Payment Orchestration Platform Market Size 2026-2030

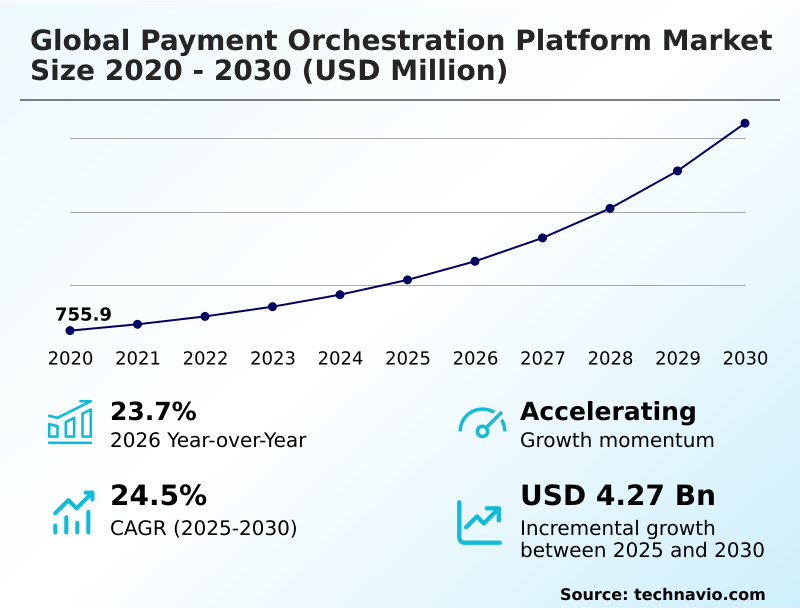

The payment orchestration platform market size is valued to increase by USD 4.27 billion, at a CAGR of 24.5% from 2025 to 2030. Demand for cross-border interoperability and unified global settlement will drive the payment orchestration platform market.

Major Market Trends & Insights

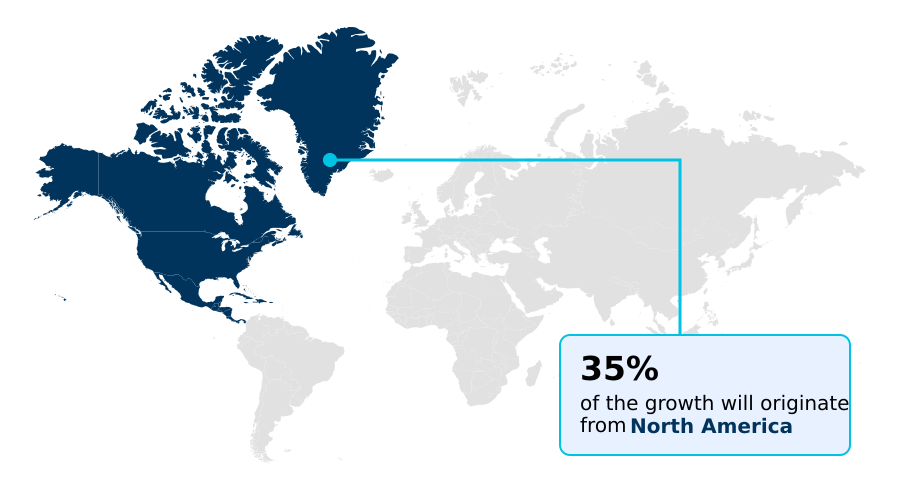

- North America dominated the market and accounted for a 35.2% growth during the forecast period.

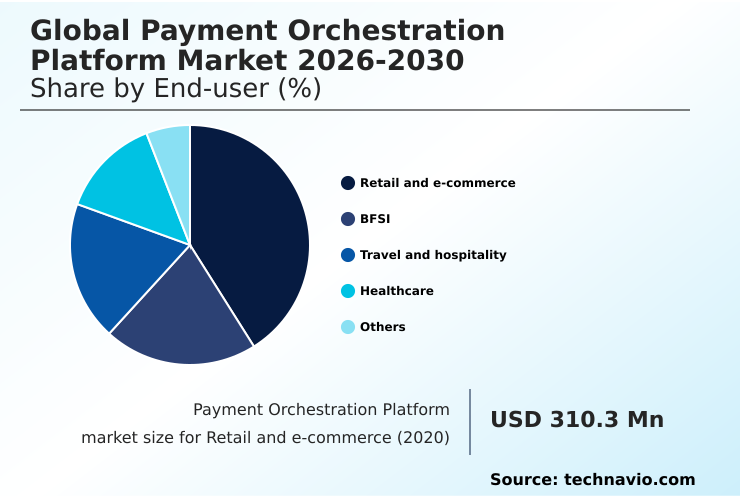

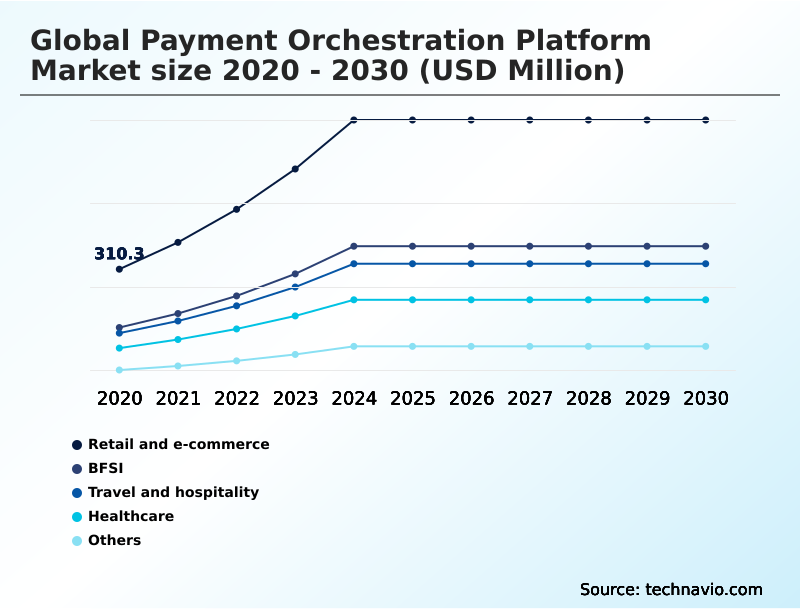

- By End-user - Retail and e-commerce segment was valued at USD 703.5 million in 2024

- By Deployment - Cloud based segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 5.66 billion

- Market Future Opportunities: USD 4.27 billion

- CAGR from 2025 to 2030 : 24.5%

Market Summary

- The payment orchestration platform market is defined by its role as a sophisticated middleware layer designed to simplify the complexities of modern digital commerce. For enterprises, the primary driver is the need to manage a fragmented global payment landscape, requiring cross-border interoperability to connect with numerous acquiring banks and local payment methods (LPMs) through a single API integration.

- A significant trend is the evolution of these platforms from simple transaction routers to comprehensive hubs for transaction lifecycle management, incorporating advanced capabilities like chargeback automation and payout orchestration. For instance, a global subscription service utilizes an orchestration platform's smart retries and support for diverse payment flows to reduce involuntary churn, directly enhancing customer retention.

- However, the market faces challenges from the erosion of vendor neutrality as major payment processors introduce their own orchestration services. This dynamic forces businesses to weigh the convenience of an integrated solution against the benefits of an agnostic platform that ensures operational resilience and optimizes cost structures across multiple providers.

What will be the Size of the Payment Orchestration Platform Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Payment Orchestration Platform Market Segmented?

The payment orchestration platform industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Retail and e-commerce

- BFSI

- Travel and hospitality

- Healthcare

- Others

- Deployment

- Cloud based

- On-Premises

- Application

- Cross border transactions

- Risk management

- Advanced analytics and reporting

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By End-user Insights

The retail and e-commerce segment is estimated to witness significant growth during the forecast period.

The retail and e-commerce segment leads in adoption, driven by the critical need for revenue optimization and a seamless user experience.

Merchants leverage platforms to enhance the checkout experience, using intelligent routing and smart retries for authorization rate maximization, which can improve success rates by over 5%.

These systems provide essential multi-acquirer support, enabling businesses to navigate backend processing complexities and maintain transaction resiliency. By supporting diverse local payment methods (LPMs), orchestration of payment flows becomes a cornerstone for international expansion, directly impacting customer retention.

This strategic approach to payment processing is vital for managing global operations, reducing revenue leakage, and sustaining a competitive edge in a crowded digital marketplace, ensuring a positive return on investment.

The Retail and e-commerce segment was valued at USD 703.5 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Payment Orchestration Platform Market Demand is Rising in North America Get Free Sample

The geographic landscape is characterized by distinct regional dynamics. In North America, mature markets focus on cost structure optimization and treasury and liquidity services, with multi-processor strategies boosting authorization rates by 3-5%.

In contrast, APAC is defined by its fragmented ecosystem, where local payment methods account for over 60% of digital transactions, making payout orchestration and dynamic currency conversion essential for managing payment flows.

Latin America is undergoing significant ecosystem consolidation, simplifying cross-border settlement for merchants entering the region. Meanwhile, the Middle East and Africa are leveraging omnichannel payments for high-growth sectors like travel and retail.

Across all regions, platforms enabling a unified commerce experience are gaining traction, addressing the universal need to reduce technical debt and streamline compliance management.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Deciding between a traditional payment gateway vs orchestration platform is a critical inflection point for modern enterprises. While some consider the cost of building in-house orchestration, the complexity and ongoing maintenance favor specialized third-party solutions. The primary benefit lies in improving authorization rates with smart routing, which intelligently directs transactions to the best-fit processor in real-time.

- This capability is crucial for reducing involuntary subscription churn in recurring revenue models. Furthermore, a key strategy involves the seamless integration of diverse payment options, such as integrating BNPL into checkout flows to meet consumer demand without adding technical debt.

- Beyond initial acceptance, these platforms are instrumental in automating chargeback dispute resolution, a process that can reduce associated operational overhead by more than 60% compared to manual methods. For global businesses, a local payment method integration strategy is non-negotiable for market penetration. Advanced platforms also address the complexities of orchestrating cross-border marketplace payouts and managing foreign exchange in payment flows.

- Foundational to this is ensuring PCI compliance with tokenization, which secures customer data while providing the flexibility needed for managing multi-processor payment routing. The move toward achieving ISO 20022 message compliance is also simplified, alongside centralizing multi-country payment reconciliation.

What are the key market drivers leading to the rise in the adoption of Payment Orchestration Platform Industry?

- The primary market driver is the growing demand for cross-border interoperability, which enables unified global settlement and streamlined payment management across disparate regions.

- The market is primarily driven by the enterprise need for cross-border interoperability and a unified approach to managing payment stack fragmentation. Businesses are adopting these platforms to reduce cross-border transaction fees by an average of 15% through intelligent routing.

- The increasing demand for vertical-specific payment logic, particularly in travel, requires support for complex processes like split payments and the handling of Level 2 and Level 3 data, which specialized platforms deliver with over 99% settlement accuracy.

- Furthermore, the relentless pursuit of cost structure optimization and operational resilience compels merchants to adopt a multi-processor strategy. This is facilitated by on-premises deployment or cloud-based SaaS architecture, allowing for dynamic management of acquiring banks and significant technical debt reduction.

What are the market trends shaping the Payment Orchestration Platform Industry?

- A key market trend is the convergence of traditional payment processing and dedicated orchestration layers. This blurs the lines between financial settlement services and neutral routing technology.

- Key trends are reshaping the market, led by the evolution toward comprehensive transaction lifecycle management. Platforms are integrating advanced AI and open banking connectivity to move beyond simple routing. AI-driven models now deliver a 3-5% uplift in authorization rates compared to static rules.

- Another major shift is the focus on back-office automation, where automated data normalization and reconciliation capabilities can reduce manual workloads by over 40%. The convergence of payment gateway functions with agnostic middleware is creating hybrid systems that handle both routing and settlement.

- This trend supports complex financial products like BNPL integration and simplifies the management of the entire payment stack, providing enterprises with a single source of truth for all transaction data.

What challenges does the Payment Orchestration Platform Industry face during its growth?

- A key challenge affecting industry growth is the erosion of vendor neutrality, coupled with the increasing commoditization of the core orchestration layer by large ecosystem players.

- The market faces significant challenges, including the erosion of vendor neutrality as major financial technology firms bundle their own orchestration features. This dynamic complicates the goal of achieving a truly agnostic middleware solution. The operational instability caused by constant industry consolidation is another major issue, with company divestitures impacting an estimated 20% of enterprise merchants' backend processing setups.

- Furthermore, escalating technical complexity around post-transaction processes creates hurdles. The necessity for ISO 20022 compliance, advanced dispute management, and adherence to data sovereignty regulations can increase platform implementation timelines by up to 25%, demanding deeper expertise in financial messaging and compliance management from vendors.

Exclusive Technavio Analysis on Customer Landscape

The payment orchestration platform market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the payment orchestration platform market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Payment Orchestration Platform Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, payment orchestration platform market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ACI Worldwide Inc. - Core offerings provide a unified middleware layer, enabling intelligent routing, multi-acquirer support, and centralized fraud management through a single API integration for global payment processing.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ACI Worldwide Inc.

- Adyen NV

- APEXX Fintech Ltd.

- BlueSnap Inc.

- Bridger AI Ltd.

- CellPoint Digital

- Checkout Ltd.

- Corefy

- Gr4vy Inc.

- IXOPAY GmbH

- ModoPayments LLC

- Payoneer Global Inc.

- PayPal Holdings Inc.

- PayU

- Rapyd Financial Ltd.

- Rebilly Inc.

- Spreedly Inc.

- Stripe Inc.

- Worldline SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Payment orchestration platform market

- In March, 2025, Rapyd completed its acquisition of PayU's Global Payment Organisation (GPO) assets, significantly expanding its payment network and acquiring capabilities across Latin America and Africa.

- In April, 2025, CellPoint Digital and Checkout.com entered a strategic partnership to provide a combined solution for travel merchants, integrating advanced routing technology with a high-performance global acquiring network.

- In April, 2025, eBay announced a partnership with Checkout.com, leveraging the latter as a primary global payment partner to help optimize authorization rates and transaction performance for its marketplace.

- In May, 2025, Stripe launched Stripe Orchestration, a new offering that allows enterprise users to route transactions to third-party payment processors directly from the Stripe platform, validating the multi-processor strategy.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Payment Orchestration Platform Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 24.5% |

| Market growth 2026-2030 | USD 4272.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 23.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, The Netherlands, Italy, Spain, China, India, Japan, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The payment orchestration platform market is centered on a sophisticated middleware layer, often built on a SaaS architecture, which provides a single API access point to a web of financial services. This API integration is fundamental to its value, enabling intelligent routing and multi-acquirer support for true unified commerce.

- Core capabilities include robust fraud management, secure tokenization, and card vaulting to ensure transaction resiliency. Platforms manage complex payment processing for everything from split payments and BNPL integration to omnichannel payments, while also handling payout orchestration.

- A key boardroom consideration is the technology's role in risk mitigation, particularly regarding ISO 20022 compliance and the handling of financial messaging, where platforms can reduce compliance-related errors by over 95%. Support for open banking connectivity and real-time payment rails is becoming standard.

- These systems offer features like smart retries, chargeback automation, and revenue recovery tools, all contributing to a more efficient and secure payment ecosystem that supports cross-border interoperability and diverse local payment methods (LPMs).

What are the Key Data Covered in this Payment Orchestration Platform Market Research and Growth Report?

-

What is the expected growth of the Payment Orchestration Platform Market between 2026 and 2030?

-

USD 4.27 billion, at a CAGR of 24.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Retail and e-commerce, BFSI, Travel and hospitality, Healthcare, and Others), Deployment (Cloud based, and On-premises), Application (Cross border transactions, Risk management, Advanced analytics and reporting, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Demand for cross-border interoperability and unified global settlement, Erosion of company neutrality and commoditization of orchestration layer

-

-

Who are the major players in the Payment Orchestration Platform Market?

-

ACI Worldwide Inc., Adyen NV, APEXX Fintech Ltd., BlueSnap Inc., Bridger AI Ltd., CellPoint Digital, Checkout Ltd., Corefy, Gr4vy Inc., IXOPAY GmbH, ModoPayments LLC, Payoneer Global Inc., PayPal Holdings Inc., PayU, Rapyd Financial Ltd., Rebilly Inc., Spreedly Inc., Stripe Inc. and Worldline SA

-

Market Research Insights

- Market dynamics are shifting payments from a cost center to a strategic tool for revenue optimization and enhanced customer retention. Enterprises navigate payment stack fragmentation by adopting a multi-processor strategy, which improves operational resilience against provider outages.

- This approach has been shown to boost authorization rate maximization by up to 5% while advanced back-office automation can reduce manual reconciliation costs by 40%. The emphasis is on achieving a seamless frontend customer experience decoupled from backend processing complexities. As ecosystem consolidation continues, maintaining vendor neutrality becomes critical for leveraging competitive transaction fees.

- Businesses now use orchestration to manage complex payment flows, ensure data normalization for a single source of truth, and support specialized vertical-specific payment logic, turning their payment infrastructure into a competitive advantage.

We can help! Our analysts can customize this payment orchestration platform market research report to meet your requirements.

RIA -

RIA -