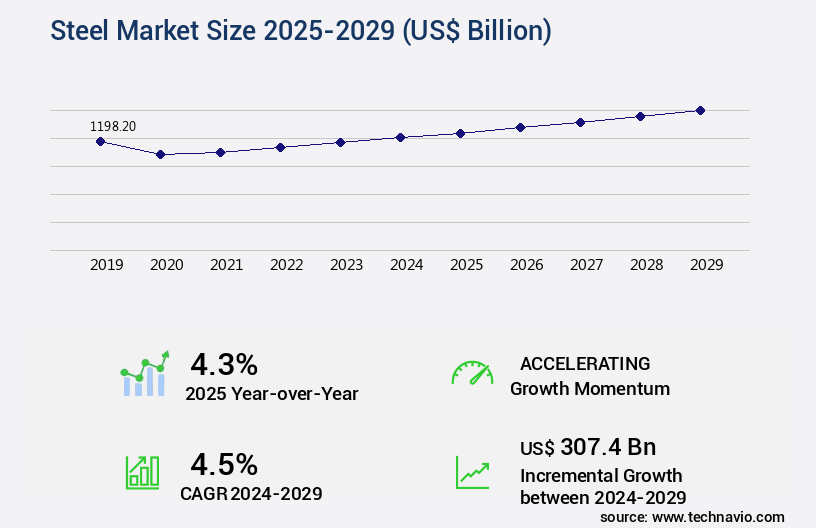

Steel Market Size 2025-2029

The steel market size is valued to increase USD 307.4 billion, at a CAGR of 4.5% from 2024 to 2029. Urbanization and infrastructure development will drive the steel market.

Major Market Trends & Insights

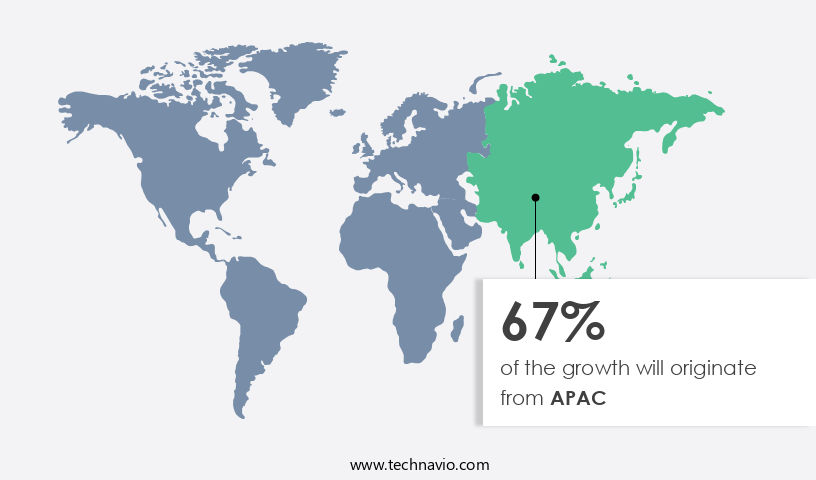

- APAC dominated the market and accounted for a 67% growth during the forecast period.

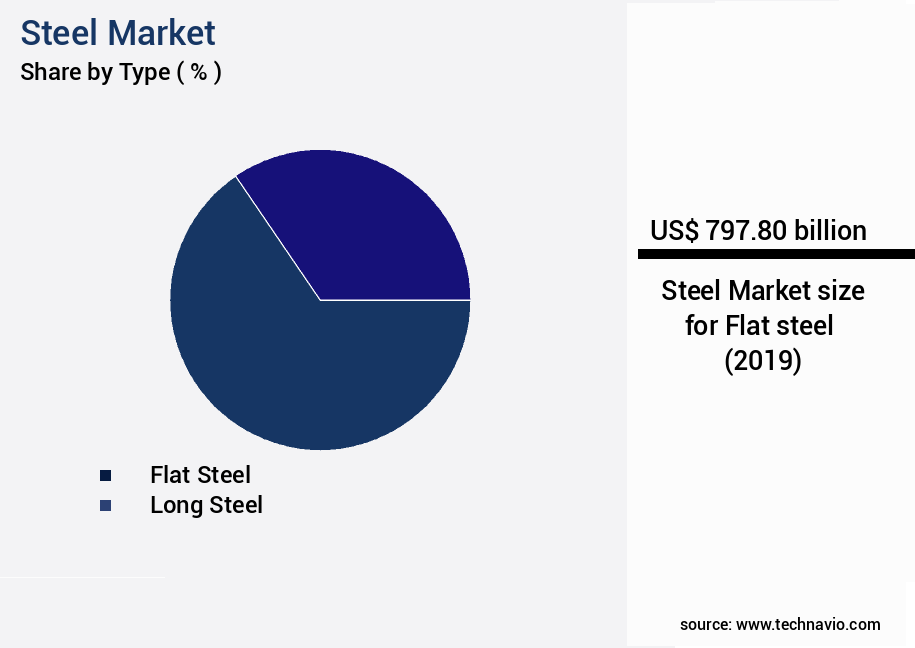

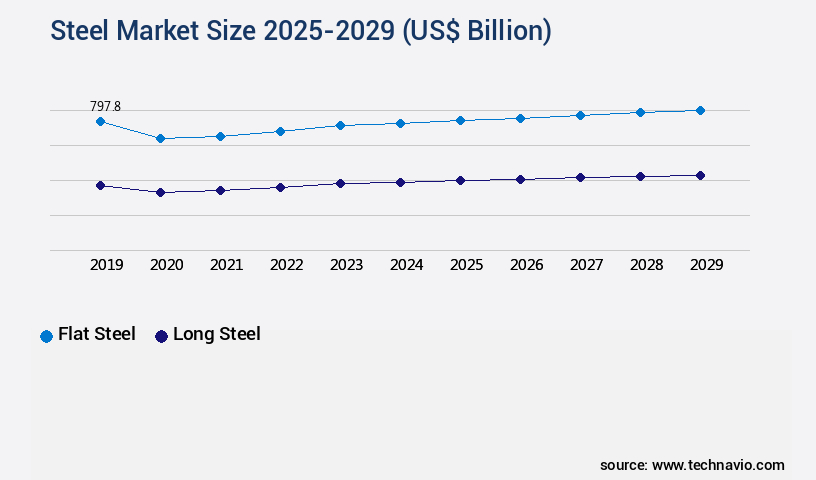

- By Type - Flat steel segment was valued at USD 797.80 billion in 2023

- By Application - Structural steel segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 28.76 billion

- Market Future Opportunities: USD 307.40 billion

- CAGR from 2024 to 2029 : 4.5%

Market Summary

- The market is a significant player in the industrial sector, with a current size of over 1,300 million metric tons in annual production. This market's expansion is primarily driven by urbanization and infrastructure development, as steel is a crucial component in constructing buildings, bridges, and transportation systems. Additionally, there is a growing trend toward sustainable steel production, as companies seek to reduce their carbon footprint and meet increasing environmental regulations. However, the market faces challenges from trade barriers and protectionist policies, which can disrupt global supply chains and impact pricing. These issues can lead to volatility in the market and create uncertainty for businesses.

- Despite these challenges, the steel industry continues to evolve, with innovations in production methods and materials driving efficiency and cost savings. As the world's population grows and urbanizes, the demand for steel is expected to remain strong, making it an essential commodity for businesses across various industries.

What will be the Size of the Steel Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Steel Market Segmented ?

The steel industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Flat steel

- Long steel

- Application

- Structural steel

- Automotive steel

- Electrical steel

- Packaging steel

- End-user

- Construction

- Transportation

- Machinery

- Metal goods

- Others

- Method

- Basic oxygen furnace

- Electric arc furnace

- Open hearth furnace

- Geography

- North America

- US

- Mexico

- Europe

- Germany

- Italy

- Russia

- Middle East and Africa

- Turkey

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Type Insights

The flat steel segment is estimated to witness significant growth during the forecast period.

In the ever-evolving market, flat steel, a significant sector, is characterized by its versatility and robustness. This category includes hot-rolled coils (HRC), cold-rolled coils (CRC), galvanized steel, tinplate, and steel plates, each designed to meet specific industrial demands. Hot-rolled steel sheets offer high yield strength and tensile strength, while cold-rolled steel sheets provide improved surface finish and formability. Galvanized steel coatings ensure corrosion resistance, making them ideal for harsh environments. The steel industry continues to innovate, with advancements in heat treatment processes, steel weldability, and microalloyed steel grades. Ductile iron properties and stainless steel grades cater to high-strength applications, while steel forming processes enhance production efficiency.

The Flat steel segment was valued at USD 797.80 billion in 2019 and showed a gradual increase during the forecast period.

Steel quality control is ensured through non-destructive testing and microstructure analysis. The steel industry's focus on research and development has led to the emergence of high-strength low-alloy steel, which boasts impressive strength-to-weight ratios. A notable example of flat steel's impact is its extensive use in the automotive sector, where it contributes to the manufacturing of body panels and structural components. In fact, the automotive industry accounts for approximately 16% of global steel consumption. As the market continues to evolve, the demand for advanced materials and processing technologies will persist, driving innovation and growth within this essential industry.

Regional Analysis

APAC is estimated to contribute 67% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Steel Market Demand is Rising in APAC Request Free Sample

The market in the Asia-Pacific (APAC) region is experiencing significant growth, fueled by industrial expansion, infrastructure development, and strategic investments. China, a key player, produces over half of the world's crude steel output, with a 5.8% year-on-year increase in industrial production in 2024. This growth is driven by robust manufacturing and infrastructure sectors, as well as China's leadership in the electric vehicle (EV) industry, which accounted for 70% of global EV production and 80% of domestic EV sales in 2024.

India and other countries in the region are also experiencing a manufacturing surge, while Japan and South Korea focus on high-value steel applications. These factors collectively shape the evolving global steel landscape.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is a dynamic and complex industry that plays a pivotal role in various sectors, from construction and automotive to energy and manufacturing. The market's growth is influenced by numerous factors, including the influence of alloying elements on steel strength and the effect of heat treatment on steel microstructure. In the pursuit of improving steel weldability, preheating techniques have gained significance, while advanced steel alloys with enhanced corrosion resistance continue to dominate the market. Steel's fatigue behavior under cyclic loading and optimal steel selection criteria for structural applications are crucial considerations for engineers and designers, as durability and component design are paramount.

Non-destructive testing techniques are essential in ensuring the structural integrity of steel, particularly in large, complex structures. Advanced manufacturing processes for high-strength steel are increasingly being adopted, with a focus on sustainability and energy efficiency. Developing high-performance steel for the automotive industry is a significant trend, as lightweight materials contribute to improved fuel efficiency and reduced emissions. Steel surface treatment methods, such as corrosion protection coatings, are essential for extending the life of steel structures and components. Innovative steel manufacturing technologies are continually being developed to address the evolving demands of various industries. Steel recycling methods have a substantial impact on the environmental footprint of the steel industry, with significant advancements in recycling techniques and energy consumption reduction.

Comparing different steel grades based on their mechanical properties reveals the importance of understanding the unique characteristics of each type. For instance, cold rolling significantly influences the mechanical behavior of steel, making it a popular choice for various applications. Steel industry best practices emphasize quality control and continuous improvement, ensuring the delivery of reliable and consistent products. In terms of numerical comparison, recent studies suggest that the adoption of advanced manufacturing processes for high-strength steel has led to a notable increase in production efficiency, with some facilities reporting output improvements of up to 20%. This underscores the importance of embracing innovation and technology in the steel industry.

The steel industry continues to evolve rapidly, driven by technological advancements and increasing demands for performance, sustainability, and cost-efficiency. A critical factor in this evolution is the influence of alloying elements, which significantly impacts steel strength, effect heat treatment, and steel microstructure. By carefully selecting and balancing elements like chromium, nickel, and molybdenum, manufacturers can tailor properties such as hardness, toughness, and corrosion resistance to meet specific application needs. One of the key challenges in fabrication is improving steel weldability through preheating, a process that helps minimize thermal stress and prevents cracking during and after welding. This is particularly important in advanced steel alloys, which are engineered for enhanced corrosion resistance and higher strength. These alloys are often employed in environments where durability is paramount, such as in marine or chemical processing industries.

Understanding steel fatigue behavior under cyclic loading is essential in applications subjected to repeated stress, such as bridges, automotive components, and aerospace structures. Engineers must consider the optimal steel selection criteria structural application to ensure both performance and longevity. This selection process is closely tied to steel component design considerations, which factor in load-bearing capacity, environmental exposure, and manufacturability. To ensure durability, engineers rely on non-destructive testing techniques structural steel, such as ultrasonic testing, radiography, and magnetic particle inspection, which allow for the detection of internal flaws without damaging the material. These techniques are increasingly used in advanced manufacturing processes high-strength steel, which involve precision techniques such as laser cutting and additive manufacturing to produce complex, reliable parts.

Sustainability has also become a central focus in the steel industry. Steel recycling methods play a pivotal role in reducing the environmental impact of steel production, conserving raw materials, and cutting down on efficiency energy consumption. These efforts align with broader goals of developing high-performance steel automotive industry, where lighter yet stronger materials contribute to fuel efficiency and reduced emissions.

What are the key market drivers leading to the rise in the adoption of Steel Industry?

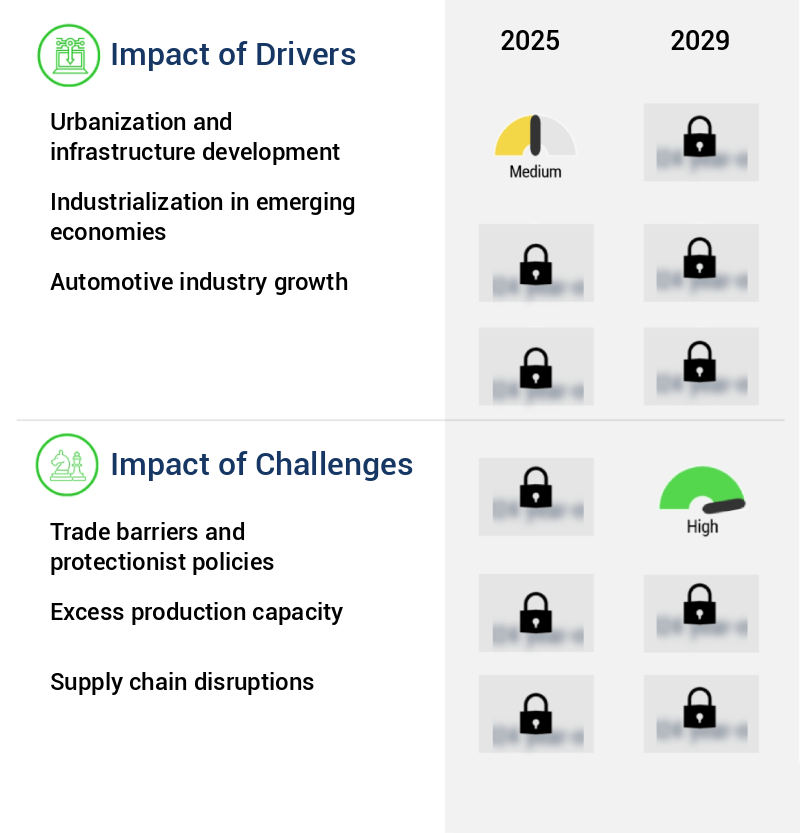

- Urbanization and infrastructure development serve as the primary catalyst for market growth.

- Urbanization and infrastructure development are key factors fueling the demand in the market. With over half of the world's population living in urban areas as of 2024, according to the United Nations Department of Economic and Social Affairs, the need for robust infrastructure to accommodate housing, transportation, utilities, and public services is increasingly pressing. This demographic shift is driving unprecedented investment in long-term infrastructure solutions, particularly in emerging economies. For instance, India allocated approximately 25.5% of its fiscal year 2023-2024 budget, equivalent to around USD 122 billion, towards infrastructure development.

- The infrastructure sector's reliance on steel is substantial, making it a significant market driver. As urbanization continues to advance and populations grow, the demand for steel in infrastructure applications is expected to persist and evolve, underpinning its essential role in shaping the global economy.

What are the market trends shaping the Steel Industry?

- Shifting production toward sustainability is becoming a mandatory trend in the market. Market trends indicate a clear move towards sustainable production methods.

- A significant trend in the market is the increasing emphasis on sustainable production. This shift is influenced by regulatory pressures, industry initiatives to reduce carbon emissions, and technological advancements. One notable example of this trend is Hyundai Steel's announcement on March 25, 2025, regarding a substantial investment in a new Electric Arc Furnace (EAF)-based integrated steel mill in Louisiana. This facility, valued at approximately 5.8 billion indexed dollars, is projected to yield 2.7 million metric tons of automotive-grade steel annually upon completion in 2029.

- The novelty of this development lies in its full-cycle integration of low-carbon EAF technology, marking a departure from conventional blast furnace methods. This transition underscores the steel industry's ongoing evolution towards more sustainable and efficient production processes.

What challenges does the Steel Industry face during its growth?

- Trade barriers and protectionist policies pose a significant challenge to the growth of industries by impeding international trade and competition.

- The market experiences continuous challenges from trade barriers and protectionist policies. These measures, designed to safeguard domestic industries, introduce volatility, disrupt supply chains, and escalate geopolitical tensions among major steel-producing and consuming nations. In March 2025, the United States imposed a 25% tariff on all steel and aluminum imports, extending earlier protectionist actions by revoking previous exemptions. This policy aimed to bolster domestic production and decrease reliance on foreign steel. However, it elicited immediate opposition from key trading partners and sparked concerns about the possibility of a broader global trade conflict. Trade restrictions have significant implications for the steel industry, impacting both production and consumption patterns.

- For instance, in 2024, the European Union accounted for approximately 30% of global steel imports, with China representing around 18%. The implementation of protectionist measures can lead to price fluctuations and supply disruptions, affecting various sectors that rely on steel, such as construction, automotive, and manufacturing. Furthermore, these policies can result in retaliatory actions, potentially leading to a trade war and further market instability. Despite these challenges, the market continues to evolve, with ongoing advancements in technology and production methods. For example, the increasing adoption of electric arc furnaces and mini-mills has led to a shift towards more efficient and cost-effective steel production.

- Additionally, the rise of green steel, produced using renewable energy sources, is gaining momentum as companies seek to reduce their carbon footprint and meet sustainability goals. In conclusion, the market faces ongoing challenges from trade barriers and protectionist policies, which can lead to market instability, supply chain disruptions, and geopolitical tensions. However, the industry remains dynamic, with advancements in technology and production methods driving innovation and efficiency. Companies must stay informed of market trends and adapt to changing regulatory environments to remain competitive in this complex and evolving landscape.

Exclusive Technavio Analysis on Customer Landscape

The steel market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the steel market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Steel Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, steel market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ansteel Group Corp. Ltd. - This company specializes in manufacturing and supplying high-quality steel, catering to various industries such as automotive, railway, shipbuilding, and construction.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ansteel Group Corp. Ltd.

- ArcelorMittal SA

- Baosteel Group Corp.

- Beijing Shougang Co. Ltd.

- Gerdau SA

- HBIS Group Co. Ltd.

- JFE Holdings Inc.

- JSW Steel

- Nippon Steel Corp.

- Nucor Corp.

- PAO Severstal

- POSCO holdings Inc.

- Salzgitter AG

- Shagang Group Inc.

- SSAB AB

- Steel Dynamics Inc

- Tata Steel Ltd.

- Tenaris SA

- thyssenkrupp AG

- United States Steel Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Steel Market

- In January 2024, ArcelorMittal, the world's leading steel and mining company, announced a strategic partnership with Siemens Energy to jointly develop and commercialize hydrogen-reduced iron (HRI) and direct reduced iron (DRI) technologies for the steel industry (ArcelorMittal press release, 2024). This collaboration aimed to reduce carbon emissions in steel production by replacing traditional coke with hydrogen.

- In March 2024, Nippon Steel Corporation, Japan's largest steelmaker, completed the acquisition of a 20% stake in ThyssenKrupp's steel business for € 1.6 billion (Bloomberg, 2024). This deal marked a significant expansion of Nippon Steel's presence in Europe and strengthened its global market position.

- In May 2024, the European Union (EU) approved the merger between Tata Steel Europe and ThyssenKrupp Steel Europe, subject to certain conditions (European Commission press release, 2024). The combined entity, Tata Steel Europe, became the second-largest steel producer in Europe, with a market share of approximately 20%.

- In February 2025, United States Steel Corporation (U.S. Steel) announced the launch of its new mini-mill, Gary Works, in Gary, Indiana, with an annual production capacity of 3 million tons (U.S. Steel press release, 2025). This expansion was a significant investment in the American steel industry, aiming to meet the growing demand for steel in the domestic market.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Steel Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

252 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2025-2029 |

USD 307.4 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.3 |

|

Key countries |

China, India, US, Japan, South Korea, Russia, Italy, Turkey, Germany, and Mexico |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- Amidst the dynamic landscape of global industries, the market continues to evolve, driven by advancements in technology and shifting consumer demands. Two key aspects of steel production that have garnered significant attention are steel surface treatment and heat treatment processes. Steel surface treatment, including galvanized coatings and various forms of painting, plays a crucial role in enhancing steel's durability and resistance to environmental factors. For instance, galvanized steel coatings provide superior corrosion resistance, extending the life cycle of steel structures. Heat treatment processes, such as annealing, quenching, and tempering, significantly impact steel's weldability, tensile strength, and microstructure.

- Advanced high-strength steel, with its increased yield strength and improved microalloyed grades, is a testament to the power of these processes. Steel quality control measures, including non-destructive testing and microstructure analysis, ensure the consistency and reliability of steel components. Steel production efficiency and structural integrity are further bolstered through the implementation of advanced steel processing technologies, such as casting methods and forming processes. Ductile iron, with its unique properties, offers a compelling alternative to traditional steel grades. Its high strength and fatigue resistance make it an attractive choice for various industries, including automotive and construction. The market's continuous evolution is a reflection of the relentless pursuit of innovation and efficiency.

- By integrating the latest advancements in steel technology, industry experts are able to provide high-performance, cost-effective solutions for a wide range of applications. A notable example of this progress can be seen in the steel recycling processes, which not only contribute to environmental sustainability but also reduce production costs and improve overall market competitiveness. As the market continues to adapt and grow, the integration of these advancements will undoubtedly play a pivotal role in shaping its future. In the realm of steel material selection, the balance between strength, cost, and environmental impact is a critical consideration. For instance, high-strength low-alloy steel offers increased strength with lower alloy content, making it an attractive alternative to traditional carbon steel.

- Stainless steel grades, with their exceptional corrosion resistance, are another popular choice for industries that demand high levels of durability and reliability. The selection of the appropriate steel grade and processing method is a complex decision that requires a deep understanding of the application's unique requirements and the market's evolving landscape. In summary, the market is a vibrant and ever-changing ecosystem, shaped by advancements in technology, consumer demands, and industry expertise. By focusing on key areas such as steel surface treatment, heat treatment processes, and steel material selection, we can gain valuable insights into the market's current trends and future potential.

What are the Key Data Covered in this Steel Market Research and Growth Report?

-

What is the expected growth of the Steel Market between 2025 and 2029?

-

USD 307.4 billion, at a CAGR of 4.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Flat steel and Long steel), Application (Structural steel, Automotive steel, Electrical steel, and Packaging steel), End-user (Construction, Transportation, Machinery, Metal goods, and Others), Method (Basic oxygen furnace, Electric arc furnace, and Open hearth furnace), and Geography (APAC, Europe, North America, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Urbanization and infrastructure development, Trade barriers and protectionist policies

-

-

Who are the major players in the Steel Market?

-

Ansteel Group Corp. Ltd., ArcelorMittal SA, Baosteel Group Corp., Beijing Shougang Co. Ltd., Gerdau SA, HBIS Group Co. Ltd., JFE Holdings Inc., JSW Steel, Nippon Steel Corp., Nucor Corp., PAO Severstal, POSCO holdings Inc., Salzgitter AG, Shagang Group Inc., SSAB AB, Steel Dynamics Inc, Tata Steel Ltd., Tenaris SA, thyssenkrupp AG, and United States Steel Corp.

-

Market Research Insights

- The market encompasses a diverse range of products and processes, including mechanical properties, thermal processing, sustainability, coating techniques, production optimization, structural analysis, lifecycle assessment, component manufacturing, application guide, high-performance steel, design standards, surface engineering, performance metrics, industry standards, quality assurance, advanced alloys, manufacturing methods, failure prevention, material modeling, recycling technology, testing methodologies, material science, corrosion protection, design optimization, and innovations. According to industry data, global steel production reached 1.8 billion metric tons in 2020, a 3.2% increase from the previous year.

- In contrast, the average steel product specifications require a minimum yield strength of 250 MPa and a tensile strength of 485 MPa. These requirements highlight the importance of steel production optimization, material modeling, and quality assurance to meet market demands and maintain high-performance standards.

We can help! Our analysts can customize this steel market research report to meet your requirements.

RIA -

RIA -