3D Imaging Market Size 2024-2028

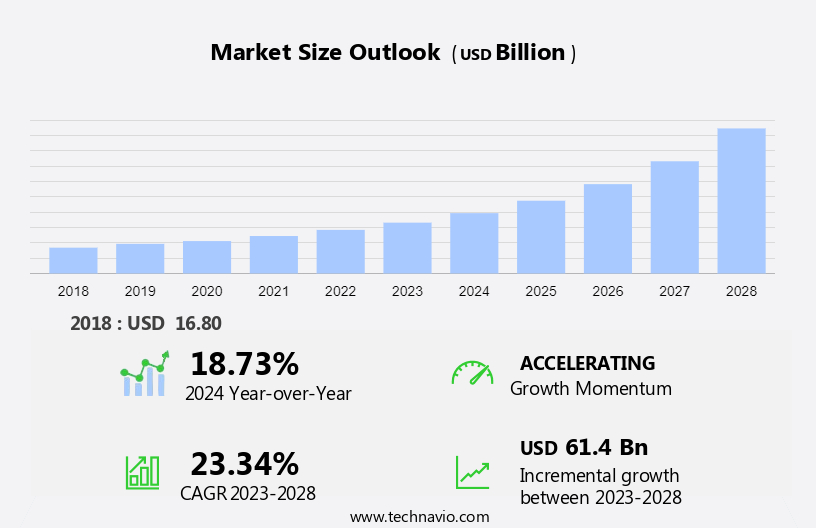

The 3D imaging market size is forecast to increase by USD 61.4 billion, at a CAGR of 23.34% between 2023 and 2028. The market is experiencing significant growth due to several key drivers. First, the media industry is increasingly utilizing 3D technology for content creation and consumption, offering more teleportation and telepresence experiences for audiences.

In the gaming sector, there is a demand for lifelike animations and interactive experiences, driving the adoption of 3D imaging. Additionally, advancements in sensor technologies, algorithms, and robotics are enabling the development of autonomous vehicles and augmented reality applications, expanding the market's scope. Furthermore, in healthcare, 3D imaging is revolutionizing solutions for orthopedic implants, dental prosthetics, and organ replicas, enhancing spatial understanding and improving patient outcomes. However, high initial costs of 3D imaging equipment remain a challenge for market growth.

What will the Size of the 3D Imaging Market be during the Forecast Period?

3D imaging technology has emerged as a game-changer in various sectors, revolutionizing the way information is visualized and processed. This technology, which captures and displays three-dimensional images, has found significant applications in healthcare, entertainment, architecture, engineering, manufacturing, environmental science, media, and more. In the healthcare industry, 3D imaging technology plays a crucial role in anatomical visualizations, diagnostics, and surgical planning. High-resolution 3D images enable medical professionals to gain a clearer understanding of complex conditions, leading to improved patient care and outcomes. Hospitals and medical services have increasingly adopted this technology to enhance their diagnostic capabilities and provide better patient experiences. Further, the entertainment industry has embraced 3D imaging technology to create experiences for audiences. From motion pictures to TV shows, 3D technology brings an added dimension to visual storytelling, enhancing the viewer's engagement and enjoyment. In the realm of amusement, 3D technology is used to create thrilling experiences at theme parks and other attractions. Architecture and construction have also benefited from 3D imaging technology. Design and designing processes have been streamlined with the use of 3D models, enabling architects and engineers to visualize structures in their entirety before construction begins. This leads to more accurate planning, reduced costs, and improved project outcomes.

Additionally, manufacturing industries have adopted 3D imaging technology for various applications, including quality control, prototyping, and assembly line optimization. High-resolution 3D images allow manufacturers to closely examine products, ensuring that they meet the required standards. In addition, 3D imaging technology is used to create digital prototypes, reducing the need for physical models and saving time and resources. Environmental science applications of 3D imaging technology include the creation of three-dimensional models of ecosystems and landscapes. These models help researchers and policymakers better understand complex environmental systems and make informed decisions about conservation and restoration efforts. The media industry utilizes 3D imaging technology to create engaging and interactive content. News organizations, for instance, use 3D technology to create reports, while educational institutions employ it to create interactive learning materials. Three-dimensional image sensors, cameras, and screens are essential components of 3D imaging technology. These devices capture and display 3D images, making it possible to experience depth and perspective in various applications. In the automotive industry, 3D imaging technology is used for security and observation purposes, enhancing safety and reducing the risk of accidents.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Large enterprise

- SMEs

- Application

- Healthcare

- Industrial

- Media and entertainment

- Defense

- Others

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- APAC

- China

- South America

- Middle East and Africa

- North America

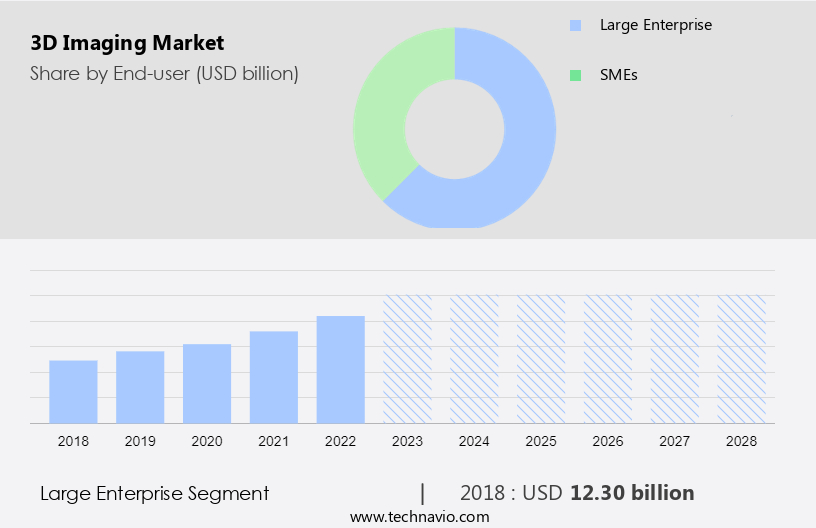

By End-user Insights

The large enterprise segment is estimated to witness significant growth during the forecast period. Three-dimensional (3D) imaging has become an indispensable technology in large-scale enterprises, revolutionizing industries such as manufacturing, healthcare, aerospace, and automotive. By generating precise 3D replicas of objects, this technology enables detailed analysis and visualization of intricate solutions with unparalleled accuracy. This is particularly beneficial in complex problem-solving scenarios. Data processing and storage are integral components of 3D imaging, requiring substantial computational resources. Real-time processing is essential to ensure optimal efficiency, making motion cameras and 3D image sensors crucial. Stereoscopic imaging and gesture recognition are advanced features that further enhance the capabilities of 3D imaging. In the manufacturing sector, 3D imaging is used for rapid prototyping, enabling companies to create accurate models for product development.

In healthcare, it is used for object measurement, position tracking, and facial recognition systems, contributing to improved patient care and identity verification. Inspecting critical components in industries like aerospace and automotive is made easier with 3D imaging, ensuring quality and safety. Optical illusion and 3D displays are popular applications of this technology in the entertainment industry and consumer electronics. Hospitals and hospitals are increasingly adopting 3D imaging for medical diagnosis and treatment planning. With the growing importance of 3D imaging, the demand for 3D image sensors, cameras, and screens is expected to rise.

Get a glance at the market share of various segments Request Free Sample

The large enterprise segment was valued at USD 12.30 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

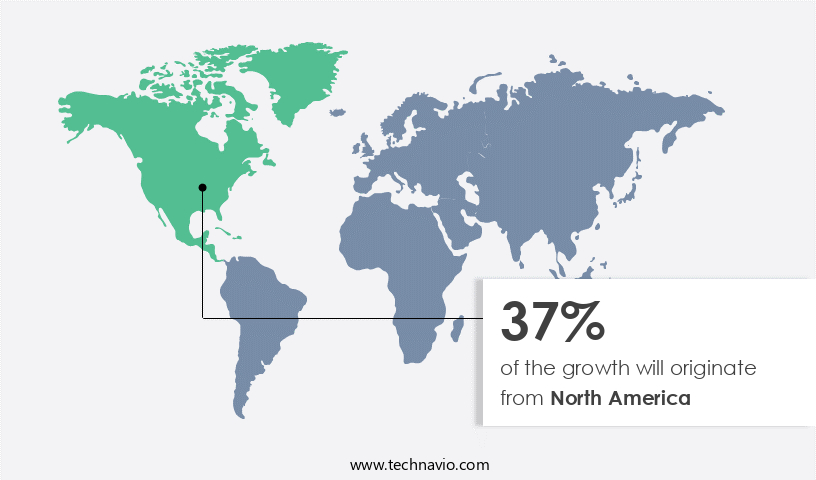

North America is estimated to contribute 37% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

Key contributors to this expansion include the US, Mexico, and Canada. The demand for 3D imaging systems is increasing in industries such as aerospace and defense, consumer electronics, and healthcare. This growth can be attributed to the integration of 3D effects in gaming consoles, motion recognition technology, and the adoption of 3D displays in smartphones and tablets. Moreover, modern robotics and 4D technologies are revolutionizing industries like media and amusement, architecture and engineering, industrial automation, and agricultural processes. Government and industry investments in mechanical computerization and high definition representation are further fueling the market's growth. Strategic partnerships among industry players are also on the rise to capitalize on the burgeoning opportunities in the region. Key players include companies specializing in 3D clinical imaging, 4D technology for smart fitness gadgets, and 3D delivering and showing solutions for various industries.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Increasing product launches is the key driver of the market. The market is experiencing significant growth across various industries in the United States, including healthcare, entertainment, architecture, engineering, manufacturing, environmental science, media, and more. This expansion is driven by the integration of advanced technologies and features into 3D imaging solutions. For instance, in the healthcare sector, anatomical visualizations, diagnostics, surgical planning, and prosthetic development are increasingly utilizing 3D imaging for enhanced patient care.

In the entertainment industry, gaming and movies are employing 3D imaging for virtual reality experiences. In architecture and engineering, detailed models and designs are being created for clients to better understand and visualize projects. Similarly, archaeologists are using 3D imaging to study historical artifacts. The competition in the market is intensifying due to these new developments, leading to continuous innovation and differentiation.

Market Trends

An increase in strategic collaborations and M&A is the upcoming trend in the market. The market is witnessing an uptick in strategic partnerships and mergers and acquisitions (M&A). Companies are collaborating with other businesses and research institutions to innovate 3D imaging technologies, broaden their product portfolios, and extend their reach. For example, in January 2022, Alma Medical Pvt Ltd entered into an agreement with Contextflow GmbH to integrate Contextflow's advanced algorithm for recognizing and analyzing lung-specific image data in CT scans into a new digital health platform. This collaboration will enable hundreds of radiologists to incorporate this artificial intelligence (AI) tool into their clinical workflow, thereby enhancing their efficiency.

Moreover, this trend reflects the growing importance of AI and advanced algorithms in 3D imaging applications, including teleportation and telepresence experiences in the media industry, content creation and consumption, special effects in gaming, lifelike animations, interactive experiences, depth perception, sensor technologies, and algorithms in robotics, autonomous vehicles, augmented reality, spatial understanding, healthcare solutions, orthopedic implants, dental prosthetics, and organ replicas.

Market Challenge

High initial costs of 3D imaging equipment is a key challenge affecting the market growth. Three-dimensional (3D) imaging has emerged as a crucial technology in numerous industries, playing a significant role in enhancing quality control processes. This process involves converting or altering two-dimensional (2D) data into a 3D format, creating a perception of depth. To generate precise 3D renderings for inspection and testing applications, various technologies are integrated with 3D imaging techniques. Advanced equipment employs a range of sensors, including optical, acoustic, laser scanning, radar, thermal, and seismic sensors, as well as light-detecting modules and semiconductors. Environmental scientists utilize 3D imaging for terrain and ecosystem reconstruction, contributing to conservation efforts. Artificial intelligence (AI) and image processing technologies are employed to analyze vast amounts of data, enhancing the accuracy and efficiency of these applications.

Further, augmented reality (AR) and virtual reality (VR) technologies enable visualization of complex data sets, providing new insights for research and development. In the medical field, 3D imaging is integral to diagnostics, surgeries, and personalized medicine. Holographic displays offer enhanced resolution and scanning capabilities, enabling detailed analysis of biometric data and authentication systems. Neuroscience applications benefit from 3D imaging in studying the intricacies of the human brain. Space exploration also relies on 3D imaging for celestial body analysis and monitoring ecological systems.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Agilent Technologies Inc. - The company provides advanced 3D imaging solutions through its BioTek Gen5 software, enabling users in the market to visualize and analyze data in a more comprehensive and accurate manner.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Canfield Scientific Inc.

- Canon Inc.

- GE Healthcare Technologies Inc.

- Guangzhou Frontop Computer Graphics Technology Co. Ltd.

- Hologic Inc.

- HP Inc.

- Infineon Technologies AG

- Koninklijke Philips N.V.

- Medtronic Plc

- Microsoft Corp.

- Olympus Corp.

- Panasonic Holdings Corp.

- Samsung Electronics Co. Ltd.

- Siemens Healthineers AG

- Sony Group Corp.

- STEMMER IMAGING AG

- STMicroelectronics International N.V.

- Trimble Inc.

- Vatech Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Three-dimensional imaging technology has gained significant traction across various industries, including healthcare, entertainment, architecture, engineering, manufacturing, environmental science, media, and more. In healthcare, anatomical visualizations are revolutionizing diagnostics, enabling surgical planning, prosthetic development, and personalized medicine. Architects and engineers utilize detailed models and designs to better understand and present their clients' projects. The entertainment industry, from gaming to movies, leverages 3D imaging for virtual reality, special effects, and lifelike animations. Environmental scientists employ 3D imaging for ecological monitoring, reconstructing terrains and ecosystems, and contributing to conservation efforts. Artificial intelligence and image processing play a crucial role in enhancing the capabilities of 3D imaging, from reconstruction to authentication systems. In addition, AR and VR technologies offer experiences in healthcare, entertainment, and education.

Further, resolution and scanning capabilities are essential factors for 3D imaging devices, with applications ranging from medical diagnostics and surgeries to consumer electronics and automotive industries. The on-premise and cloud segments cater to different needs, with large enterprises driving the market growth. The aging population and lifestyle diseases necessitate advanced healthcare solutions, while the media industry focuses on content creation, consumption, and experience. Three-dimensional imaging technology offers high-definition representation in various sectors, from hospitals to educational institutions, public places, manufacturing plants, and security and surveillance systems. The technology's applications extend to automotive, with cars and driverless vehicles incorporating 3D imaging for parking surveillance and anti-theft measures. Social media, forensics, mobile commerce, and medical services also benefit from 3D imaging solutions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

196 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 23.34% |

|

Market Growth 2024-2028 |

USD 61.4 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

18.73 |

|

Regional analysis |

North America, Europe, APAC, South America, and Middle East and Africa |

|

Performing market contribution |

North America at 37% |

|

Key countries |

US, China, Germany, Canada, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Agilent Technologies Inc., Canfield Scientific Inc., Canon Inc., GE Healthcare Technologies Inc., Guangzhou Frontop Computer Graphics Technology Co. Ltd., Hologic Inc., HP Inc., Infineon Technologies AG, Koninklijke Philips N.V., Medtronic Plc, Microsoft Corp., Olympus Corp., Panasonic Holdings Corp., Samsung Electronics Co. Ltd., Siemens Healthineers AG, Sony Group Corp., STEMMER IMAGING AG, STMicroelectronics International N.V., Trimble Inc., and Vatech Co. Ltd. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -