3D Display Market Size 2024-2028

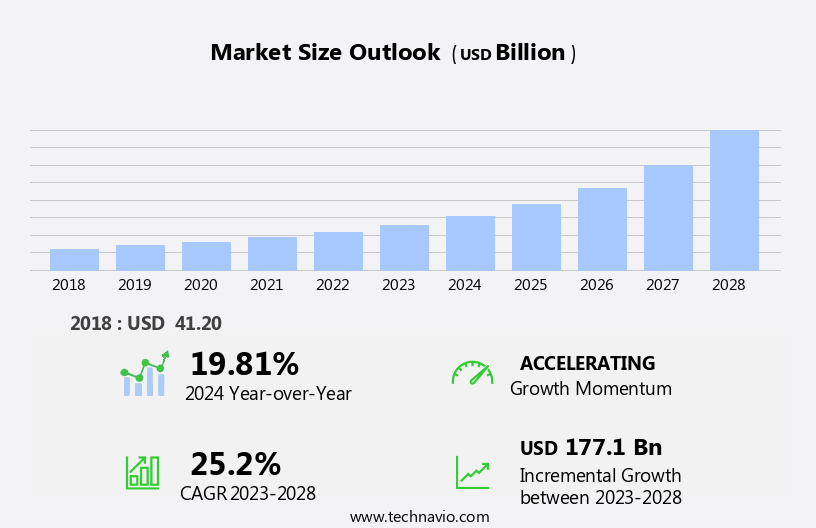

The 3d display market size is forecast to increase by USD 177.1 billion, at a CAGR of 25.2% between 2023 and 2028.

- The market is experiencing significant growth in various industries, with automotive applications and healthcare being key adopters. The integration of 3D displays in automobiles enhances the driving experience by providing a more immersive and realistic view of the road and environment. In the healthcare sector, 3D displays are increasingly utilized in medical imaging and surgical planning, offering improved accuracy and visualization for medical professionals. However, the high cost associated with 3D display technology poses a significant challenge for market expansion.

- This obstacle necessitates ongoing research and development efforts to reduce production costs and make 3D displays more accessible and affordable for a broader range of applications and industries. Companies seeking to capitalize on the opportunities presented by the market must focus on innovation and cost reduction strategies to stay competitive and meet the evolving demands of consumers and industries.

What will be the Size of the 3D Display Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, with dynamic advancements in technology shaping its applications across various sectors. 3D tracking technology enhances user experience in entertainment and training, while 3D sensor technology drives the development of head-mounted displays and holographic displays. 3D architectural design offers new perspectives, and 3D market growth is fueled by the integration of 3D mapping and multi-view display. 3D frame rate and display standards optimize viewing, while 3D scanning and 3D depth perception enable precise object recognition and data analysis. Light field display and stereoscopic projection offer immersive experiences, and 3D resolution, convergence, and refresh rate enhance visual quality.

Augmented reality headsets and autostereoscopic displays revolutionize user interaction, and 3D design and modeling facilitate innovative applications. Parallax barrier technology and polarization filters improve 3D visualization, and 3D simulation and animation offer realistic experiences. 3D fatigue and crosstalk are ongoing challenges, while 3D color gamut and contrast enhance content creation. 3D industry trends include voxel display, field of view expansion, and 3D content availability. Depth cues and user interface design optimize the immersive experience, and 3D software development and signage expand consumer adoption. The 3D technology roadmap unfolds with ongoing research and development, shaping the future of 3D applications and market trends.

How is this 3D Display Industry segmented?

The 3d display industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Screen based display

- Micro display

- Application

- Televisions

- Smartphones

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- South Korea

- Rest of World (ROW)

- North America

.

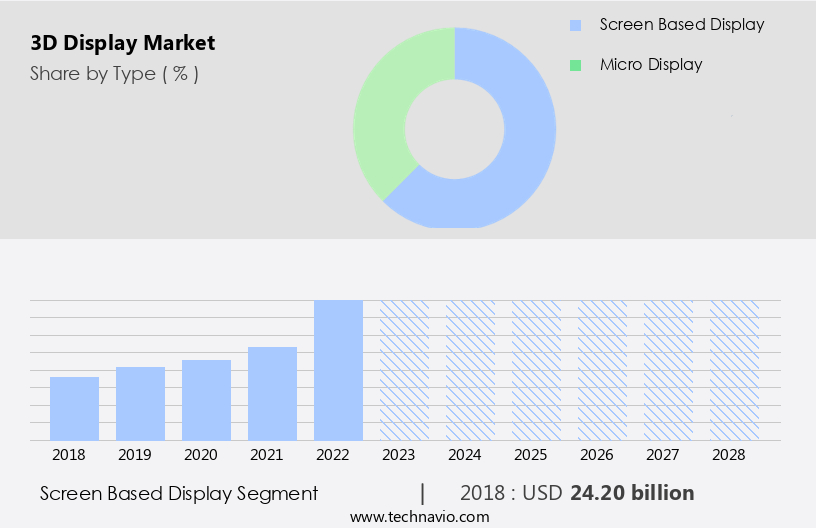

By Type Insights

The screen based display segment is estimated to witness significant growth during the forecast period.

The market encompasses various technologies, including 3D tracking, sensor technology, and holographic displays, among others. The screen-based display segment leads the market, driven by its widespread adoption in industries such as entertainment, gaming, and education. This segment's growth can be attributed to its ability to deliver an immersive viewing experience, enhancing user engagement and satisfaction. 3D sensors and tracking systems enable depth perception, while head-mounted displays offer a more personalized, interactive experience. 3D architectural design and mapping applications provide innovative solutions for various industries. 3D video capture and processing, along with animation and simulation, are essential components of the 3D content creation process.

3D training and education are becoming increasingly popular, offering a more engaging and effective learning experience. The market is expected to grow, fueled by advancements in 3D technology, such as higher resolution, faster refresh rates, and wider fields of view. 3D rendering, depth cues, and parallax barrier technology contribute to the creation of realistic and immersive 3D visualizations. 3D design, modeling, and navigation are essential for various industries, including healthcare, automotive, and manufacturing. 3D user interfaces and experiences are becoming more common, enhancing the overall user experience. 3D signage and virtual reality headsets offer new opportunities for advertising and entertainment.

The market's future trends include advancements in 3D printing, augmented reality, and immersive experiences. 3D content availability, depth perception, and color gamut are critical factors influencing consumer adoption. 3D technology roadmaps and industry trends indicate continued growth and innovation in this field.

The Screen based display segment was valued at USD 24.20 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

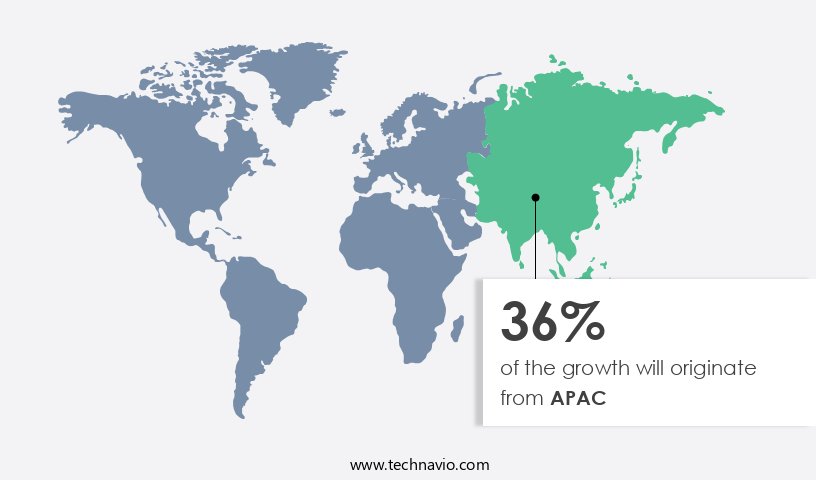

APAC is estimated to contribute 36% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the dynamic world of technology, the market is witnessing significant advancements, driven by various entities. In the realm of entertainment and interaction, 3D technology offers immersive experiences through movies, video games, and virtual reality. The integration of 3D sensors and tracking systems enhances user experience, enabling interactive applications and real-time 3D mapping. The hardware development sector is pushing the boundaries of 3D display technology through innovations like head-mounted displays, holographic displays, and autostereoscopic displays. These advancements cater to diverse industries, such as architectural design, medical imaging, and education, offering benefits like improved depth perception and enhanced visualization. Moreover, the market growth is fueled by the increasing adoption of 3D technology in various sectors.

For instance, 3D modeling and animation are transforming industries like film, advertising, and product design. Simultaneously, 3D printing and data analysis are revolutionizing manufacturing and research processes. The future trends include advancements in 3D frame rate, resolution, and convergence, ensuring smoother and more realistic viewing experiences. Furthermore, advancements in 3D video processing and content availability are expected to boost consumer adoption. In the realm of 3D display standards, multi-view displays, light field displays, and parallax barrier technology are shaping the future of 3D visualization. Additionally, advancements in 3D glasses technology, such as polarization filters and anaglyph glasses, are improving user comfort and experience.

As the market evolves, it is essential to address challenges like crosstalk, brightness, and fatigue. The industry is also focusing on developing technologies that offer wider fields of view and higher color gamuts. In conclusion, the market is witnessing rapid growth, driven by advancements in technology, expanding applications, and increasing consumer demand. The future holds immense potential for this dynamic and innovative sector.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of 3D Display Industry?

- The emergence of 3D displays represents a significant driver for the automotive market, as this technology enhances the driving experience by providing a more immersive and realistic interface for navigation, entertainment, and safety systems.

- The market is experiencing significant growth due to its increasing adoption in various industries, particularly in the automotive sector. These advanced displays offer a more immersive and harmonious user experience, enhancing the way information is presented. Parallax barrier technology and 3D simulation are key enablers, providing depth perception and a more natural way of interacting with content. In the automotive industry, 3D displays are utilized for applications like navigation, entertainment, and driver assistance systems, offering a more intuitive and realistic interface. For instance, a 3D navigation system can display a 3D map, providing a more detailed and engaging view of the surrounding area.

- Furthermore, 3D modeling, 3D image processing, and 3D user interface are essential components that contribute to the market's growth. Additionally, advancements in 3D content availability, 3D software development, and 3D signage are expanding the market's potential applications. Virtual reality headsets are another emerging technology that relies on 3D displays to deliver an immersive experience. The market's future looks promising, driven by the increasing demand for advanced and interactive displays.

What are the market trends shaping the 3D Display Industry?

- The 3D display technology is gaining significant traction in the medical industry, representing an emerging market trend. This advanced technology is increasingly being adopted for various applications, including medical imaging and surgical planning.

- 3D display technology has gained significant traction in various industries, particularly in medical applications, entertainment, and architectural design. The integration of 3D tracking and interaction technologies has revolutionized the way data is visualized and experienced. In the medical field, 3D displays are utilized for diagnostic imaging, surgical planning, and training, providing a more immersive and harmonious user experience. For instance, CSpace, a 3D display developed by Coretec, offers high-resolution, full-color images in a glass chamber. This technology enables users to view 360-degree perspectives of the images without the need for additional visualization aids. In the realm of 3D entertainment, head-mounted displays and holographic displays have emerged as popular choices for delivering immersive experiences.

- Additionally, 3D sensor technology and multi-view display systems are driving the growth of the 3D market. As the technology continues to evolve, advancements in 3D frame rate, brightness, and display standards are expected to further enhance the user experience. Augmented reality headsets are also gaining popularity, offering a blend of real and virtual environments. Overall, the 3D technology roadmap presents exciting opportunities for innovation and growth in various industries.

What challenges does the 3D Display Industry face during its growth?

- The high cost of implementing 3D display technology is a significant challenge impeding the growth of the industry.

- The market faces a significant barrier to growth due to the high cost of devices and associated equipment. While 3D game consoles retail between USD200 and USD400, 3D projectors range from USD1,000 to USD10,000. This price point makes 3D displays an unattainable luxury for individuals in lower-income demographics. The expense doesn't stop at the display; new 3D games and the maintenance and repair costs add to the financial burden. These expenses stem from the intricate technology used in 3D displays, which is more complex than standard displays. Moreover, factors like 3D crosstalk, 3D convergence, and 3D depth perception require specific attention to ensure optimal viewing experience.

- These factors contribute to the need for 3D glasses, adding to the overall cost. The 3D viewing distance, 3D resolution, 3D refresh rate, stereoscopic projection, depth of field, 3D rendering, 3D visualization, and 3D video processing further add to the complexity and cost of 3D displays. As 3D technology continues to evolve, future trends include advancements in light field displays and 3D printing. However, the high cost of these technologies may limit their widespread adoption. Additionally, concerns regarding 3D fatigue and the potential health effects of prolonged exposure to 3D displays remain ongoing areas of research. Despite these challenges, the market for 3D displays is expected to grow as the technology becomes more accessible and affordable.

Exclusive Customer Landscape

The 3d display market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the 3d display market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, 3d display market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alphabet Inc. - The company specializes in advanced 3D display technologies, showcasing innovative solutions such as 3D Swirl.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alphabet Inc.

- AUO Corp.

- Avalon Holographics Inc.

- Continental AG

- Dimenco BV

- FoVI3D

- FUJIFILM Holdings Corp.

- LG Electronics Inc.

- Mitsubishi Electric Corp.

- New 3D Technologies Inc.

- NVIDIA Corp.

- Ostendo Technologies Inc.

- Panasonic Holdings Corp.

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- SeeReal Technologies SA

- Sharp Corp.

- Sony Group Corp.

- Toshiba Corp.

- VividQ Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in 3D Display Market

- In February 2024, Samsung Display unveiled its new 110-inch Micro LED 3D TV, showcasing a significant leap in large-format 3D display technology (Samsung Press Release, 2024). This innovative product, featuring over 11 million micro-LEDs, offers enhanced picture quality and depth perception.

- In July 2024, LG Display and Sony announced a strategic partnership to jointly develop next-generation 3D displays using organic light-emitting diode (OLED) technology (LG Display Newsroom, 2024). This collaboration aims to accelerate the commercialization of high-performance, cost-effective 3D displays for various applications, including gaming, cinema, and education.

- In October 2024, Osram, a leading lighting solutions provider, secured a â¬50 million investment from the European Union to develop advanced 3D sensing technologies for various industries, including automotive and consumer electronics (European Commission Press Release, 2024). This funding will contribute to the development of next-generation 3D displays and sensors, enhancing user experiences and expanding market opportunities.

- In March 2025, Panasonic and Foxconn announced a joint venture to establish a new company, "3DBox," focusing on the production and sales of 3D displays for various markets, including education, healthcare, and entertainment (Panasonic Press Release, 2025). This strategic move will combine Panasonic's expertise in display technology with Foxconn's manufacturing capabilities, aiming to capture a significant market share and drive innovation in the 3D display industry.

Research Analyst Overview

- The market encompasses a diverse range of applications, from architectural visualization and gaming consoles to healthcare, education, and retail industries. Plasma and LCD technologies, including QLED and OLED, dominate the market, while microLED and 3D privacy technologies are gaining traction. In the entertainment industry, 3D broadcasting and 3D video streaming are transforming the viewing experience, and 3D gaming engines offer immersive experiences for gamers. Industrial design and 3D software libraries facilitate product prototyping and design iterations, while 3D accessibility enhances user experience for individuals with visual impairments. In the healthcare sector, 3D models aid in medical training and patient education.

- Retail display and digital signage incorporate 3D technology to capture consumers' attention, and 3D ethics and security considerations are essential for ethical and secure 3D content streaming. Mobile devices and desktop computers support 3D applications, including 3D mobile apps and 3D Blu-ray. 3D development kits and LED backlighting enable the creation of custom 3D content, and 3D interaction design ensures intuitive user experiences. Museum exhibits and education and training programs leverage 3D technology to enhance learning and engagement.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled 3D Display Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

170 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 25.2% |

|

Market growth 2024-2028 |

USD 177.1 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

19.81 |

|

Key countries |

US, China, South Korea, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this 3D Display Market Research and Growth Report?

- CAGR of the 3D Display industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the 3d display market growth of industry companies

We can help! Our analysts can customize this 3d display market research report to meet your requirements.

RIA -

RIA -