Specialty Fluids Market 2024-2028

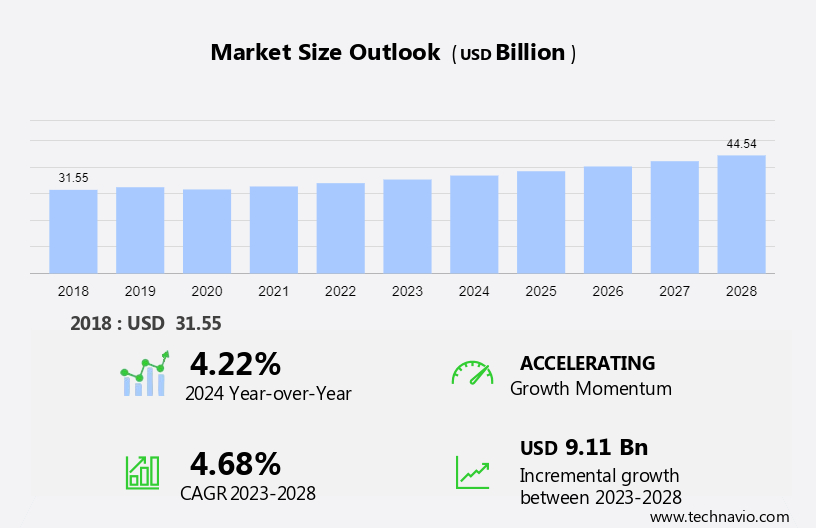

The specialty fluids market size is forecast to increase by USD 9.11 billion at a CAGR of 4.68% between 2023 and 2028. The growth rate of the market depends on several factors, including the growing chemical industry in APAC, the rapid industrialization around the globe, and the innovations in aerosols.

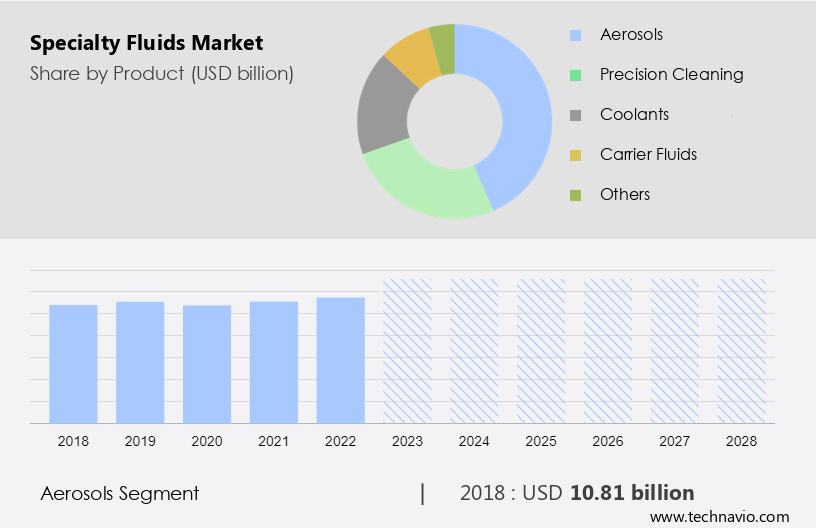

The report includes a comprehensive outlook on the Specialty Fluids Market, offering forecasts for the industry segmented by Product, which comprises aerosols, precision cleaning, coolants, carrier fluids, and others. Additionally, it categorizes Type into hydrofluorocarbon (HFC), hydrofluoroolefin (HFO), polyethylene glycol, and alcohol ethoxylates, and covers Regions, including APAC, North America, Europe, South America, and Middle East and Africa. The market research report provides market size, historical data spanning from 2018 to 2022, and future projections, all presented in terms of value in USD billion for each of the mentioned segments.

What will be the Specialty Fluids Market Size During the Forecast Period?

Specialty Fluids Market Definition

Specialty fluids contain hydrofluorocarbon (HFC), hydrofluoroolefin (HFO), polyethylene glycol, alcohol ethoxylates, isoparaffins, or other products with zero ozone-depleting and low global warming potential. These fluids exhibit superior properties such as low boiling point, low surface tension, excellent solvent retention, non-flammability, high dielectric strength, and chemical and thermal stability.

To Know more about the Market Report Request Free Sample

Specialty Fluids Market: Key Drivers, Trends, Challenges

Key Specialty Fluids Market Driver

The growing chemical industry in APAC is the key factor driving market growth. The chemical industry in APAC contributes significantly to the economic growth of the region. In China and India, the chemical industry has led to the growth of the manufacturing and agriculture sectors. It offers building blocks for various downstream industries such as paper, textiles, leather, and paints. In addition, the chemical industry in APAC has registered rapid growth because of the increase in the number of M&A, high demand for chemical and chemical products, and increasing investments in the region.

Furthermore, the high domestic consumption of chemicals drives the chemical industry in the region. Urbanization and industrialization have increased the demand for chemicals in adhesives, paints, construction, and textile segments. The expanding manufacturing sector in the region has increased the demand for specialty fluids, coatings, and paints, which has led to a rise in the consumption of specialty fluids. Thus, such developments are expected to drive the growth of the global specialty fluids market during the forecast period.

Significant Specialty Fluids Market Trends

Increasing investments in CSP technology is the primary trend shaping market growth. The increasing focus on sustainability has increased innovations in CSP technology. CSP technology generates solar power by using mirrors or lenses to concentrate solar energy or thermal energy into a small area. The light is converted into heat to produce electricity. Moreover, many countries and organizations are investing heavily in the development of CSP technology.

For instance, in October 2023, the Gujarat government approved more than USD 300 million for the development and construction of solar power plants. The project combines the concentrated solar power and photovoltaic project and will have a total capacity of 600-800 MW. Thus, increasing innovations in CSP technology is the market trends and analysis that will lead to a rise in the demand for specialty fluids, which, in turn, will boost the growth of the global specialty fluids market during the forecast period.

Major Specialty Fluids Market Challenge

Volatility in crude oil prices is a challenge that affects market growth. Each petrochemical feedstock has a unique correlation with oil prices, and this correlation is influenced by the supply and demand of feedstock, the manufacturing process, and the part of the world where the product is produced. Fluctuations in petrochemical feedstock prices adversely affect the demand for specialty fluids. Fluctuations in global crude oil prices affect the profitability and performance of oil and gas E&P companies.

Moreover, low crude oil prices can lead to the cancelation or rescheduling of oil and gas E&P projects. In addition, the plunge in global crude oil and natural gas prices has impeded the entire upstream oil and gas sector during the past decade. Several oil and gas E&P projects were canceled or postponed across the world. Hence, fluctuation in global crude oil prices is one of the major factors that will hinder market growth during the forecast period.

Specialty Fluids Market Segmentation by Product, Type, and Geography

Specialty Fluids Market Product Analysis

The market share growth by the aerosols segment will be significant during the forecast period. The rise in demand for aerosols is driving the demand for specialty fluids in aerosol applications. The growth in the use of aerosols is majorly driven by the increasing consumption of personal care products, such as deodorants, shaving creams, hair sprays, and body sprays. Aerosols are colloidal systems of solid or liquid particles that are suspended in a gas.

Get a glance at the market contribution of the End User segment Request Free Sample

The aerosols segment accounted for USD 10.81 billion in 2018. Specialty fluids are used as replacements for hydrochlorofluorocarbons (HCFCs) in aerosols. They meet the diverse requirements of formulators and are environment-friendly and ozone-safe. Specialty fluids are used in aerosols as they exhibit superior cleaning properties. In addition, they are nonflammable and less toxic. These fluids contain a low concentration of volatile organic compounds (VOCs), exhibit quick drying, and are compatible with most materials. These benefits have increased the use of specialty fluids in aerosols, driving market growth during the forecast period.

Specialty Fluids Market Type Analysis

In 2023, the hydrofluorocarbon (HFC) segment led the global specialty fluids and is expected to retain its dominant position throughout the forecast period. HFC-32 is a versatile aerosol refrigerant suitable for air-conditioning and heat pump applications. HFC-152a is viable in mobile vehicle air-conditioning applications. Hydrofluorocarbon-152a is suitable for commercial refrigeration applications, chillers, and industrial refrigeration. The global HVAC industry is expected to grow during the forecast period due to the exponential growth in the global construction sector. Furthermore, market players are providing cost advantages and maintenance and support services for a limited period to end-users, which is encouraging these end-users to opt for HVAC equipment. This is expected to increase the adoption of HFC as an aerosol refrigerant, which, in turn, is anticipated to drive the growth of the HFC segment of the market in focus during the forecast period.

Specialty Fluids Market Region Analysis

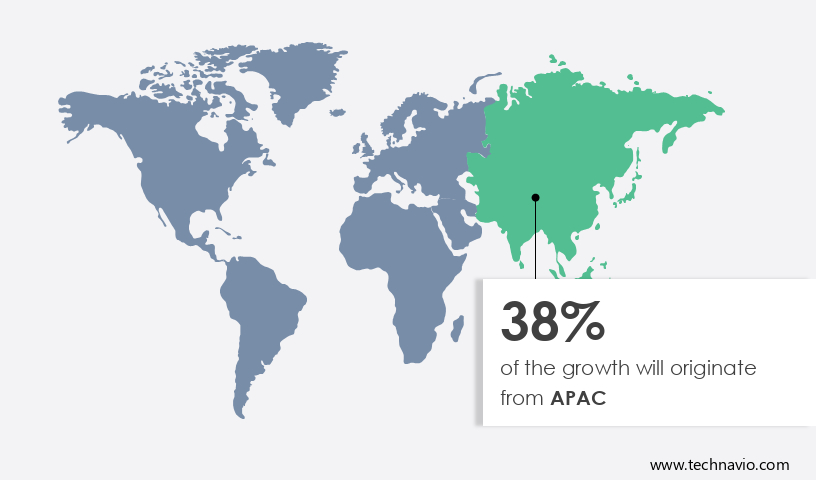

APAC is estimated to contribute 38% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

Increasing sales of fragrance products, hair care products, and skincare products are driving the demand for aerosols in APAC, which, in turn, is driving the specialty fluids market research and growth in the region. Growth in automotive manufacturing is promoting the use of automotive spray paints across APAC, leading to increased sales of specialty fluids. China held the largest share of the specialty fluids market in the region.

Furthermore, with the expansion of the oil and gas industry and government initiatives for foreign investments in the region, the specialty fluids market in the region is registering growth. Moreover, E&P activities involve the extensive use of specialty fluids; hence, the increasing investments in the oil and gas industry and the rise in the number of E&P and mining activities will fuel the demand for specialty fluids in the region. Thereby propelling the growth of the regional specialty fluids market during the forecast period.

Key Specialty Fluids Market Companies

Companies are implementing various strategies by analyzing factors such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product or service launches, to enhance their presence in the market.

- Baker Hughes Co.: The company offers specialty fluids such as TekPlug fluid loss control system, Super InsulGel insulating packer fluid, and others.

The report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

Baker Hughes Co., BASF SE, BP Plc, Clariant International Ltd., Compagnie de Saint Gobain, ConocoPhillips Co., DuPont de Nemours Inc., Exxon Mobil Corp., Kluber Lubrication Munchen SE and Co. KG, Mitsubishi Chemical Group Corp., Momentive Performance Materials Inc., PTT Public Co. Ltd., Quaker Chemical Corp., Repsol SA, Shell plc, Solvay SA, TETRA Technologies Inc., The Chemours Co., and Valvoline Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Segment Overview

The specialty fluids market growth and forecasting by revenue at global, regional & country levels and analyzes the market growth and trends from 2018-2028.

- Product Outlook

- Aerosols

- Precision cleaning

- Coolants

- Carrier fluids

- Others

- Type Outlook

- Hydrofluorocarbon (HFC)

- Hydrofluoroolefin (HFO)

- Polyethylene glycol

- Alcohol ethoxylates

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- South America

- Chile

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

|

Specialty Fluids Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

186 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Market forecasting period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.68% |

|

Market Growth 2024-2028 |

USD 9.11 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.22 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 38% |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Baker Hughes Co., BASF SE, BP Plc, Clariant International Ltd., Compagnie de Saint Gobain, ConocoPhillips Co., DuPont de Nemours Inc., Exxon Mobil Corp., Kluber Lubrication Munchen SE and Co. KG, Mitsubishi Chemical Group Corp., Momentive Performance Materials Inc., PTT Public Co. Ltd., Quaker Chemical Corp., Repsol SA, Shell plc, Solvay SA, TETRA Technologies Inc., The Chemours Co., and Valvoline Inc. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and market analysis and report for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Specialty Fluids Market Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the growth of the market forecast between 2024 and 2028

- Precise estimation of the market size and its contribution to the market in focus on the parent market

- Accurate predictions about upcoming trends and changes in consumer behavior

- The market growth analysis across APAC, North America, Europe, South America, and Middle East and Africa

- A thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of specialty fluids market companies

We can help! Our analysts can customize this report to meet your requirements. Get in touch

RIA -

RIA -