Vacuum Insulation Panels Market Size 2026-2030

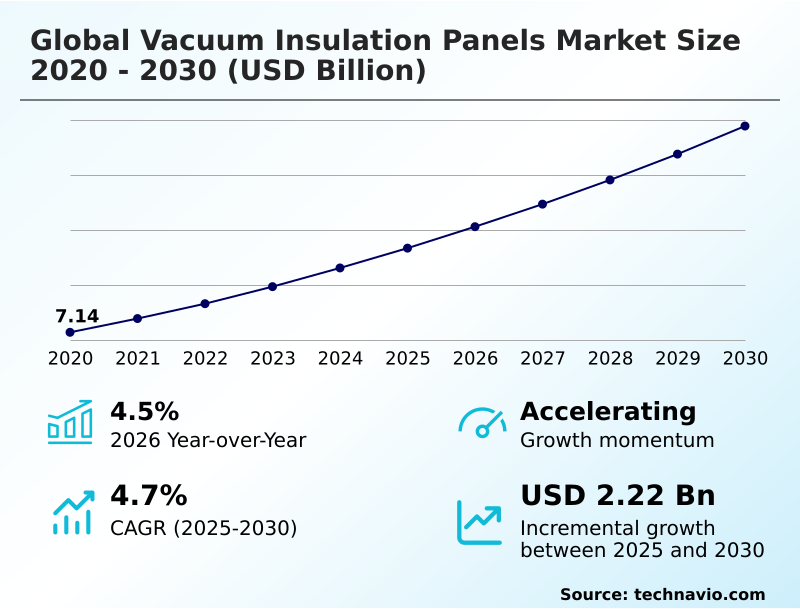

The vacuum insulation panels market size is valued to increase by USD 2.22 billion, at a CAGR of 4.7% from 2025 to 2030. Increased urbanization and investment in infrastructure development will drive the vacuum insulation panels market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 38.1% growth during the forecast period.

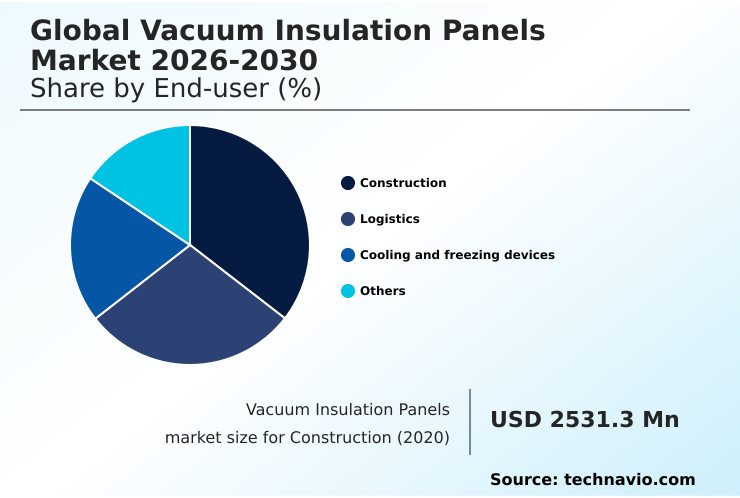

- By End-user - Construction segment was valued at USD 3.01 billion in 2024

- By Material - Silica segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.75 billion

- Market Future Opportunities: USD 2.22 billion

- CAGR from 2025 to 2030 : 4.7%

Market Summary

- The vacuum insulation panels market is advancing rapidly, driven by a convergence of stringent energy regulations and the need for high-performance thermal management in space-constrained applications. These panels, which leverage a microporous insulation structure under vacuum to achieve an exceptionally low thermal conductivity value, are becoming indispensable in sectors such as construction, logistics, and appliance manufacturing.

- Key drivers include the push for zero-energy building design and the operational cost savings associated with superior building envelope efficiency. In logistics, a major pharmaceutical distributor could leverage temperature-controlled packaging with integrated panels to guarantee the hermetic seal integrity of vaccine shipments across fluctuating climates, ensuring compliance and preventing costly product loss.

- A prominent trend is the development of hybrid core materials, combining the benefits of fumed silica core structures with cost-effective alternatives to broaden application viability. The market is also addressing durability challenges like thermal cycling stress and moisture vapor transmission by engineering more robust high-barrier multilayer films.

- This focus on innovation is expanding the use of panels from niche applications to mainstream solutions, where both thermal performance and spatial efficiency are paramount.

What will be the Size of the Vacuum Insulation Panels Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Vacuum Insulation Panels Market Segmented?

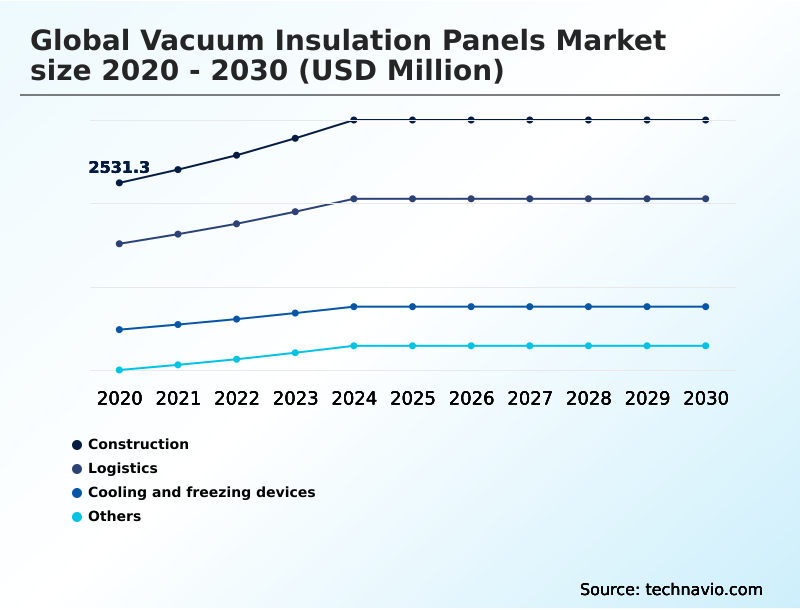

The vacuum insulation panels industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Construction

- Logistics

- Cooling and freezing devices

- Others

- Material

- Silica

- Fiberglass

- Others

- Product

- Flat

- Special shape

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By End-user Insights

The construction segment is estimated to witness significant growth during the forecast period.

The construction segment leverages vacuum insulation panels to meet stringent energy efficiency regulations, particularly for sustainable building. In high-density urban projects, these panels provide a competitive advantage by maximizing usable floor area without compromising thermal performance.

The low thermal conductivity value and long panel service life of units produced with advanced vacuum sealing technology make them ideal for permanent structures. The microporous insulation structure resists core material compression and limits moisture vapor transmission.

This is crucial for achieving nearly zero-energy building standards. Applications are expanding from building envelopes to specialized uses like medical device insulation and electronic component cooling.

The manufacturing process, often requiring a clean room environment and high-vacuum chamber, supports custom panel sizing to fit complex architectural designs, while a growing focus on recyclable insulation materials aligns with circular economy goals.

Their adoption in retrofits has been shown to improve a building's thermal envelope efficiency by over 30%.

The Construction segment was valued at USD 3.01 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 38.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Vacuum Insulation Panels Market Demand is Rising in APAC Get Free Sample

The geographic landscape is characterized by varied regional priorities. In Europe, the focus is on building retrofit insulation using premium fumed silica core panels that meet stringent codes for energy-efficient building materials, ensuring long-term thermal stability.

North America sees high demand in cold chain logistics insulation, where maintaining hermetic seal integrity in insulated shipping solutions is paramount.

The APAC region, a hub for appliance manufacturing, heavily utilizes cost-effective fiberglass core material to achieve high R-value per inch, with some leading manufacturers reporting a 99.8% success rate in their VIP manufacturing process.

Emerging applications like battery thermal management for electric vehicles are creating new opportunities globally. Advanced designs now mitigate the panel edge effect, improving overall thermal performance by up to 10% in integrated systems.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the industry involves a deep cost-benefit analysis of vacuum insulation panels, especially when comparing silica vs fiberglass vip cores for different applications. For high-rise construction, thin insulation solutions for high-rise buildings are essential, with passive house design with vacuum insulation becoming a benchmark for energy efficiency. Simultaneously, integrating vips in modular construction streamlines building processes.

- A critical aspect is reducing thermal bridging with vip solutions, though installers face challenges of installing vacuum insulation panels. In the automotive sector, vacuum insulation for electric vehicle batteries is a key innovation area. For existing structures, vip thermal performance in building retrofits offers a path to modernization.

- The logistics sector is improving cold chain logistics with vips, using vip solutions for temperature-sensitive shipping to protect goods. A thorough lifecycle assessment of vacuum insulation panels is influencing material selection, considering the durability of vacuum insulation in appliances and medical equipment, such as vacuum insulation panels in medical refrigerators, where consistent energy savings with vip in refrigeration is critical.

- The manufacturing process of vacuum insulation panels, protected by advanced barrier films for vip longevity, determines overall quality. Research into best core materials for vacuum insulation, including exploring aerogel-based vacuum insulation panel benefits, continues to drive innovation, especially for specialized uses like vacuum insulation panels for cryogenic storage, where performance is an order of magnitude higher than conventional methods.

What are the key market drivers leading to the rise in the adoption of Vacuum Insulation Panels Industry?

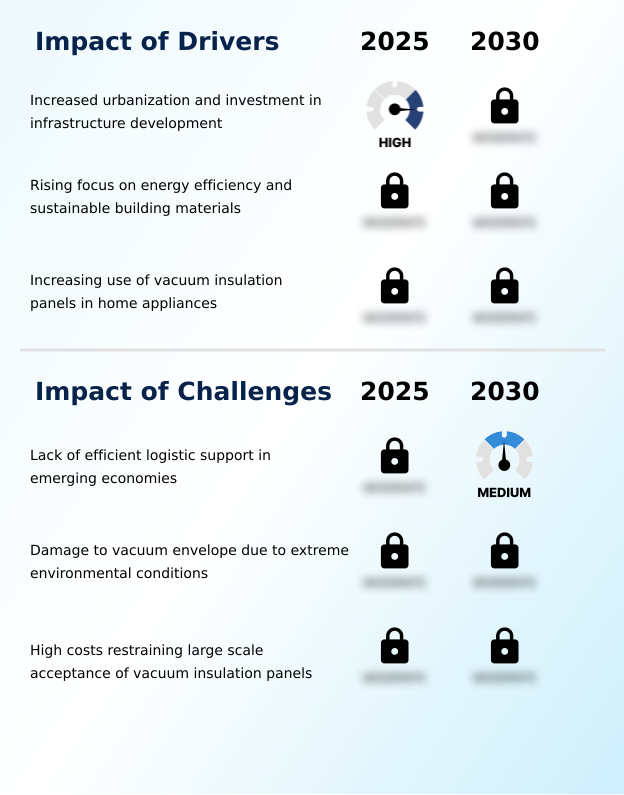

- Increased urbanization and significant investments in infrastructure development are key drivers for the market's growth.

- The push toward sustainability is a major driver, with regulations mandating passive house standards and zero-energy building design.

- Achieving this level of building envelope efficiency relies on sustainable insulation materials that provide high R-value insulation and enable effective thermal bridge mitigation.

- In practice, implementing these materials improves a building's effective thermal resistance by over 40% compared to conventional insulation. Beyond construction, demand for passive building insulation is growing.

- The logistics sector requires robust refrigerated transport insulation and specialized pharmaceutical shipping containers that maintain temperature stability for 120+ hours without power.

- Furthermore, critical infrastructure like industrial pipeline insulation and data center cooling solutions are adopting these technologies to reduce operational energy consumption by up to 20%.

What are the market trends shaping the Vacuum Insulation Panels Industry?

- A key market trend involves integrating advanced core materials like aerogel and polyurethane, which enhances thermal performance and diversifies insulation solutions.

- The integration of advanced core materials is reshaping the market, with aerogel-infused cores and polyurethane-based cores offering new balances between cost and performance. These innovations, alongside developments in nano-porous materials and open-cell foam cores, facilitate architectural insulation design for complex geometries, a critical factor in modular construction insulation.

- This evolution supports a broader range of thin-profile insulation panels and advanced thermal management solutions. Rigorous thermal performance testing shows that new panel designs with improved getter material integration can extend service life by up to 15%.

- This is particularly vital for cryogenic insulation systems and enhancing appliance energy efficiency, where some next-generation refrigerators demonstrate a 25% improvement in thermal resistance over previous models.

What challenges does the Vacuum Insulation Panels Industry face during its growth?

- A key challenge affecting industry growth is the lack of efficient logistical support for fragile insulation components in emerging economies.

- Key challenges center on long-term durability, as high-performance thermal insulation can suffer from vacuum level degradation over time. Issues such as barrier film delamination and heat-sealed seam fatigue, exacerbated by thermal cycling stress, impact the reliability of space-saving insulation solutions. The effectiveness of high-barrier multilayer films is compromised by the inherent gas permeation rate and outgassing characteristics of core materials.

- Panels with inconsistent core material density are 30% more likely to fail prematurely. These vulnerabilities are critical for applications like ultra-low temperature freezers and temperature-controlled packaging, where a single panel failure can result in significant product loss.

- Developing improved structural insulation panels and fire-resistant insulation cores that resist these degradation pathways is essential for broader market acceptance, as failure rates in some harsh environments can reach up to 5% annually.

Exclusive Technavio Analysis on Customer Landscape

The vacuum insulation panels market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the vacuum insulation panels market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Vacuum Insulation Panels Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, vacuum insulation panels market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Avery Dennison Corp. - Delivers advanced vacuum insulation panels, providing high-performance thermal solutions across construction, refrigeration, and logistics sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Avery Dennison Corp.

- BASF SE

- Bridgestone Corp.

- Dow Chemical Co.

- Etex NV

- Evonik Industries AG

- Kingspan Group

- Knauf Digital GmbH

- Morgan Advanced Materials

- OCI Co. Ltd.

- Panasonic Holdings Corp.

- Sealed Air Corp.

- Siltherm

- Thermacor Process Inc.

- Tiger Corp.

- Turna d.o.o.

- va Q tec AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Vacuum insulation panels market

- In February, 2025, Kingspan Group announced a strategic expansion of its vacuum insulation production capacity in Europe to meet the surging demand for its Optim R product line, targeting high-rise residential and commercial refurbishment projects.

- In April, 2025, va Q tec AG revealed a new partnership with a major global airline to deploy a fleet of high-performance thermal containers for distributing temperature-sensitive oncology medications across Southeast Asia.

- In July, 2025, Panasonic Holdings Corp. introduced its newest line of energy-efficient refrigerators for the European market, featuring an integrated vacuum insulation system that achieves a 30% reduction in electricity usage compared to previous models.

- In September, 2025, Morgan Advanced Materials announced a successful test flight of a specialized thermal shield for satellite components that utilized a bespoke fiberglass-based vacuum panel to withstand extreme thermal radiation in space.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Vacuum Insulation Panels Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 305 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.7% |

| Market growth 2026-2030 | USD 2217.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.5% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is defined by a push for greater building envelope efficiency, driven by passive house standards and zero-energy building design. The core of this technology, whether a fumed silica core or a fiberglass core material, relies on a sophisticated VIP manufacturing process conducted in a clean room environment using a high-vacuum chamber.

- Maintaining hermetic seal integrity with high-barrier multilayer films is paramount to prevent vacuum level degradation caused by gas permeation rate and moisture vapor transmission. Advanced vacuum sealing technology mitigates heat-sealed seam fatigue and barrier film delamination from thermal cycling stress.

- Key performance metrics include the thermal conductivity value and R-value per inch, which determine effective thermal resistance and overall panel service life. Innovations in microporous insulation structure, including aerogel-infused cores, polyurethane-based cores, and other nano-porous materials like open-cell foam cores, address the outgassing characteristics and core material compression of evacuated powder insulation.

- These materials, along with getter material integration and phase change materials (PCMs), reduce radiant heat transfer through gas-filled pores. For designers, thermal bridge mitigation and minimizing the panel edge effect through custom panel sizing are critical.

- This focus on performance has led to integrated systems that demonstrate a 30% improvement in thermal efficiency, a decisive factor in boardroom decisions on product strategy and compliance.

What are the Key Data Covered in this Vacuum Insulation Panels Market Research and Growth Report?

-

What is the expected growth of the Vacuum Insulation Panels Market between 2026 and 2030?

-

USD 2.22 billion, at a CAGR of 4.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Construction, Logistics, Cooling and freezing devices, and Others), Material (Silica, Fiberglass, and Others), Product (Flat, and Special shape) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increased urbanization and investment in infrastructure development, Lack of efficient logistic support in emerging economies

-

-

Who are the major players in the Vacuum Insulation Panels Market?

-

Avery Dennison Corp., BASF SE, Bridgestone Corp., Dow Chemical Co., Etex NV, Evonik Industries AG, Kingspan Group, Knauf Digital GmbH, Morgan Advanced Materials, OCI Co. Ltd., Panasonic Holdings Corp., Sealed Air Corp., Siltherm, Thermacor Process Inc., Tiger Corp., Turna d.o.o. and va Q tec AG

-

Market Research Insights

- The market for high-performance thermal insulation is expanding as industries adopt space-saving insulation solutions to meet efficiency and sustainability goals. In construction, energy-efficient building materials are now mandated by codes that have seen a 40% tightening in thermal performance requirements over the last decade.

- The adoption of thin-profile insulation panels allows architects to maximize floor space without compromising on high R-value insulation. In logistics, the use of temperature-controlled packaging and insulated shipping solutions has reduced product spoilage rates by over 75% for certain high-value pharmaceuticals.

- These sustainable insulation materials ensure long-term thermal stability, which is critical for applications ranging from cold chain logistics insulation to refrigerated transport insulation and advanced battery thermal management systems.

We can help! Our analysts can customize this vacuum insulation panels market research report to meet your requirements.

RIA -

RIA -