Air Motor Market Size 2024-2028

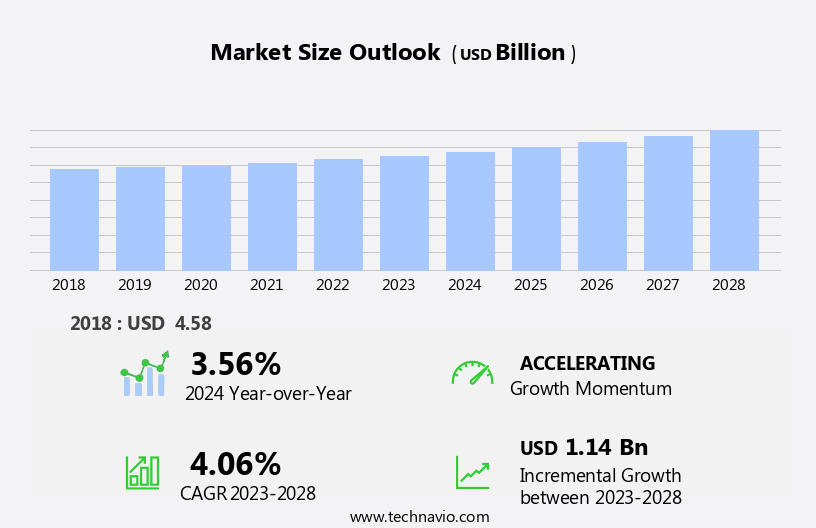

The air motor market size is forecast to increase by USD 1.14 billion at a CAGR of 4.06% between 2023 and 2028.

What will be the Size of the Air Motor Market During the Forecast Period?

How is this Air Motor Industry segmented and which is the largest segment?

The air motor industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Vane air motor

- Piston air motor

- Gear air motor

- Application

- Transportation

- Chemical

- Food and beverage

- Healthcare

- Others

- Geography

- APAC

- China

- Japan

- Europe

- Germany

- France

- North America

- US

- South America

- Middle East and Africa

- APAC

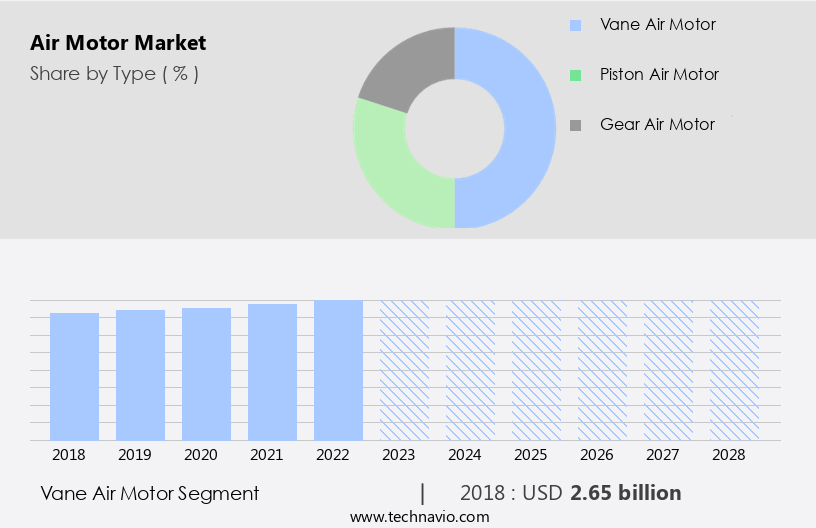

By Type Insights

- The vane air motor segment is estimated to witness significant growth during the forecast period.

The market is driven by the extensive utilization of air motors in various industries, including the printing, paint finishing, petrochemical, agricultural, nuclear, and cement industries. In 2023, vane air motors held a significant market share due to their high adoption in tooling and industrial machinery applications. These motors operate by utilizing a bladed wheel that rotates due to a pressure gradient withIn the motor housing. Compressed air powers the motor, generating the required torque for the shaft. The capacity to deliver variable torques and their fastening capabilities make vane air motors a popular choice in tools and machinery.

Additionally, the increasing demand for industrial tools and the ability of air motors to operate efficiently in harsh industrial environments with minimal fuel consumption are significant factors driving market growth. Industries with volatile environments, such as oil and gas, food and beverages, automotive, and heavy duty applications, also rely on air motors for their safety, reliability, flexibility, and productivity. Air motors come in various types, including vane air motors, piston air motors, and gear air motors, each offering unique advantages for specific applications. Air motors provide rotary and linear motion, and their energy efficiency makes them a viable alternative to diesel and natural gas engines.

However, factors such as air leakage, extreme temperatures, and high vibrations can impact their performance and lifespan. The market growth is further fueled by advancements in technology, including air pressure regulators, air receivers, safety valves, mufflers, filters, lubricators, and gauges.

Get a glance at the Air Motor Industry report of share of various segments Request Free Sample

The Vane air motor segment was valued at USD 2.65 billion in 2018 and showed a gradual increase during the forecast period.

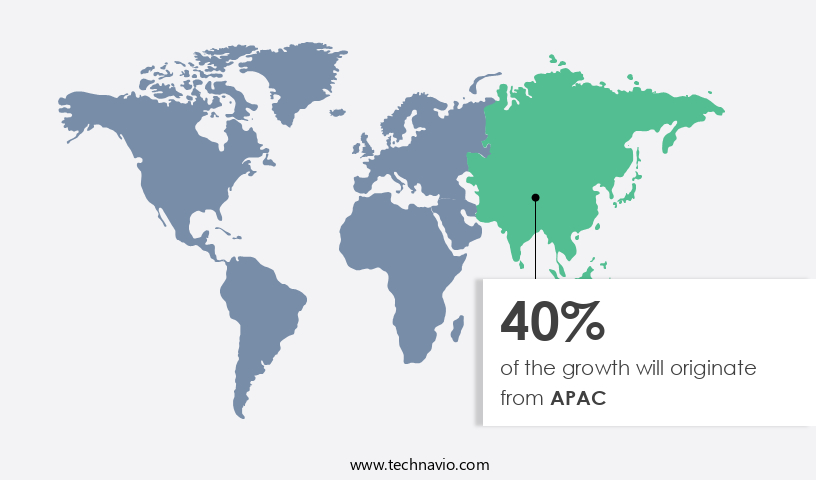

Regional Analysis

- APAC is estimated to contribute 40% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market in Asia Pacific is projected to experience steady expansion over the forecast period. Key contributors to this growth include China, Japan, India, Vietnam, South Korea, Malaysia, and Australia. These countries' industrial sectors, particularly manufacturing, are driving market growth due to increasing investments and the widespread adoption of pneumatic tools. In the manufacturing industry, air motors are utilized extensively in packaging machinery In the food and beverage sector and paint systems In the automotive industry. China, a significant consumer of packaging machinery, significantly influences the market's expansion in APAC. Air motors, including vane air motors, piston air motors, and gear air motors, are integral to industrial applications in various industries, such as the printing industry, paint finishing industry, petrochemical industry, agricultural industry, nuclear industry, and heavy-duty environments.

The market caters to diverse industries, prioritizing safety, reliability, flexibility, and productivity in volatile environments. Air motors offer energy efficiency, handling clockwise and anti-clockwise rotations, and providing fastening capabilities with variable torques. Applications include air guns, tires shops, handheld equipment, bolts, and electric tools, among others. Additionally, the market encompasses air turbine motors, electrical power, air pressure regulators, air receivers, safety valves, mufflers, filters, lubricators, and gauges. The food and agriculture, chemical, petrochemical, nuclear industries, and automotive industries are significant consumers of air motors.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Air Motor Industry?

Increasing number of applications in various tools is the key driver of the market.

What are the market trends shaping the Air Motor Industry?

Increasing focus on reducing overall air consumption by air motors is the upcoming market trend.

What challenges does the Air Motor Industry face during its growth?

Fluctuation in prices of raw materials used for manufacturing air motors is a key challenge affecting the industry growth.

Exclusive Customer Landscape

The air motor market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the air motor market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, air motor market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Atlas Copco AB - The PZB series of piston air motors from the company is recognized for its energy efficiency and distinctive low speed, high starting torque capabilities. With a compact design and three versatile mount configurations, installation is streamlined. This air motor range caters to various industrial applications, providing optimal performance and reliability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Atlas Copco AB

- DEPRAG SCHULZ GMBH u. CO. KG

- Desoutter Industrial Tools

- Eimco Elecon India Ltd.

- Fiam Utensili Pneumatici S.p.A.

- GLOBE Benelux BV

- IDEX Corp.

- Ingersoll Rand Inc.

- James Engineering

- MD Compressed Air Technology GmbH and Co. KG

- MODEC SAS

- Parker Hannifin Corp.

- PTM mechatronics GmbH

- Regal Rexnord Corp.

- Robert Bosch GmbH

- Sommer Technik GmbH

- SPX FLOW Inc.

- Stryker Corp.

- Thomas C. Wilson LLC

- TONSON Air Motors Manufacturing Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Air motors, also known as pneumatic motors, convert compressed air into mechanical work. This process generates rotary or linear motion, which is essential in various industries for powering tools and machinery. The market for air motors encompasses a wide range of applications, including the printing industry, paint finishing, petrochemical, agricultural, nuclear, and numerous others. Compressed air, the primary energy source for air motors, is produced through various means such as diesel and natural gas engines. The inlet pressure, torque, and speed relationship of air motors are crucial factors in determining their suitability for various applications. Air motors are employed in a multitude of industries and applications.

In the printing industry, they power air guns used for applying adhesives and ink. In paint finishing, they are used to operate sanders, grinders, and other handheld equipment. The petrochemical industry relies on air motors for their high power density and reliability in volatile environments. The agricultural industry utilizes air motors in heavy-duty applications, such as powering pumps and conveyor systems. In the nuclear industry, air motors are used in safety-critical applications due to their flexibility and productivity. Air motors are also used In the cement industry for powering various tools and machinery. Vane air motors, piston air motors, and gear air motors are common types of air motors used in this industry.

In tire shops, air motors power various handheld equipment, including wrenches and inflators. The market is driven by several factors, including energy efficiency, safety, reliability, and flexibility. Air motors offer several advantages over their electric counterparts, such as faster response times and the ability to operate in extreme temperatures and high vibration environments. Air motors are used in various industrial tools, such as drills, grinders, ratchets, sanders, cutters, and wrenches. They are also used In the automotive industry for powering pneumatic tools and In the food and agriculture industries for powering various machinery. Air motors are available in various types, including vane air motors, piston air motors, and gear air motors.

Vane air motors are known for their high power density and efficiency, while piston air motors offer high torque and speed capabilities. Gear air motors provide a high level of power and torque for heavy-duty applications. The market growth is driven by the increasing demand for air motors in various industries, including the printing, paint finishing, petrochemical, agricultural, nuclear, cement, and automotive industries. The market is expected to grow due to the advantages offered by air motors over electric tools, such as faster response times, the ability to operate in extreme temperatures and high vibration environments, and energy efficiency.

Air motors are an essential component in various industries, providing mechanical work through the conversion of compressed air. Their versatility, reliability, and energy efficiency make them a preferred choice for numerous applications. The market is expected to grow due to the increasing demand for air motors in various industries and their advantages over electric tools.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

179 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.06% |

|

Market growth 2024-2028 |

USD 1.14 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.56 |

|

Key countries |

US, China, Japan, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Air Motor Market Research and Growth Report?

- CAGR of the Air Motor industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the air motor market growth of industry companies

We can help! Our analysts can customize this air motor market research report to meet your requirements.

RIA -

RIA -