Enjoy complimentary customisation on priority with our Enterprise License!

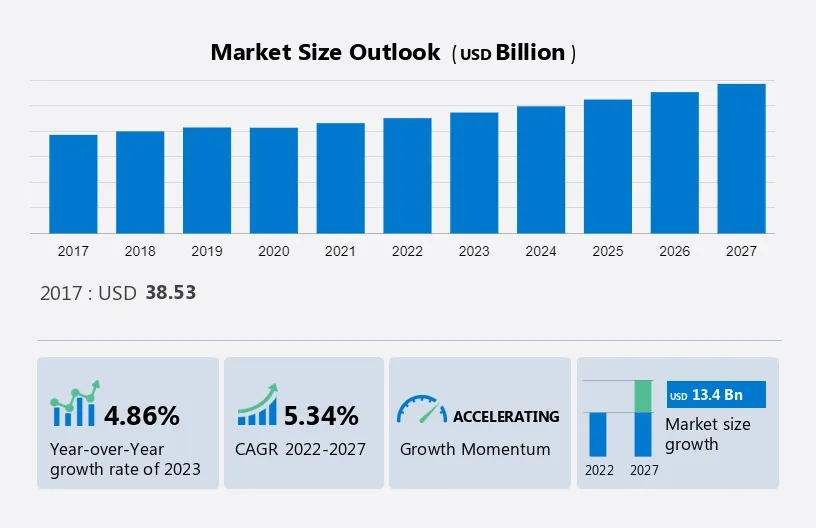

The electronic chemicals and materials market size is estimated to grow at a CAGR of 5.34% between 2022 and 2027. The market size is forecast to increase by USD 13.4 billion. The growth of the market depends on several factors, including the development of upgraded applications in the electronics industry, advances in materials, and the growing demand for silicon wafers.

This electronic chemicals and materials market report extensively covers market segmentation by application (IC manufacturing, PCB manufacturing, and semiconductor packaging), product (wafers, atmospheric and specialty gases, ancillary and photoresist chemicals, CMP slurries and pads, and others), and geography (APAC, North America, Europe, South America, and Middle East and Africa). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

To learn more about this report, View Report Sample

The development of upgraded applications in the electronics industry is notably driving the market growth, although factors such as the slowdown in the semiconductor industry growth the market growth. Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The development of upgraded applications in the electronics industry is the key factor driving the growth of the global electronic chemicals and materials market. Advancements in the electronics industry, such as 3D printing, drones, claytronics, aerogels, and conductive polymers, require faster, smaller, and cheaper electronics. Recent technological advances and improvements to existing equipment used to manufacture chemicals and materials have improved the quality and performance of consumer electronics. The cost of producing electronic devices is dropping, and the introduction of new devices is increasing.

Market vendors are developing strategies to meet the growing demand for advancements in electronics. The use of flat screens, such as LCD, LED, plasma screens, etc., is increasing. These displays are used in mobile phones, computers, and other devices. Various chemicals and materials are required to manufacture and process these displays. Therefore, increasing the adoption of these displays is expected to boost the market growth during the forecast period. Also, new applications of polymers for electrical and electronic applications are expected to contribute to the growth of the global electronic chemicals and materials market.

The increasing number of fabs is the primary trend in the global electronic chemicals and materials market. Semiconductor products such as ICs, PCBs, and others are either developed in-house by companies known as IDMs or manufactured according to designs that customers provide to pure foundries. The demand for manufacturing multiple semiconductor components and products used in Internet of Things (IoT) devices is expected to increase the demand for multiple electronic chemicals and materials such as wafers. Thus, the demand for new fab construction is expected to increase as semiconductor product makers increasingly focus on introducing new technologies to stay competitive. This is expected to drive demand for new high-value electronic chemicals and materials.

In addition, the growing demand for sensor systems, consumer electronics, medical devices, and IoT connectivity devices has significantly increased the demand for semiconductor wafers. To meet this huge demand for semiconductor products, semiconductor manufacturers are increasing the throughput of their production facilities or building new fabs. For example, in April 2021, electronics manufacturer Samsung Electronics Co. Ltd. announced its plans to invest approximately USD 115 billion in foundry and chip businesses by 2030. The semiconductor contract manufacturing and design firm has announced plans to build and operate an advanced semiconductor manufacturing facility in the United States. The company had planned to spend about USD 12 billion, including capital expenditures, on the project between 2021 and 2029. The steady development of these new factories for semiconductor products is expected to boost demand for electronic chemicals and electronic materials during the forecast period.

The slowdown in the semiconductor industry is a major challenge impeding the growth of the global electronic chemicals and electronic materials market. Market dynamics have changed significantly in some industries, such as semiconductors and automotive, and manufacturers are beginning to feel the effects of excessive demand volatility. The declining demand for consumer electronics and automobiles and a global shortage of skilled workers will have a direct impact on the profitability of manufacturing companies. Thus, sudden and unexpected changes in market dynamics can have a significant impact on manufacturing processes and investments in capital goods.

The escalating trade war between China and the United States and the global impact of the COVID-19 pandemic are expected to affect global production across the semiconductor industry. Additionally, large inventories of smartphones and cloud infrastructure have led to price pressures, negatively impacting sales across the semiconductor industry. The tariff war between the US and China has hit electronics companies in both countries hard. Each country has a concentration of electronic equipment manufacturers (OEMs). Rising electronics prices will therefore affect the growth of the semiconductor industry in these countries. Such an unfavorable scenario is impacting his CAPEX of new manufacturing facilities, thereby negatively impacting demand for all types of electronic chemicals and materials in the market. Additionally, the outbreak of the COVID-19 pandemic has negatively impacted demand for all types of consumer electronics, especially in the first half of 2020. Most of the major manufacturing activities around the world stopped in the first quarter of 2020 due to the rising number of COVID-19 cases. Therefore, the market demand for electrochemicals and materials is expected to grow slowly over the forecast period.

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Electronic Chemicals and Materials Market Customer Landscape

Vendors are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product launches, to enhance their presence in the market.

Air Liquide SA: The company offers advanced electronics and materials such as Voltaix and ALOHA deposition precursors and enScribe etchants.

The report also includes detailed analyses of the competitive landscape of the market and information about 15 market vendors, including:

Qualitative and quantitative analysis of vendors has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize vendors as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize vendors as dominant, leading, strong, tentative, and weak.

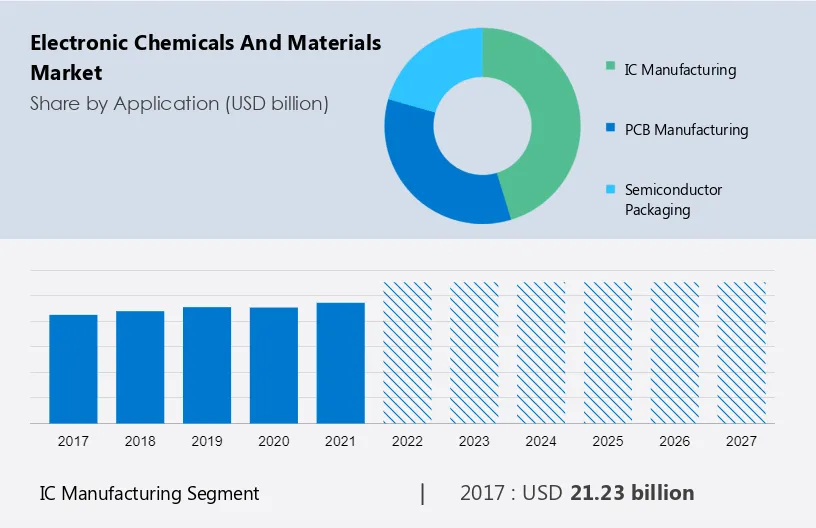

The market share growth by the IC manufacturing segment will be significant during the forecast period. ICs, also called chips or microchips, are semiconductor wafers in which multiple components such as diodes, resistors, transistors, and external connections are fabricated on very small silicon chips. All circuit components and connections are formed on a single thin wafer called a monolithic IC. In an IC chip, all circuit elements and their interconnections are manufactured at the same time. Wafer fabrication, masking, etching, doping, atomic diffusion, ion implantation, metallization, and assembly and packaging are critical steps in IC manufacturing.

Get a glance at the market contribution of various segments View the PDF Sample

The IC manufacturing segment was valued at USD 21.23 billion in 2017 and continued to grow until 2021. Suppliers such as The Linde Group, Air Products, Cabot Microelectronics, and Solvay offer a wide range of electronic chemicals and materials for IC manufacturing. Solvay offers electronics-grade sulfur hexafluoride (SF6) used in the manufacture of semiconductor devices, including ICs. SF6 is mainly used as an etching gas during IC manufacturing. Due to its density and large molecular size, SF6 is largely accepted as the preferred etching gas for consumers. Similarly, Air Products develops and supplies several electronic chemicals and materials that an electronic device maker uses in his IC manufacturing. The company provides gases for IC manufacturing and packaging. The company is focused on developing high-quality gases that improve performance by reducing defects and total cost of ownership for consumers involved in IC manufacturing, assembly, and packaging. Rising demand for electronic devices, coupled with rapid urbanization, is expected to drive demand for a wide range of electronic chemicals and IC manufacturing materials. This will drive the growth of the segment in the global electronic chemicals and materials market during the forecast period.

For more insights on the market share of various regions Download PDF Sample now!

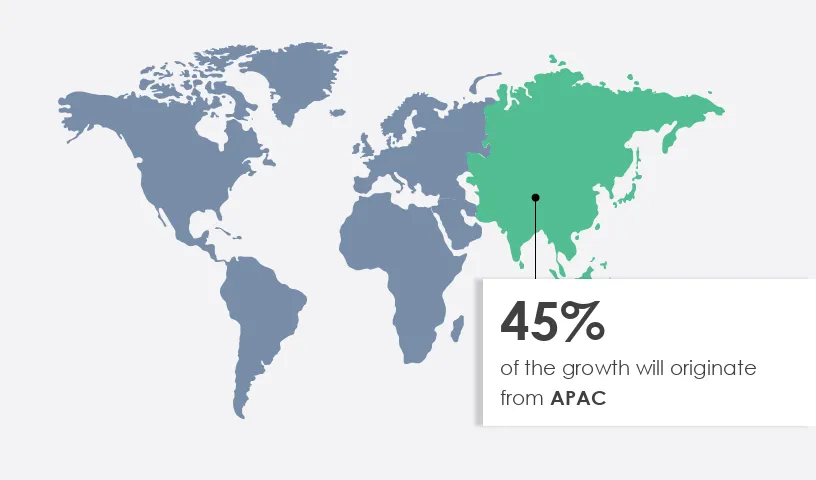

APAC is estimated to contribute 45% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. Population growth coupled with urbanization and industrialization are expected to increase growth opportunities for the electronic chemicals and materials market in APAC countries. The urban population of several countries in the Asia-Pacific region has increased significantly in recent years. According to the World Bank Group, Japan, Singapore, Australia, and China will account for 92%, 100%, 86%, and 60% of the total urban population, respectively, in 2021. This will propel the growth of the APAC electrochemical and materials market during the forecast period.

APAC is a manufacturing hub for manufacturers of power electronics, optoelectronics, logic, memory devices, and more. For example, Semiconductor Manufacturing International Corp., Taiwan Semiconductor Manufacturing Co. Ltd., Samsung Electronics Co. Ltd., etc., and United Microelectronics Corporation. Semiconductor manufacturing divisions in South Korea, Taiwan, and China. The market for electronic chemicals and materials in the region has great potential due to the presence of several consumer electronics suppliers. Many providers are available in Japan, China, and South Korea. In addition, the region has a high concentration of consumer electronics manufacturers, and the demand for integrating semiconductor ICs into consumer electronics is expected to increase.

This report forecasts the contribution of all the segments to the growth of the market. In addition, we have included the COVID-19 impact and the recovery strategies for each segment. In 2020, the regional electronic chemicals and materials market was adversely affected by COVID-19. Governments in APAC countries such as India, China, Japan, Australia, and Indonesia have imposed nationwide lockdowns to curb the spread of the disease. This has resulted in the temporary closure of several manufacturing industries, including electronic chemicals and materials production plants, and some reduction in the region's electronic chemicals and materials production, especially in the first half of 2020. With the arrival of vaccination campaigns to resume in the first half of 2021, the demand for electronic chemicals and materials increased in the region. In addition, rising demand for semiconductor ICs by end-users such as automotive equipment and consumer electronics manufacturers, rapid urbanization, and growing interest in technological advancements will boost the APAC electrochemical and materials market growth during the forecast period.

The electronic chemicals and materials market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

Technavio categorizes the global electronic chemicals and material market as a part of the global commodity chemicals market within the global chemicals market. The global commodity chemicals market covers companies that primarily produce industrial and basic chemicals, including, but not limited to, plastics, synthetic fibers, films, commodity-based paints and pigments, explosives, and petrochemicals. The market excludes chemical companies that produce diversified chemicals, fertilizers and agricultural chemicals, industrial gases, and specialty chemicals. Our market research report has extensively covered external factors influencing the parent market growth during the forecast period.

|

Electronic Chemicals and Materials Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

189 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.34% |

|

Market growth 2023-2027 |

USD 13.4 billion |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

4.86 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 45% |

|

Key countries |

US, China, Japan, South Korea, and Germany |

|

Competitive landscape |

Leading Vendors, Market Positioning of Vendors, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Air Liquide SA, Air Products and Chemicals Inc., Asahi Kasei Corp., Ashland Inc., BASF SE, Covestro AG, Dow Chemical Co., DuPont de Nemours Inc., Entegris Inc., FUJIFILM Corp., Honeywell International Inc., Huntsman International LLC, LG Corp., Linde Plc, Mitsubishi Chemical Corp., Puyang Huicheng Electronic Material Co. Ltd., Saudi Arabian Oil Co., Shin Etsu Chemical Co. Ltd., Solvay SA, and Resonac Holdings Corp. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements.

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Application

7 Market Segmentation by Product

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights