Plasticizer Alcohols Market Size 2026-2030

The plasticizer alcohols market size is valued to increase by USD 5.65 billion, at a CAGR of 9.7% from 2025 to 2030. Rapid expansion of infrastructure and construction activities in emerging economies will drive the plasticizer alcohols market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 38.8% growth during the forecast period.

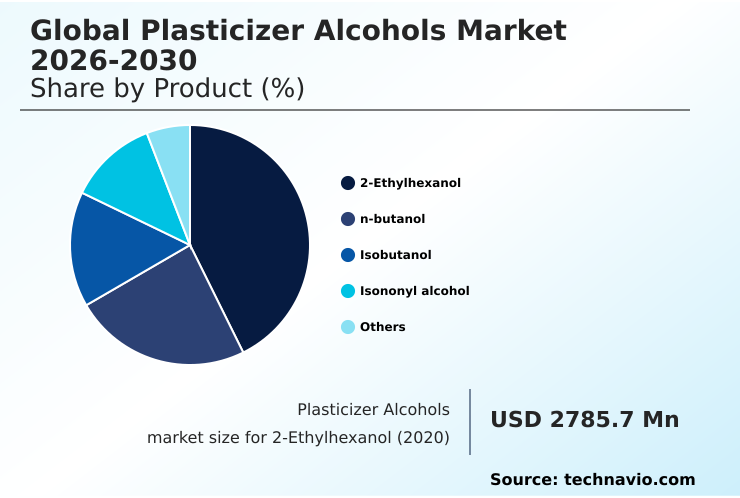

- By Product - 2-Ethylhexanol segment was valued at USD 3.83 billion in 2024

- By End-user - Automotive segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 8.72 billion

- Market Future Opportunities: USD 5.65 billion

- CAGR from 2025 to 2030 : 9.7%

Market Summary

- The plasticizer alcohols market is foundational to the performance of modern polymers, primarily serving to impart flexibility and durability. Demand is fundamentally tied to the health of the global construction and automotive sectors, which rely on plasticized materials for applications ranging from electrical insulation and flooring to vehicle interiors.

- A significant market driver involves the continuous infrastructure development in emerging economies, creating sustained consumption. Concurrently, the industry is navigating a pivotal trend toward sustainability, with a marked shift away from traditional chemicals to non-phthalate and bio-based alternatives. This transition is propelled by stringent international regulations and growing consumer awareness.

- However, this evolution introduces challenges; for instance, a chemical manufacturer aiming to align with new environmental standards must manage the operational complexities and costs of reformulating its product lines.

- This often involves significant investment in R&D and plant retrofitting to handle different feedstocks, all while contending with the inherent volatility of raw material pricing, which can impact profitability and supply chain stability.

What will be the Size of the Plasticizer Alcohols Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Plasticizer Alcohols Market Segmented?

The plasticizer alcohols industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- 2-Ethylhexanol

- n-butanol

- Isobutanol

- Isononyl alcohol

- Others

- End-user

- Automotive

- Construction

- Others

- Type

- PVC products

- Non-PVC products

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Product Insights

The 2-ethylhexanol segment is estimated to witness significant growth during the forecast period.

Market segmentation by product reveals a distinct shift toward high-performance solutions. While traditional alcohols remain prevalent, the demand for high-molecular-weight alcohols and specialty alcohols is increasing for applications requiring superior plasticizer performance characteristics.

Products derived from isononyl alcohol (INA) and 2-propylheptanol (2-PH) are instrumental in formulating low volatility plasticizers. These are essential for creating diisononyl phthalate (DINP) and dotyl terephthalate (DOTP). Such ester-based plasticizers offer enhanced polymer chain lubrication, reducing plasticizer migration.

This trend is driven by the need for materials like isodecyl alcohol (IDA) to produce diisodecyl phthalate (DIDP), which provides durability in demanding environments, with some formulations achieving a 25% reduction in material degradation over time.

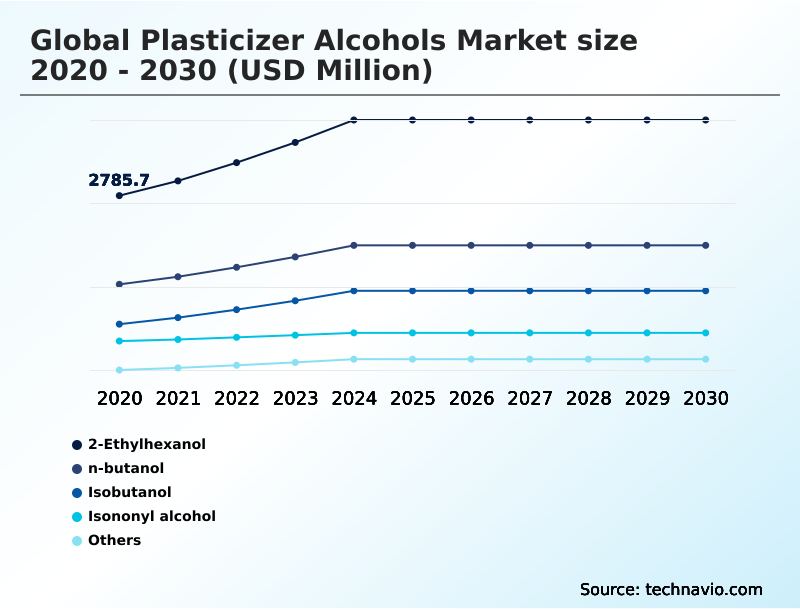

The 2-Ethylhexanol segment was valued at USD 3.83 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 38.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Plasticizer Alcohols Market Demand is Rising in APAC Get Free Sample

The geographic landscape is defined by a strategic buildup of regional production capacity, especially within integrated refinery complexes in APAC. These facilities leverage advanced oxo-process technology to convert petrochemical derivatives like propylene into essential oxo-alcohols.

The large-scale production of 2-ethylhexanol (2-EH) and n-butanol through hydroformylation and subsequent esterification supports both domestic demand and export activities. In contrast, North American and European markets focus on producing specialty chemical intermediates.

This geographical specialization impacts global trade, with APAC accounting for over 38% of incremental growth.

The establishment of new downstream petrochemical units in high-growth regions ensures a captive supply for industrial solvent applications and reduces reliance on imports, reshaping global supply chains for isobutanol and other key chemical intermediates.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Analyzing the global plasticizer alcohols market 2026-2030 competitive landscape reveals a strategic focus on navigating the impact of REACH on plasticizers and mitigating supply chain risk in petrochemicals. The global plasticizer alcohols market 2026-2030 key drivers are linked to plasticizer demand in emerging economies, especially the demand for DOTP in construction.

- A key discussion point is the 2-ethylhexanol vs isononyl alcohol debate, as companies weigh performance against cost. The global plasticizer alcohols market 2026-2030 emerging trends show a clear move toward sustainable alternatives to phthalate plasticizers and investment in bio-based alcohol production, highlighting the benefits of high molecular weight plasticizers.

- PVC compounding with specialty alcohols is becoming standard for high-end applications like plasticizer alcohols in automotive interiors. The global plasticizer alcohols market 2026-2030 segmentation analysis and regional outlook indicate that while the price volatility of propylene feedstock remains a challenge, the non-phthalate plasticizers market share is growing.

- This shift toward a circular economy for PVC plasticizers is a central theme, underscored by advancements in oxo-alcohol production process efficiency, where optimized catalyst use has improved yields by over 5% in certain facilities.

What are the key market drivers leading to the rise in the adoption of Plasticizer Alcohols Industry?

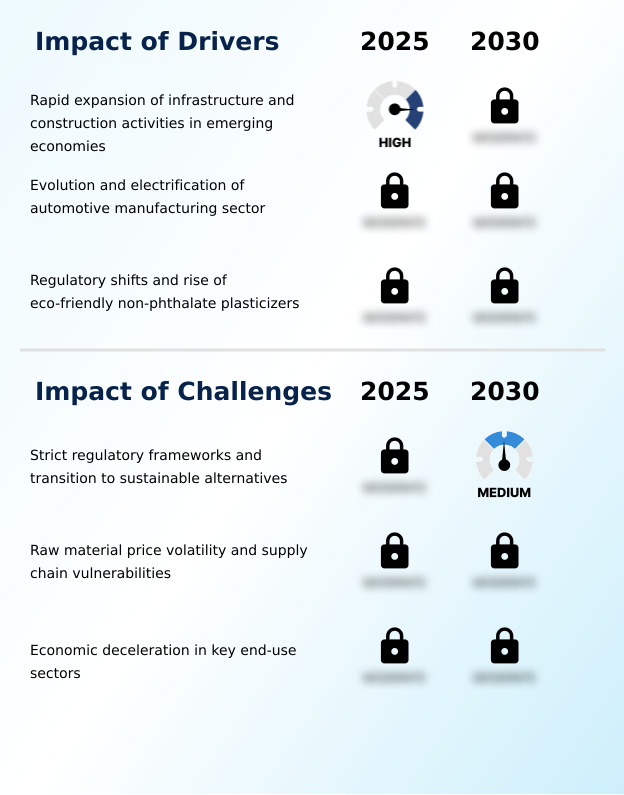

- The rapid expansion of infrastructure and construction activities in emerging economies is a primary driver for the market, fueling demand for plasticized PVC in building applications.

- Robust end-user industry demand is the primary market driver, particularly from sectors requiring high-performance polymers. In construction, demand for construction chemicals used in flexible PVC applications is strong, contributing to enhanced construction material durability.

- The automotive sector's focus on automotive lightweighting materials is fueling the need for advanced plasticizers for automotive interiors that offer low fogging characteristics and superior material property enhancement. This requires high-purity alcohols to ensure PVC flexibility enhancement without compromising safety.

- For specialized uses like wire and cable insulation, where performance is critical, demand for premium-grade polyvinyl chloride (PVC) is growing at a rate 10% faster than standard grades, underscoring the market's shift toward value-added solutions.

What are the market trends shaping the Plasticizer Alcohols Industry?

- A key trend is the accelerating transition toward bio-based and circular feedstocks for alcohol production. This shift is driven by sustainability mandates and the increasing demand for products with a lower carbon footprint.

- The market is undergoing a significant transformation toward sustainable plasticizer production, driven by stringent green chemistry principles. This trend involves the adoption of a mass balance approach to integrate bio-derived alcohol streams and promote circular feedstock integration. As a result, the availability of bio-based plasticizers and other eco-friendly plasticizer alternatives with a reduced product carbon footprint (PCF) is increasing.

- Producers are securing international sustainability and carbon certification (ISCC) for their non-phthalate plasticizers, including advanced citrate plasticizers and adipate plasticizers. These efforts in environmental impact reduction, which have led to a 20% decrease in emissions for certain product lines, are supported by emerging chemical recycling technologies and a more secure non-fossil feedstock supply chain, fundamentally altering the competitive landscape.

What challenges does the Plasticizer Alcohols Industry face during its growth?

- Strict regulatory frameworks and the mandated transition toward sustainable alternatives present a significant challenge, compelling producers to innovate and reformulate their product portfolios.

- The market faces significant headwinds from supply chain vulnerability and feedstock price volatility, particularly for propylene feedstock and synthesis gas (syngas). These challenges are compounded by stringent regulatory compliance frameworks, such as the REACH regulation, which restricts the use of certain phthalate plasticizers like dioctyl phthalate (DOP) due to their volatile organic compound (VOC) content.

- This has forced a move away from legacy chemicals and disrupted the supply of key inputs like trimellitic anhydride (TMA). The risk of force majeure events at major production hubs can tighten supply, causing price spikes of over 30% in a single quarter.

- Moreover, the economic deceleration impact on end-use industries adds another layer of uncertainty, making it difficult to balance production with fluctuating demand while adhering to evolving chemical safety standards.

Exclusive Technavio Analysis on Customer Landscape

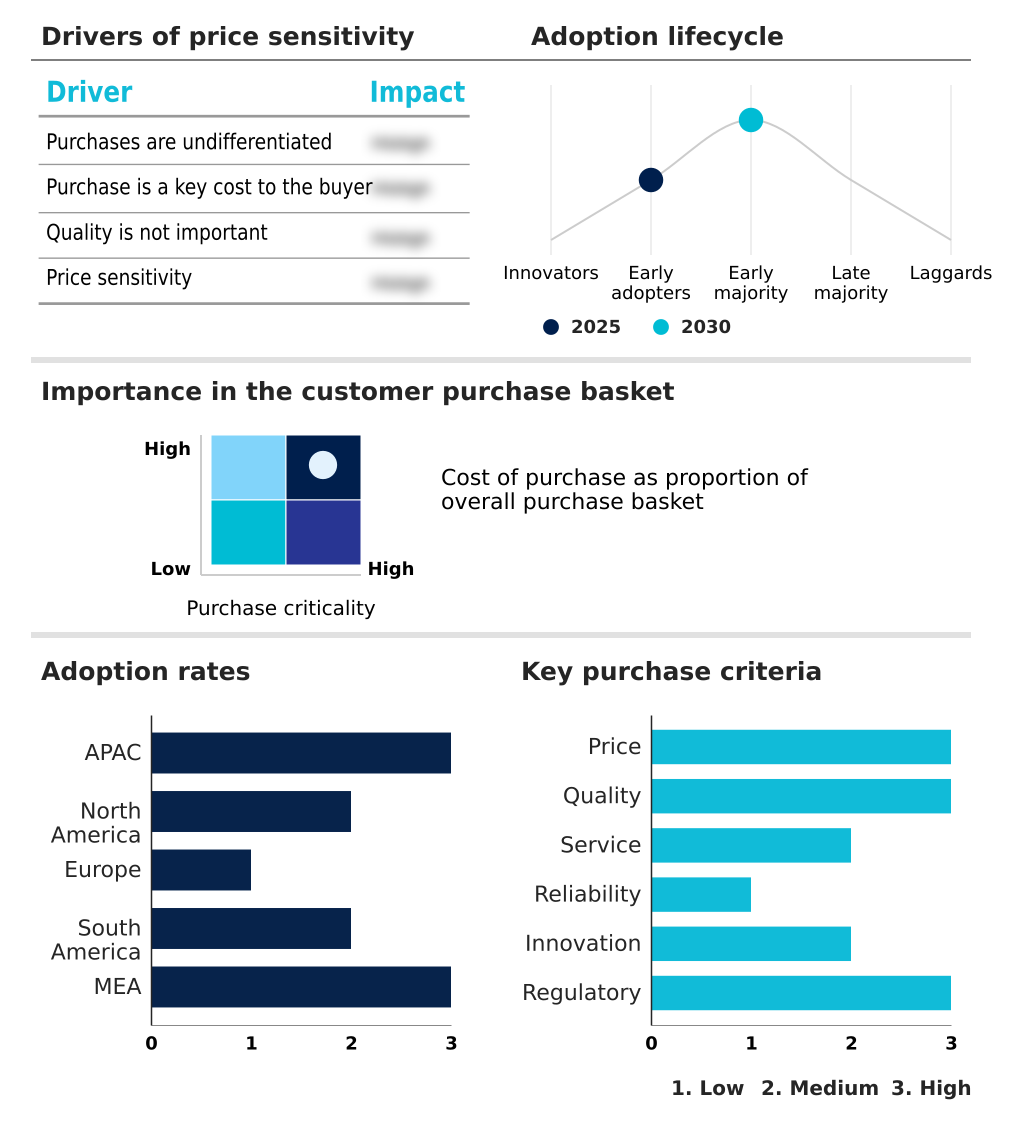

The plasticizer alcohols market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the plasticizer alcohols market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Plasticizer Alcohols Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, plasticizer alcohols market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amines and Plasticizers ltd. - Offerings center on advanced oxo-alcohol intermediates and plasticizer raw materials, engineered to enhance flexible PVC and polymer performance for global industrial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amines and Plasticizers ltd.

- Arkema Group

- BASF SE

- Dow Chemical Co.

- Eastman Chemical Co.

- Evonik Industries AG

- Exxon Mobil Corp.

- INEOS Group Holdings S.A.

- Innospec Inc.

- KH Neochem Co. Ltd.

- Lanxess AG

- LG Chem Ltd.

- Polynt SpA

- Roquette Freres SA

- Sasol Ltd.

- Saudi Basic Industries

- Shell plc

- Supreme Plasticizers

- Tecnosintesi S.p.A.

- VVF Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Plasticizer alcohols market

- In August 2024, BASF SE signed a Memorandum of Understanding with UPC Technology Corp. for the long-term supply of plasticizer alcohols from its Zhanjiang Verbund site, securing feedstock for plasticizer production in South China.

- In October 2024, Evonik Industries AG announced a significant expansion of its production capacities for isononanol-based plasticizers at its facility in Marl, Germany, to meet growing demand for non-phthalate alternatives.

- In January 2025, Braskem announced an investment of approximately USD 100 million to expand its domestic Polyvinyl Chloride (PVC) production capabilities in Brazil, directly increasing regional demand for plasticizers and their alcohol precursors.

- In February 2025, OQ Chemicals GmbH announced global price revisions for its portfolio of oxo intermediates and alcohols, citing fluctuating raw material costs and complex supply chain dynamics.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Plasticizer Alcohols Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 311 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.7% |

| Market growth 2026-2030 | USD 5648.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.0% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Egypt and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The plasticizer alcohols market is evolving beyond commodity chemicals into a sophisticated ecosystem driven by performance and sustainability. Key boardroom decisions now center on managing the production of vital chemical intermediates while aligning with stringent environmental standards like the REACH regulation.

- The industry is pivoting toward high-molecular-weight alcohols and specialty alcohols to meet demand for products with low fogging characteristics and minimal plasticizer migration, particularly for sensitive applications in automotive interiors and wire and cable insulation.

- This shift requires significant capital investment in technologies for synthesizing isononyl alcohol (INA) and 2-propylheptanol (2-PH), which are crucial for diisononyl phthalate (DINP) and other advanced esters. Balancing the use of traditional inputs like 2-ethylhexanol (2-EH) against the need for high-purity alcohols for adipate plasticizers and citrate plasticizers is a key strategic challenge.

- This transition is not without cost, as moving to greener formulations can increase operational expenses by up to 15% due to complex purification processes, a factor that directly impacts corporate budgeting and product pricing strategies.

What are the Key Data Covered in this Plasticizer Alcohols Market Research and Growth Report?

-

What is the expected growth of the Plasticizer Alcohols Market between 2026 and 2030?

-

USD 5.65 billion, at a CAGR of 9.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (2-Ethylhexanol, n-butanol, Isobutanol, Isononyl alcohol, and Others), End-user (Automotive, Construction, and Others), Type (PVC products, and Non-PVC products) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rapid expansion of infrastructure and construction activities in emerging economies, Strict regulatory frameworks and transition to sustainable alternatives

-

-

Who are the major players in the Plasticizer Alcohols Market?

-

Amines and Plasticizers ltd., Arkema Group, BASF SE, Dow Chemical Co., Eastman Chemical Co., Evonik Industries AG, Exxon Mobil Corp., INEOS Group Holdings S.A., Innospec Inc., KH Neochem Co. Ltd., Lanxess AG, LG Chem Ltd., Polynt SpA, Roquette Freres SA, Sasol Ltd., Saudi Basic Industries, Shell plc, Supreme Plasticizers, Tecnosintesi S.p.A. and VVF Ltd.

-

Market Research Insights

- The plasticizer alcohols market is shaped by dynamic end-user industry demand, where material property enhancement is critical. The push for automotive lightweighting materials has spurred innovation, while PVC flexibility enhancement remains a core requirement in construction, contributing to a 9.0% year-over-year market expansion.

- This growth is not uniform; high-performance polymers see adoption rates nearly 15% higher in regulated markets compared to price-sensitive regions. The ongoing development of eco-friendly plasticizer alternatives and adherence to strict chemical safety standards are creating new value streams.

- Strategic investments in specialty chemical synthesis and circular feedstock integration are essential for navigating this landscape, where feedstock price volatility continues to be a primary concern for maintaining stable production costs and profitability.

We can help! Our analysts can customize this plasticizer alcohols market research report to meet your requirements.

RIA -

RIA -