Enjoy complimentary customisation on priority with our Enterprise License!

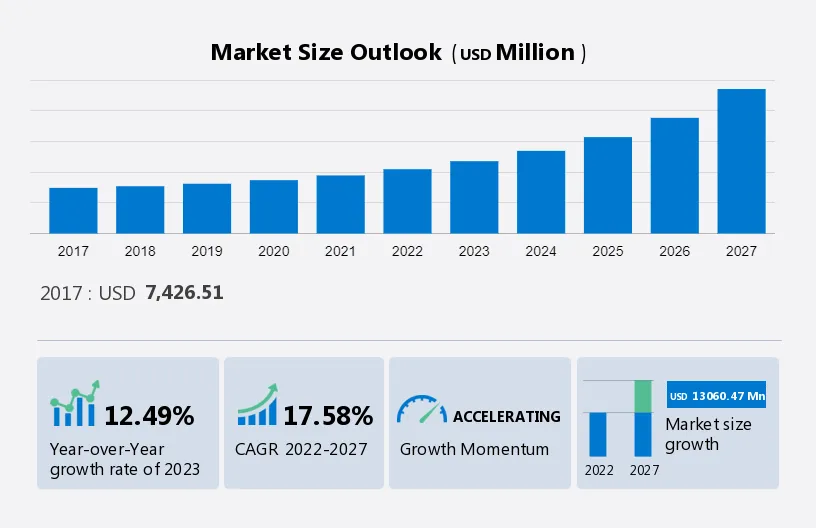

The gaming simulators market size is estimated to grow by USD 13.06 billion at a CAGR of 17.58% between 2022 and 2027. The integration of gaming simulators with VR headsets enhances the immersive experience for gamers, driving demand for more advanced gaming setups. The increasing sophistication of games, including realistic graphics and complex gameplay, is driving the adoption of gaming simulators that can provide a more immersive and engaging experience. Gaming simulators that provide the ultimate gaming experience, with realistic controls and feedback, are attracting gamers looking for a more authentic gaming experience.

This market research report extensively covers market segmentation by component (hardware and software), end-user (commercial and residential), type (racing, shooting, and flight), and geography (North America, Europe, APAC, South America, and Middle East and Africa).

The market share growth by the hardware segment will be significant during the forecast period. Hardware development has been rapid since 2010. An increasing number of companies, such as Vertuix are investing heavily in hardware to build a better interface to complement the core software.

Figure 1: Market by Component (2017-2027)

Get a glance at the market contribution of various segments View the PDF Sample

The hardware segment was valued at USD 5.03 billion in 2017. The focused market has relatively high hardware investments. The investments are used to enhance the experience of users. Since 2010, there has been a transition from PC to mobile gaming to virtual reality (VR) headsets to simulators. A major factor for the seamless transition is the improving hardware standards that provide gamers with the ideal platform to enjoy gaming. Thus, various companies have been adopting new business strategies for launching new hardware components that will support enhanced experience. Therefore, the segment will show growth during the forecast period.

Based on end-user, the commercial segment holds the largest market share. The commercial user's segment uses simulators as a capital investment. As the product is not affordable for the majority of the population, only interested people can experience simulation at commercial places. The market is growing as an increasing number of consumers are finding value in the product. The market is a niche market, especially in APAC. In APAC, the availability of the product is less, despite the population being enthusiastic about the gaming experience. During the forecast period, we expect the availability of simulators to increase as many businesses are buying the product. This will help the market grow and will compel businesses to reduce their profit margins.

Based on type, the racing segment holds the largest market share. Racing games are played either from the first-person perspective or a third-person perspective. In the case of simulators, racing games are only played from the first-person perspective. The gameplay will have the gamer drive a car in the virtual world using hardware. The hardware used is the racing simulator, which is a prototype of the original car equipment. One of the major factors driving the global gaming simulators market by racing is the high demand for F1. Fans who are passionate about F1 and want to experience racing are willing to pay a premium price for racing simulators. G-force simulation is expected to attract more users as it is a parameter that is only theoretically known to fans who watch F1 racing. With the high penetration of motion simulation, the interest among F1 fans will likely increase.

Figure 2: Market by Region

For more insights on the market share of various regions Download PDF Sample now!

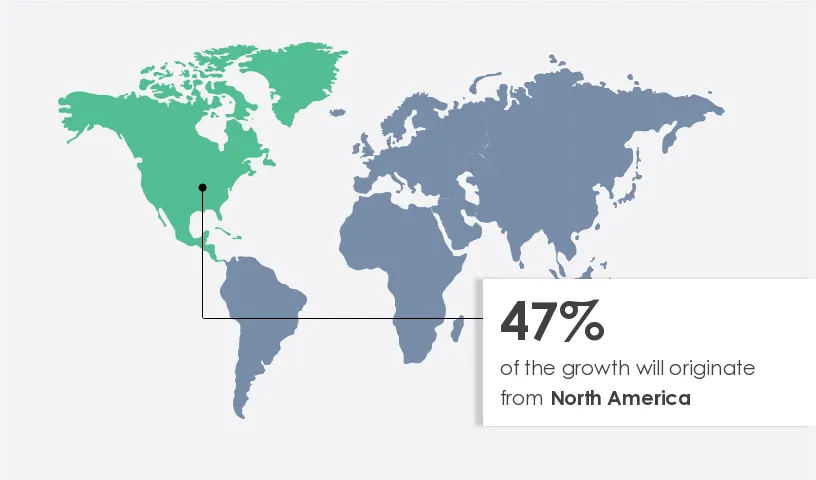

North America is estimated to contribute 47% to the growth of the market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The major factor contributing to its large market size is the high average disposable income of the population in North America. This has increased the spending capability of people and has made simulators more affordable for the population.

The popularity of e-sports leagues is driving the growth of the market in North America. The popularity of e-sports has been driven by the availability of channels, such as Twitch and YouTube, which Provides free telecast of e-sports. In addition, e-sports gamers are receiving visas similar to professional athletes in the US, which is encouraging enthusiasts to take up e-sports professionally. As a result, the region is witnessing an increasing number of investments in the opening of new e-sports arenas. Furthermore, growing investments and business strategies by these companies will propel the growth of the regional market in focus during the forecast period.

The market is experiencing significant growth driven by the increasing popularity of virtual reality (VR) and simulation games. Products like the Next Level Racing F-GT Lite and the Roto VR Chair are revolutionizing the gaming experience. With the rise of high-speed internet networks, gamers can enjoy these simulators at home or in places like amusement parks and theme parks. VR headsets and touch devices enhance gameplay, making popular games more immersive. This surge in demand is also seen in training programs for pilots and drivers, where simulators offer realistic experiences aided by technological advancements like augmented reality and high-fidelity simulations, ensuring compliance with stringent safety regulations. Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Gaming simulators integrated with VR headsets are the key factors driving the market growth. Virtual reality (VR) provides an immersive environment for gamers, enhancing their experience by allowing them to be fully engaged in the game without distractions. Understanding simulation games, actions, and game progression is crucial for developing more immersive and engaging gaming experiences. Technological advancements in VR have led to more realistic graphics, improved motion tracking, and enhanced audio, further enhancing the immersion. Augmented reality (AR) is also becoming increasingly popular, blending virtual elements with the real world to create unique gaming experiences. High-fidelity simulations in VR allow for realistic training scenarios, benefiting industries such as healthcare, aviation, and military training. VR headsets can serve as a cost-effective alternative to expensive LED screens. The rising integration of these simulators with VR headsets is expected to boost the market. As VR headsets become more prevalent, consumers are gaining a better understanding of their capabilities and ease of use, making them more inclined to use VR headsets for gaming.

Acceptance of 360-degree camera as next-generation technology in the market is a key market trend. Technological advances in the global VR content market have led to the introduction of 360-degree videos. VR is considered a mainstream gaming platform in the entertainment domain and is making its way to various digital arenas. The concept of VR with these simulators is rapidly growing, and it is one of the leading technological transformations in the gaming world.

The addition of a 360-degree field of vision to the VR headset enhances the QoE of the gaming simulator. Gamers get not only a front view but also a 360-degree view of the VR environment. With tech giants like Facebook launching its flagship VR device Oculus Rift, Sony launching Morpheus, and HTC launching Vive, VR integration with 360-degree content and these simulators will experience increased growth during the forecast period. The next iteration of the virtual car mechanic simulation from Red Dot Games and PlayWay will be released in August 2021. This Car Mechanic Simulator will allow players to build a garage and make it their own. Besides, there are over 72 different vehicles to repair, fix, test, paint, tune, and rebuild with VR.

Gaming simulators are expensive, which is a major factor hindering the market. The primary challenge for the market is that the product is pricing out the majority of the middle-class population. Simulators are predominantly used in commercial places as owning one is not a financially viable option for over 99% of the population. An average gamer that wants to experience gaming using a gaming simulator will need to pay a price premium to play for a limited time. In commercial places, an average gamer cannot fully enjoy the simulation experience because he can only afford a limited time. This is more common in Asia, where the demand for such a gaming experience is high, but the average disposable income is relatively low.

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the gaming simulation market.

Eleetus- The company offers gaming simulators such as Realistic G.

The research report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

3D perception AS, Adacel Technologies Ltd., Aero Simulation Inc., Atomic Motion Systems, BLUEHALO LLC, CKAS Mechatronics Pty Ltd, Cruden, CXC Simulations, D BOX Technologies Inc., Eleetus LLC, GTR Simulators, Guillemot Corp. SA, Hammacher Schlemmer and Co. Inc., Lean Games Ltd., Playseat BV, RSEAT Ltd., Simtechpro SL, SimXperience, Sony Group Corp., and Vesaro Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

The market is thriving with the increasing demand for stress busters and immersive gaming experiences. Game hubs and privacy and security concerns are driving the market growth. Technologies like cloud computing and gesture-based gaming are revolutionizing the industry. Leading companies like Velocità Racing Simulator and Full Swing Golf are pushing boundaries with innovative products. The market offers a wide range of game genres, catering to various preferences. With the rise of smartphones and AR and VR headsets, the market is witnessing a surge in mobile gaming and live gaming experiences. The market's future looks promising with advancements in AI and ML algorithms, haptic feedback systems, and the development of the metaverse.

The market is evolving rapidly with advancements in technology and a focus on providing immersive experiences. Simulators offer a controlled and risk-free environment for trainees to develop their decision-making abilities in diverse scenarios. Virtual reality (VR) technologies cater to a wide range of sectors, including aerospace, automotive, and maritime, offering advanced training solutions such as the Full Mission Bridge Simulator for the maritime and aviation sectors. These technologies have seen significant advancements, including improved graphics and advanced training solutions, making them valuable tools for industries requiring immersive training experiences, particularly in the maritime and aviation sectors.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

167 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 17.58% |

|

Market growth 2023-2027 |

USD 13.06 billion |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

12.49 |

|

Regional analysis |

North America, Europe, APAC, South America, and Middle East and Africa |

|

Performing market contribution |

North America at 47% |

|

Key countries |

US, China, Japan, UK, and Germany |

|

Competitive landscape |

Leading companies, Market Positioning of companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

3D perception AS, Adacel Technologies Ltd., Aero Simulation Inc., Atomic Motion Systems, BLUEHALO LLC, CKAS Mechatronics Pty Ltd, Cruden, CXC Simulations, D BOX Technologies Inc., Eleetus LLC, GTR Simulators, Guillemot Corp. SA, Hammacher Schlemmer and Co. Inc., Lean Games Ltd., Playseat BV, RSEAT Ltd., Simtechpro SL, SimXperience, Sony Group Corp., and Vesaro Ltd. |

|

Market dynamics |

Parent market analysis, Market Forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements.

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Component

7 Market Segmentation by End-user

8 Market Segmentation by Type

9 Customer Landscape

10 Geographic Landscape

11 Drivers, Challenges, and Trends

12 Vendor Landscape

13 Vendor Analysis

14 Appendix

Get lifetime access to our

Technavio Insights