Residential Digital Faucets Market Size Report 2024-2028

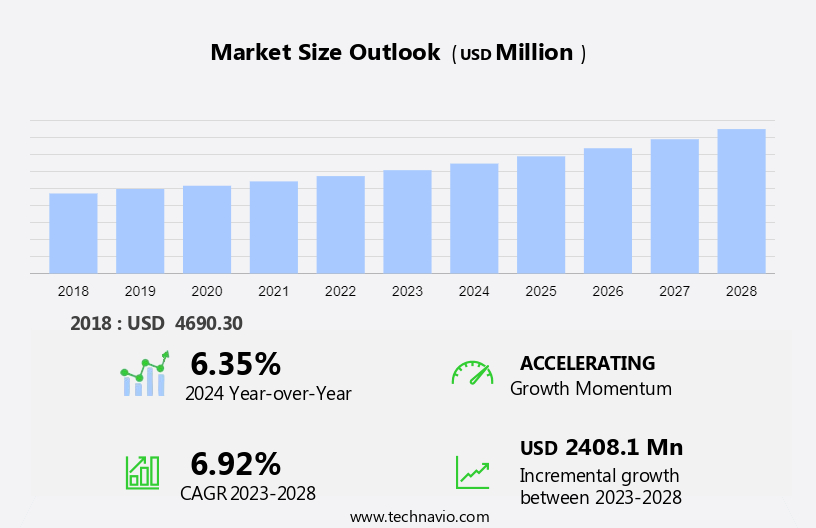

The residential digital faucets market size is forecast to increase by USD 2.40 billion at a CAGR of 6.92% between 2023 and 2028. The market is experiencing significant growth due to several key factors. Firstly, the increasing consumer expenditure on bathroom and kitchen remodeling projects is driving demand for advanced and technologically innovative faucets. Secondly, the flourishing residential construction industry is providing new opportunities for market expansion. Lastly, technological advancements in digital faucets, such as touchless controls, temperature regulation, and energy efficiency, are making these products increasingly desirable for homeowners. As a result, the market for residential digital faucets is poised for continued growth in the coming years. Our report examines historical data from 2018 - 2022, besides analyzing the current and forecasted market scenario.

The market in the region is experiencing significant growth due to escalating consumer expenditures on bathroom and kitchen remodeling and renovation projects. Innovative offerings from digital faucet manufacturers are further fueling this trend, as consumers are increasingly drawn to these advanced products. These faucets, equipped with features such as touchless control, temperature regulation, and energy efficiency, add value and convenience to homeowners' daily lives. As a result, the market for residential digital faucets is poised for continued expansion in the region.

What will the Residential Digital Faucets Market Size be during the Forecast Period?

Market Forecast 2023-2027

To learn more about this report, Request Residential Digital Faucets Market Analysis Report Free Sample

Residential Digital Faucets Market Dynamics

This market report predicts significant growth in the Metal Industry, driven by advancements in Artificial Intelligence and the Internet of Things. Smart Toilets, equipped with IR Sensors and Motion Sensors, are becoming increasingly popular, leading to an increased demand for digital faucets. E commerce Platforms provide a convenient Online Distribution Channel for these products, making them easily accessible to consumers. Residential digital faucets offer Multi functionality faucets, including personalized temperature control, water flow adjustment, and aesthetic appeal. The Trend of remodeling homes has led to digital faucets becoming a Style Statement in the residential segment. Strategic acquisitions by manufacturers have expanded their offerings in the Commercial Faucet Segment, including the Hospitality Sector. The digital faucet system consists of a metal portion, water system, handle, cartridge, spout, mixing chamber, aerator, and intake source. These components work together to provide a seamless and efficient water delivery experience. Overall, the market is poised for continued growth, offering consumers convenience, functionality, and design innovation. Our researchers studied the market research and growth data for years, with 2023 as the base year and 2023 as the estimated year, and presented the key drivers, trends, and challenges for the market.

Key Residential Digital Faucets Market Driver- Technological advancements in residential digital faucets

The plumbing sector is witnessing significant growth in the adoption of residential digital faucets, driven by the increasing consumer preference for water-saving technology and sensor-based fixtures in bathroom and kitchen applications. These advanced faucets, which include sink faucets, bidet faucets, and sanitary ware faucets, are increasingly becoming a popular choice for homeowners undergoing bathroom and kitchen remodeling projects.

Furthermore, faucets rank among the top upgraded features during these home improvement initiatives in the US, with a substantial portion of the expenditure allocated to residential digital faucets. The latest technological advancements, such as flow control and temperature control features, are major factors contributing to the rising demand for these products in the market. Overall, these factors will be a major factor in boosting the growth of the market during the forecast period.

Significant Residential Digital Faucets Market Trends - Strong distribution network between manufacturers and retailers

In the plumbing sector, the market is witnessing significant growth as companies prioritize expanding their distribution networks with retailers and e-commerce partners. This strategy is crucial for establishing a strong global presence, particularly in countries like China and India, where the market remains largely unorganized. companies are also investing in advanced technologies, such as water saving mechanisms and sensor-based faucets, to cater to evolving consumer preferences.

Furthermore, major players in the market, including Kohler, LIXIL, and Masco, are capitalizing on the growing popularity of e-commerce platforms by offering their products on websites like Amazon, Alibaba, and The Home Depot. The integration of water saving technology and sensor-based functionality in digital faucets is expected to further fuel market growth. Hence, major companies in the market will adopt further strategies to strengthen their distribution network with online and offline partners during the forecast period.

Major Residential Digital Faucets Market Challenge - Threat from unorganized markets

In the plumbing sector, the implementation of water saving technology has gained significant traction. One such innovation is sensor-based faucets, which are gaining popularity due to their convenience and efficiency. However, the adoption of these advanced faucets is relatively low in emerging markets due to their higher cost compared to conventional faucets.

Furthermore, the primary component driving up the cost is the inclusion of electronic sensors and other digital components. Despite the benefits of water conservation and modern functionality, the high price point restricts their accessibility in regions such as Brazil, Mexico, Argentina, South Africa, and India. Consequently, the penetration of sensor-based faucets in these markets remains lower than in developed countries like the UK and the US. Hence, these factors may hinder their adoption during the forecast period

Residential Digital Faucets Market Segmentation

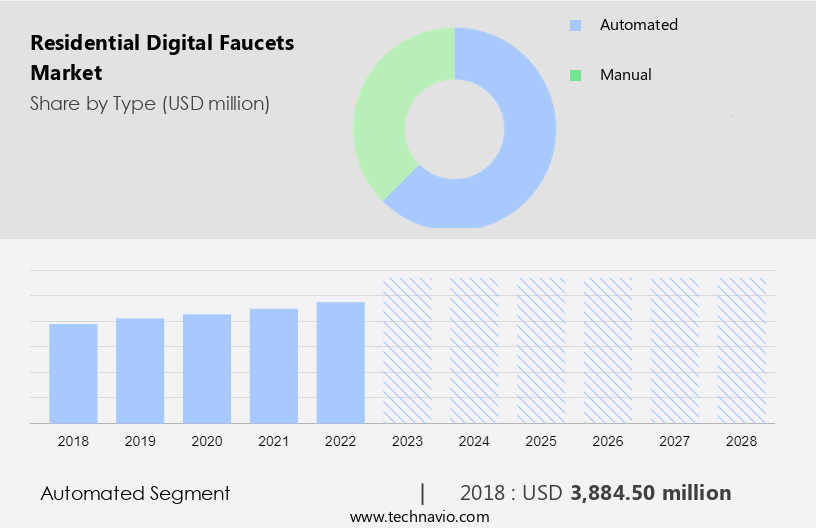

Type Segment Analysis

The automated segment was valued at USD 3.88 billion in 2018. By type the market is divided into the automated and manual segment. The automated segment will account for a major share of the market's growth during the forecast period. Digital faucets, also referred to as electronic or smart faucets, are gaining popularity in both residential and commercial sectors. These advanced bathroom and kitchen accessories employ sensors and hands-free technology for operation. The fittings consist of metal balls and rubber seals, ensuring a consistent water flow and leak-free performance. Colours, designs, and finishes cater to various consumer preferences, transforming these functional items into stylish bathroom and kitchen accessories.

Customised Report as per your requirements!

Smart goods, including digital faucets, are in demand due to increasing consumer disposable income and the renovation trend. Urbanisation and industrial investment have further fueled market growth. Young homeowners and millennials, in particular, are drawn to these touch-free faucets for their basic cleanliness and sanitary benefits. The bathroom segment dominates the worldwide sales of digital faucets, with one-hand mixer and two-hand mixer models available. Kitchen applications also benefit from these faucets, with compression, ceramic disc, metal, and plastics materials used in their construction. The temperature gauges and touch sensors add to the convenience and sophistication of these smart home technology products. The hotel business and real estate sector are significant contributors to the commercial digital faucets market. Home remodelling investment and the growing interest in smart home technology are expected to boost sales in the residential sector. Overall, the market is set for significant growth, offering a wide range of benefits to consumers and businesses alike.

Regional Analysis of the Residential Digital Faucets Market

For more insights on the Residential Digital Faucets Market Share of various regions Download Sample PDF now!

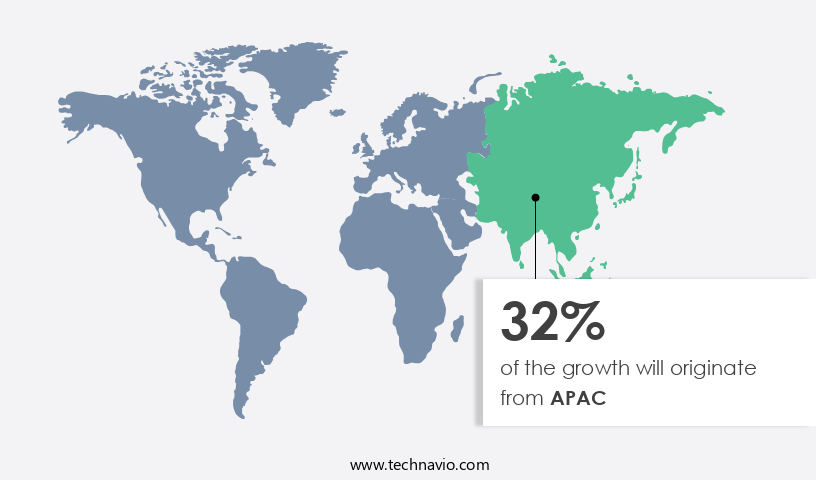

APAC is estimated to contribute 32% to the growth by 2027. Technavio's analysts have provided extensive insight into the market forecasting, detailing the regional trends and drivers influencing the market's trajectory throughout the forecast period. The market encompasses the sales of electronic and smart faucets for both bathroom and kitchen applications. These faucets incorporate advanced technologies such as touch sensors, temperature gauges, and hands-free operation. The market is driven by various factors, including the renovation trend, industrial investment, and urbanisation. Young homeowners and millennials, in particular, are showing a preference for these modern bathroom and kitchen accessories. Digital faucets come in various designs, colours, and finishes to suit different consumer preferences.

Bathroom segments, including one-hand mixers and two-hand mixers, are popular choices for residential applications. In contrast, kitchen segments cater to the demand for more substantial and functional faucets. The market is witnessing significant growth due to the increasing consumer disposable income and the worldwide sales of smart goods. The market is further propelled by the adoption of smart home technology and the demand for basic cleanliness and sanitary goods. Plumbing fittings manufacturers are investing in research and development to produce digital faucets with advanced features such as compression, ceramic disc, metal, and plastics. The bathroom segment dominates the market, with the hotel business and real estate sector being significant contributors

Who are the Major Residential Digital Faucets Market Companies?

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Acquaviva India Pvt. Ltd. - The company offers residential digital faucets such as deck-mounted and wall-mounted.

BRIZO KITCHEN and BATH CO - The company offers advanced water delivery systems

We also have detailed analyses of the market’s competitive landscape and offer information on 20 market companies, including:

Acquaviva India Pvt. Ltd., BRIZO KITCHEN and BATH CO, CERA Sanitaryware Ltd., Danube Group, Elkay Manufacturing Co., Euronics Industries Pvt. Ltd., Jaquar India, Kajaria Ceramics Ltd., Kohler Co., Kraus USA Inc., LIXIL Corp., Masco Corp., Moen Inc., Oras Ltd., Prism Johnson Ltd., RN Valves and Faucets, Roca Sanitario SA, Stanley Black and Decker Inc., Taiwan Kingbird Enterprises Inc., and Toto Ltd.

Technavio market forecast the an in-depth analysis of the market and its players through combined qualitative and quantitative data. The analysis classifies companies into categories based on their business approaches, including pure-play, category-focused, industry-focused, and diversified. Companies are specially categorized into dominant, leading, strong, tentative, and weak, based on their quantitative data analysis.

Segment Overview

The residential digital faucets market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD Billion" for the period 2024-2028, as well as historical data from 2018 - 2022 for the following segments.

- Type Outlook

- Automated

- Manual

- Distribution Channel

- Offline

- Online

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

Market Analyst Overview

The overall faucet market is experiencing significant growth due to the increasing adoption of smart home technologies. These faucets offer convenience and functionality with features such as touch control, motion sensors, and temperature control. The integration of digital technology in residential faucets is a game-changer, enabling users to customize their water usage and save water. The market is driven by factors such as increasing disposable income, urbanization, and the growing trend towards energy efficiency. Manufacturers are focusing on innovation and design to cater to the evolving needs of consumers.

Furthermore, the market is segmented based on technology, application, and region. The touch control segment is expected to dominate the market due to its ease of use and growing popularity. The Asia Pacific region is expected to witness the highest growth in the market due to increasing urbanization and rising disposable income. In conclusion, the market is set for growth due to the increasing demand for smart home technologies and the growing trend towards energy efficiency. Manufacturers are focusing on innovation and design to cater to the evolving needs of consumers. In the market, the increasing personal disposable income and demand for high quality home decor are driving the adoption of internet enabled intelligent gadgets, which offer significant energy and power savings.

|

Residential Digital Faucets Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

166 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.92% |

|

Market growth 2024-2028 |

USD 2.40 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.35 |

|

Regional analysis |

North America, Europe, APAC, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 32% |

|

Key countries |

US, China, UK, Japan, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks, Residential Digital Faucets Market Industry Report |

|

Key companies profiled |

Acquaviva India Pvt. Ltd., BRIZO KITCHEN and BATH CO, CERA Sanitaryware Ltd., Danube Group, Elkay Manufacturing Co., Euronics Industries Pvt. Ltd., Jaquar India, Kajaria Ceramics Ltd., Kohler Co., Kraus USA Inc., LIXIL Corp., Masco Corp., Moen Inc., Oras Ltd., Prism Johnson Ltd., RN Valves and Faucets, Roca Sanitario SA, Stanley Black and Decker Inc., Taiwan Kingbird Enterprises Inc., and Toto Ltd. |

|

Market dynamics |

Parent market analysis, Market Forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the market forecast period, Residential Digital Faucets Market Growth Analysis |

|

Customization purview |

If our residential digital faucets market worth report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

Request Residential Digital Faucets Market Forecast Sample PDF

What are the Key Data Covered in this Residential Digital Faucets Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the residential digital faucets market growth and forecasting of the market between 2024 and 2028

- Precise estimation of the residential digital faucets market size and its contribution to the parent market

- Accurate predictions about upcoming residential digital faucets market trends and analysis and changes in consumer behavior

- Growth of the market industry across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough residential digital faucets market growth analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive market analysis and report on the factors that will challenge the market research and growth of market companies

RIA -

RIA -