Viral Vectors Market Size 2024-2028

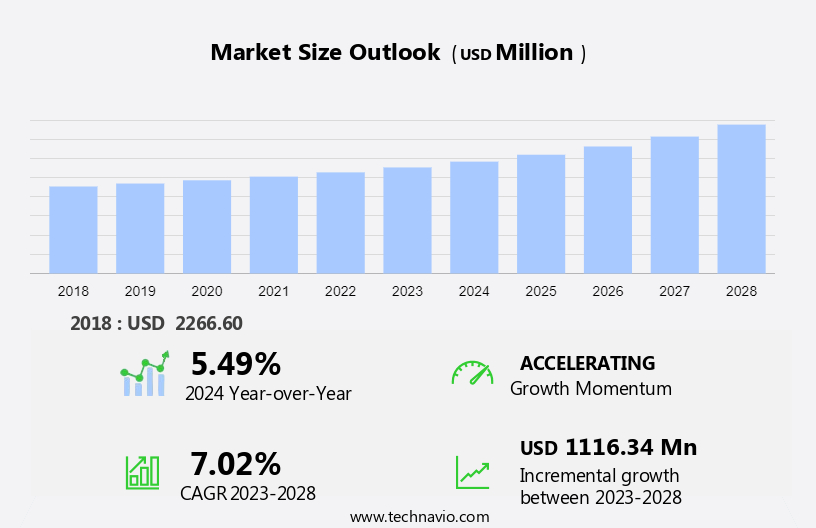

The global viral vectors market size is estimated to grow by USD 1.17 billion, at a CAGR of 7.02% between 2023 and 2028. The market growth and forecasting report also includes an in-depth analysis of drivers, trends, and challenges. Our report examines historical data from 2018-2022, besides analyzing the current market scenario.

Recent discoveries have improved the understanding of viral molecular biology and genetics, which has enabled the use of viruses as vaccine platforms and as potential agents for the treatment of cancer and infectious diseases, such as HIV. Viral vectors are considered a feasible option to deliver vaccine antigens and to specifically target and kill disease-causing agents due to their ability to effectively induce both humoral and cell-mediated immune responses. Recombinant viral vector vaccines have the potential to be used as therapeutic vaccines, as they enable an intracellular antigen expression and induce a strong cytotoxic T lymphocyte response, which results in the elimination of virus-infected cells. The advantages have led to an increase in their use in the development of vaccines. Thus, the increasing use of viral vectors for the development of vaccines to treat various diseases will drive the growth of the market during the forecast period.

What will be the size of the Market During the Forecast Period?

To learn more about this report, Download Report Sample

Segmentation by Application, End-user, and Geography Analysis

The market is experiencing rapid expansion driven by the surge in vaccine development and the growing demand for viral vector vaccines. As vaccine candidates progress through clinical and preclinical development, emphasis is placed on replication-deficient chimp adenovirus vector like ChAdOx1 and replication-incompetent human adenovirus vector for their efficacy. With increasing focus on treating genetic disorders and target diseases, funding for gene therapy development continues to rise, fueling innovations in viral vector manufacturing. The market is further bolstered by advancements in cell and gene therapy manufacturing and therapeutic genes, paving the way for novel therapeutic approaches and in vivo gene transfers.

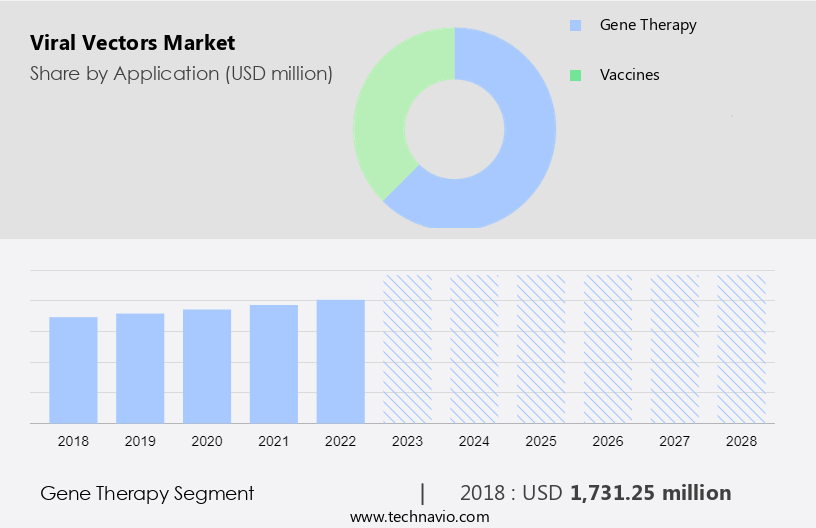

Application Analysis

The market share growth by the gene therapy segment will be significant during the forecast period. In recent years, viral vectors have emerged as potent tools in gene therapy, offering effective delivery mechanisms for treating various disorders. Adenovirus vectors, known for their broad host cell range and immunogenicity, show promise in cancer therapy, including oncolytic adenoviruses targeting pancreatic cancer.

Get a glance at the market contribution of various segments Download PDF Sample

The gene therapy segment was valued at USD 1.73 billion in 2018. Adeno-associated virus vectors, heralded for their low immunogenicity and integration capacity, are utilized in therapies like ZOLGENSMA for spinal muscular atrophy. Herpes simplex virus vectors exhibit efficacy in treating conditions like diabetic neuropathy. Retrovirus and lentivirus vectors enable long-term gene transfer, with lentiviral vector therapy like ZYNTEGLO proving effective for beta-thalassemia. Ongoing clinical trials, including those targeting Alzheimer's disease and HIV-1 infection, underscore the growing demand and potential of viral vector-based gene therapies, driving market growth.

End-user Analysis

The pharmaceutical and biotechnology companies segment will account for the largest share of this segment.?Pharmaceutical companies and biotechnology companies are exploring the use of viral vectors for genome therapy and cell therapy to develop personalized therapies tailored to individual patients' genetic profiles, with the aim of improving treatment outcomes and minimizing adverse effects. Furthermore, owing to the increasing prevalence of chronic diseases and rising disease burden globally, the development of efficient therapies such as gene therapy and personalized medicine is increasing. The US FDA stated that over 800 active investigational new drug applications were filed in the same year. Thus, the growing focus of pharmaceutical and biotechnology companies on the use of advanced therapies is driving the growth of the segment of the market during the forecast period.

The academic and research institutes segment is also showing steady growth. Academic institutes and research institutes are among the key users of viral vector products. Growing investments in genomic research and growing interest in editing the DNA of genes and the genome during basic and applied research, which is aimed at advancing the understanding of human stem cells, human cells and tissues, diseases, genetic pathways and gene expressions, and regenerative medicines, are driving the demand across the academic institutes and research laboratories segment. Further, growing investments and initiatives in basic and applied research activities that focus on improving the understanding of genetic connections between hereditary diseases and cancer are driving the use of viral vectors. Thus, such factors will drive market growth during the forecast period.

Regional Analysis

For more insights about the market share of various regions Download PDF Sample now!

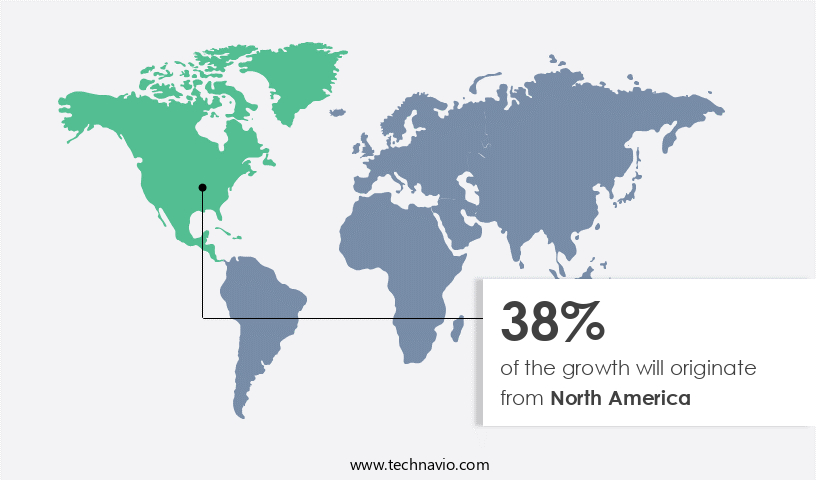

North America is estimated to contribute 38% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers will shape the market during the forecast period. North America holds the largest share of the market, primarily due to the strong prevalence of infectious and non-infectious diseases and the increasing investments in developing gene therapies and vaccines in the region. The prevalence of diseases such as cancer, HIV, and genetic and inherited disorders has been increasing at a significant rate in developed countries in the region.

Further, market players have been leading to various developments, such as the expansion of manufacturing facilities and others. In October 2021, Merck announced the opening of its second Carlsbad, California-based facility, significantly expanding its global CDMO footprint. This new facility will more than double the companys existing capacity to support large-scale commercial and industrial manufacturing for viral gene therapy. Thus, the market in North America is expected to grow during the forecast period.

Buy Full Report Now

Key Market Players

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market forecasting report also includes detailed analyses of the competitive landscape of the market and information about 20 market companies, including:

- Batavia Biosciences BV: The company offers viral vector tools such as SCOUT technology and SIDUS platform that combines our biological materials.

Bayer AG, Catalent Inc., Creative Biogene, Danaher Corp., F. Hoffmann La Roche Ltd., FinVector Oy, FUJIFILM Holdings Corp., Institut Merieux, Lonza Group Ltd., Merck KGaA, Novartis AG, Oxford Biomedica Plc, REGENXBIO Inc, Sirion Biotech GmbH, Syncona Ltd., Takara Holdings Inc., Thermo Fisher Scientific Inc., uniQure NV, and Virovek Inc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Dynamics and Customer Landscape

The viral vector manufacturing market is witnessing exponential growth, driven by the escalating demand for doses of viral vectored vaccine worldwide. As a pivotal component in vaccine production, the Global viral vector manufacturing market is characterized by the quest for enhanced effectiveness of viral vectors and optimized dosage delivery. With a focus on eliciting robust immune response against a spectrum of target diseases and disorders, manufacturers are innovating to tailor vectors to specific target cell type. This market evolution is closely intertwined with advancements in cell and gene therapies, emphasizing clinical development, and expanding viral capacity. Additionally, the market is buoyed by the demand for supporting products such as monoclonal antibodies, assay kits, and vector amplification kits to streamline manufacturing processes. Our researchers analyzed the market research and growth data with 2023 as the base year, along with the key market growth analysis, trends, and challenges. A holistic analysis of drivers, trends, and challenges will help companies refine their marketing strategies to gain a competitive advantage.

Key Market Drivers

Increasing use of viral vectors to develop gene therapies is the key factor driving the market. Researchers have found the application of viral vectors encouraging the development of gene therapies to treat and prevent life-threatening diseases in recent years. Significant improvements in vector engineering, delivery, and safety have increased the demand for vector-based therapies. Thus, viral vectors are extensively being used for the development of gene therapies. By addressing genetic disorders at their root, new technologies in the field of cell and gene therapy hold the potential to not only treat symptoms but also to cure diseases. By introducing healthy genes into human cells, adeno-associated viruses (AAVs) have the potential to treat patients with diseases that are currently incurable.

Moreover, the main groups of viral vectors applied for gene therapies include adenoviruses, herpes simplex, retroviruses, lentiviruses, and measles viruses. The most used viral vector in gene therapies is adenoviruses. Adenovirus vectors are considered to generate low pathogenicity and toxicity, and they provide long-term transgene expression through chromosomal integration. Hence, they are extensively used in gene therapies. Thus, increasing use of viral vectors to develop gene therapies is expected to drive the growth of the market during the forecast period.

Significant Market Trends

The rising number of M&A and collaborations is the primary trend shaping the market. Established international market players, such as Thermo Fisher Scientific Inc. (Thermo Fisher Scientific), have been involved in major M&A and collaborations in the last few years. M&A and collaborations are expected to increase the shares of the vendors in the market. Companies also opt for M&A and collaborations as a business strategy to expand their product portfolios and strengthen their businesses.

For instance, in December 2021, Thermo Fisher Scientific announced its completion of the acquisition of PPD Inc. The agreement aimed to increase Thermo Fisher Scientific's revenue through the services clinical development spectrum. The increasing number of M&A and collaboration activities for the development of gene therapies and vaccines are expected to drive the growth of the market during the forecast period.

Major Market Challenges

Risks associated with viral vectors is the major challenge that affects te market. The major concerns associated are the risks of an immune response, inflammation, off-target effects, and insertional mutagenesis. The immune response could limit the effectiveness of viral treatments. It can also result in the creation of antibodies that can prevent a second dosage of the same virus. Inflammation can result in death if an extremely high dosage of adenovirus is administered. Insertional mutagenesis is a major challenge associated with gene therapies.

Moreover, the risk of inserting a gene into a tumor suppressor gene or activating an oncogene is present in vectors that integrate into the unwanted locations of the genome, such as the retrovirus. Besides, discovering the appropriate virus to infect the desired cells is difficult, and there is a risk that the virus could cross the Weismann barrier and infect the germline cells. Furthermore, viruses are susceptible to genetic variations, and incorporation into undesirable sites such as regulatory and oncogenes will have undesirable results. The risk factors associated with viral vectors may limit their usage, which, in turn, can challenge market growth during the forecast period.

Key Market Customer Landscape

The market report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market forecast report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Customer Landscape

Segment Overview

The market research report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "USD Million" for the period 2024-2028, as well as historical data from 2018 - 2022 for the following segments.

- Application Outlook

- Gene therapy

- Vaccines

- End-user Outlook

- Pharmaceutical and biotechnology companies

- Academics and research institutes

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Rest of Europe

- Asia

- China

- India

- Rest of World (ROW)

- Argentina

- Australia

- Brazil

- North America

Market Analyst Overview:

The market is undergoing profound transformation, fueled by advancements in clinical studies and drug delivery approaches for combating infectious and viral diseases. Innovations like self-amplifying messenger RNA vaccine and recombinant viral vectors are reshaping cancer management, offering promising avenues for treating various cancers including brain, skin, liver, colon, breast, and kidney cancer. Academic centers and oncology institutes are at the forefront of pioneering therapies like suicide gene therapy and oncolytic virotherapy, while anti-angiogenesis and therapeutic gene vaccines represent novel approaches in oncology. Radiology and Oncology sectors are leveraging advanced analytics-based models and augmented reality to enhance cancer therapeutics development. As the demand for effective therapeutics grows, the market continues to evolve with the integration of digital tools and virtual reality in medical product approval procedures and genotoxicity testing.

Further, the market is at the forefront of revolutionizing cancer treatment, offering targeted therapies for brain cancer, skin cancer, liver cancer, colon cancer, breast cancer, and non-small cell lung cancer. Therapeutic cancer vaccine and novel drugs delivered through advanced drug delivery option hold promise in combating these malignancies. Tailored recombinant proteins and viral vectors, considering tropism and type of virus, are essential in designing effective treatments. With the aid of cell lines, test models, and purification kits, manufacturers ensure quality and potency in viral vector production. Additionally, outsourcing drug discovery services streamline research efforts, accelerating medical product approval procedure. The integration of augmented and virtual reality tools enhances efficiency in life sciences research, propelling advancements in cancer therapeutics.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

166 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.02% |

|

Market Growth 2024-2028 |

USD 1.17 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.49 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

North America at 38% |

|

Key countries |

US, Canada, UK, China, and Japan |

|

Competitive landscape |

Leading companies, Market Positioning of companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Batavia Biosciences BV, Bayer AG, Catalent Inc., Creative Biogene, Danaher Corp., F. Hoffmann La Roche Ltd., FinVector Oy, FUJIFILM Holdings Corp., Institut Merieux, Lonza Group Ltd., Merck KGaA, Novartis AG, Oxford Biomedica Plc, REGENXBIO Inc, Sirion Biotech GmbH, Syncona Ltd., Takara Holdings Inc., Thermo Fisher Scientific Inc., uniQure NV, and Virovek Inc |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

Download Sample PDF at your Fingertips

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the growth of the between 2024 and 2028

- Precise estimation of the size and its contribution to the market in focus on the parent market

- Detailed analysis of customer landscape covering Diver of price sensitivity, Adoption of the lifecycle, and key purchase criteria

- Companies landscape comparing criticality of inputs and factors of differentiation

- Exclusive Matrix on companies' position and classification

- Accurate predictions about upcoming trends and changes in consumer behavior

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- A thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -