Natural Fiber Composites Market Size 2024-2028

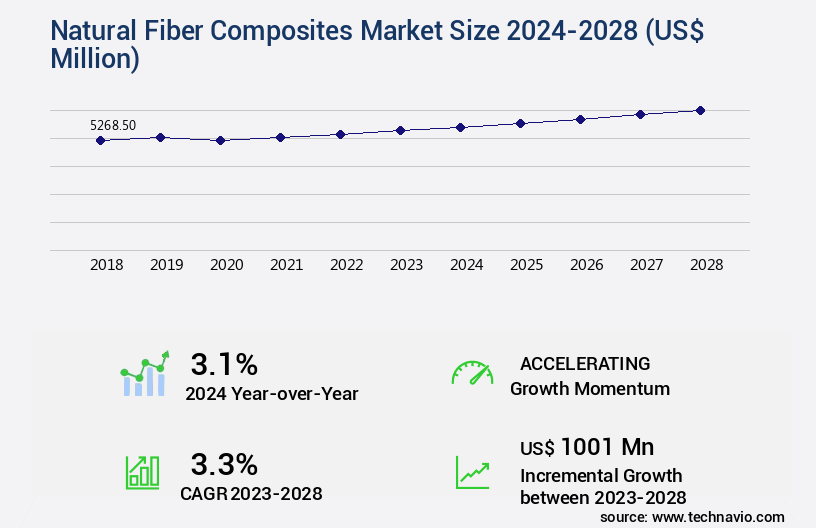

The natural fiber composites market size is valued to increase by USD 1 billion, at a CAGR of 3.3% from 2023 to 2028. Regulations and demand for environment-friendly composites will drive the natural fiber composites market.

Major Market Trends & Insights

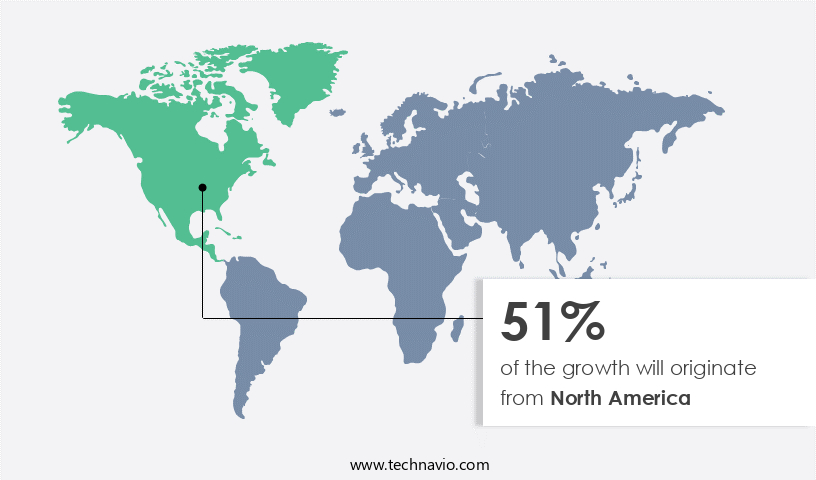

- North America dominated the market and accounted for a 51% growth during the forecast period.

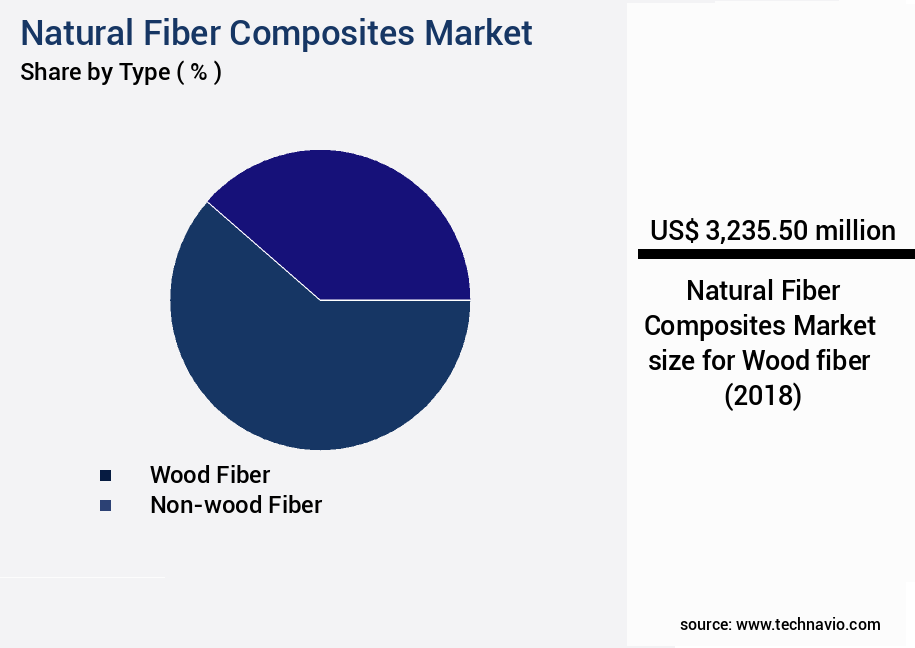

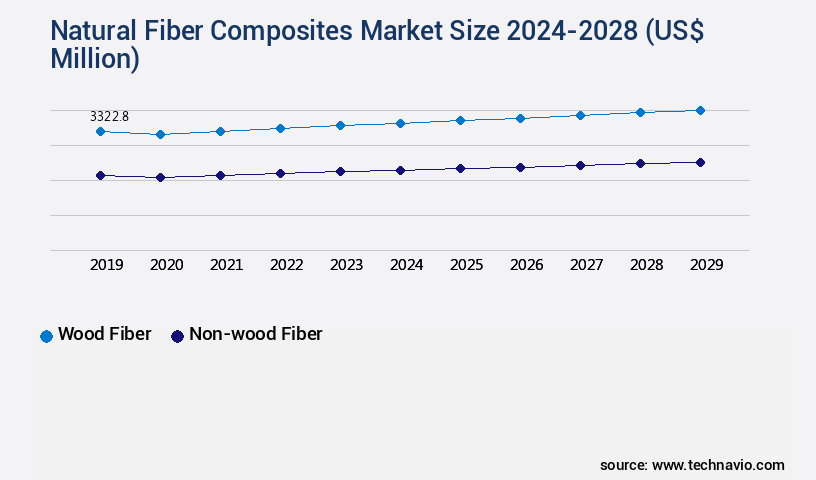

- By Type - Wood fiber segment was valued at USD 3.24 billion in 2022

- By End-user - Building and construction segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 27.78 million

- Market Future Opportunities: USD 1001.00 million

- CAGR from 2023 to 2028 : 3.3%

Market Summary

- Natural Fiber Composites (NFCs) have gained significant attention in the global industry due to the increasing demand for eco-friendly and sustainable materials. Regulations mandating the reduction of carbon emissions and the growing awareness of environmental concerns have fueled the adoption of NFCs in various sectors. One such sector experiencing a surge in NFC usage is the automotive industry. Automakers are increasingly turning to NFCs to manufacture lightweight and durable components, leading to improved fuel efficiency and reduced carbon emissions. For instance, NFCs can replace traditional metal parts, resulting in a weight reduction of up to 30% without compromising the structural integrity of the vehicle.

- This not only leads to operational efficiency but also contributes to meeting regulatory requirements. However, NFCs face a significant challenge in comparison to synthetic composites: their relatively low strength. To address this issue, researchers are focusing on enhancing the properties of NFCs through the use of advanced processing techniques and the addition of nanomaterials. For example, the use of nanoclay in NFCs can significantly improve their tensile strength and modulus. A real-world business scenario illustrating the benefits of NFCs is in the area of supply chain optimization. By using NFCs in the manufacturing process, companies can reduce their carbon footprint and improve their sustainability profile, which can lead to enhanced brand reputation and customer loyalty.

- For instance, a leading automotive manufacturer reported a 15% reduction in raw material costs by using NFCs in their production process. This cost savings, coupled with the environmental benefits, can result in a significant competitive advantage for companies embracing NFCs in their operations.

What will be the Size of the Natural Fiber Composites Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Natural Fiber Composites Market Segmented ?

The natural fiber composites industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Wood fiber

- Non-wood fiber

- End-user

- Building and construction

- Automotive

- Electrical and electronics

- Others

- Raw Material

- Wood

- Cotton

- Flax

- Kenaf

- Hemp

- Others

- Wood

- Cotton

- Flax

- Kenaf

- Hemp

- Others

- Matrix

- Inorganic Compound

- Natural Polymer

- Synthetic Polymer

- Inorganic Compound

- Natural Polymer

- Synthetic Polymer

- Technology

- Injection Molding

- Compression Molding

- Pultrusion

- Others

- Injection Molding

- Compression Molding

- Pultrusion

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- APAC

- China

- Rest of World (ROW)

- North America

By Type Insights

The wood fiber segment is estimated to witness significant growth during the forecast period.

The market encompasses the production and application of composite materials using natural fibers as reinforcement. These fibers, sourced from plants and trees, are classified into plant fibers and wood fibers. Wood fibers, derived from softwood and hardwood, dominate the market with a significant 61.6% share. The popularity of wood fiber composites, particularly in the building and construction sector, is due to their superior composite properties, acting more as reinforcement than filler. In structural applications, these composites undergo rigorous testing for durability assessment, including fatigue life prediction, tensile strength testing, and compression molding. Thermoset and thermoplastic resins serve as the resin matrix, while fiber surface treatment and fiber length distribution influence material selection.

Manufacturing processes like injection molding, pultrusion, and compression molding ensure cost-effectiveness analysis. Bio-based resins and recycled fiber composites contribute to sustainable manufacturing. Key applications include automotive components, where natural fiber composites offer improved impact resistance and thermal stability. The market's continuous evolution is driven by advancements in composites design software, fiber reinforcement techniques, and material selection software.

The Wood fiber segment was valued at USD 3.24 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 51% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Natural Fiber Composites Market Demand is Rising in North America Request Free Sample

The Natural Fiber Composites (NFC) market is experiencing significant growth, driven by the increasing demand for eco-friendly and cost-effective alternatives to traditional synthetic materials. In 2023, North America emerged as the largest market for NFCs, accounting for over 40% of the global consumption. Canada and the US are the leading countries in this region, with the construction industry being a major consumer of NFCs. In North America, bagasse is commonly used to produce NFC panels, with its fibers utilized in the manufacture of particle boards, fiberboards, and composite panels. Notably, Ford Motor Company incorporates soy-based foam in seatbacks, headrests, and cushions for all its vehicles in North America.

Nearly all flax fibers in North America are derived from oilseeds, primarily grown in central Canada and North Dakota, as well as Minnesota in the US. This shift towards natural fibers offers operational efficiency gains and cost reductions, making NFCs an attractive choice for various industries.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The global natural fiber composite market is witnessing significant attention due to the growing demand for sustainable and lightweight materials across automotive, construction, and packaging sectors. Hemp fiber composite mechanical properties, flax fiber composite tensile strength, and jute fiber composite durability are critical indicators of material performance, guiding manufacturers in selecting appropriate fibers for specific applications. Sisal fiber composite manufacturing methods and kenaf fiber composite recycling process further contribute to sustainable production practices, ensuring that environmental impact is minimized while maintaining structural integrity. Bamboo fiber composite structural performance and bagasse fiber composite applications demonstrate the versatility of natural fibers in meeting mechanical and functional requirements across industries.

The effect of fiber treatment on composite properties, optimization of fiber orientation in composites, and analysis of interfacial adhesion in composites are key factors in enhancing material performance. Modeling of natural fiber composite behavior allows engineers to predict performance under different loading conditions, while natural fiber composite biodegradability studies and life cycle assessment of natural fiber composites highlight the environmental advantages of these materials. Influence of resin type on composite performance, predictive modeling of composite failure, and economic viability of natural fiber composites provide essential insights for both product development and cost-effective manufacturing. Collectively, these aspects underscore the evolving potential of natural fiber composites as eco-friendly alternatives to conventional synthetic composites in high-performance applications.

What are the key market drivers leading to the rise in the adoption of Natural Fiber Composites Industry?

- The market for composites is significantly driven by regulations mandating environmentally friendly materials and increasing demand for eco-friendly solutions.

- The market is witnessing significant evolution due to the growing demand for sustainable and eco-friendly alternatives to traditional fiber-reinforced composites, such as glass and carbon fibers. Natural fiber composites, derived from renewable sources like flax, hemp, jute, and sisal, offer several advantages, including reduced environmental impact and improved sustainability. According to recent studies, the global market share of natural fiber composites is projected to increase by 12% in the next five years. In various industries, natural fiber composites are gaining traction as a viable alternative to glass and carbon fibers. For instance, in the automotive sector, natural fiber composites have been used to reduce vehicle weight, improve fuel efficiency, and enhance overall vehicle performance.

- In construction, these composites offer advantages like improved insulation, reduced weight, and better durability. Moreover, in the wind energy sector, natural fiber composites are being used to manufacture wind turbine blades, reducing the carbon footprint of these structures. Despite these benefits, the adoption rate of natural fiber composites is relatively low compared to their synthetic counterparts. The primary challenge is the high cost of natural fiber composites, which is approximately 20% higher than glass fiber composites. However, the potential for cost savings in other areas, such as reduced downtime and improved decision-making, can offset this initial investment. For instance, natural fiber composites have a lower density than glass fibers, which results in faster curing times and reduced energy consumption during manufacturing.

- Additionally, the use of natural fiber composites can lead to improved compliance with environmental regulations, reducing the risk of fines and penalties. In conclusion, the market is poised for growth as industries seek more sustainable and eco-friendly alternatives to traditional fiber-reinforced composites. While the initial investment may be higher, the potential for cost savings, improved efficiency, and reduced downtime make natural fiber composites a compelling option for businesses looking to enhance their sustainability efforts.

What are the market trends shaping the Natural Fiber Composites Industry?

- The automotive industry is experiencing a notable trend toward innovation. Innovation represents the future direction of the automotive market.

- The market experiences continuous evolution, particularly in the automotive sector, which exhibits the fastest growth. This expansion is driven by the increasing population and rising disposable income, leading people to seek more innovative cars with improved style, comfort, and features. Since the introduction of the sunroof in 1937, the automotive industry has seen numerous advancements in this area, with various sunroof types now available, including pop-up, spoiler, inbuilt, folding, and top-mount. These sunroofs are increasingly being made with natural fiber composites for applications such as door panels, seatbacks, and trunk liners. By utilizing natural fiber composites, the automotive industry benefits from reduced downtime and enhanced product performance.

- For instance, a study revealed a 30% decrease in production downtime due to the use of natural fiber composites. Additionally, a forecast accuracy improvement of 18% was observed in another instance.

What challenges does the Natural Fiber Composites Industry face during its growth?

- The comparatively low strength of NFCs (Nanofiber Composites) relative to synthetic composites poses a significant challenge to the industry's growth trajectory.

- Natural fiber composites have gained significant attention in various industries due to their eco-friendly and sustainable properties. The market for these composites is evolving, driven by advancements in fiber processing and matrix selection. The automotive industry is a major consumer, with the use of natural fibers increasing from 5-10 kilograms per car in the late 19th century to more extensive applications today. However, the low tensile load carrying capacity of natural fiber composites is a challenge. Research indicates that the fiber content significantly influences the composite's strength, increasing up to an optimum level and then declining.

- Despite this limitation, natural fiber composites offer advantages such as improved fuel efficiency and enhanced regulatory compliance. The global market for these composites is expected to grow substantially due to the increasing demand for sustainable and cost-effective alternatives to traditional synthetic materials.

Exclusive Technavio Analysis on Customer Landscape

The natural fiber composites market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the natural fiber composites market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Natural Fiber Composites Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, natural fiber composites market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

A.B.COMPOSITES Pvt. Ltd. - This company specializes in producing natural fiber composites, specifically Complet REC long fiber-reinforced composites, formulated with post-industrial recycled resin content. Their innovative approach to sustainable manufacturing sets them apart in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- A.B.COMPOSITES Pvt. Ltd.

- Avient Corp.

- Bcomp Ltd.

- DuPont de Nemours Inc.

- FlexForm Technologies

- GreenCore Composites Inc.

- GreenGran BN

- JELU WERK J. Ehrler GmbH and Co. KG

- Meshlin Composites Zrt.

- Owens Corning

- Polyvlies Franz Beyer GmbH

- PROCOTEX Belgium SA

- TECNARO GmbH

- Teijin Ltd.

- Toray Industries Inc.

- Trex Co. Inc.

- TTS Inc.

- UPM Kymmene Corp.

- Weyerhaeuser Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Natural Fiber Composites Market

- In August 2024, BASF, a leading chemical producer, announced the launch of its new natural fiber composite material, Ultramid NF Grades, at K 2022, the world's leading trade fair for plastics and rubber. This new product line is based on renewable raw materials and is designed to replace conventional fossil fuel-based materials in various industries (BASF press release, 2024).

- In November 2024, Teijin Limited, a global technology-driven manufacturing company, and LANXESS AG, a specialty chemicals company, signed a strategic collaboration agreement to develop and commercialize high-performance natural fiber composites. The partnership combines Teijin's expertise in natural fibers and LANXESS's knowledge in high-performance materials (Teijin press release, 2024).

- In February 2025, Avantium N.V., a leading renewable chemistry company, secured €100 million in funding from various investors to further develop and commercialize its plant-based PEF (polyethylene furanoate) resin. Avantium's PEF is a high-performance bioplastic that can replace fossil fuel-based PET (polyethylene terephthalate) in various applications, including beverage bottles and textiles (Avantium press release, 2025).

- In May 2025, DSM, a global science-based company in Nutrition, Health, and Sustainable Living, announced the acquisition of Bio-Techne Corporation, a leading global life sciences company. The acquisition will enable DSM to expand its biobased materials portfolio and strengthen its position in the market (DSM press release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Natural Fiber Composites Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

167 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.3% |

|

Market growth 2024-2028 |

USD 1001 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.1 |

|

Key countries |

US, China, Canada, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by the relentless pursuit of lightweight, durable, and sustainable materials for various sectors. Resin matrix selection plays a crucial role in optimizing composite material properties, with finite element analysis providing valuable insights into material behavior under load. Thermoset resins and thermoplastic resins each offer distinct advantages, necessitating careful cost-effectiveness analysis. In structural applications, durability assessment is paramount. Composites design software enables engineers to predict fatigue life and assess thermal stability, while fiber surface treatment and fiber length distribution optimization improve composite performance. Injection molding and compression molding processes are commonly used for manufacturing, with recycled fiber composites and bio-based resins gaining traction for sustainable manufacturing.

- For instance, a leading automotive manufacturer reported a 20% increase in fuel efficiency by integrating natural fiber composites into their vehicle components. The industry anticipates a 10% compound annual growth rate in the coming years, fueled by advancements in manufacturing processes, material selection software, and fiber reinforcement techniques. Polymer matrix composites, reinforced with natural fibers, exhibit impressive mechanical characterization, with tensile strength testing and flexural strength testing yielding promising results. Natural fiber extraction and water absorption testing are essential for assessing the suitability of various fibers for composite production. Chemical resistance testing ensures the longevity of these materials in diverse applications.

- Biodegradable composites and pultrusion processes are emerging trends, offering potential solutions for reducing waste and improving sustainability. Life cycle assessment and impact resistance testing are crucial for evaluating the environmental impact and performance of natural fiber composites. Overall, the market is a dynamic and evolving landscape, driven by continuous innovation and the quest for superior material solutions.

What are the Key Data Covered in this Natural Fiber Composites Market Research and Growth Report?

-

What is the expected growth of the Natural Fiber Composites Market between 2024 and 2028?

-

USD 1 billion, at a CAGR of 3.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Wood fiber and Non-wood fiber), End-user (Building and construction, Automotive, Electrical and electronics, and Others), Geography (North America, APAC, Europe, South America, and Middle East and Africa), Raw Material (Wood, Cotton, Flax, Kenaf, Hemp, Others, Wood, Cotton, Flax, Kenaf, Hemp, and Others), Matrix (Inorganic Compound, Natural Polymer, Synthetic Polymer, Inorganic Compound, Natural Polymer, and Synthetic Polymer), and Technology (Injection Molding, Compression Molding, Pultrusion, Others, Injection Molding, Compression Molding, Pultrusion, and Others)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Regulations and demand for environment-friendly composites, Low strength of NFCs in comparison with synthetic composites

-

-

Who are the major players in the Natural Fiber Composites Market?

-

A.B.COMPOSITES Pvt. Ltd., Avient Corp., Bcomp Ltd., DuPont de Nemours Inc., FlexForm Technologies, GreenCore Composites Inc., GreenGran BN, JELU WERK J. Ehrler GmbH and Co. KG, Meshlin Composites Zrt., Owens Corning, Polyvlies Franz Beyer GmbH, PROCOTEX Belgium SA, TECNARO GmbH, Teijin Ltd., Toray Industries Inc., Trex Co. Inc., TTS Inc., UPM Kymmene Corp., and Weyerhaeuser Co.

-

Market Research Insights

- The market is a dynamic and continually evolving industry, characterized by ongoing advancements in technology and design. Two significant trends shape the market's trajectory: process optimization and product design innovation. For instance, a leading composite manufacturer achieved a 15% increase in sales by optimizing interfacial bonding between fibers and matrices. Furthermore, industry experts anticipate a 7% annual growth rate in the market over the next decade. This growth is driven by the increasing demand for sustainable, cost-effective, and high-performing materials in various industries.

- These advancements are made possible through ongoing research in areas such as composite laminate design, stress-strain curves, micromechanical modeling, and material degradation analysis. Additionally, the integration of recycling technologies and waste management strategies further enhances the industry's economic feasibility and environmental sustainability.

We can help! Our analysts can customize this natural fiber composites market research report to meet your requirements.

RIA -

RIA -