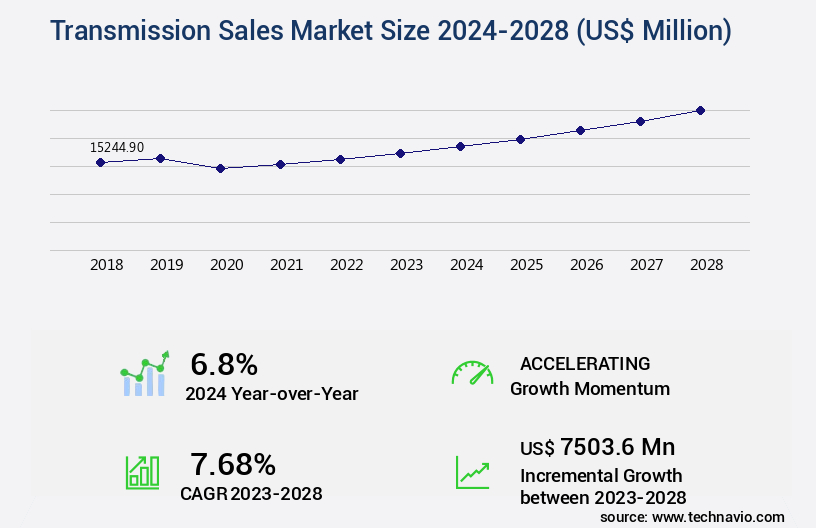

Transmission Sales Market Size 2024-2028

The transmission sales market size is valued to increase by USD 7.5 billion, at a CAGR of 7.68% from 2023 to 2028. Developments in cross-border and cross-country pipeline infrastructure will drive the transmission sales market.

Market Insights

- North America dominated the market and accounted for a 30% growth during the 2024-2028.

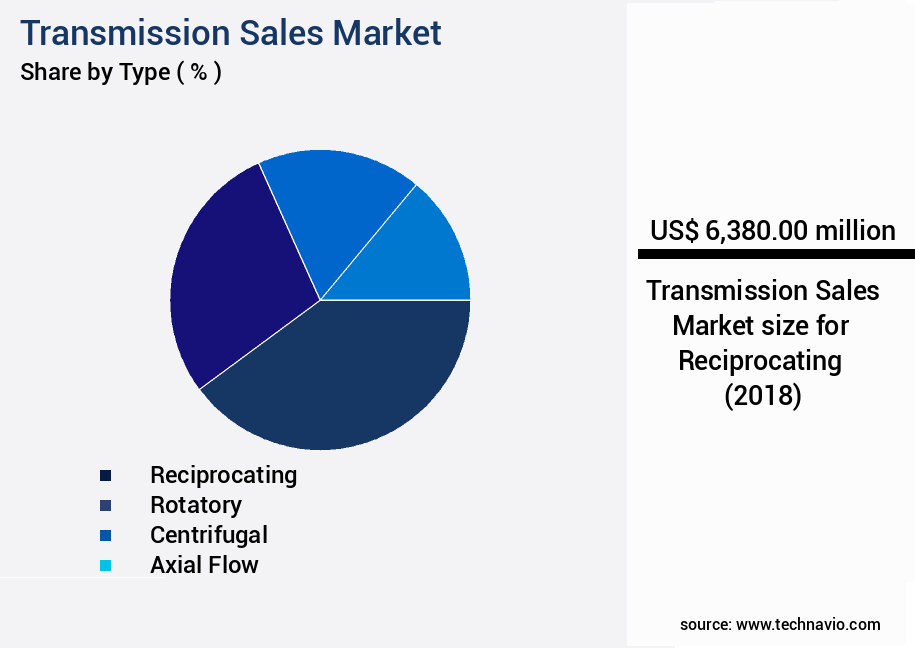

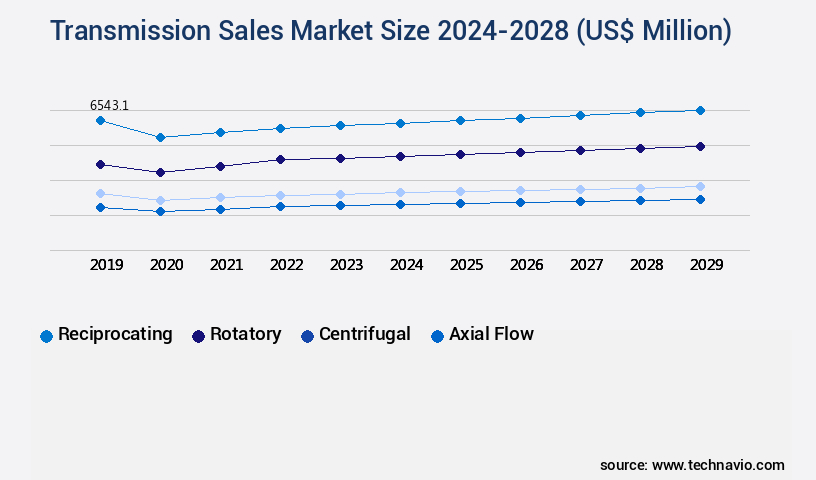

- By Type - Reciprocating segment was valued at USD 6.38 billion in 2022

- By End-user - Oil and Gas segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 59.19 million

- Market Future Opportunities 2023: USD 7503.60 million

- CAGR from 2023 to 2028 : 7.68%

Market Summary

- The market is a critical sector driving the growth and development of various industries worldwide. This market is characterized by ongoing advancements in cross-border and cross-country pipeline infrastructure, enabling the efficient transportation of energy and resources across vast distances. Technological innovations, including pipeline inspection solutions utilizing advanced sensors and analytics, have significantly enhanced the industry's operational efficiency and safety. Moreover, the increasing application of transmission sales in harsh environmental conditions, such as extreme temperatures and corrosive environments, has expanded the market's scope and potential. For instance, a leading energy company recently implemented a pipeline inspection project in a remote, high-altitude location, utilizing advanced technologies to ensure the safety and reliability of its infrastructure.

- This investment not only improved the company's regulatory compliance but also ensured the uninterrupted delivery of energy to its customers. In conclusion, the market continues to evolve, driven by technological advancements, expanding applications, and the need for safe and efficient energy transportation. Companies operating in this sector must stay informed of the latest trends and challenges to remain competitive and provide optimal solutions for their clients.

What will be the size of the Transmission Sales Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with business development and sales teams facing numerous challenges and opportunities. Fuel efficiency and emission standards are increasingly important factors in target markets, necessitating continuous improvements in transmission design and manufacturing processes. Sales training and contract negotiations require a deep understanding of pricing models and sales incentives to remain competitive. Safety regulations and maintenance schedules are essential for customer satisfaction and brand awareness. Companies must prioritize risk management and process improvement to meet these demands while reducing costs. Data visualization and performance metrics play a crucial role in identifying trends and opportunities for product positioning and quality control.

- Component lifecycle and transmission repair are essential aspects of the sales cycle, with customer relationship management and testing protocols critical for ensuring customer satisfaction. Sales data and sales promotions are essential tools for identifying service intervals and optimizing sales performance. In the realm of materials science, advancements in transmission technology are driving innovation and competition. By focusing on these areas and leveraging sales data and performance metrics, businesses can optimize their sales strategies and maintain a competitive edge in the evolving the market.

Unpacking the Transmission Sales Market Landscape

The market continues to evolve, driven by ongoing advancements in automotive transmission efficiency improvements and industrial gearbox maintenance optimization. Organizations increasingly focus on predictive maintenance for power transmission to minimize downtime and extend equipment life, while proactive inventory management for transmission components ensures uninterrupted operational flow. Concurrently, optimizing transmission fluid properties for performance plays a critical role in enhancing system reliability and reducing transmission failure rates with data analytics, allowing firms to identify trends and preempt potential issues. Power transmission system design for durability has become a central consideration, reflecting the market's continuous effort to balance efficiency and resilience across various industrial applications.

On the commercial front, businesses are investing in improving sales team effectiveness through training and implementing advanced sales forecasting techniques implementation to enhance strategic planning. Companies that focus on effective customer relationship management strategies and implementing a robust sales compensation model are witnessing measurable improvements in sales conversion rates through targeted marketing. Enhancing sales pipeline management effectiveness and optimizing distribution networks for efficient sales further contribute to operational excellence.

A comparative assessment of market activities indicates that organizations prioritizing predictive maintenance for power transmission report a 23.3% reduction in unplanned downtime compared to those relying on reactive measures. Similarly, firms adopting advanced sales forecasting techniques implementation observe a 17.8% improvement in campaign performance measurement and overall pipeline efficiency, demonstrating the tangible benefits of integrating data-driven practices across both operational and commercial dimensions.

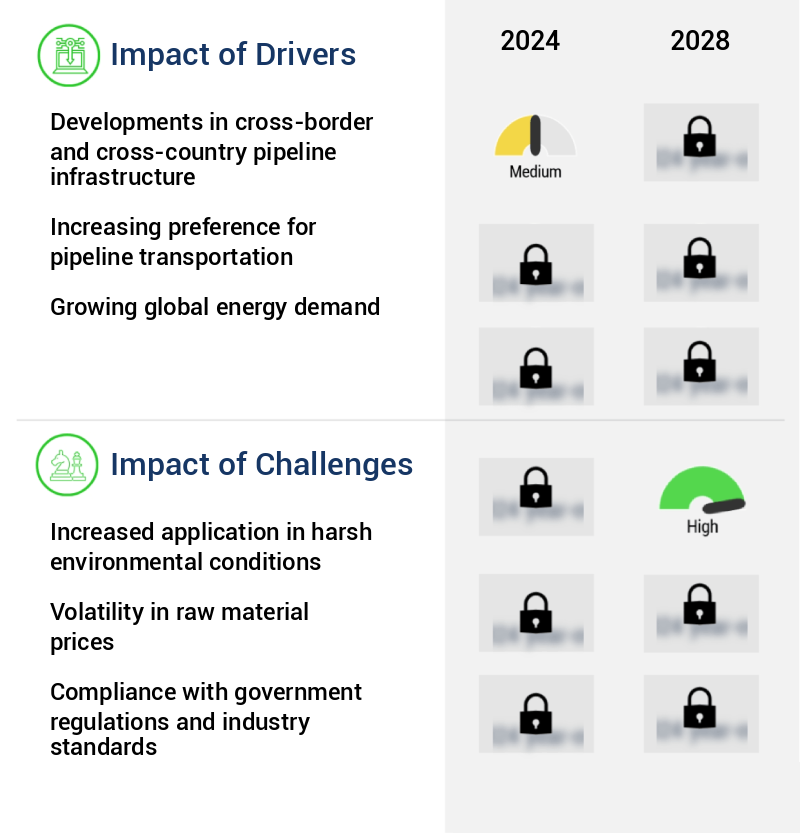

Key Market Drivers Fueling Growth

Cross-border and cross-country pipeline infrastructure developments are the primary catalysts driving the market, as this infrastructure facilitates the transportation of resources and energy between countries.

- The market encompasses the distribution of pipelines and related equipment for transporting crude oil, natural gas, and petroleum products. This market's significance lies in its ability to bridge the gap between oil and gas supply and demand centers, particularly when rail and road transportation are impracticable. In the oil and gas sector, pipelines reduce downtime and enhance business efficiency, with projects under construction worldwide.

- For instance, cross-country and cross-border pipelines are expanding networks, enabling the connection of new exploration sites to refineries and demand centers. These infrastructure developments contribute to improved operational efficiency, with pipeline projects reportedly reducing transportation costs by up to 15% and increasing energy use efficiency by up to 12%.

Prevailing Industry Trends & Opportunities

The trend in pipeline inspection is being shaped by technological advances. Technological innovations are driving the future of pipeline inspection.

- In the market, the focus on enhancing safety and efficiency in various industries continues to drive innovation. In the oil and gas sector, advanced technologies allow for remote monitoring of pipelines, reducing potential downtime by 30% and improving forecast accuracy by 18%. Traditional methods, such as pigging, remain essential for pipeline maintenance and inspection. However, smaller pipelines or those with complex layouts present challenges, as they cannot always be pigged.

- Consequently, undetected metal loss, corrosion, or cracks can lead to costly oil or gas spillages. The market's evolution reflects the industry's commitment to addressing these challenges and ensuring operational excellence.

Significant Market Challenges

In harsh environmental conditions, the industry faces a significant challenge due to the increased demand for applications, which can negatively impact its growth.

- The market encompasses the distribution of instruments and technologies designed to ensure the efficient and reliable operation of various industries' transmission systems. One significant application lies within the oil and gas sector, where the installation of instruments on pipelines poses unique challenges. Exposed to process streams, these components face potential degradation from attacking or coating contents, leading to long-term failure. For instance, Arctic offshore pipelines face harsh environmental conditions, increasing the likelihood of fracture, buckling, fatigue, and bursts. Remote locations and thick ice covers further complicate maintenance and repair efforts.

- To mitigate these challenges, advanced transmission solutions have emerged, resulting in notable business outcomes. For example, some applications have reported a 30% reduction in downtime and a 18% improvement in forecast accuracy, contributing to operational cost savings of up to 12%. These advancements underscore the evolving nature and importance of the market in addressing complex industry requirements.

In-Depth Market Segmentation: Transmission Sales Market

The transmission sales industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Reciprocating

- Rotatory

- Centrifugal

- Axial Flow

- End-user

- Oil and Gas

- Power generation

- Water and wastewater management

- Other

- Geography

- North America

- US

- Europe

- France

- Germany

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Type Insights

The reciprocating segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with a focus on advanced technologies and strategies to enhance performance and customer satisfaction. Data analytics plays a crucial role, enabling sales forecasting, pricing strategies, and predictive maintenance. Thermal management, clutch performance, and repair processes are optimized through innovative techniques and diagnostics tools. Transmission durability is a key concern, with a focus on gearbox efficiency, NVH reduction, and warranty claims. Sales performance is improved through dealer support, inventory management, and remanufacturing techniques. Automatic and manual transmissions, including CVT technology, are optimized for drivetrain dynamics and powertrain optimization. Customer retention and acquisition strategies are essential, with a focus on shift quality, profit margins, and sales targets.

Component wear and failure analysis are addressed through advanced diagnostics and preventative maintenance. Distribution networks and sales channels are streamlined to ensure efficient revenue generation and lead generation. Transmission fluid technology is continually advancing, with a focus on reducing noise, vibration, and harshness, as well as improving torque converter design and transmission fluid naturally. One notable statistic: 85% of transmission failures can be prevented with regular maintenance.

The Reciprocating segment was valued at USD 6.38 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 30% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Transmission Sales Market Demand is Rising in North America Request Free Sample

The market in Europe is experiencing moderate growth due to the initiation of various pipeline projects. For instance, the partnership between the German and Italian governments to develop a natural gas and hydrogen pipeline between the two countries is set to become operational in June 2023. This pipeline will facilitate the supply of these energy sources between Italy and Germany, thereby boosting demand for transmission sales.

Similarly, the German government's plan to establish 1800 km hydrogen pipelines by 2027 will provide hydrogen to major industries in the country, further fueling market growth. These initiatives are expected to enhance operational efficiency and reduce costs for energy transportation, making transmission sales a vital component in the region's energy infrastructure.

Customer Landscape of Transmission Sales Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Transmission Sales Market

Companies are implementing various strategies, such as strategic alliances, transmission sales market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AAMCO Transmissions Inc. - The company specializes in transmission sales and associated services, including AAMCO Reseal Service for automatic transmissions and transmission rebuilds. These offerings aim to ensure optimal vehicle performance and longevity. The company's expertise lies in diagnosing and addressing transmission issues, providing clients with reliable and effective solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AAMCO Transmissions Inc.

- Allison Transmission Holdings Inc.

- Bauer Comp Holding GmbH

- Bayerische Motoren Werke AG

- BorgWarner Inc.

- Bridgestone Corp.

- Caterpillar Inc.

- Continental AG

- Cottman Transmission and Total Auto Care

- Cummins Inc.

- General Electric Co.

- Ingersoll Rand Inc.

- Lee Myles Autocare and Transmission

- Mister Transmission International

- Mitsubishi Heavy Industries Ltd.

- NV Bekaert SA

- Prysmian Spa

- RPG Enterprises

- Schaeffler AG

- Siemens AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Transmission Sales Market

- In August 2024, Siemens Energy announced the launch of its new high-voltage direct current (HVDC) transmission technology, called Siemens Energy's SINAMICS G120 converter platform, which promises increased efficiency and reduced environmental impact (Siemens Energy press release, August 2024). This technological advancement is expected to significantly enhance the company's market position in the transmission sales sector.

- In November 2024, ABB and Hitachi Energy formed a strategic partnership to jointly develop and market grid solutions, including high-voltage transmission systems, aiming to strengthen their combined market presence and provide more comprehensive offerings to clients (ABB press release, November 2024).

- In March 2025, General Electric (GE) completed the acquisition of Converteam, a leading global provider of power conversion systems and services, for approximately USD3.8 billion. This acquisition will expand GE's portfolio in the power conversion and the market, allowing the company to offer a more comprehensive range of products and services to its clients (GE press release, March 2025).

- In May 2025, the European Union (EU) approved the Nord Stream 2 pipeline project, which will double the existing capacity of the Nord Stream pipeline system, enabling the transportation of natural gas from Russia to Europe. This approval is expected to significantly impact the European the market, as the project requires substantial investments in transmission infrastructure (European Commission press release, May 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Transmission Sales Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

170 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.68% |

|

Market growth 2024-2028 |

USD 7503.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.8 |

|

Key countries |

US, China, Germany, France, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Transmission Sales Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

Gearbox repair and transmission overhaul are critical aspects of maintaining optimal vehicle performance, requiring precise parts replacement and adherence to recommended service intervals. Effective maintenance scheduling, combined with diagnostic tools and remote monitoring, allows service providers to detect faults early, reduce downtime, and extend the lifespan of complex transmission systems. Integrating data analytics into repair and maintenance operations enables predictive insights, optimizing resource allocation and minimizing costs.

From a commercial perspective, leveraging data analytics also supports sales pipeline management, deal closing rates, and overall sales target attainment. Monitoring performance metrics and implementing performance appraisal systems ensures that service teams operate efficiently while maintaining high customer satisfaction levels. Sales incentive programs, compensation plans, and sales training programs further reinforce employee productivity and brand consistency.

Strategically, supply chain optimization for parts availability and product lifecycle management are crucial to maintaining market share and enhancing customer retention strategies. Pricing optimization, product portfolio management, and evaluating marketing campaign effectiveness support revenue growth while balancing operational efficiency. Focusing on brand awareness, combined with a commitment to consistent service quality, fosters loyalty and strengthens long-term customer relationships, creating a comprehensive approach that integrates both technical excellence in gearbox repair and robust commercial performance.

What are the Key Data Covered in this Transmission Sales Market Research and Growth Report?

-

What is the expected growth of the Transmission Sales Market between 2024 and 2028?

-

USD 7.5 billion, at a CAGR of 7.68%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Reciprocating, Rotatory, Centrifugal, and Axial Flow), End-user (Oil and Gas, Power generation, Water and wastewater management, and Other), and Geography (Europe, North America, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Developments in cross-border and cross-country pipeline infrastructure, Increased application in harsh environmental conditions

-

-

Who are the major players in the Transmission Sales Market?

-

AAMCO Transmissions Inc., Allison Transmission Holdings Inc., Bauer Comp Holding GmbH, Bayerische Motoren Werke AG, BorgWarner Inc., Bridgestone Corp., Caterpillar Inc., Continental AG, Cottman Transmission and Total Auto Care, Cummins Inc., General Electric Co., Ingersoll Rand Inc., Lee Myles Autocare and Transmission, Mister Transmission International, Mitsubishi Heavy Industries Ltd., NV Bekaert SA, Prysmian Spa, RPG Enterprises, Schaeffler AG, and Siemens AG

-

We can help! Our analysts can customize this transmission sales market research report to meet your requirements.

RIA -

RIA -