Enjoy complimentary customisation on priority with our Enterprise License!

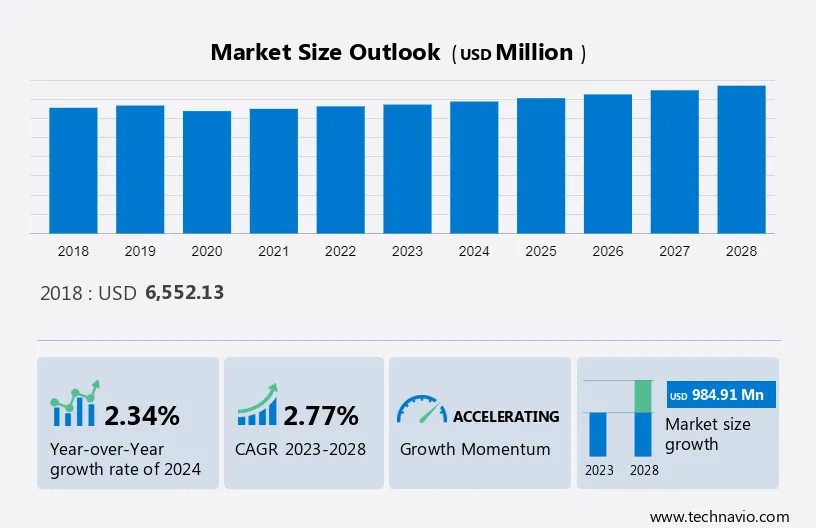

The semiconductor fabrication software market size is estimated to grow at a CAGR of 2.77% between 2023 and 2028. The market size is forecast to increase by USD 984.91 million. The growth of the market depends on several factors, including the growing complexity of semiconductor device designs, the increasing requirement for SoC technology, and the demand for miniaturized electronic devices of high precision across sectors. Semiconductor fabrication software comprises design software tools and production software tools. EDA is a software tool that is used to design electronic systems. It can vary from computer or mobile device chips to chips used in satellites. The value of EDA tools is increasing over time due to the growing complexity of electronics. The growth of SoC circuits involves integrating multiple components on a chip while production software tools are used in the manufacturing of semiconductor devices.

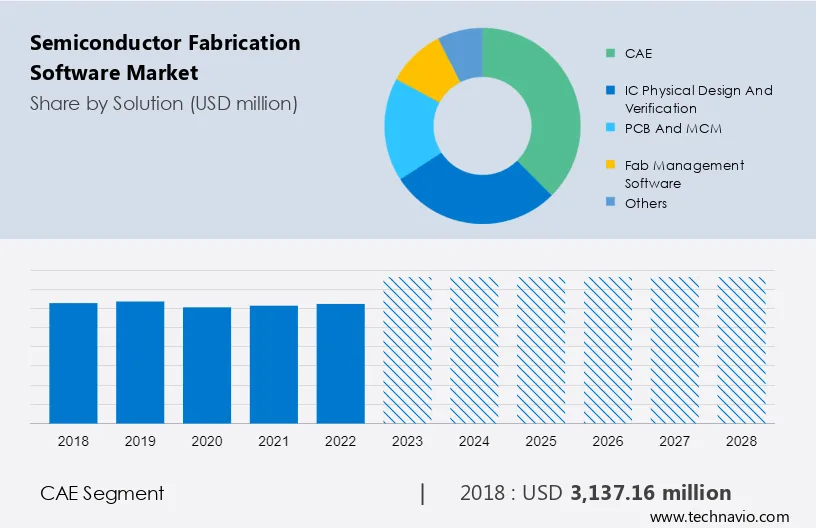

The report offers extensive research analysis on the Semiconductor Fabrication Software Market, with a categorization based on Solution, including CAE, IC physical design and verification, PCB and MCM, fab management software, and others. It further segments the market by End-user, encompassing process documentation, process integration, and others. Additionally, the report provides Geographical segmentation, covering APAC, North America, Europe, Middle East and Africa, and South America. Market size, historical data (2018-2022), and future projections are presented in terms of value (in USD million) for all the mentioned segments.

For More Highlights About this Report, Download Free Sample in a Minute

The growing complexity of semiconductor device designs is notably driving the market growth. The semiconductor industry has a definite need for high functionality, performance, and bandwidth. The increasing complexity of semiconductor chip design has made the manufacturing process of semiconductor devices complex and complicated. Some major chip makers, such as Intel and Samsung, are trying to avoid this effect by adding more engineers to design teams.

Moreover, semiconductor manufacturers do not differentiate manufacturing but instead focus on functions and performance characteristics to gain a competitive advantage in the market. The complexity of semiconductor design has created a demand for advanced software tools for semiconductor design and manufacturing. Hence, the complexity and smaller footprint of nodes will drive the market during the forecast period

The high need for semiconductor memory devices is the key trend shaping market growth. Semiconductor manufacturers are shifting their focus from logic, analogue, and discrete devices to memory devices such as 3D NAND and dynamic random access memory (DRAM). The main reason for this change is the high growth potential of devices in the semiconductor memory market. This need is complemented by the dynamics of the consumer electronics market, which offers new opportunities for sellers.

Moreover, the additional features such as more resistance to vibration, low chances of corruption due to impact, less possibility of data loss, etc. require precise chip fabrication, for which semiconductor fabrication software solutions are a necessity. OEMs of high-functionality smartphones, tablet PCs, PDAs, and notebooks are expected to launch new products integrated with 3D NAND during the forecast period. Thus, the market is expected to foresee significant growth during the forecast period.

Increasing chip shortage globally is a challenge that affects market growth. A global shortage of chips has affected the electronics industry, limiting the world's ability to produce everything from cars to consumer goods, and driving up prices. Procurement problems are even negatively affecting chip manufacturers, at least indirectly, adding to the confusion in the semiconductor industry.

Moreover, widespread shortages prevent companies from replenishing inventories. In addition, companies ordered more wood chips than needed to build inventories, which squeezed capacity and drove up costs. Many chip manufacturers require consumers to commit to long-term non-cancellable orders to avoid duplicate orders. Thus, such factors may impede the growth of the market during the forecast period.

The market share growth by the CAE segment will be significant during the forecast period. The CAE segment refers to a particular software used for engineering tasks. This segment includes tools such as electronic system level (ESL), register transfer level (RTL) simulation, hardware-assisted verification, analysis tool, synthesis, analogue and mixed signal simulator, formal verification, design input, and logic and formal verification. ESL tools play a vital role in this segment as it is the fastest-growing segment compared to other CAE segment.

Get a glance at the market contribution of various segments Download the PDF Sample

The CAE segment showed a gradual increase in the market share of USD 3,137.16 million in 2018. The CAE segment will witness slow growth as most users already own licenses for EDA software due to the contractual business model adopted by the EDA players. These tools are used for solving partial differential equations and boundary values problems deriving algorithms to deal with problems in fluid flows or carrying out flight tests. Thus, due to such factors, the CAE segment will grow at a moderate rate during the forecast period.

Process documentation is required as companies that manufacture semiconductors must exert every effort to maintain their flow and focus as complexity and costs rise. As companies get closer to launch, they need to reduce the chance that their product will fail and keep investors confident. Companies organize operations to provide the desired, high-quality outputs by imposing document controls with the correct software solution. They can help maintain a laser-like focus on consumer needs and give the tools needed to constantly enhance the caliber. The risk of process gaps, delays, and errors can be reduced by automating these procedures with the appropriate software, which can also help optimize the entire process, leading to the increased demand for semiconductor fabrication software solutions during the forecast period.

For more insights on the market share of various regions Download PDF Sample now!

APAC is estimated to contribute 52% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. The APAC region has transformed itself into an electronics manufacturing hub. Most of the major countries in the region, such as Japan, South Korea, Taiwan, and China, are known for their electronic device manufacturing capabilities.

In addition, developing countries such as India are also treading the same path with the emergence of several home-grown brands such as Micromax. The Indian government has also started the Make in India initiative to promote manufacturing in the country. This initiative will likely give a boost to the manufacturing sector in the region, creating the need for semiconductor fabrication software solutions during the forecast period.

The Semiconductor Fabrication Software Market report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Semiconductor Fabrication Software Market Customer Landscape

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The research report also includes detailed analyses of the competitive landscape of the market and information about 20 market companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The semiconductor fabrication software market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2018 to 2028

|

Semiconductor Fabrication Software Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

180 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.77% |

|

Market Growth 2024-2028 |

USD 984.91 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

2.34 |

|

Regional analysis |

APAC, North America, Europe, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 52% |

|

Key countries |

US, China, India, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Advanced Micro Devices Inc., Agnisys Inc., Aldec Inc., ANSYS Inc., Applied Materials Inc., Cadence Design Systems Inc., KLA Corp., Lam Research Corp., Onto Innovation Inc., PDF Solutions Inc., Sasken Technologies Ltd., Siemens AG, Synopsys Inc., The PEER Group Inc., Thermo Fisher Scientific Inc., Zuken Inc., Cantier Systems Pte Ltd., Fabmatics GmbH, Mindteck India Ltd., and Tismo Technology Solutions Pvt. Ltd. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements.

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Solution

7 Market Segmentation by End-user

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.