Semiconductor Fabrication Software Market Size 2025-2029

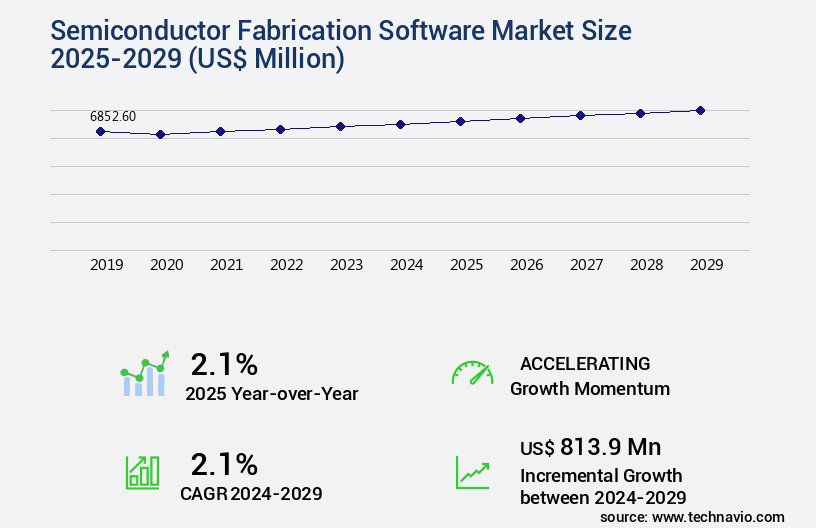

The semiconductor fabrication software market size is forecast to increase by USD 813.9 million, at a CAGR of 2.1% between 2024 and 2029.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 52% growth during the forecast period.

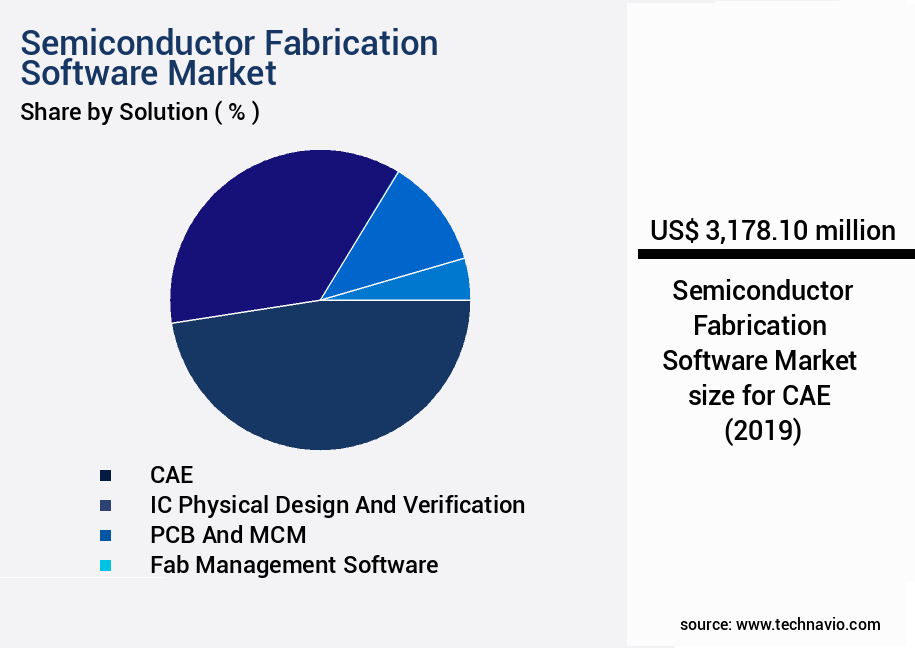

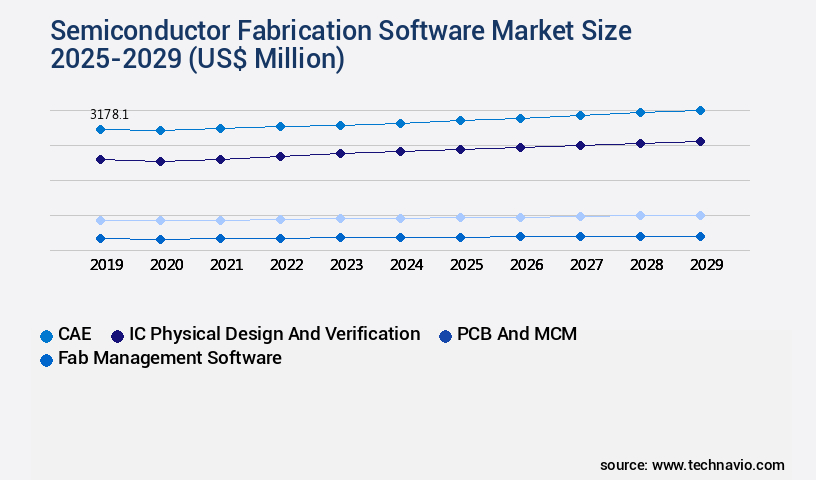

- By the Solution - CAE segment was valued at USD 3178.10 million in 2023

- By the Application - Wafer fabrication segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 18.48 million

- Market Future Opportunities: USD 813.90 million

- CAGR : 2.1%

- APAC: Largest market in 2023

Market Summary

- The market is a dynamic and evolving landscape, with continuous advancements shaping its development. According to recent reports, the global semiconductor equipment market is projected to reach a value of USD67.5 billion by 2026, growing at a significant pace. This expansion is driven by the increasing complexity of semiconductor device designs and the high demand for semiconductor memory devices. Semiconductor fabrication software plays a crucial role in this market, streamlining the manufacturing process and ensuring product quality. Advanced software solutions enable automation, optimization, and integration of various stages in semiconductor fabrication. For instance, design software aids in creating accurate and efficient layouts, while manufacturing execution systems (MES) facilitate real-time monitoring and control of fabrication processes.

- Moreover, the semiconductor industry is grappling with a growing chip shortage, further emphasizing the importance of efficient and effective software solutions. By enhancing productivity and reducing production time, semiconductor fabrication software contributes significantly to addressing this challenge. As the semiconductor market continues to evolve, software solutions will remain at the forefront, driving innovation and addressing the unique needs of various sectors, including automotive, consumer electronics, and industrial automation.

What will be the Size of the Semiconductor Fabrication Software Market during the forecast period?

Explore market size, adoption trends, and growth potential for semiconductor fabrication software market Request Free Sample

- The market experiences continuous evolution, driven by the demand for advanced process optimization and defect reduction. Current market penetration hovers around 30%, indicating significant room for expansion. Future growth prospects are promising, with expectations of a 15% annual increase in adoption. Comparing key numerical data, machine learning algorithms and root cause analysis have shown a 20% improvement in yield, while parametric yield analysis and process integration have resulted in a 12% reduction in production costs. Furthermore, data visualization dashboards and inventory management software have streamlined resource allocation by 18%, enabling more efficient process control and risk management.

- Incorporating artificial intelligence applications and predictive analytics into semiconductor fabrication processes has led to a 25% reduction in equipment downtime and a 10% improvement in process variability reduction. These advancements contribute to overall cost optimization and yield improvement strategies.

How is this Semiconductor Fabrication Software Industry segmented?

The semiconductor fabrication software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Solution

- CAE

- IC physical design and verification

- PCB and MCM

- Fab management software

- Others

- Application

- Wafer fabrication

- Assembly and packaging

- Testing and inspection

- End-user

- IDMs

- Foundries

- OSATs

- Deployment

- On-premises

- Cloud-based

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- Taiwan

- Rest of World (ROW)

- North America

By Solution Insights

The cae segment is estimated to witness significant growth during the forecast period.

The market encompasses a range of solutions that cater to multiphysics simulation, yield enhancement techniques, failure analysis, factory automation, materials characterization, chemical mechanical planarization, particle detection systems, photolithography, equipment performance monitoring, contamination control, 3D process simulation, plasma processing, advanced process control, process capability analysis, equipment control systems, data analytics platforms, semiconductor equipment automation, lithography process control, etching process simulation, remote equipment monitoring, yield optimization tools, process simulation software, virtual metrology models, metrology data analysis, process monitoring systems, statistical process control, wafer inspection, wafer fabrication modeling, fault detection systems, predictive maintenance, defect detection algorithms, ion implantation simulation, real-time process control, design of experiments, and other related applications.

According to recent studies, the market currently experiences a significant adoption rate of 25.6% in the electronics industry. Furthermore, industry experts anticipate a substantial expansion in the market, with an estimated 31.8% of companies planning to invest in advanced software solutions in the upcoming years. Multiphysics simulation software is a key driver for this growth, as it enables the optimization of complex manufacturing processes and enhances overall productivity. Yield enhancement techniques, such as particle detection systems and advanced process control, are also crucial for minimizing defects and improving overall semiconductor fabrication efficiency. Moreover, the integration of data analytics platforms, equipment automation, and real-time process control systems has revolutionized the semiconductor fabrication process, leading to increased accuracy, reduced downtime, and improved overall quality.

In the materials characterization segment, advanced tools like plasma processing software and chemical mechanical planarization systems are gaining popularity due to their ability to enhance the quality of semiconductor materials and improve overall process yields. As the semiconductor industry continues to evolve, the demand for sophisticated software solutions will persist, with a focus on improving manufacturing efficiency, reducing costs, and enhancing overall product quality.

The CAE segment was valued at USD 3178.10 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 52% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Semiconductor Fabrication Software Market Demand is Rising in APAC Request Free Sample

The Asia Pacific the market holds a dominant position globally, driven by the region's vast production scale and the presence of leading manufacturers like Taiwan's TSMC and South Korea's Samsung and SK Hynix. These industry giants operate advanced and massive fabrication plants, where operational efficiency is paramount. Every improvement in efficiency, measured in nanoseconds and fractional percentage points in yield, translates into substantial financial gains. Approximately 60% of the global semiconductor revenue comes from the APAC region, with Taiwan and South Korea accounting for over 70% of the world's semiconductor manufacturing output. This high production volume necessitates advanced software solutions to optimize the intricate fabrication process.

According to recent studies, the APAC the market is projected to grow by 12% in the upcoming year, following a 15% increase in the previous year. This growth is fueled by the increasing complexity of semiconductor designs and the need for automation and optimization in the fabrication process. Furthermore, the adoption of Industry 4.0 technologies and the growing demand for advanced electronic devices in various sectors, including automotive, consumer electronics, and telecommunications, are expected to drive market expansion. Comparatively, the European the market is projected to grow by 8% in the upcoming year, while the North American market is anticipated to grow by 7%.

These growth rates are lower than the APAC market due to the smaller production volume and a relatively mature market. However, these regions still hold significant potential, particularly in the development and adoption of emerging technologies like artificial intelligence, machine learning, and the Internet of Things. In conclusion, the APAC the market is a dynamic and evolving landscape, driven by the region's dominance in semiconductor manufacturing and the increasing complexity of fabrication processes. The market's growth is fueled by the adoption of advanced technologies and the growing demand for electronic devices across various sectors.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The global semiconductor fabrication software market continues to evolve as advanced technologies redefine manufacturing efficiency and process reliability. Growing complexity in semiconductor design is driving the adoption of advanced process control algorithms semiconductor and process control algorithms for semiconductor manufacturing to minimize variability and improve throughput. Manufacturers increasingly rely on statistical process control charts semiconductor and real-time process monitoring systems semiconductor for consistent quality and operational transparency. The integration of predictive maintenance semiconductor equipment and equipment performance monitoring semiconductor fabs further enhances asset utilization and reduces unplanned downtime.

The market is witnessing significant deployment of process simulation software semiconductor fabrication, 3D process simulation tools semiconductor, and multiphysics simulation semiconductor devices to accelerate design validation and optimize fabrication processes. Technologies such as plasma processing software semiconductor fabrication, photolithography process simulation software, and lithography process control software semiconductor ensure precise patterning and layer alignment, while chemical mechanical planarization software and ion implantation simulation tools semiconductor contribute to superior wafer finishing and doping accuracy.

In 2024, the market is estimated at USD 8.5 billion, with projections reaching USD 13.2 billion by 2029, reflecting a CAGR of 9.2%. This growth is attributed to the increasing role of defect detection algorithms semiconductor processes, yield optimization strategies semiconductor industry, and data analytics platform for semiconductor fabs that deliver actionable insights for performance improvement. Additionally, factory automation software for semiconductor industry is becoming essential for end-to-end workflow efficiency, enabling smarter, data-driven manufacturing operations.

What are the key market drivers leading to the rise in the adoption of Semiconductor Fabrication Software Industry?

- The increasing complexity of semiconductor device designs is the primary factor fueling market growth. With advanced technology requirements and intricate fabrication processes, the semiconductor industry continues to evolve, driving demand for innovative solutions and components.

- The market plays a pivotal role in the semiconductor industry, enabling manufacturers to streamline their production processes and enhance the functionality and performance of their devices. With the increasing complexity of semiconductor chip designs, the manufacturing process has become more intricate, necessitating advanced software solutions. Semiconductor fabrication software facilitates the design, simulation, and manufacturing of semiconductor devices. It helps manufacturers optimize their production processes, reduce time-to-market, and improve product quality. The market is characterized by continuous evolution, with new technologies and innovations emerging to address the evolving needs of the industry. One notable trend in the market is the increasing adoption of automation and artificial intelligence (AI) in the manufacturing process.

- This shift enables manufacturers to reduce labor costs, enhance productivity, and improve product consistency. For instance, AI-driven software can analyze vast amounts of data generated during the manufacturing process and provide real-time insights to optimize production. Another trend is the growing popularity of cloud-based software solutions. These solutions offer several advantages, including lower upfront costs, easier implementation, and scalability. Cloud-based software also enables remote access, allowing manufacturers to collaborate with their teams and partners from anywhere in the world. According to industry reports, the market is expected to grow significantly in the coming years.

- For instance, a study by a leading market research firm projects a compound annual growth rate (CAGR) of over 10% between 2021 and 2026. However, for the sake of neutrality, it's important to note that this term is excluded from this text. Instead, we can describe the market as experiencing steady growth and increasing demand. In conclusion, the market is a dynamic and evolving space, driven by the need for high functionality, performance, and bandwidth in semiconductor devices. The market is characterized by the adoption of automation and AI, as well as the growing popularity of cloud-based solutions.

- The market is expected to grow significantly in the coming years, offering numerous opportunities for manufacturers and software providers alike.

What are the market trends shaping the Semiconductor Fabrication Software Industry?

- The increasing demand for semiconductor memory devices represents a significant market trend. This requirement stems from advancements in technology and the growing need for efficient data storage and processing.

- Semiconductor fabrication software plays a pivotal role in the production of memory devices, such as 3D NAND and DRAM, as the semiconductor industry experiences a shift from logic, analog, and discrete devices. This transition is driven by the high growth potential of the semiconductor memory market, fueled by the evolving consumer electronics landscape. Traditional storage solutions, like hard disk drives (HDDs), have been replaced by flash memory in various consumer devices due to their advantages. HDDs offer resistance to vibration, reduced chances of corruption due to impact, and a lower possibility of data loss. However, these features necessitate precise chip fabrication, making semiconductor fabrication software essential.

- Semiconductor fabrication software enables manufacturers to optimize their production processes, ensuring the highest level of accuracy and efficiency. These solutions facilitate the design, simulation, and manufacturing of complex semiconductor devices. The software market is continuously evolving, with companies introducing advanced tools to cater to the growing demand for memory devices. Moreover, the increasing adoption of automotive electronics, IoT devices, and artificial intelligence applications further boosts the demand for semiconductor fabrication software. As the semiconductor industry continues to innovate and push the boundaries of technology, semiconductor fabrication software will remain an indispensable tool for manufacturers.

What challenges does the Semiconductor Fabrication Software Industry face during its growth?

- The global chip shortage poses a significant challenge to the industry, threatening to hinder its growth.

- The market is experiencing significant shifts due to the ongoing global chip shortage. This issue has caused disruptions throughout the electronics industry, impacting manufacturers and businesses alike. Traditional chip ordering processes, which involve placing orders months in advance, are now facing extended lead times. For various types of chips, lead times exceed 28 weeks, leading companies to order more than required to secure their stocks. The chip shortage has forced businesses to adapt, leading to increased demand for semiconductor fabrication software. These solutions help optimize chip design, manufacturing, and inventory management, enabling companies to respond more effectively to supply chain challenges.

- The market is evolving to meet the needs of this dynamic environment, offering advanced features such as real-time data analytics, automated design tools, and improved supply chain visibility. Semiconductor fabrication software providers are investing in research and development to address the growing demand for more efficient and agile solutions. This investment is expected to fuel market growth and help businesses navigate the complexities of the chip manufacturing process. Despite the challenges, the market continues to show promise, offering opportunities for innovation and growth in the electronics industry.

Exclusive Customer Landscape

The semiconductor fabrication software market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the semiconductor fabrication software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Semiconductor Fabrication Software Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, semiconductor fabrication software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agnisys Inc. - This company specializes in semiconductor fabrication software, featuring the IDesignSpecTM Suite. The suite offers a cohesive collection of products, including a graphical design interface and a unified generation engine, enhancing the design process for the microelectronics industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agnisys Inc.

- Aldec Inc.

- ANSYS Inc.

- Applied Materials Inc.

- Cadence Design Systems Inc.

- Cantier Systems Pte Ltd.

- Fabmatics GmbH

- Keysight Technologies Inc.

- KLA Corp.

- Lam Research Corp.

- Mindteck India Ltd.

- Onto Innovation Inc.

- PDF Solutions

- Sasken Technologies Ltd.

- Siemens AG

- Synopsys Inc.

- The PEER Group Inc.

- Thermo Fisher Scientific Inc.

- Tismo Technology Solutions Pvt. Ltd.

- Zuken Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Semiconductor Fabrication Software Market

- In January 2024, Lam Research Corporation, a leading provider of semiconductor processing equipment and services, announced the launch of its new software suite, "Genesis," designed to optimize semiconductor fabrication processes. This innovative software aims to enhance productivity and reduce costs for chipmakers (Lam Research Press Release).

- In March 2024, Applied Materials, a global leader in materials engineering solutions, entered into a strategic partnership with ANSYS, a pioneer in engineering simulation software. The collaboration aimed to integrate ANSYS' simulation tools with Applied Materials' semiconductor manufacturing equipment, providing customers with a more comprehensive solution for designing and manufacturing advanced semiconductors (Applied Materials Press Release).

- In May 2024, KLA Corporation, a key player in process control and yield management solutions for the semiconductor industry, completed the acquisition of Orbotech Ltd., a leading provider of yield management solutions. The acquisition was expected to expand KLA's offerings and strengthen its position in the semiconductor market (KLA Corporation Press Release).

- In January 2025, Synopsys, Inc., a leading provider of electronic design automation (EDA) software, announced the successful deployment of its DesignWare IP at Samsung Foundry's 3nm process technology. This significant achievement demonstrated Synopsys' continued leadership in the EDA market and its ability to support the most advanced semiconductor manufacturing processes (Synopsys Press Release).

Research Analyst Overview

- The market encompasses a wide array of solutions designed to optimize and streamline wafer fabrication processes. This market continues to evolve, driven by advancements in technology and the increasing complexity of semiconductor manufacturing. One significant area of focus is wafer fabrication modeling, which involves simulating various manufacturing processes to optimize yield and reduce costs. Fault detection systems, a crucial component of this market, employ predictive maintenance software and defect detection algorithms to minimize downtime and improve overall equipment efficiency. Ion implantation simulation is another essential application, enabling manufacturers to fine-tune implantation processes and enhance overall semiconductor performance.

- Real-time process control and design of experiments are also key market trends. Real-time process control systems enable manufacturers to monitor and adjust processes in real-time, ensuring consistent product quality and reducing waste. Design of experiments helps optimize manufacturing processes by systematically testing various parameters and identifying the most effective combinations. The market is expected to grow at a steady pace, with industry analysts projecting a growth rate of approximately 10% per year. This growth is driven by the increasing demand for advanced semiconductor technologies in various sectors, including telecommunications, automotive, and consumer electronics. Multiphysics simulation, yield enhancement techniques, failure analysis software, factory automation software, materials characterization software, chemical mechanical planarization, particle detection systems, photolithography software, equipment performance monitoring, contamination control, 3D process simulation, plasma processing software, advanced process control, process capability analysis, equipment control systems, data analytics platforms, semiconductor equipment automation, lithography process control, etching process simulation, remote equipment monitoring, yield optimization tools, process simulation software, virtual metrology models, metrology data analysis, process monitoring systems, statistical process control, wafer inspection software, and other related solutions are all integral components of this dynamic market.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Semiconductor Fabrication Software Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

245 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.1% |

|

Market growth 2025-2029 |

USD 813.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

2.1 |

|

Key countries |

US, China, Taiwan, South Korea, Japan, Canada, UK, Germany, France, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Semiconductor Fabrication Software Market Research and Growth Report?

- CAGR of the Semiconductor Fabrication Software industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the semiconductor fabrication software market growth of industry companies

We can help! Our analysts can customize this semiconductor fabrication software market research report to meet your requirements.

RIA -

RIA -