Aluminum Market Size 2026-2030

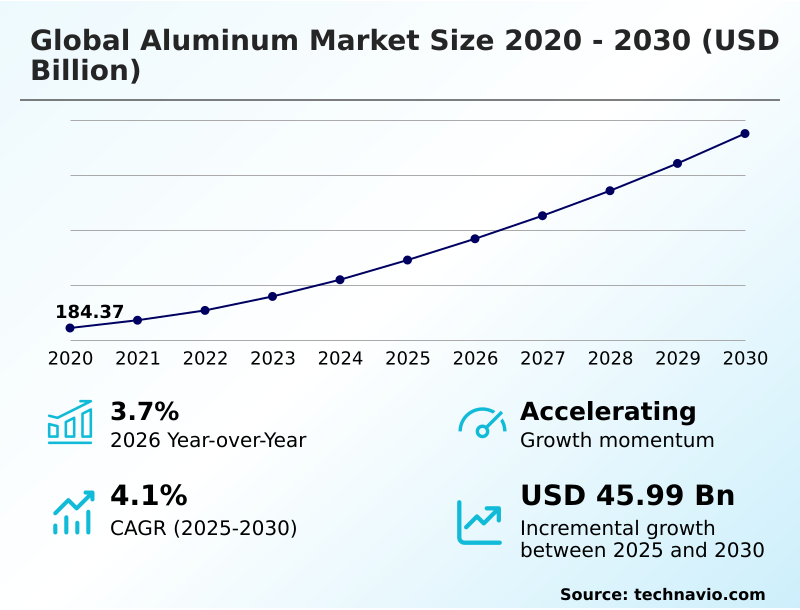

The aluminum market size is valued to increase by USD 45.99 billion, at a CAGR of 4.1% from 2025 to 2030. Proliferation of electric vehicle adoption and automotive lightweighting will drive the aluminum market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 64.7% growth during the forecast period.

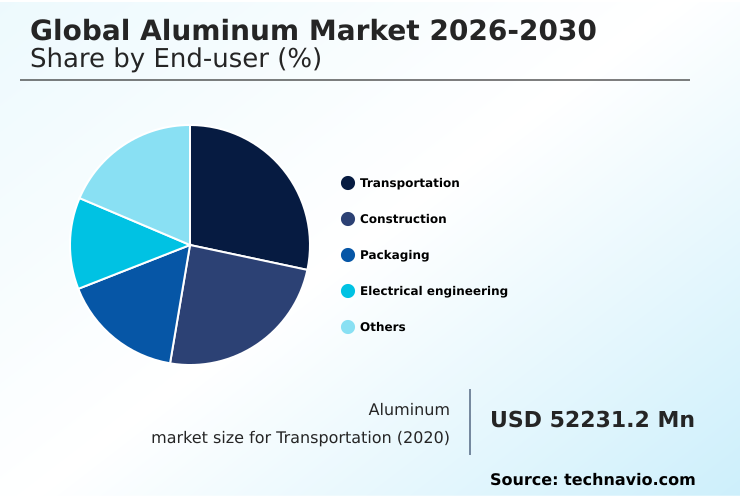

- By End-user - Transportation segment was valued at USD 57.77 billion in 2024

- By Type - Primary aluminum segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 70.71 billion

- Market Future Opportunities: USD 45.99 billion

- CAGR from 2025 to 2030 : 4.1%

Market Summary

- The aluminum market is undergoing a significant transformation, driven by the dual imperatives of technological innovation and sustainability. The demand for lightweight, high-strength materials in the automotive sector, particularly for electric vehicles, is a primary catalyst for growth. Concurrently, the aerospace and packaging industries continue to rely on aluminum for its unique properties.

- A key dynamic is the industry-wide push toward decarbonization, with producers investing in renewable energy sources and advanced recycling technologies to reduce their carbon footprint. For instance, a downstream manufacturer might now select a supplier not just on price but based on a verifiable low-carbon production certificate, a decision that impacts the entire supply chain.

- This shift toward a circular economy, where scrap is a valuable resource, is reshaping sourcing strategies and operational models. The market is also navigating challenges related to energy costs and geopolitical trade policies, which add layers of complexity to supply chain management and long-term investment planning.

- The ability to innovate in both production processes and alloy development will be crucial for maintaining a competitive edge.

What will be the Size of the Aluminum Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Aluminum Market Segmented?

The aluminum industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

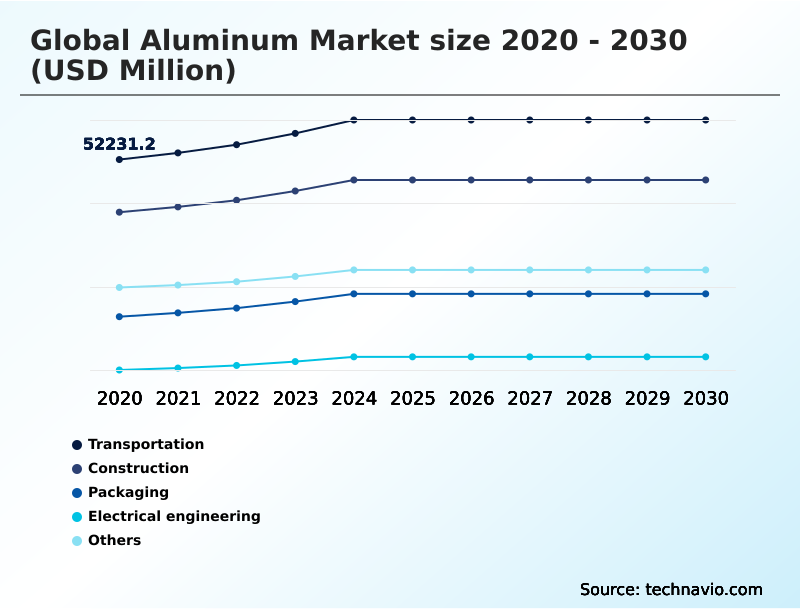

- End-user

- Transportation

- Construction

- Packaging

- Electrical engineering

- Others

- Type

- Primary aluminum

- Secondary aluminum

- Technology

- Extrusion

- Casting

- Rolling

- Others

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- Italy

- France

- North America

- US

- Canada

- Mexico

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By End-user Insights

The transportation segment is estimated to witness significant growth during the forecast period.

The transportation segment remains a primary end-user, with automotive lightweighting initiatives driving substantial consumption. The shift to electric vehicles necessitates high-strength aluminum for structural frame components and vehicle battery enclosures to offset battery weight and improve range.

Advanced manufacturing techniques in the automotive sector, including high-pressure die casting, have increased aluminum use per vehicle, with global car sales growing 2.5 percent.

This trend, coupled with the need for corrosion resistant alloys and high strength-to-weight ratio materials, solidifies the segment's role.

Sustainable aluminum solutions and the decarbonization of industry further reinforce the material's strategic importance in modern vehicle engineering, demanding continuous aluminum alloy development to meet performance standards.

The Transportation segment was valued at USD 57.77 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 64.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Aluminum Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the aluminum market is dominated by the APAC region, which accounts for over 64% of the market's incremental growth. This expansion is fueled by rapid industrialization, robust infrastructure development, and a burgeoning automotive manufacturing sector.

Countries like China and India are at the forefront, driven by domestic demand for construction, transportation, and packaging materials. A notable trend is the region's increasing focus on producing high-value and sustainable aluminum solutions.

For instance, the number of automotive suppliers in Vietnam obtaining IATF 16949 certification recently surpassed 900, signaling a strategic move toward meeting stringent global quality standards. This commitment enhances the region's role in the global supply chain for high-performance applications.

The integration of renewable energy sources into smelting operations is also gaining traction, aligning with the global demand for materials with a reduced carbon footprint, which is a key factor in geopolitical supply chain risk.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global aluminum market 2026-2030 is increasingly shaped by strategic decisions around capital investment in smelter modernization and the mitigation of geopolitical risk in bauxite supply. The financial commitment required for transitioning from legacy systems to inert anode or hydrogen-based smelting is substantial, creating a competitive divide between well-capitalized producers and smaller players.

- This transition is essential for achieving low-carbon aluminum production methods, which are becoming a prerequisite for market access in environmentally sensitive sectors. Concurrently, the industry is exploring the comparative performance of aluminum vs steel in automotive applications, with a focus on lifecycle emissions and recyclability.

- The implementation of a carbon border tax on aluminum further complicates trade flows, incentivizing regionalized supply chains and investments in advanced scrap sorting for alloys. The role of AI in aluminum smelting operations is also expanding, offering pathways to optimize energy efficiency in primary smelting and improve process control.

- This technological adoption, coupled with a deeper understanding of the circular economy in aluminum packaging, is critical for future competitiveness. For example, while the initial outlay for advanced sorting infrastructure is high, it unlocks the potential to produce high-grade secondary aluminum, a process that consumes a fraction of the energy required for primary production, thereby improving long-term operational margins.

What are the key market drivers leading to the rise in the adoption of Aluminum Industry?

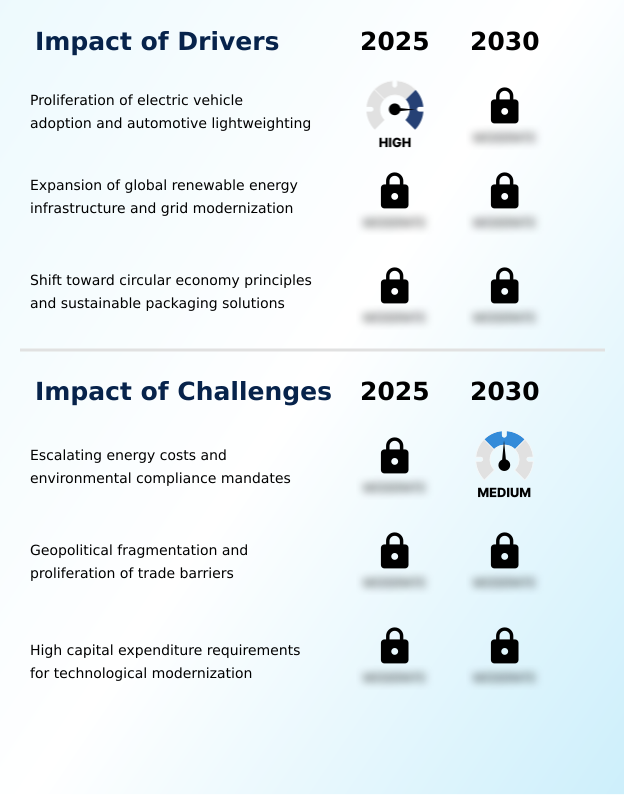

- The proliferation of electric vehicle adoption and the associated push for automotive lightweighting are key drivers stimulating demand for advanced aluminum alloys.

- The global aluminum market 2026-2030 is propelled by strong demand from the automotive and energy sectors. The transition to electric vehicles is a significant driver, as automotive lightweighting with high-strength aluminum is critical for improving efficiency and battery range.

- This has spurred advancements in rolled aluminum products and architectural aluminum systems for vehicle battery enclosures. Simultaneously, the expansion of renewable energy infrastructure relies on aluminum for its durability and cost-effectiveness.

- For instance, the use of advanced aluminum composite core conductors in new grid projects has increased energy efficiency by 20% over conventional materials.

- This push for electrification and the need for heat exchanger materials in green technologies create a stable demand base. The principles of the circular economy and sustainable packaging solutions also bolster the market, promoting secondary aluminum recycling.

What are the market trends shaping the Aluminum Industry?

- The ascendancy of low-carbon aluminum is reshaping the market, driven by consumer demand and the implementation of carbon border adjustment policies. This shift is compelling producers to adopt sustainable manufacturing practices.

- Key trends are reshaping the global aluminum market 2026-2030, led by the imperative for decarbonization of industry. This is fueling the demand for low-carbon aluminum, with producers leveraging renewable energy integration to reduce the carbon footprint of energy-intensive smelting operations. The implementation of carbon border adjustment policies is creating a premium for sustainable aluminum solutions.

- Technologically, the adoption of AI and advanced robotics is optimizing production, with some automated facilities achieving up to a 15% improvement in process consistency. This technological modernization enhances smelting energy efficiency. Furthermore, the industry is expanding closed-loop recycling systems and investing in advanced scrap sorting infrastructure to improve circular material flow.

- These efforts in primary aluminum production reflect a market-wide shift toward sustainability.

What challenges does the Aluminum Industry face during its growth?

- Escalating energy costs and the imperative to comply with stringent environmental mandates present a significant challenge to profitability and operational stability in aluminum production.

- The global aluminum market 2026-2030 faces significant hurdles, primarily from high capital expenditure requirements and escalating energy costs. Modernizing aging smelting facilities and adopting breakthrough inert anode technology demand massive investment, with project costs often exceeding initial estimates by 15-20%. These financial pressures are compounded by volatile electricity prices, which directly impact the profitability of primary aluminum production.

- Geopolitical fragmentation and the proliferation of protectionist trade policies disrupt established supply chains for bauxite and alumina, creating uncertainty and forcing companies to diversify sourcing strategies. Additionally, stringent environmental compliance mandates and the high cost of carbon tracking mechanisms add another layer of complexity.

- This challenging environment requires companies to focus on operational efficiency, risk management, and strategic investments in less energy-intensive secondary production to remain competitive.

Exclusive Technavio Analysis on Customer Landscape

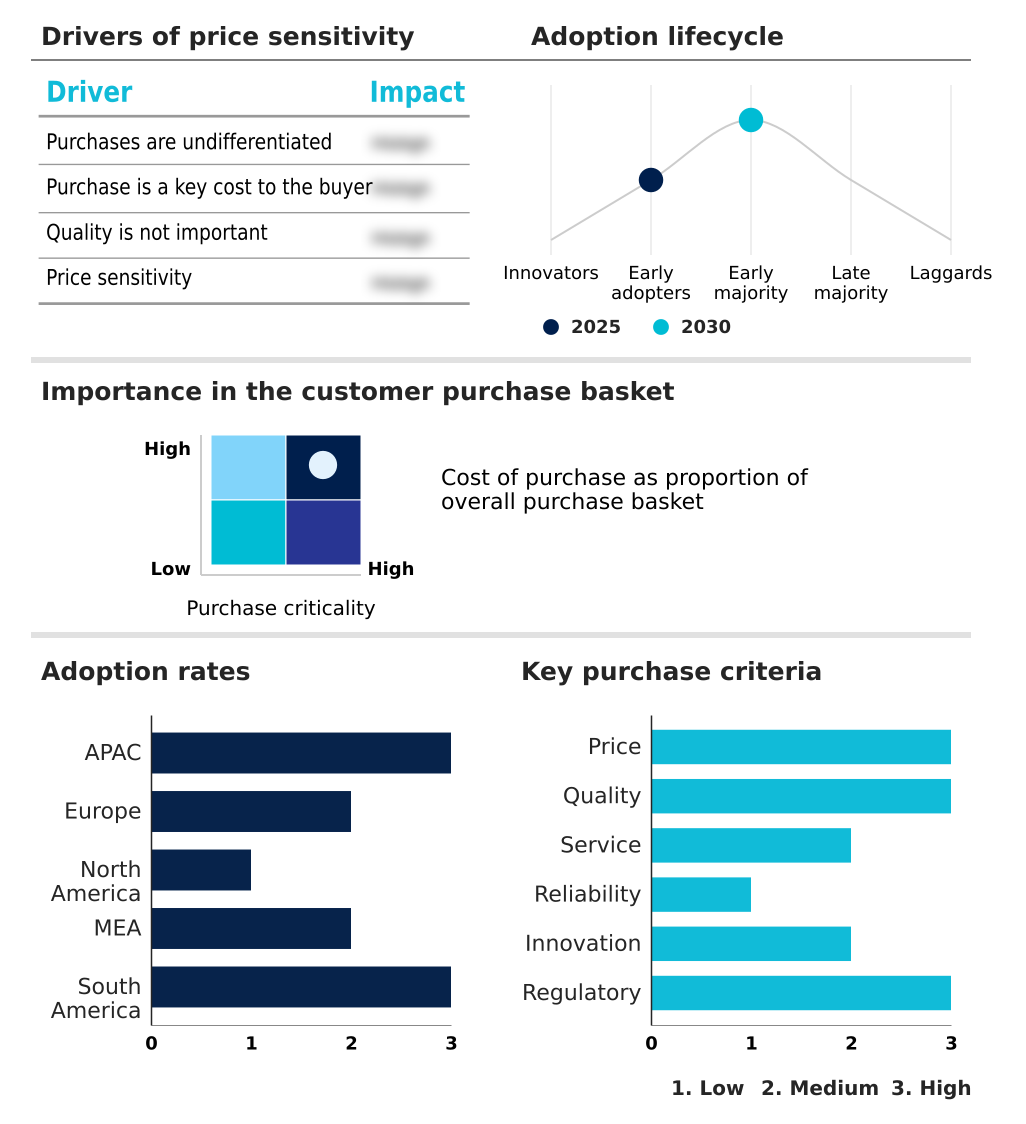

The aluminum market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the aluminum market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Aluminum Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, aluminum market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alcoa Corp. - Analysis indicates a portfolio of primary aluminum, alumina, and bauxite products, targeting critical aerospace, automotive, and industrial applications through vertically integrated operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alcoa Corp.

- Aluminium Bahrain BSC

- Aluminum Corp. of China Ltd.

- Arconic Corp.

- Bonnell Aluminum Inc.

- Century Aluminum Co.

- China Hongqiao Group Ltd.

- Constellium SE

- Granges AB

- Hindalco Industries

- Hubei Xingfa Chemicals Group

- Jindal Aluminium Ltd.

- Kaiser Aluminum Corp.

- National Aluminium Co. Ltd.

- Norsk Hydro ASA

- Rio Tinto Ltd.

- Saudi Arabian Mining Co.

- UACJ Corp.

- United Co. RUSAL

- Vedanta Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Aluminum market

- In August 2025, Ball Corp. announced a 4.1 percent year-over-year increase in aluminum packaging shipments for the second quarter, highlighting growing demand for sustainable aluminum products.

- In January 2025, Rio Tinto and Norsk Hydro announced a strategic partnership, committing to invest approximately $45 million over five years to develop and test carbon capture technologies for existing smelters.

- In March 2025, Norsk Hydro ASA initiated construction of a new aluminum recycling plant in Torija, Spain, designed to produce 120,000 metric tons of low-carbon extrusion ingot annually from post-consumer scrap.

- In May 2025, Emirates Global Aluminum announced its intention to construct a new primary aluminum smelter in the United States, the first of its kind in the country in several decades.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Aluminum Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 306 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.1% |

| Market growth 2026-2030 | USD 45994.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.7% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, Germany, Italy, France, UK, Spain, Poland, US, Canada, Mexico, Saudi Arabia, South Africa, UAE, Egypt, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The aluminum market is advancing through a period of structural change, driven by the imperative for primary aluminum production to become more sustainable. Investment in bauxite refining and alumina smelting is now closely tied to environmental performance, compelling firms to innovate.

- Key operational processes like molten metal processing and extrusion die technology are being optimized for energy efficiency and material throughput. The development of advanced casting techniques is crucial for serving the automotive sector's demand for complex, lightweight components.

- A major focus is on secondary aluminum recycling, as it consumes approximately 95% less energy than primary production, directly impacting bottom-line profitability and aligning with circular economy principles. This makes investments in scrap sorting technology and beverage can recycling infrastructure a boardroom-level priority.

- Furthermore, the push for low-carbon aluminum and green aluminum production is transforming supply chains, with anodized surface treatment and other finishing processes also being evaluated for their environmental impact. The development of specialized aerospace grade alloys and materials for heat exchangers continues to drive research and development efforts across the industry.

What are the Key Data Covered in this Aluminum Market Research and Growth Report?

-

What is the expected growth of the Aluminum Market between 2026 and 2030?

-

USD 45.99 billion, at a CAGR of 4.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Transportation, Construction, Packaging, Electrical engineering, and Others), Type (Primary aluminum, and Secondary aluminum), Technology (Extrusion, Casting, Rolling, and Others) and Geography (APAC, Europe, North America, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of electric vehicle adoption and automotive lightweighting, Escalating energy costs and environmental compliance mandates

-

-

Who are the major players in the Aluminum Market?

-

Alcoa Corp., Aluminium Bahrain BSC, Aluminum Corp. of China Ltd., Arconic Corp., Bonnell Aluminum Inc., Century Aluminum Co., China Hongqiao Group Ltd., Constellium SE, Granges AB, Hindalco Industries, Hubei Xingfa Chemicals Group, Jindal Aluminium Ltd., Kaiser Aluminum Corp., National Aluminium Co. Ltd., Norsk Hydro ASA, Rio Tinto Ltd., Saudi Arabian Mining Co., UACJ Corp., United Co. RUSAL and Vedanta Ltd.

-

Market Research Insights

- The aluminum market is defined by a dynamic interplay of economic and environmental factors. The push for decarbonization has made secondary aluminum, which uses 95% less energy than primary production, a strategic priority. This focus on a circular material flow drives investment in closed-loop recycling systems and advanced sorting technologies, improving resource efficiency.

- Concurrently, the expansion of clean energy infrastructure creates significant demand; for example, advanced aluminum composite core conductors have demonstrated the ability to increase grid energy efficiency by twenty percent over traditional materials. Downstream aluminum processing capabilities are being enhanced to produce high-performance materials for automotive structural components, where lightweighting is critical.

- However, the industry grapples with geopolitical supply chain risk and volatile energy prices, necessitating robust supply chain diversification and risk management strategies to ensure stability.

We can help! Our analysts can customize this aluminum market research report to meet your requirements.

RIA -

RIA -