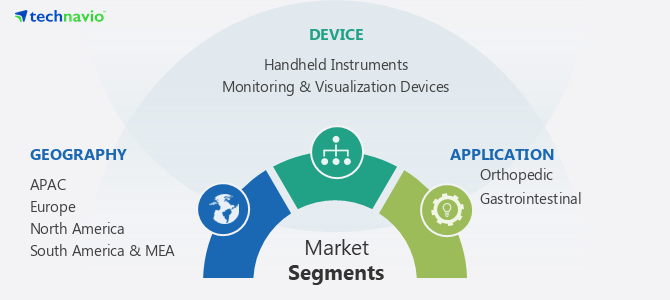

How is this market segmented?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in USD bn for the period 2025-2030, as well as historical data from 2019-2024 for the following segments:

- Device

- Handheld Instruments

- Monitoring & Visualization Devices

- Application

- Orthopedic

- Gastrointestinal

- End-use

- Hospitals & Clinics

- Ambulatory Surgical Centers

- APAC

- China

- India

- Japan

- Australia

- Rest of APAC

- Germany

- Spain

- Italy

- UK

- Rest of Europe

- US

- Canada

- Brazil

- UAE

- South Africa

- Others

- Device

- Handheld Instruments: The handheld instruments segment is expected to maintain a significant market share due to their essential role in surgical procedures and continuous innovation.

- Monitoring & Visualization Devices: The monitoring & visualization devices segment is anticipated to experience robust growth, driven by technological advancements in imaging and real-time surgical guidance.

- End-use

- Hospitals & Clinics: The hospitals & clinics segment is projected to retaIn the largest market share, due to the high volume of surgical procedures performed In these settings and the availability of advanced medical facilities.

- Ambulatory Surgical Centers: The ambulatory surgical centers segment is expected to witness the fastest growth rate, driven by the increasing preference for outpatient surgical procedures and favorable reimbursement policies.

- Application

- Orthopedic: The orthopedic segment is expected to remain a major application area, driven by the rising prevalence of orthopedic disorders and the increasing adoption of minimally invasive techniques for joint replacement and other procedures.

- Gastrointestinal: The gastrointestinal segment is anticipated to grow substantially, fueled by the increasing incidence of gastrointestinal cancers and the demand for less invasive diagnostic and therapeutic interventions.

Regional Analysis

- APAC: The Asia Pacific region is expected to exhibit the highest CAGR due to improving healthcare infrastructure, increasing government initiatives, and economic development in countries like India and China. The presence of a large population pool with low per capita income drives demand for affordable treatment options.

- Europe: Europe is a major market for minimally invasive surgical instruments, driven by well-established healthcare infrastructure and favorable reimbursement policies. Germany and the UK are key contributors to regional growth, with high adoption rates of advanced surgical technologies.

- North America: North America dominates the market due to the presence of well-established healthcare infrastructure, favorable government reimbursement policies, and high prevalence of chronic diseases. The U.S. and Canada lead the region in terms of market size and technological advancements.

- South America & MEA: The South America and MEA regions offer significant growth opportunities, driven by increasing investments in healthcare infrastructure and rising demand for advanced surgical procedures. Brazil and the UAE are emerging as key markets In these regions, with growing adoption of minimally invasive surgical techniques.

Market Dynamics

Our minimally invasive surgical instruments market researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of minimally invasive surgical instruments market?

Benefits of MIS procedures, including reduced patient trauma and quicker recovery times, drive market growth. Minimally invasive surgical (MIS) procedures offer several advantages over traditional open surgery, including minimized patient trauma & discomfort, lower risk of infection, and quicker procedure & recuperation periods, which usually result in reduced healthcare expenditures. The necessity to undertake highly skilled activities utilizing specialized tools with limited visibility along with ranges of motion, on the other hand, introduced higher levels of experience for the surgical team.

What are the market trends shaping the minimally invasive surgical instruments market?

Technological advancements in MIS instruments, such as surgical robots, enhance surgical precision and patient safety. The market is constantly transforming based on innovative advancements, especially In the fields of cardiac, orthopedic, ophthalmic, neurological, and oral surgical procedures. Improved product designs offer accuracy and level of control In the operating room. The introduction of novel MIS products is anticipated to boost market growth, allowing complex procedures to be performed which were earlier considered unsuitable for minimally invasive techniques.

What challenges does the minimally invasive surgical instruments market face?

The need for highly skilled surgical teams and the high cost of advanced equipment pose challenges to market growth. The high cost of MIS equipment, including endoscopic cameras, visualization scanners, nonmagnetic monitoring, specialized devices & catheters, contrast injectors, and pricey robotic systems, poses a significant challenge for healthcare providers, especially in developing countries. This factor can limit the adoption of MIS techniques and restrict market growth.

Key Companies & Market Insights

Leading companies are implementing strategies such as product innovations, acquisitions, and geographic expansions to enhance their market position. Key players In the minimally invasive surgical instruments marketinclude:

- Medtronic

- Siemens Healthineer AG

- Ethicon, Inc. (Johnson & Johnson)

- Depuy Synthes

- GE Healthcare

- Abbott Laboratories

- Intutive Surgical, Inc.

- Nuvasive, Inc.

- Zimmer Biomet

These companies are strategically focused on product development, market expansion, and partnerships to maintaIn their competitive edge In the growing minimally invasive surgical instruments market.

|

Market Scope |

|

|

Report Coverage |

Details |

| Base year | 2024 |

| Page number | 195 |

| Key countries | U.S., Canada, Germany, UK, France, Italy, Spain, China, Japan, India, Australia |

| Forecast period | 2025-2029 |

| Historic period | 2019-2023 |

| Report coverage | Market size, forecasts, segmentation |

| Regional Analysis | APAC

|

| Growth momentum and CAGR | 9.5% |

| Performing market contribution | Europe, APAC, North America |

RIA -

RIA -