Quantum Dots (QD) Market Size 2024-2028

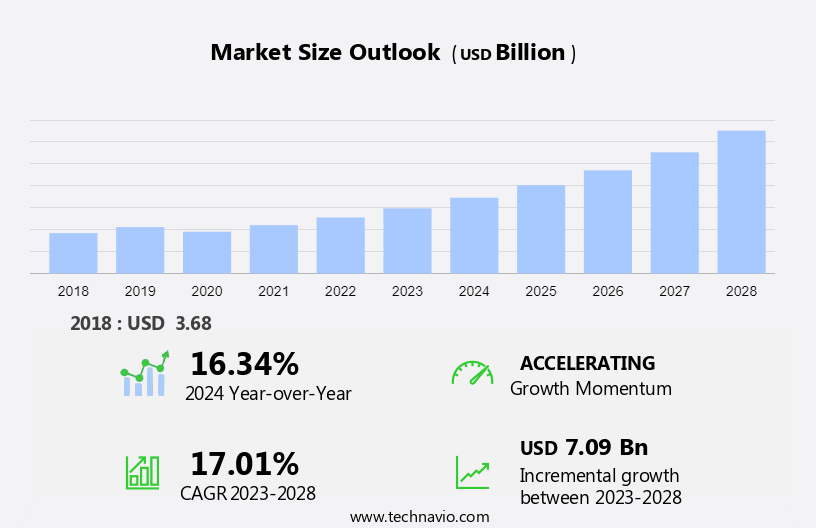

The Quantum Dots (QD) Market size is forecast to increase by USD 7.09 billion, at a CAGR of 17.01% between 2023 and 2028. Market growth is contingent upon various factors, notably the rising demand for devices optimized for superior performance and high resolution. Concurrently, consumer interest in cadmium-free quantum dots is burgeoning, driven by their environmental benefits. Additionally, there's a growing need for energy-efficient devices, aligning with sustainability trends. These factors collectively shape the trajectory of the market, reflecting evolving consumer preferences towards technologically advanced, eco-friendly products. As demand for optimized devices and eco-friendly solutions continues to rise, manufacturers are compelled to innovate, driving further growth in the market.

The market growth and forecasting report includes key player's detailed analyses of the competitive landscape of the market and information about 20 market companies, including American Elements, Indium Corp., LG Electronics Inc., Merck KGaA, Nanorh, Nanosys Inc., Nippon Chemical Industrial Co. Ltd., NNCrystal US Corp., Ocean NanoTech LLC, QD Laser Inc., Quantum Solutions UK, RANVOUS Inc., Samsung Electronics Co. Ltd., UbiQD Inc., Core Quantum Technologies, Crystalplex Corp., Strem Chemicals Inc., and XTPL S.A.. Additionally, ams OSRAM AG offers quantum dots that are used in a variety of applications, including as fluorescent materials, in displays, security features on banknotes, used for general lighting, LEDs, and others.

What will be the Size of the Market During the Forecast Period?

For More Highlights About this Report, Download Free Sample in a Minute

Market Segmentation

By Material

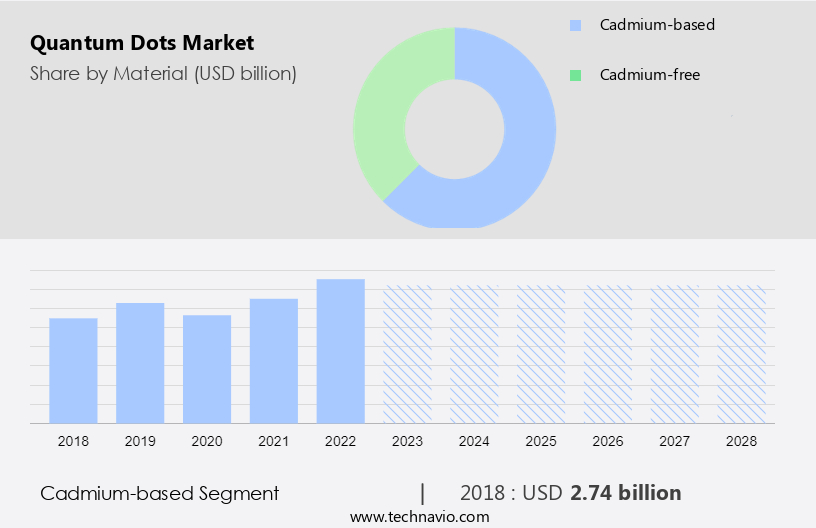

The cadmium-based segment is estimated to witness significant growth during the forecast period. The main features of the cadmium-based segment are broad UV excitation, narrow emission, strong photoluminescence (PL), and high photostability, making them appropriate for use in bioimaging, EL and PV devices, catalytic hydrogen generation, sensors, and other applications. In addition, the cadmium selenide (CdSe) segment is renowned for its uniform size distribution and flexibility.

Get a glance at the market contribution of various segments Download the PDF Sample

The cadmium-based segment was the largest segment and was valued at USD 2.74 billion in 2018. Moreover, CdSe coresegment may be driven at a range of wavelengths and emitted with a narrow peak, resulting in color-pure emission that spans virtually the whole visible spectrum. In addition, for demonstrations and proof-of-concept work, CdSe core segment are a low-cost option. Furthermore, because of its appropriate and customizable bandgap over the visible spectrum, CdSe, the most common form of QD, has emerged as one of the most thoroughly investigated fluorescent semiconductor nanocrystal families. Hence, such factors are fuelling the growth of this segment which in turn drives the market growth during the forecast period.

By Product

The growing adoption of quantum dots in displays segments will increase the market growth. Quantum dot displays feature a restricted spectrum, good stability, and consume little power and thus display makers are increasingly employing them. In addition, they are utilized in displays of flat-panel TV screens, digital cameras, cellphones, gaming consoles, and personal digital assistant (PDA) devices. Moreover, LEDs with quantum dot luminophores are a potential breakthrough in the display ecology. Furthermore, displays use it and have several advantages, including superb color rendering, high lighting efficiency, and inexpensive cost. Hence, such factors are fuelling the growth of this segment which in turn drives the market growth during the forecast period.

By region

For more insights on the market share of various regions Download PDF Sample now!

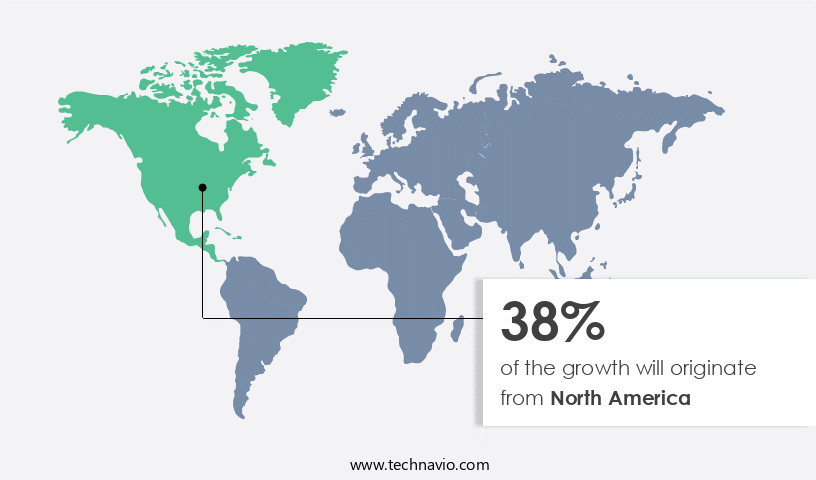

North America is estimated to contribute 38% to the growth of the global market during the forecast period.

Technavio's analysts have provided extensive insight into the market forecast, detailing the regional trends and drivers influencing the market's trajectory throughout the forecast period. Several factors such as high display demand and the early adoption of quantum dot technology in applications including healthcare and automotive drive quantum dots market growth.

Moreover, because of the widespread adoption of quantum dot displays, the US market has the region's largest market share. Furthermore, several consumer electronics manufacturers in North America are working on producing hybrid quantum dot displays to address the rising need for flexible displays. Therefore, this technique will assist consumer gadgets that require a flexible display. Hence, such factors are driving the market growth in North America during the forecast period.

Market Dynamics and Customer Landscape

The market is witnessing significant growth propelled by advancements in plasmonic devices and quantum computers. With innovations like cadmium-based QDs, it enhances electroluminescence (EL) and photovoltaic (PV) devices. Moreover, QDs play a pivotal role in catalytic hydrogen production and facilitate the development of high-quality display devices. Extensive research and development activities in nanotechnology and quantum computing drive the market forward, supporting applications in diverse fields such as cell biology research and microscopy. Harnessing the unique properties of atoms, QDs offer promising solutions for next-generation technologies.

Key Driver

Increasing demand for optimized devices with better performance and high resolution is notably driving the market. The growing demand for optimized devices with better performance and high resolution has gained market traction in the last few years in multiple domains, including consumer electronics and communication. In addition, modern screens not only have improved brightness and contrast ratios, but they also have higher resolutions and use less power than older displays.

Moreover, display makers are designing screens with higher characteristics to increase their market position. In addition, they are widely utilized in display systems because they provide richer color resolution, better color purity, a highly immersive high-dynamic-range (HDR) experience, and superior energy efficiency than traditional displays. Furthermore, because they have narrow emission spectra and broad excitation profiles, they can more efficiently convert light into any hue in the visible spectrum. Hence, such factors are driving the market growth during the forecast period.

Significant Trends

Increasing adoption of optoelectronics is one of the emerging market trends shaping the growth. Quantum dots are mainly used in LCD devices, including TVs, smartphones, and tablets. In addition, these displays use LED backlights to enhance the color gamut by inserting a thin film of them between the backlight and the display. Furthermore, the narrow color-band frequency emission and small size of these materials help manage the brightness of the display, and almost 80% less power is consumed by this material than LCD and OLED displays.

For instance, Sony and Samsung are developing quantum dot-based 4K and 8K LED LCD TVs. In addition, these are also popular in optoelectronic devices such as telecom components and lasers to increase their efficiency. Furthermore, they allow LCD technology to grow in the display market for applications such as signage, monitors, and TVs. Hence, such factors are driving the market growth during the forecast period.

Major Market Restrain

The lack of raw material availability for quantum dots is a major challenge hindering the market. Rare earth materials, including cadmium, selenium, zinc, and indium, are used in its manufacturing. In addition, as there are a limited number of suppliers who deal with the quality of raw materials for quantum dots, these materials are very expensive owing to their limited availability and high demand globally.

Moreover, they are created by a variety of processes that employ materials with comparable characteristics. In addition, materials appropriate for the creation of these devices are difficult to obtain. Moreover, cadmium is a hazardous metal that is not environment friendly. Furthermore, cadmium, selenium, and indium are all being employed more and more in the production of these materials. However, due to their scarcity, these commodities should be handled wisely. Hence, such factors are hindering the market growth during the forecast period.

Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market research and growth, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth and trends strategies.

Global Market Customer Landscape

Market Players

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

MaTecK Gmbh: The company offers quantum dots that are used in different applications such as photovoltaic devices, biosensors, flat panel displays, lasers, memory elements, and others.

Market analysis and report of qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Segment Overview

The market research report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "USD Billion" for the period 2024 to 2028, as well as historical data from 2018 to 2022 for the following segments

- Material Outlook

- Cadmium-based

- Cadmium-free

- Product Outlook

- Displays

- Others

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- The U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- South America

- Chile

- Argentina

- Brazil

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

Market Analyst Overview

The market is witnessing rapid growth across various sectors such as consumer electronics companies, agriculture, medicine, and environmental monitoring. Quantum dots, including alloyed quantum dots and core-shell quantum dots, are revolutionizing industries with their unique properties. Applications range from flat-panel LED displays and LED TVs to OLED screens and microLED TVs, offering superior illumination efficiency and luminous efficiency. With advancements like quantum dot enhancement film (QDEF) and nanocell technology, quantum dots are driving innovation in LCD-based QLED panel technology and solid-state lighting. As demand rises for technologically advanced products, the quantum dot industry continues to expand, shaping the future of lighting, displays, and beyond.

Further, the market is witnessing rapid expansion, driven by innovations such as 4K tech and Colloidal QD LED. These advancements cater to diverse applications in the consumer vertical, including fitness trackers and mobile phones, enhancing display quality and energy efficiency. With concerns over heavy metal contamination, Indium and zinc emerge as viable substitutes for cadmium in QD technology, ensuring environmental sustainability. QDs also enable advancements in infrared range applications like night vision and surveillance, while their integration into LCD displays and LED backlighting revolutionizes TV sets and lighting companies. Moreover, QDs facilitate mass production and enhance solar cells efficiency, driving their adoption in greenhouses and optical coherence tomography systems.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 17.01% |

|

Market Growth 2024-2028 |

USD 7.09 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

16.34 |

|

Regional analysis |

North America, Europe, APAC, Middle East and Africa, and South America |

|

Performing market contribution |

North America at 38% |

|

Key countries |

US, Canada, China, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

American Elements, ams OSRAM AG, Indium Corp., LG Electronics Inc., MaTecK GmbH, Merck KGaA, Nanorh, Nanosys Inc., Nippon Chemical Industrial Co. Ltd., NNCrystal US Corp., Ocean NanoTech LLC, QD Laser Inc., Quantum Solutions UK, RANVOUS Inc., Samsung Electronics Co. Ltd., UbiQD Inc., Core Quantum Technologies, Crystalplex Corp., Strem Chemicals Inc., and XTPL S.A. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market report forecast during the forecast period

- Detailed information on factors that will drive the growth of the market between 2023 and 2028

- Precise estimation of the market size and its contribution to the market in focus on the parent market

- Accurate predictions about upcoming trends and changes in consumer behavior

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough market analysis and report of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of Industry companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -