Vertebral Augmentation Market Size 2024-2028

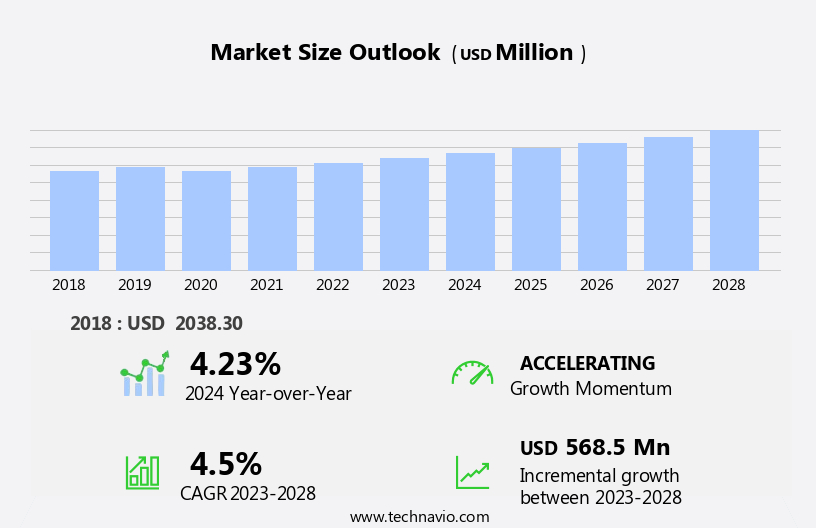

The vertebral augmentation market size is forecast to increase by USD 568.5 billion at a CAGR of 4.5% between 2023 and 2028.

- The market is experiencing significant growth due to several key trends. The aging population in North America is a major driver, as the prevalence of vertebral compression fractures increases with age. Additionally, the availability of reimbursements for these procedures has expanded, making vertebral augmentation more accessible to patients. Furthermore, the availability of alternate medication options for the treatment of vertebral compression fractures has led some patients to opt for minimally invasive surgical procedures like vertebral augmentation instead. These factors are expected to fuel market growth In the coming years. However, challenges such as the high cost of these procedures and the need for specialized training and equipment for surgeons may limit market expansion.

- Despite these challenges, the market is poised for continued growth due to its ability to provide effective pain relief and improve the quality of life for patients suffering from vertebral compression fractures.

What will be the Size of the Vertebral Augmentation Market During the Forecast Period?

- The market encompasses minimally invasive procedures, including vertebroplasty and kyphoplasty, used to treat various spinal conditions such as vertebral compression fractures due to osteoporosis, spinal metastatic tumors, hemangiomas, myelomas, and ankylosing spondylitis. These procedures are commonly performed in hospitals and ambulatory surgery centers to alleviate back pain, reduce physical activity limitations, and improve symptoms of depression, loss of independence, decreased lung capacity, difficulty sleeping, and kyphosis. Vertebroplasty involves injecting bone cement into the vertebral body, while kyphoplasty utilizes a balloon to restore vertebral height before cement injection. The market's growth is driven by the increasing prevalence of spinal compression fractures and the rising demand for minimally invasive alternatives to open spine surgery.

- The PVA (polyvinyl alcohol) POD system and KhPhon bone cement are popular technologies used in vertebral augmentation procedures.

How is this Vertebral Augmentation Industry segmented and which is the largest segment?

The vertebral augmentation industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

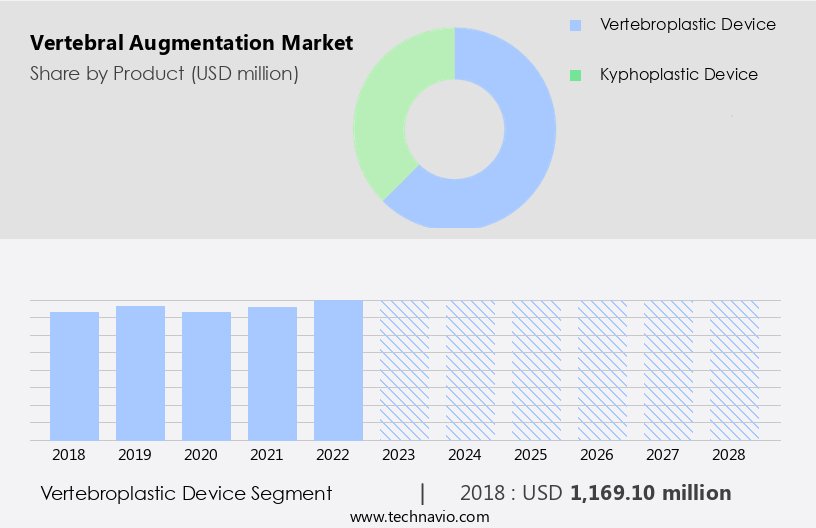

- Product

- Vertebroplastic device

- Kyphoplastic device

- Geography

- North America

- US

- Europe

- Germany

- UK

- Asia

- China

- Japan

- Rest of World (ROW)

- North America

By Product Insights

- The vertebroplastic device segment is estimated to witness significant growth during the forecast period.

Vertebral augmentation procedures, including vertebroplasty and kyphoplasty, are minimally invasive treatments for spinal compression fractures caused by osteoporosis, spinal tumors, or spinal disorders such as ankylosing spondylitis. These procedures involve the use of vertebral augmentation devices, such as vertebroplastic and kyphoplastic devices, to deliver biocompatible cement or balloons into the affected vertebra. The procedures are typically performed on an outpatient basis in hospitals and ambulatory surgery centers. Vertebroplasty, a type of vertebral augmentation, involves injecting cement into the vertebral body through a small incision to stabilize the fracture and alleviate pain. Kyphoplasty, another type, uses a balloon to create a cavity In the vertebral body and then fills it with cement to restore vertebral height and correct kyphosis.

Percutaneous kyphoplasty (PKP) is a variation of kyphoplasty that uses imaging techniques to guide the procedure. The aging population, with its increased prevalence of spinal disorders and degenerative conditions, is driving the demand for these minimally invasive treatments. Vertebroplasty and kyphoplasty offer significant benefits over open spine surgery, including reduced physical activity, improved patient outcomes, and faster recovery times. Conditions such as osteoporosis, vertebral compression fractures, spinal metastatic tumors, hemangiomas, myelomas, and ankylosing spondylitis can be treated effectively with these procedures. Consumer awareness and healthcare infrastructure development have also contributed to the growth of the market. Minimally invasive techniques, such as percutaneous vertebroplasty and balloon kyphoplasty, have gained popularity due to their patient-specific implants and biocompatible materials.

Imaging techniques, such as CT scans and X-rays, are used to diagnose and guide the treatment process, ensuring accurate and effective results.

Get a glance at the Vertebral Augmentation Industry report of share of various segments Request Free Sample

The Vertebroplastic device segment was valued at USD 1.17 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

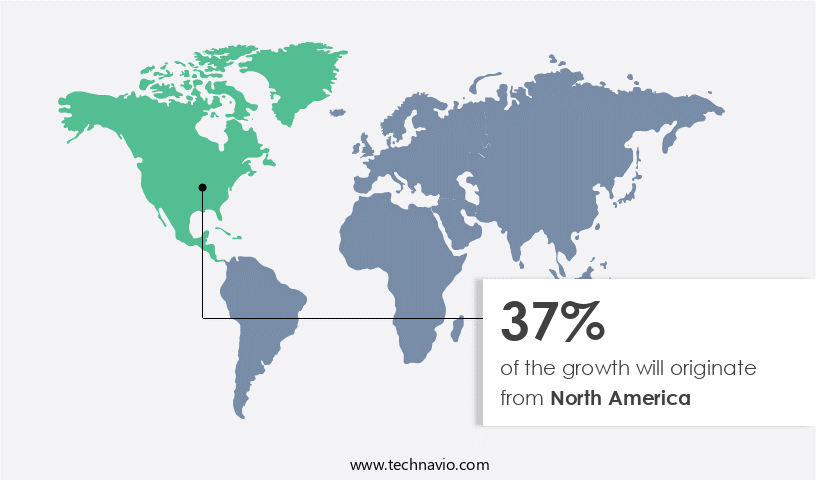

- North America is estimated to contribute 37% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American market dominates the global vertebral augmentation industry due to a high prevalence of spinal disorders, including osteoporosis, and well-established healthcare infrastructure. In the US alone, approximately 1.2 million spinal surgeries are performed annually, encompassing procedures like spinal fusion, decompression, and discectomy. Factors such as an aging population, increased consumer awareness, and advancements in minimally invasive techniques, including percutaneous vertebroplasty and balloon kyphoplasty, further fuel market growth. Technological innovations, like patient-specific implants and biocompatible materials, contribute to the industry's expansion. Government initiatives and healthcare infrastructure development In the region also support market growth. Spinal disorders, such as vertebral compression fractures, spinal metastatic tumors, hemangiomas, myelomas, ankylosing spondylitis, and degenerative discs, continue to drive demand for vertebral augmentation procedures.

These minimally invasive techniques offer benefits such as reduced back pain, improved physical activity, decreased depression, and increased independence, making them increasingly popular among patients.

Market Dynamics

Our vertebral augmentation market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Vertebral Augmentation Industry?

Rising geriatric population is the key driver of the market.

- The market is experiencing significant growth due to the increasing prevalence of spinal disorders, particularly In the geriatric population. By 2050, it is projected that the number of Americans aged 65 and above will reach one-fifth of the total population, and those aged 85 and above will account for 4%, a tenfold increase from 1950. Age-related declines in musculoskeletal function, neurological function, and bone flexibility make injuries more common in this demographic. As a result, the number of vertebral compression fractures due to osteoporosis, spinal metastatic tumors, hemangiomas, myelomas, ankylosing spondylitis, and other spine-related disorders is increasing. Vertebroplasty and Kyphoplasty, minimally invasive vertebral augmentation procedures, have gained popularity due to their ability to reduce back pain, improve physical activity levels, alleviate depression, and restore lost independence.

- These procedures involve the use of Vertebroplastic and Kyphoplastic Devices, such as the PVA Pod System and Khphon bone cement, to stabilize and restore the height of the vertebral body. Imaging techniques, such as CT and X-ray, are used to guide the insertion of the Vertebroplasty needle or Kyphoplasty balloon. Minimally invasive techniques, including Percutaneous Vertebroplasty and Balloon Kyphoplasty, have gained popularity due to their ability to minimize patient discomfort and reduce hospital stays. The market for these procedures is expected to continue growing due to consumer awareness, healthcare infrastructure development, and the increasing prevalence of spinal disorders.

What are the market trends shaping the Vertebral Augmentation Industry?

Availability of reimbursements is the upcoming market trend.

- The market encompasses the use of advanced devices, including Vertebroplastic and Kyphoplastic Devices, for the treatment of various spinal disorders. These minimally invasive procedures, which include Kyphoplasty and Vertebroplasty, are commonly employed for conditions such as Osteoporosis, Vertebral Compression Fractures, Spinal Metastatic Tumors, Hemangiomas, Myelomas, Ankylosing Spondylitis, and other Spine Related Disorders. The aging and geriatric population, who are more susceptible to these conditions, are the primary consumers of these treatments. The adoption of these procedures is on the rise due to the numerous benefits they offer. They provide relief from back pain, reduced physical activity, depression, loss of independence, decreased lung capacity, and difficulty sleeping.

- Additionally, they help correct Kyphosis and Spinal Compression Fractures, which can lead to severe complications if left untreated. The use of minimally invasive techniques, such as Percutaneous Kyphoplasty (PKP) and Percutaneous Vertebroplasty, has gained popularity due to their ability to minimize the risk of complications and reduce hospital stays. These procedures utilize Patient-Specific Implants, Biocompatible Materials, and Cement Augmentation Technology, ensuring optimal patient outcomes. Imaging Techniques play a crucial role In the successful execution of these procedures, enabling accurate diagnosis and treatment planning. The healthcare infrastructure development, coupled with increasing consumer awareness, has led to the expansion of Ambulatory Surgery Centers and Trauma Centers, offering these treatments to a larger patient population.

- The favorable reimbursement scenario In the US healthcare system, driven by initiatives like the Affordable Care Act, has resulted in increased adoption of Vertebral Augmentation Procedures. These treatments have proven to be effective alternatives to traditional Spinal Surgeries, such as Open Spine Surgery. The use of advanced technologies, like the PVA Pod System and Khphon bone cement, in Balloon Kyphoplasty Vertebroplasty, further enhances the efficacy and safety of these procedures.

What challenges does the Vertebral Augmentation Industry face during its growth?

Availability of alternate medication options is a key challenge affecting the industry growth.

- The market encompasses the use of Vertebroplastic and Kyphoplastic Devices for the treatment of various spinal conditions, including Vertebral Compression Fractures due to Osteoporosis, Spinal Metastatic Tumors, Hemangiomas, Myelomas, Ankylosing Spondylitis, and Kyphosis. Vertebroplasty and Kyphoplasty, minimally invasive procedures, are gaining popularity due to their ability to alleviate back pain, reduce physical activity limitations, and improve patient quality of life. These procedures involve the injection of cement augmentation material, such as Khphon bone cement, using the PVA Pod System or Balloon Kyphoplasty Vertebroplasty. Despite the benefits of Vertebral Augmentation Procedures, the market faces competition from opioid analgesic medications, which have been traditionally used for pain management.

- The affordability and non-invasive nature of medications contribute to their widespread use. Furthermore, the development of novel drug delivery systems and enhanced medications negatively impacts the demand for Vertebral Augmentation Devices. Interventional paIn therapies, such as non-narcotic treatments for chronic pain, are increasingly popular. For instance, epidural steroid injections have seen a surge in demand, with a growth rate of over 120% between 2000 and 2008, and continue to grow in double digits. Hospitals and Ambulatory Surgery Centers offer these procedures, along with Open Spine Surgeries, to cater to the growing demand for minimally invasive techniques. The aging and geriatric population, with a higher prevalence of Spine Related Disorders, such as Degenerative Discs and Spinal Stenosis, fuels the demand for Minimally Invasive Surgeries.

- Consumer Awareness and Healthcare Infrastructure Development also contribute to the market growth. Imaging Techniques aid In the accurate diagnosis and treatment planning, further increasing the adoption of Vertebral Augmentation Procedures. The market for Vertebral Augmentation Devices is driven by the need for Biocompatible Materials and Patient-Specific Implants, which ensure optimal safety and efficacy. Cement Augmentation Technology continues to evolve, with advancements in imaging techniques and materials, to cater to the diverse needs of the patient population.

Exclusive Customer Landscape

The vertebral augmentation market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the vertebral augmentation market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, vertebral augmentation market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Becton Dickinson and Co. - The company provides a vertebral augmentation system, AVAmax, featuring 8 and 10 gauge vertebral balloons. This system is designed to deliver bone cement to vertebral bodies, aiding In the treatment of vertebral compression fractures. The system's balloons facilitate the creation of a cavity, ensuring precise placement of the bone cement. The use of vertebral augmentation can help restore vertebral body height and improve overall spinal stability. This minimally invasive procedure offers an alternative to traditional surgical options for patients suffering from osteoporotic fractures.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Becton Dickinson and Co.

- Benvenue Medical Inc.

- BIOPSYBELL Srl

- G21 Srl

- Globus Medical Inc.

- IZI Medical Products

- Johnson and Johnson Services Inc.

- Medtronic Plc

- Merit Medical Systems Inc.

- RONTIS AG

- Spine Wave Inc.

- Stryker Corp.

- Tecres Spa

- Tsunami Medical Srl

- ZAVATION

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Vertebral augmentation is a minimally invasive procedure used to treat various spinal conditions, including vertebral compression fractures, spinal metastatic tumors, hemangiomas, myelomas, and ankylosing spondylitis. This process involves the injection of biocompatible materials into the vertebral body to restore height and stability, thereby alleviating back pain and improving physical function. Two common types of vertebral augmentation procedures are kyphoplasty and vertebroplasty. Kyphoplasty utilizes a balloon to create a cavity In the vertebral body, which is then filled with cement. Vertebroplasty, on the other hand, involves the direct injection of cement into the vertebral body without the use of a balloon.

Both procedures are carried out on an outpatient basis in hospitals and ambulatory surgery centers. The aging and geriatric population is a significant driver of the market. With the increasing prevalence of spinal disorders, such as osteoporosis, degenerative discs, and spinal stenosis, the demand for minimally invasive procedures like vertebral augmentation is on the rise. These procedures offer several advantages over traditional open spine surgery, including reduced physical activity, shorter hospital stays, and quicker recovery times. The use of patient-specific implants and advanced cement augmentation technology has further boosted the popularity of vertebral augmentation. Imaging techniques, such as CT scans and X-rays, are employed to create customized implants that fit perfectly into the vertebral body, ensuring optimal results.

Moreover, the use of biocompatible materials In the cement ensures that the body does not reject the implant. Consumer awareness and healthcare infrastructure development are also contributing to the growth of the market. As more people become aware of the benefits of minimally invasive procedures, the demand for vertebral augmentation is expected to increase. Furthermore, the expansion of healthcare infrastructure, particularly in developing countries, is creating new opportunities for market growth. Despite the numerous advantages of vertebral augmentation, there are still challenges that need to be addressed. These include the high cost of the procedure and the lack of reimbursement policies in some regions.

Additionally, there is a need for more clinical studies to establish the long-term safety and efficacy of vertebral augmentation. In conclusion, the market is poised for significant growth due to the increasing prevalence of spinal disorders, the aging population, and the advantages offered by minimally invasive procedures. The use of patient-specific implants, advanced cement augmentation technology, and biocompatible materials is further driving the market. However, challenges such as high costs and lack of reimbursement policies need to be addressed to ensure the widespread adoption of vertebral augmentation.

|

Vertebral Augmentation Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

134 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 568.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Key countries |

US, Germany, UK, Japan, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Vertebral Augmentation Market Research and Growth Report?

- CAGR of the Vertebral Augmentation industry during the forecast period

- Detailed information on factors that will drive the Vertebral Augmentation growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the vertebral augmentation market growth of industry companies

We can help! Our analysts can customize this vertebral augmentation market research report to meet your requirements.

RIA -

RIA -