Utility Locator Market Size 2026-2030

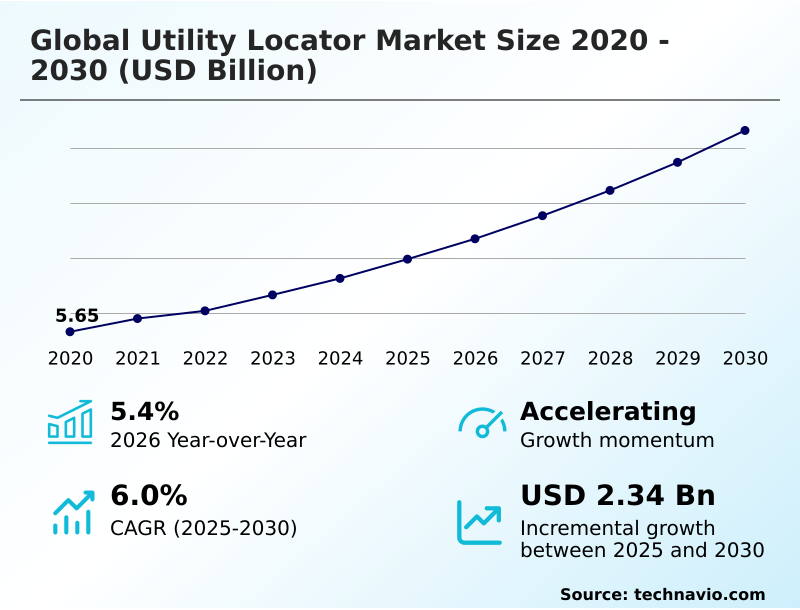

The utility locator market size is valued to increase by USD 2.34 billion, at a CAGR of 6% from 2025 to 2030. Surge in global infrastructure spending and modernization mandates will drive the utility locator market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 34.1% growth during the forecast period.

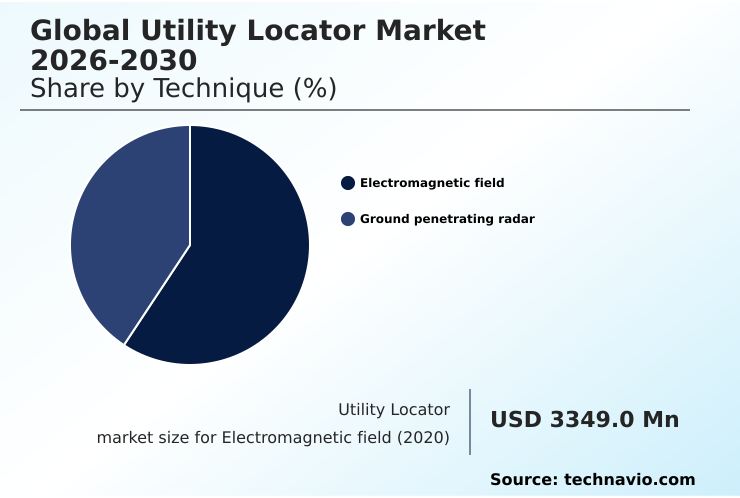

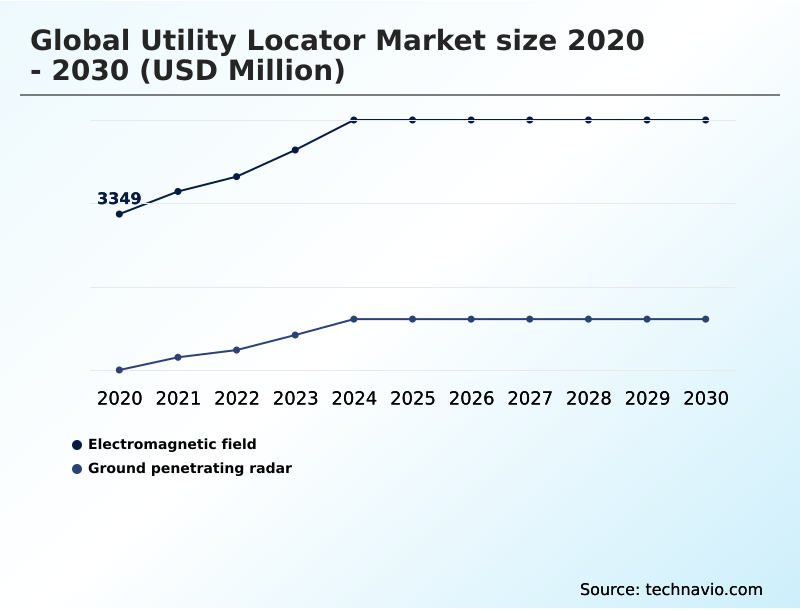

- By Technique - Electromagnetic field segment was valued at USD 3.98 billion in 2024

- By End-user - Oil and gas segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.66 billion

- Market Future Opportunities: USD 2.34 billion

- CAGR from 2025 to 2030 : 6%

Market Summary

- The utility locator market is undergoing a significant transformation, driven by massive infrastructure modernization and stringent damage prevention mandates. Core activities are shifting from simple detection to sophisticated digital subsurface mapping. The integration of high-precision GNSS receivers and cloud connectivity in intelligent utility devices enables the creation of detailed subsurface digital twins.

- This technology is critical in scenarios like urban renewal, where contractors must navigate a complex web of undocumented pipes and cables. Using a locator with advanced signal processing algorithms for real-time data collection can reduce utility strikes by more than 25%, preventing costly project delays and service disruptions.

- This move toward comprehensive subsurface characterization and GIS and BIM integration is redefining the value of locating technology. While the proliferation of non-conductive utilities and a shortage of skilled operators present ongoing hurdles, the push for digital construction workflows and proactive asset management ensures sustained demand for more advanced, data-centric locating solutions.

What will be the Size of the Utility Locator Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Utility Locator Market Segmented?

The utility locator industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Technique

- Electromagnetic field

- Ground penetrating radar

- End-user

- Oil and gas

- Electricity

- Transportation

- Others

- Type

- Metallic utilities

- Non-metallic utilities

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Technique Insights

The electromagnetic field segment is estimated to witness significant growth during the forecast period.

The electromagnetic field technique remains the foundational method for the utility locator market, highly effective for conductive infrastructure. This segment's stability is driven by its cost-efficiency and performance in detecting metallic utilities.

Technology has evolved beyond basic detection, incorporating multi-frequency transmitters and advanced signal processing algorithms to improve performance in congested areas. A key advancement is the integration of georeferencing capabilities to create as-built digital maps.

This supports proactive asset management by enabling the creation of an auditable record of locate activities. Advanced diagnostic capabilities now allow for the assessment of pipeline coating health, with some systems improving fault detection accuracy by over 20%.

This evolution transforms the locator into a critical tool for digital construction workflows, supporting pipeline integrity management.

The Electromagnetic field segment was valued at USD 3.98 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 34.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Utility Locator Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the utility locator market is characterized by a dichotomy between mature and emerging regions. North America and Europe lead in the adoption of advanced systems, driven by stringent regulations and a focus on subsurface utility engineering.

In these markets, the use of locators with geospatial coordinates and direct connection capabilities has reduced utility strikes by an estimated 20%.

Conversely, the APAC region is the fastest-growing market, propelled by massive infrastructure projects where damage prevention technology is becoming critical.

While mature markets focus on asset integrity management and digital subsurface mapping, APAC's growth is fueled by new construction, where adoption of even basic electromagnetic induction tools can improve project efficiency by over 15%.

This regional divergence creates opportunities for a wide range of products, from high-end multi-sensor platforms to rugged, cost-effective devices.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

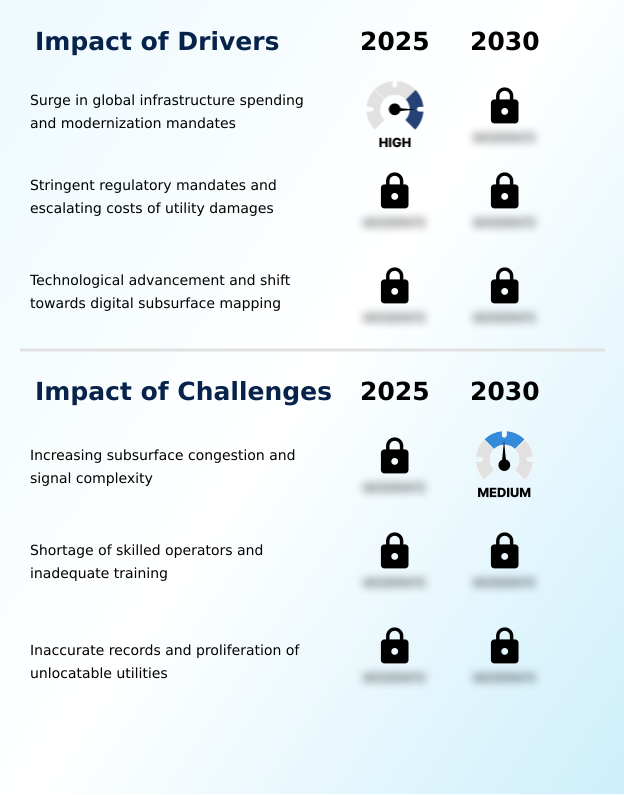

- The global utility locator market 2026-2030 is shaped by several interconnected factors. A clear understanding of the global utility locator market 2026-2030 key drivers, such as massive infrastructure spending and stricter safety regulations, is essential for strategic planning. The impact of regulations on utility locator market is profound, mandating pre-excavation surveys and compelling investment in more accurate technology.

- This directly influences the future of utility locator technology, which is trending toward integrated systems that combine electromagnetic detection with advanced GPR. An analysis of the global utility locator market 2026-2030 segmentation reveals distinct needs; for instance, the energy sector's requirements differ significantly from those of telecommunications.

- Key challenges in subsurface utility mapping, including signal interference and the presence of unrecorded lines, persist. The role of GPR in utility locating is expanding to address the proliferation of non-metallic pipes, a segment that grows nearly twice as fast as the metallic utility segment.

- Effectively navigating these dynamics requires a focus on innovation and adapting to a data-centric operational model.

What are the key market drivers leading to the rise in the adoption of Utility Locator Industry?

- The market is propelled by a significant surge in global infrastructure spending and the implementation of modernization mandates worldwide.

- Global infrastructure modernization is a primary catalyst for the utility locator market, creating sustained demand for damage prevention technology. Government initiatives mandating the expansion of fiber optic and energy networks necessitate precise digital subsurface mapping.

- The adoption of subsurface utility engineering practices has proven to reduce project delays by up to 25%. Technological advancements, particularly the integration of high-precision GNSS receivers and automated signal processing, are transforming locators into essential tools for real-time data collection.

- This enables more effective pipeline integrity management and assessment, enhancing safety and operational efficiency. The market is also driven by the need for accurate non-conductive utility detection in increasingly congested subterranean environments.

What are the market trends shaping the Utility Locator Industry?

- A defining market trend is the integration of locators into comprehensive digital workflows, driving the development of subsurface digital twins.

- The utility locator market is increasingly defined by the adoption of intelligent utility devices and a move toward comprehensive subsurface characterization. A key trend is the integration of locators into digital construction workflows, where remote data synchronization enables field data to be instantly available for office-based analysis.

- This focus on GIS and BIM integration is driving demand for advanced diagnostic capabilities that support proactive asset management. The use of multi-sensor platforms combining electromagnetic locators with high-density array systems improves the detection of non-conductive utilities by over 40%. These systems produce an auditable record of locate activities, which is critical for compliance and reduces liability.

- This shift enhances underground utility verification and supports more efficient project planning.

What challenges does the Utility Locator Industry face during its growth?

- The industry faces a key challenge from increasing subsurface congestion and the resulting signal complexity, which can impede locator performance.

- A significant market challenge stems from increasingly congested subsurface environments, which leads to signal interference and complicates the use of tracer wire. This complexity is compounded by a shortage of skilled technicians capable of interpreting ambiguous signals from multi-frequency transmitters, leading to locating errors in an estimated 15% of complex urban surveys.

- While directional guidance and other software enhancements help, they cannot fully replace operator expertise. The prevalence of inaccurate records and unlocatable non-conductive utilities forces reliance on ground penetrating radar, which requires significant training and is not effective in all soil types.

- This gap between technological capability and field application highlights a critical need for improved training and more intuitive user interfaces with features such as passive locating.

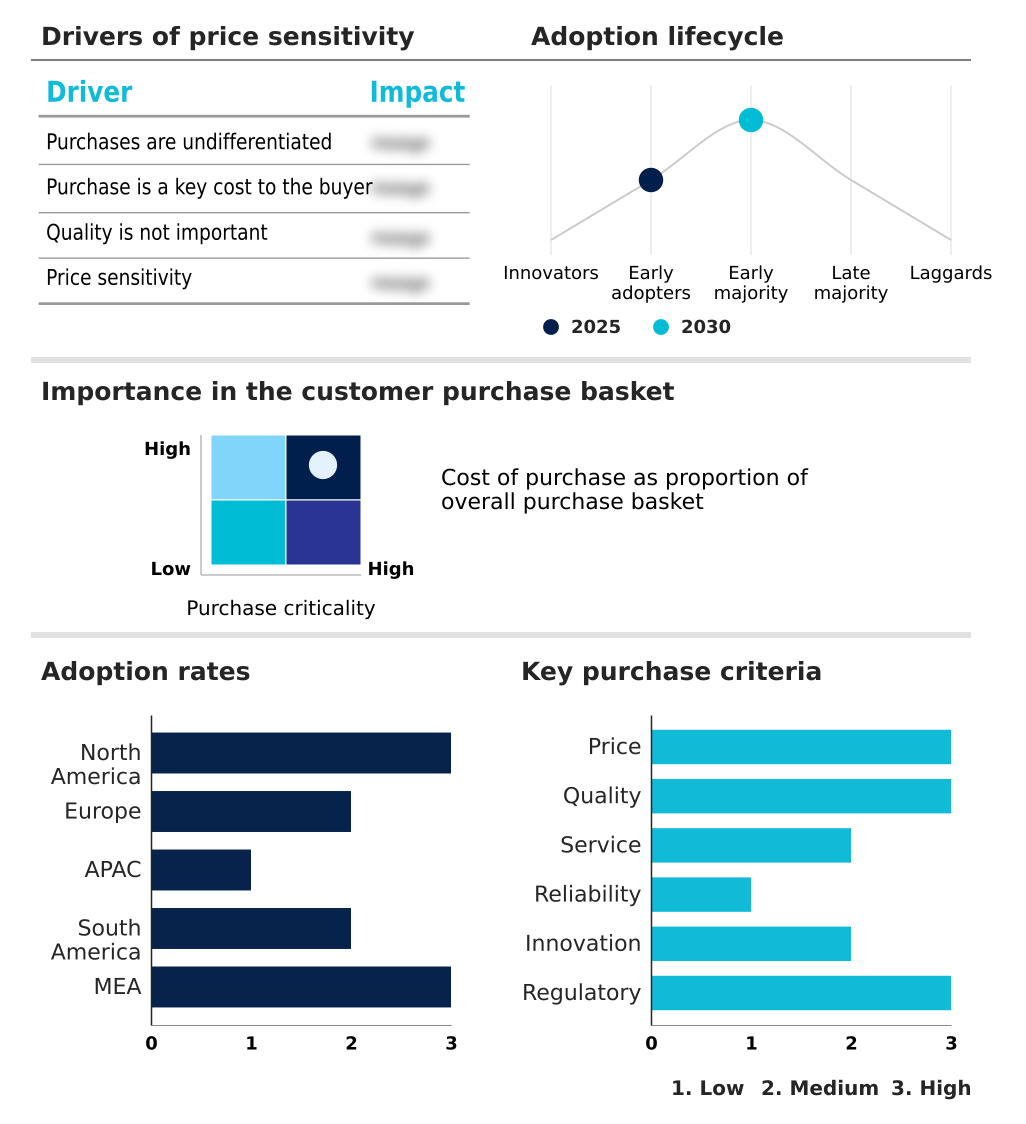

Exclusive Technavio Analysis on Customer Landscape

The utility locator market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the utility locator market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Utility Locator Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, utility locator market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - Offerings are centered on advanced damage prevention technology, providing industrial-grade systems for precise pipe and cable locating.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- Berntsen International Inc.

- Emerson Electric Co.

- Eos Positioning Systems Inc.

- Geophysical Survey Systems Inc.

- Guideline Geo AB

- Hexagon AB

- Leica Geosystems AG

- MidAmerican Technology Inc.

- Radiodetection Ltd.

- RYCOM Instruments Inc.

- SPX Technologies Inc.

- STC TECHNO AC LLC

- SubSurface Instruments Inc.

- The Toro Co.

- Vermeer Corp.

- Vivax Metrotech Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Utility locator market

- In August, 2024, a major technology firm and a leading locator manufacturer announced a strategic partnership to integrate augmented reality overlays into locator displays, providing technicians with real-time visual guidance in the field.

- In November, 2024, a European standards body announced the adoption of stricter subsurface survey mandates, similar to PAS 128, for two additional member states, increasing the requirement for high-accuracy locating and data reporting.

- In February, 2025, a prominent vendor launched a new locator series featuring onboard AI for real-time signal interpretation and interference filtering, designed to reduce operator-dependent errors during complex locates.

- In May, 2025, a consortium of infrastructure and technology companies in the APAC region secured funding for a large-scale project to develop a unified subsurface digital twin for a major capital city, mandating the use of locators with cloud connectivity.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Utility Locator Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6% |

| Market growth 2026-2030 | USD 2341.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.4% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The utility locator market is advancing beyond simple detection, becoming integral to digital asset management and risk mitigation strategies. The industry's evolution is marked by the integration of technologies such as GNSS receivers and cloud connectivity, enabling the creation of precise as-built digital maps.

- These subsurface digital twins are no longer a niche concept but a core component of modern infrastructure projects, supporting boardroom decisions on capital expenditure and compliance. The use of locators featuring advanced signal processing algorithms and fault-finding features has demonstrated the ability to reduce diagnostic time by over 30% in congested urban environments.

- This shift from reactive damage prevention to proactive asset integrity management, using tools for assessing cathodic protection systems and pipeline coating health, is critical. The technology, including electromagnetic induction and ground penetrating radar, now provides a higher level of data integrity, with features like passive locating and direct connection ensuring both safety and accuracy.

- This evolution underscores the instrument's role in creating verifiable geospatial coordinates and radargram data for long-term planning.

What are the Key Data Covered in this Utility Locator Market Research and Growth Report?

-

What is the expected growth of the Utility Locator Market between 2026 and 2030?

-

USD 2.34 billion, at a CAGR of 6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technique (Electromagnetic field, and Ground penetrating radar), End-user (Oil and gas, Electricity, Transportation, and Others), Type (Metallic utilities, and Non-metallic utilities) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Surge in global infrastructure spending and modernization mandates, Increasing subsurface congestion and signal complexity

-

-

Who are the major players in the Utility Locator Market?

-

3M Co., Berntsen International Inc., Emerson Electric Co., Eos Positioning Systems Inc., Geophysical Survey Systems Inc., Guideline Geo AB, Hexagon AB, Leica Geosystems AG, MidAmerican Technology Inc., Radiodetection Ltd., RYCOM Instruments Inc., SPX Technologies Inc., STC TECHNO AC LLC, SubSurface Instruments Inc., The Toro Co., Vermeer Corp. and Vivax Metrotech Corp.

-

Market Research Insights

- Market dynamics are shaped by a definitive shift toward digital construction workflows and intelligent utility devices. The adoption of subsurface utility engineering practices, which improve project planning accuracy by over 40%, underscores the demand for advanced locating solutions. Integrating real-time data collection with GIS and BIM integration reduces rework costs associated with utility strikes by up to 30%.

- The emphasis on damage prevention technology is driven by regulations and the high cost of repairs. Furthermore, non-conductive utility detection using multi-sensor platforms is becoming essential. This evolution supports proactive asset management and enhances subsurface characterization, justifying investment in higher-performance equipment that provides a clear and auditable record of locate activities.

We can help! Our analysts can customize this utility locator market research report to meet your requirements.

RIA -

RIA -