Data Center Mechanical Construction Market Size 2025-2029

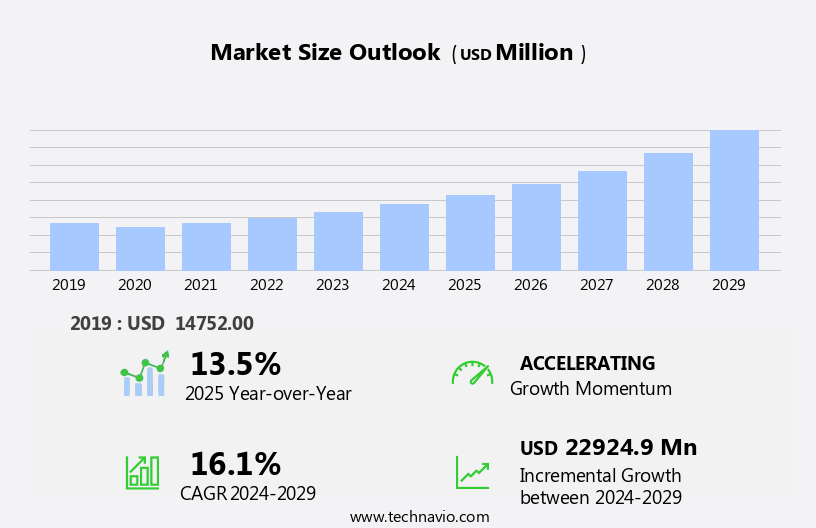

The data center mechanical construction market size is forecast to increase by USD 22.92 billion at a CAGR of 16.1% between 2024 and 2029.

- The market is experiencing significant growth, driven by the increasing adoption of High Performance Computing (HPC) across enterprises and the subsequent expansion of hyperscale centers. This trend is fueled by the ever-growing demand for data processing and storage, particularly in industries such as finance, healthcare, and technology. However, the market is not without challenges. One of the most pressing issues is the high power consumption in data centers, which necessitates the implementation of energy-efficient solutions and the adoption of renewable energy sources. Additionally, the complexity of construction projects and the need for specialized expertise add to the market's challenges.

- One of the primary drivers is the increasing investments in construction, as businesses recognize the importance of digital transformation and the role play in supporting their operations. This trend is driven by the proliferation of edge computing, 5G technology, and digital transformation initiatives. Despite these hurdles, opportunities abound for companies that can navigate the intricacies of mechanical construction and provide innovative, energy-efficient solutions to meet the demands of this rapidly evolving market. By staying abreast of the latest trends and developments, companies can position themselves to capitalize on the significant growth potential in this sector.

What will be the Size of the Data Center Mechanical Construction Market during the forecast period?

- The market is experiencing significant growth and innovation, driven by the increasing demand for more efficient and compliant solutions. Virtualization and consolidation are key trends, leading to the adoption of advanced technologies such as air-side economizers, glycol systems, and liquid cooling. Compliance with regulations, including emergency power and fire alarm systems, is also a major consideration. Data center expansion continues to be a priority, with variable refrigerant flow and chilled water systems gaining popularity for their energy efficiency.

- Innovations in automation, access control, and CCTV systems are also transforming the market, while direct expansion cooling and transformer banks remain essential components. The integration of free cooling and adiabatic cooling systems is further enhancing energy savings, and circuit breakers ensure reliable power distribution. Overall, the market is dynamic and evolving, with a focus on optimizing energy usage, ensuring compliance, and improving security and efficiency.

How is this Data Center Mechanical Construction Industry segmented?

The industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Cooling solutions

- Rack

- Server rail kit

- Others

- Type

- Air-based cooling

- Liquid-based cooling

- Hybrid cooling systems

- Variant

- Hyperscale data centers

- Colocation data centers

- Enterprise data centers

- Edge data centers

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- Middle East and Africa

- North America

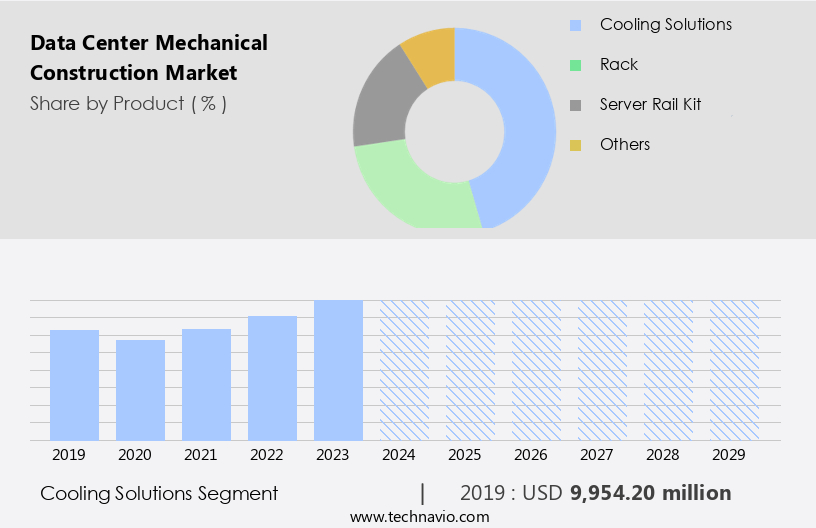

By Product Insights

The cooling solutions segment is estimated to witness significant growth during the forecast period. Data centers require efficient cooling solutions to manage the heat load generated by their IT equipment. Air-based cooling and liquid-based cooling are two primary cooling techniques used. Air-based cooling, a traditional method, utilizes air as a cooling medium. CRAC units, such as air conditioners, air economizers, air-based chiller units, and air-cooled self-contained systems, are commonly used in data centers for air-based cooling. HVAC systems, including air handling units and airflow management, are integral components of infrastructure that support air-based cooling. Liquid-based cooling, on the other hand, uses water or other liquids as a cooling medium. Project management, sustainability, energy efficiency, and renewable energy sources are key considerations for these projects

This method is gaining popularity in large-scale, hyperscale centers due to its higher energy efficiency. Precision cooling, which is a type of liquid-based cooling, ensures optimal temperature and humidity levels for IT equipment. Design plays a crucial role in cooling efficiency. Construction management and project management are essential in implementing energy-efficient cooling systems during the planning and building stages. Commissioning and monitoring ensure that cooling systems function optimally. Certifications, such as LEED and Water Usage Effectiveness, encourage the adoption of energy-efficient cooling technologies. ASHRAE standards provide guidelines for cooling systems, ensuring reliability and capacity planning.

Fire suppression and security systems are integral to operations. Upgrades and migrations require careful planning and implementation to minimize downtime and ensure data security. Analytics and building automation facilitate the optimization of cooling systems, reducing energy consumption and improving overall efficiency.

Get a glance at the market report of share of various segments Request Free Sample

The Cooling solutions segment was valued at USD 9.95 billion in 2019 and showed a gradual increase during the forecast period.

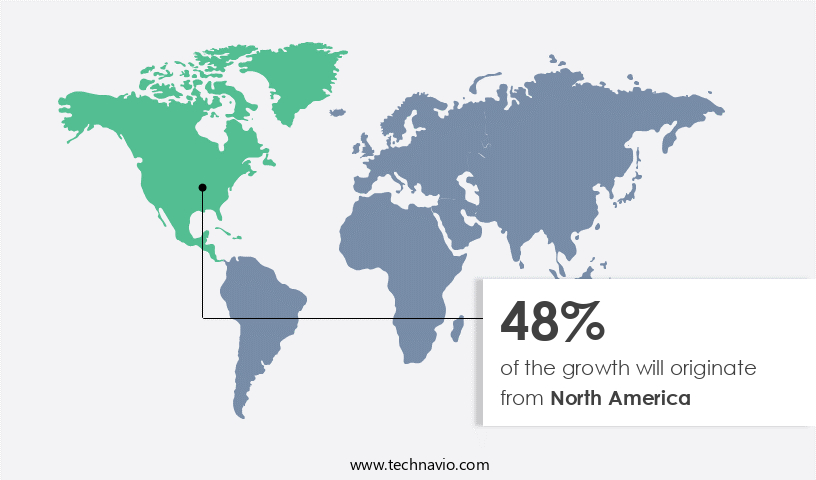

Regional Analysis

North America is estimated to contribute 48% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

In North America, the increase in establishments necessitates substantial investments in IT infrastructure and power and cooling solutions. This trend is driven by the increasing demand for Internet of Things (IoT) devices and the implementation of autonomous technologies across industries. IoT devices, with their high demand in the region due to a well-established communication network infrastructure, require efficient data processing and storage capabilities. Simultaneously, industries are adopting automation technologies to boost operational efficiency, enhance product quality, and minimize manufacturing errors. Moreover, significant investments in Artificial Intelligence (AI) in North America are fueling the development of products capable of processing vast amounts of data and facilitating M2M communication efficiently. The market is experiencing significant growth due to the increasing demand to support digital transformation and the adoption of high-performance computing (HPC) applications.

The energy efficiency is a critical concern, with Power Usage Effectiveness (PUE) and cooling technologies playing pivotal roles. Construction management, commissioning, and monitoring are essential aspects of infrastructure development. Edge computing, mechanical systems integration, and high availability HVAC systems are crucial components of design and operation. Certifications, such as LEED and ASHRAE standards, are increasingly important for sustainability and energy efficiency. Capacity planning, water conservation, and fire suppression systems are essential for optimization and resilience. Data center upgrades, security systems, and analytics are integral to maintaining and enhancing performance.

Critical power systems, UPS systems, and cloud computing are essential elements of electrical infrastructure. Precision cooling, project management, and building automation are vital for efficient operations. Air handling units and airflow management are crucial for maintaining optimal IT load and ensuring high availability. Data center decommissioning and design are essential aspects of data center lifecycle management.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Data Center Mechanical Construction Industry?

- Increased adoption of HPC across enterprises is the key driver of the market. The data traffic growth and the complexities of managing vast data volumes have fueled the intersection of big data and supercomputing. Commercial web applications' expansion, cloud computing advancements, and Human-Machine Interface (HMI) technology development are key factors propelling the High Performance Computing (HPC) market's expansion within the IT sector. Business and consumer applications generate massive amounts of structured and unstructured data, which enterprises store on-premises and in the cloud. These organizations leverage the data to gain insights and make critical operational and managerial decisions. To process this data more efficiently, firms are integrating HPC systems into their IT infrastructure. Traditional computing systems struggle to process such large volumes of data, making HPC integration an attractive solution for faster, more efficient data processing. This innovative design offers significant advantages in terms of flexibility, scalability, and cost-effectiveness. The construction of hyperscale data centers represents a crucial development in the realm of data management and processing. The ability to accommodate large amounts of data and provide efficient, scalable solutions makes these facilities an indispensable asset for businesses in today's data-driven world.

What are the market trends shaping the Data Center Mechanical Construction Industry?

- Growing investment in hyperscale data centers is the upcoming market trend. Hyperscale data centers are becoming increasingly essential for organizations handling large volumes of data. These data centers feature a design that allows for a single, massive, and scalable computer, composed of interconnected nodes operating as one machine. The growing need to manage escalating data generation has led to a significant increase in the construction of hyperscale data centers. These facilities require extensive storage capabilities and, consequently, numerous racks to integrate servers, storage devices, and network equipment. Hyperscale data centers employ new server designs and wider racks to accommodate an increased number of components. The integration of these advanced technologies results in a more efficient and effective data processing and storage solution. The massive scale of hyperscale data centers necessitates a unique architecture that can cater to the demands of handling vast amounts of data. By clustering small individual servers together, organizations can benefit from the combined processing power and storage capacity of the entire system.

What challenges does the Data Center Mechanical Construction Industry face during its growth?

- High power consumption in data centers is a key challenge affecting the industry growth. The market is experiencing significant growth due to several factors. Increasing internet penetration and the expanding use of social media are driving up data traffic, necessitating the construction of larger data centers for managing and storing vast amounts of data. Additionally, the rise of blockchain technology, automation technologies, smart city initiatives, and artificial intelligence (AI) implementation across industries are further boosting market growth. However, this growth comes with a substantial energy consumption challenge. Data centers are projected to become the largest global energy consumers by 2030, with the ICT sector accounting for approximately 23% of the world's electricity usage. Within a data center, servers and cooling solutions consume more electricity than any other infrastructure. The market is experiencing significant growth due to the increasing demand for data-intensive applications, cloud computing, and digital services.

Exclusive Customer Landscape

The data center mechanical construction market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the data center mechanical construction market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, data center mechanical construction market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - The company specializes in constructing data centers, delivering hyperscale infrastructure solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Black Box Corp.

- Chatsworth Products Inc.

- Dell Technologies Inc.

- Delta Electronics Inc.

- Eaton Corp. plc

- Equinix Inc.

- Friedhelm Loh Stiftung and Co. KG

- Green Revolution Cooling Inc.

- Legrand SA

- LiquidStack BV

- Munters Group AB

- NetRack Enclosures Pvt. Ltd.

- Nortek Air Solutions LLC

- Schneider Electric SE

- STULZ GmbH

- Submer Technologies SL

- Vertiv Holdings Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is experiencing significant growth as businesses prioritize digital transformation and the demand for data processing continues to rise. This sector encompasses various components essential to the efficient and reliable operation of data centers, including thermal management, power usage effectiveness, and mechanical systems integration. Thermal management is a critical aspect of data center design, as managing heat load is crucial to maintaining optimal operating conditions. Power usage effectiveness (PUE) is a widely adopted metric for measuring data center efficiency, with lower PUE values indicating better energy utilization. Data center relocation and the adoption of modular and smart data centers are also driving the need for advanced thermal management solutions. Data centers consume vast amounts of electricity, and cooling systems account for a significant portion of this energy usage.

Construction management plays a pivotal role in the data center infrastructure development process. Proper planning, commissioning, and monitoring are essential to ensuring data center reliability and capacity. Water conservation and optimization are increasingly important considerations, as data centers consume vast amounts of water for cooling purposes. Energy efficiency is a significant focus in the data center industry, with hyperscale data centers leading the charge. Cooling technologies, such as precision cooling and airflow management, are essential for maintaining energy efficiency and reducing heat load. Electrical infrastructure, including critical power systems and uninterruptible power supply (UPS) systems, is another crucial component of data center design. The expanding adoption of advanced technologies, such as cloud-based services and big data analytics, by communication service providers (CSPs), government agencies, and businesses is driving the demand for data centers.

Data center security, fire suppression, and data center certifications, such as LEED and ASHRAE standards, are essential for ensuring business continuity and regulatory compliance. Capacity planning, data center optimization, and maintenance are ongoing concerns for data center operators, with edge computing and cloud computing adding complexity to the landscape. Data center upgrades and migrations, as well as the integration of building automation and HVAC systems, require careful project management. The role of IT load and high availability in data center operations is increasingly important, with data center analytics and artificial intelligence (AI) playing a growing role in optimizing performance and reducing downtime.

In the data center market, there is a constant focus on improving efficiency, reliability, and sustainability. Mechanical systems integration, including the use of CRAC units and air handling units, is a key area of innovation, with smart technologies and automation driving advancements. Data center design and optimization are ongoing concerns, with a growing emphasis on water usage effectiveness and data center resilience. The data center industry is a dynamic and complex landscape, with ongoing evolution in technology, design, and operations. Effective project management, careful planning, and a focus on energy efficiency, reliability, and sustainability are essential for success in this market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

233 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 16.1% |

|

Market growth 2025-2029 |

USD 22.92 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

13.5 |

|

Key countries |

US, Canada, China, Japan, India, UK, Brazil, Germany, France, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Data Center Mechanical Construction Market Research and Growth Report?

- CAGR of the Data Center Mechanical Construction industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the data center mechanical construction market growth and forecasting

We can help! Our analysts can customize this data center mechanical construction market research report to meet your requirements.

RIA -

RIA -