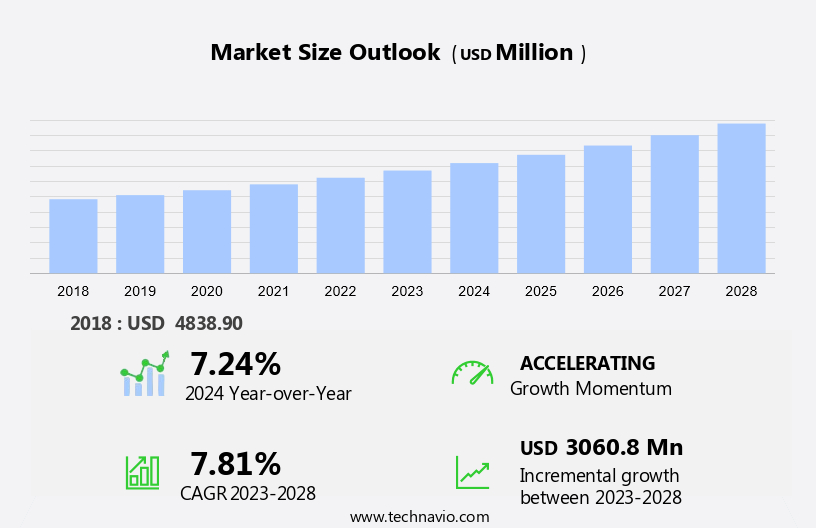

Seed Treatment Market Size 2024-2028

The seed treatment market size is forecast to increase by USD 3.06 billion at a CAGR of 7.81% between 2023 and 2028.

- The market is experiencing significant growth due to the rising awareness regarding seed-applied technologies. Traditional strategies are being adopted to develop innovative seed treatment products that cater to the evolving needs of farmers. However, the market is also facing challenges, such as the ban on chemical-based seed treatment solutions due to environmental concerns. This trend is leading to the development of eco-friendly alternatives, which are expected to gain popularity In the coming years. The market growth is being driven by the increasing demand for high-yielding crops and the need to improve agricultural productivity. Additionally, the adoption of precision farming techniques and the integration of IoT and automation in seed treatment processes are also expected to provide significant opportunities for market growth.

- Overall, the market is poised for robust growth, with a focus on sustainable and eco-friendly solutions.

What will be the Size of the Seed Treatment Market During the Forecast Period?

- The market plays a crucial role In the agricultural industry by enhancing crop production and ensuring resistance against various pests and soil-borne infections. Seed treatments are applied to seeds before planting, incorporating living organisms, bio-based seed, or chemical compounds to bolster seed strength, leaf strength, and fruit strength. These treatments protect crops against insects, pests, and climate change-induced stressors, thereby reducing the need for extensive crop protection activities. Germination time is significantly reduced with seed treatments, allowing for earlier planting and increased productivity. Integrated pest management practices and organic farming methods have fueled the demand for seed treatments, as they offer a more sustainable approach to crop production.

- Selected crops, including corn, soybean, wheat, and canola, are major beneficiaries of seed treatments. Development activities In the market continue to focus on improving pest resistance, enhancing crop yield, and addressing the challenges posed by pandemic-induced disruptions and climate change.

How is this Seed Treatment Industry segmented and which is the largest segment?

The seed treatment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2017-2022 for the following segments.

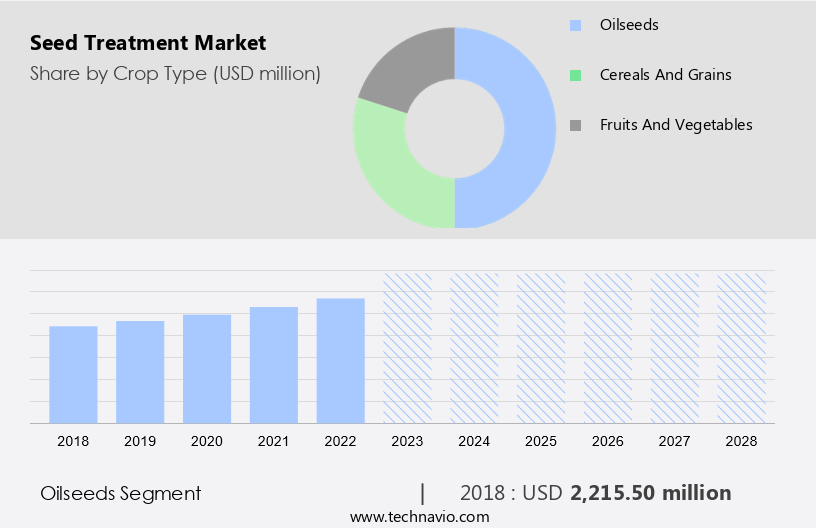

- Crop Type

- Oilseeds

- Cereals and grains

- Fruits and vegetables

- Type

- Chemical

- Non-chemical

- Geography

- North America

- US

- APAC

- China

- India

- Europe

- France

- South America

- Middle East and Africa

- North America

By Crop Type Insights

- The oilseeds segment is estimated to witness significant growth during the forecast period.

The market is driven by the chemical segment due to its superior ability to enhance crop resistance against pests, insects, and soil-borne infections. Faster germination and productivity are additional benefits, making it a preferred choice for farmers. Insecticides and fungicides are the primary chemical treatments, with insecticides dominating due to their extensive use in various crops. The demand for high-quality seeds and the need to increase agricultural yield further fuel market growth. Seedborne and soilborne diseases pose significant challenges, necessitating effective seed treatments. Integrated pest management practices and organic farming are emerging trends, driving the demand for non-chemical treatments. Key crops, such as corn, soybean, wheat, and canola, heavily utilize seed treatments for crop protection.

The market is influenced by factors like climate change, pandemics, and development activities. Chemical treatments, including synthetic seed treatments and biobased pesticides, continue to dominate, although fungicides and bio-based seed treatments are gaining traction due to health concerns and environmental sustainability.

Get a glance at the Seed Treatment Industry report of share of various segments Request Free Sample

The Oilseeds segment was valued at USD 2.21 billion in 2018 and showed a gradual increase during the forecast period.

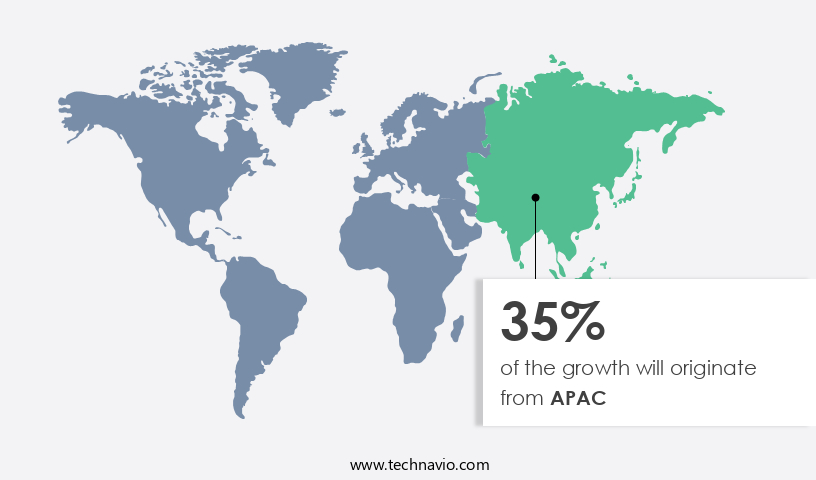

Regional Analysis

- APAC is estimated to contribute 35% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market in North America is a significant and advanced industry, with the region having the highest per-hectare consumption of agrochemicals (approximately 4.5 kilograms per hectare). The market's growth relies on enhancing crop productivity while preserving soil health. Key players in this region employ various strategies, including product launches, to expand their market share and broaden their offerings. The North American the market accommodates both international and local companies. Strategic product launches are a primary focus for key players to strengthen their presence In the regional market. This market caters to various crops, including corn, soybean, wheat, and canola, as well as fruit and vegetable plantations.

Effective seed treatments aid in combating pests, such as insects, predators, parasites, disease-causing fungi, bacteria, and viruses, ensuring high-quality agricultural products. The market also addresses concerns related to seedborne diseases and soilborne infections, impacting germination time and crop yield. In the context of health concerns, organic seed treatments are gaining popularity. The market's development is influenced by factors like climate change, pandemic, and development activities.

Market Dynamics

Our seed treatment market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Seed Treatment Industry?

Rising awareness regarding seed-applied technologies is the key driver of the market.

- The market is experiencing significant growth due to the increasing focus on crop production and the need to enhance seed resistance against pests, insects, and soil-borne infections. Seed treatment plays a crucial role in improving leaf strength, fruit strength, and seed strength, ultimately leading to higher agricultural productivity and crop yield. The demand for treated seeds is particularly high in developing economies where the demand for food is increasing faster than the availability of arable land. Farmers are adopting high-yielding hybrid seeds to maximize their production, which in turn is driving the need for seed treatments with long shelf lives and high quality.

- Government initiatives, such as the India Seed Treatment Campaign, are also promoting the usage of treated seeds to ensure food security and improve agricultural product quality. Climate change and pandemics have added to the challenges faced by farmers, making crop protection activities more critical than ever. Seed treatments using both synthetic and biobased pesticides, including fungicides, insecticides, and pesticide products, are being employed to protect crops from insect pests, predators, parasites, disease-causing fungi, bacteria, and viruses. Integrated pest management practices and organic farming practices are gaining popularity, leading to an increased demand for organic seed treatments. The market for seed treatments is expected to continue its growth trajectory as farmers seek to mitigate the risks of crop damage caused by various factors and ensure high-quality agricultural products for consumers.

What are the market trends shaping the Seed Treatment Industry?

Traditional strategies aimed towards developing innovating seed treatment products is the upcoming market trend.

- The market plays a crucial role in enhancing crop production by fortifying seeds against pests, insects, and soil-borne infections. Seed treatment is essential for various agricultural products, including fruits, vegetable crops, and high-yield crops such as corn, soybean, wheat, and canola. Seed treatment ensures leaf and fruit strength, reducing crop damage caused by insect pests, predators, parasites, disease-causing fungi, bacteria, and viruses. Seedborne diseases and soilborne diseases are significant challenges in agriculture, leading to a demand-supply gap in agricultural yield. To address these concerns, the market offers both synthetic seed treatments and biobased pesticides, including fungicides and chemicals, as well as non-chemical alternatives.

- Organic treatment is also gaining popularity in organic farming practices due to health concerns and climate change. The market is characterized by the presence of international and local players, with a focus on acquisitions, partnerships, and collaborations to broaden their offerings and increase market share. For instance, in January 2023, EVOIA partnered with Albaugh LLC. To develop innovative seed treatment products using liquid biochar extract technology. This partnership expands Albaugh LLC.'s portfolio in customized seed treatments and demonstrates its commitment to delivering new, innovative products. In summary, the market is a vital component of crop protection activities, ensuring high-quality agricultural products and addressing the challenges of pests, diseases, and climate change.

- The market offers various solutions, including synthetic and biobased seed treatments, to cater to the diverse needs of agricultural product development in developing economies and beyond.

What challenges does the Seed Treatment Industry face during its growth?

Ban on chemical-based seed treatment solutions is a key challenge affecting the industry growth.

- Seed treatment is a crucial aspect of crop production, enhancing seed resistance against pests, insects, and soil-borne infections. However, health concerns related to the use of hazardous chemicals in seed treatments have led to increasing demand for organic alternatives. The ban on certain chemicals, such as neonicotinoids In the European Union and various neonicotinoid-based products in Brazil, China, and the United States, is expected to impact the market. Farmers in developing economies rely heavily on seed treatments to protect their fruits, vegetable crops, and high-yield crops from insect pests, predators, parasites, disease-causing fungi, bacteria, and viruses. Integrated pest management practices and organic farming practices are gaining popularity as alternatives to synthetic seed treatments.

- The use of biobased pesticides, fungicides, and non-chemical treatments is on the rise. Climate change and pandemics have further accentuated the need for seed treatments to ensure healthy agricultural product development and productivity. Despite these challenges, the demand for high-quality agricultural products remains strong, particularly In the agricultural, fruit, and vegetable plantation development sectors.

Exclusive Customer Landscape

The seed treatment market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the seed treatment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, seed treatment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

AGLUKON Spezialduenger GmbH and Co. KG - The company specializes in seed treatment solutions, enhancing agricultural productivity through improved root development, germination, and uniform emergence. This innovative approach optimizes crop growth potential, ensuring better yields for American farmers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AGLUKON Spezialduenger GmbH and Co. KG

- Albaugh LLC

- Associated British Foods Plc

- BASF SE

- Bayer AG

- BioWorks Inc.

- Corteva Inc.

- Excel Crop Care Ltd.

- FMC Corp.

- Humintech GmbH

- Koch Industries Inc.

- Mitsui and Co. Ltd.

- Novozymes AS

- Nufarm Ltd.

- OMEX

- Plant Health Care Plc

- Roquette Freres SA

- Sumitomo Chemical Co. Ltd.

- Syngenta Crop Protection AG

- UPL Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Latest Market Developments and News

-

In December 2024, BASF launched a new seed treatment product designed to protect crops from soil-borne diseases and pests. This innovative treatment uses a biological active ingredient that enhances seed germination and plant growth, addressing the increasing demand for sustainable and eco-friendly agricultural solutions.

-

In November 2024, a strategic partnership between Corteva Agriscience and a leading biotech company was announced to develop advanced seed treatments that improve resistance to climate-related stresses. The partnership focuses on creating solutions for crops to withstand droughts, heat, and other environmental challenges, responding to the rising need for climate-resilient agriculture.

-

In October 2024, Syngenta introduced a new range of seed treatment products aimed at enhancing seed vigor and improving disease resistance in high-value crops like corn and soybeans. The treatments utilize advanced chemical formulations that protect seeds from early-stage pathogens, contributing to higher crop yields and quality.

-

In September 2024, FMC Corporation acquired a leading company specializing in biological seed treatments. This acquisition strengthens FMC's position in the sustainable agriculture sector, allowing the company to expand its offerings of natural, environmentally friendly seed treatment products aimed at improving crop productivity and reducing reliance on synthetic chemicals.

Research Analyst Overview

Seed treatment is an essential process in modern crop production, enhancing the overall health and productivity of agricultural products. This process fortifies seeds with various substances to bolster their resistance against pests, diseases, and environmental stressors. By strengthening seeds, farmers can improve crop yield and ensure high-quality agricultural outputs. Pests and diseases pose significant challenges to crop production, with insects, leaf strength, and fruit strength being among the most common issues. Soil-borne infections, such as seedborne diseases and soilborne diseases, can also adversely impact germination time and agricultural yield. These concerns have led to the increased adoption of seed treatments as a crucial component of crop protection activities.

Seed treatment plays a vital role in addressing health concerns related to pests and diseases. Insect pests, predators, parasites, disease-causing fungi, bacteria, and viruses can all negatively impact crop production. Seed treatments, which can include both synthetic and biobased pesticides, fungicides, and non-chemical alternatives, help mitigate these risks and promote healthier crops. The demand for seed treatments is driven by the need to maintain productivity and address the demand-supply gap in various agricultural sectors. Developing economies, in particular, have seen significant growth In the adoption of seed treatments for fruits, vegetable crops, and high-yield crops like corn, soyabean, wheat, and canola.

Integrated pest management practices have gained popularity in modern agriculture, with seed treatments being a key component. These practices aim to minimize the use of hazardous chemicals and promote sustainable farming methods. Organic treatment options have also emerged as viable alternatives to synthetic seed treatments, aligning with the growing trend towards organic farming practices. Climate change and the pandemic have further emphasized the importance of seed treatments in ensuring agricultural resilience. Seed treatments help crops withstand various environmental stressors and pests, contributing to the overall sustainability and profitability of agricultural operations. In conclusion, seed treatment is a vital process in modern crop production, addressing various challenges related to pests, diseases, and environmental stressors. The demand for seed treatments is driven by the need to maintain productivity, promote healthier crops, and ensure high-quality agricultural outputs. As the agricultural landscape continues to evolve, seed treatments will remain a crucial component of sustainable and profitable farming practices.

|

Seed Treatment Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

161 |

|

Base year |

2023 |

|

Historic period |

2017-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.81% |

|

Market growth 2024-2028 |

USD 3.06 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.24 |

|

Key countries |

US, China, India, Russia, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Seed Treatment Market Research and Growth Report?

- CAGR of the Seed Treatment industry during the forecast period

- Detailed information on factors that will drive the Seed Treatment growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the seed treatment market growth of industry companies

We can help! Our analysts can customize this seed treatment market research report to meet your requirements.

RIA -

RIA -