3D Printing Materials Market Size 2026-2030

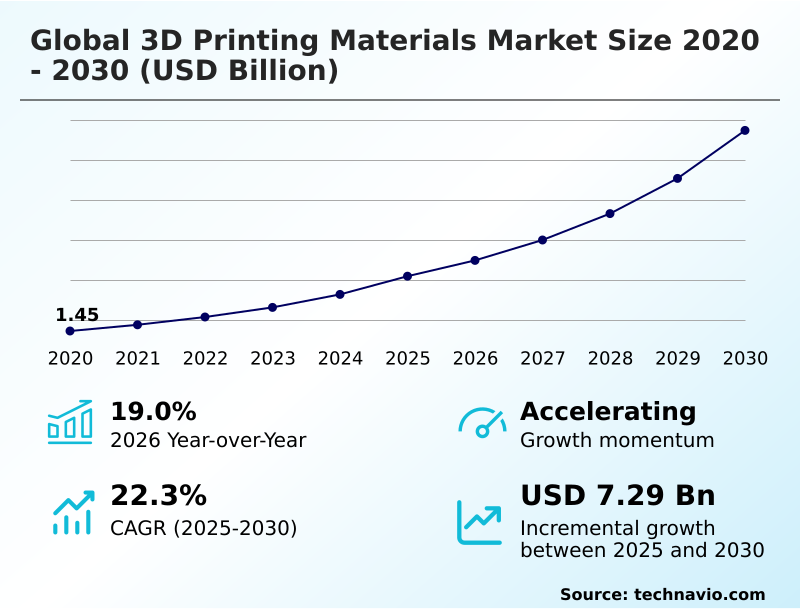

The 3d printing materials market size is valued to increase by USD 7.29 billion, at a CAGR of 22.3% from 2025 to 2030. Industrial expansion and transition to end-use functional part manufacturing will drive the 3d printing materials market.

Major Market Trends & Insights

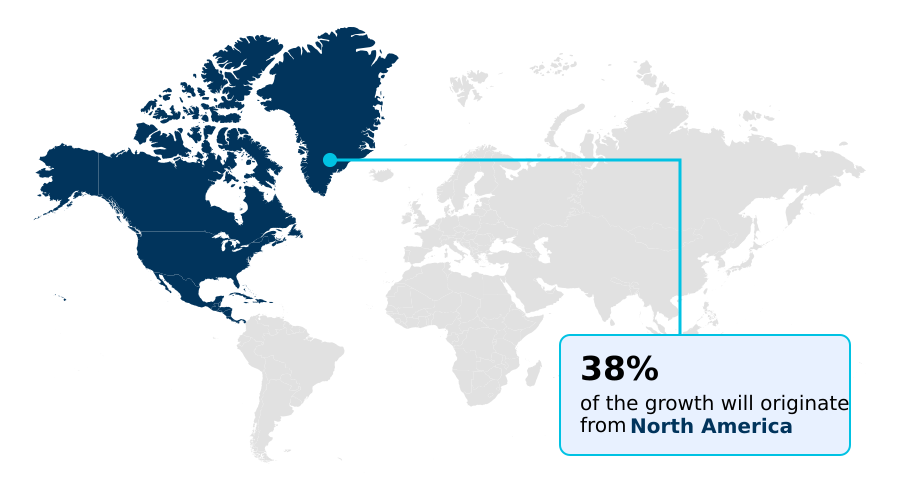

- North America dominated the market and accounted for a 38.4% growth during the forecast period.

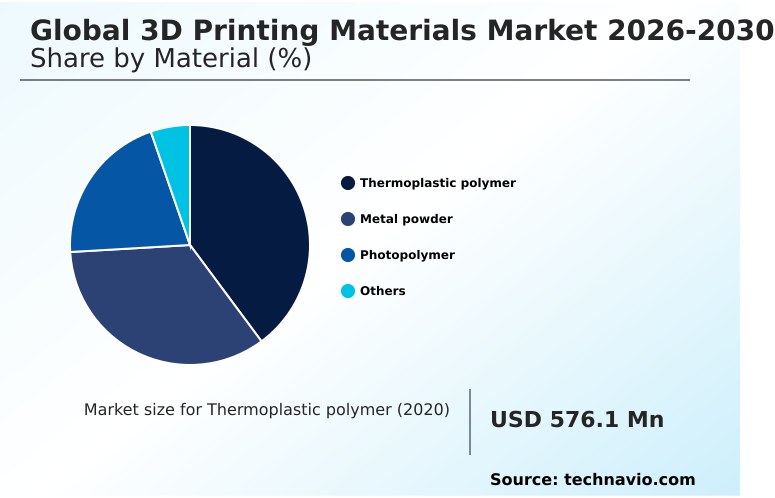

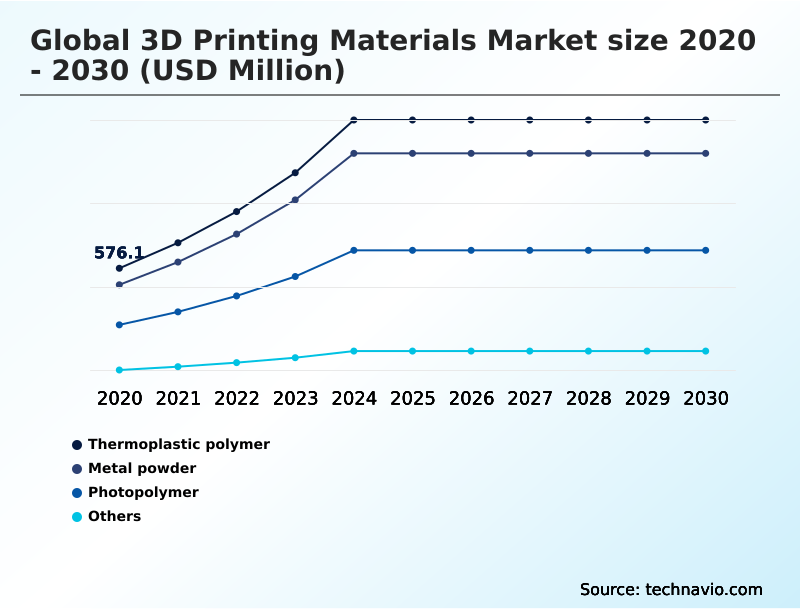

- By Material - Thermoplastic polymer segment was valued at USD 1.30 billion in 2024

- By End-user - Aerospace and defense segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 10.03 billion

- Market Future Opportunities: USD 7.29 billion

- CAGR from 2025 to 2030 : 22.3%

Market Summary

- The 3D Printing Materials Market is undergoing a rapid transition from a prototyping-centric framework to a foundational element of full-scale industrial manufacturing. Organizations are increasingly adopting localized digital inventory models, allowing aerospace and defense operators to fabricate complex replacement components on-demand directly at remote maintenance facilities.

- This strategic shift eliminates the need for massive central warehousing, resulting in a 40% reduction in long-term inventory holding costs compared to traditional physical storage methods. The primary driver accelerating this transformation is the relentless demand for lightweight, end-use functional parts; manufacturers now utilize advanced polymers and superalloys to consolidate multiple structural components into single, highly efficient assemblies.

- However, the steep cost of specialized raw feedstocks, particularly atomized metals and high-purity resins, presents a formidable challenge. Traditional injection molding inputs benefit from massive economies of scale that additive substrates currently lack, fundamentally restricting high-volume commercial expansion. Despite these financial constraints, ongoing metallurgical and chemical innovations continue to expand the operational viability of these advanced manufacturing inputs.

What will be the Size of the 3D Printing Materials Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the 3D Printing Materials Market Segmented?

The 3d printing materials industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Material

- Thermoplastic polymer

- Metal powder

- Photopolymer

- Others

- End-user

- Aerospace and defense

- Healthcare

- Automotive

- Consumer goods

- Others

- Technology

- Fused deposition modeling (FDM)

- Selective laser sintering (SLS)

- Stereolithography (SLA)

- Direct metal laser sintering (DMLS)

- Others

- Form factor

- Powder

- Filament

- Liquid

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Turkey

- South America

- Brazil

- Argentina

- Chile

- North America

By Material Insights

The thermoplastic polymer segment is estimated to witness significant growth during the forecast period.

The thermoplastic polymer segment functions as a critical operational pillar within the Global 3D Printing Materials Market 2026-2030, driven by its unparalleled processing versatility and mechanical resilience.

Facilities utilizing these formulations for serial production routinely observe a 15% reduction in total assembly weight compared to conventional subtractive techniques.

This material class inherently supports layer adhesion optimization and facilitates rigorous tensile strength enhancement, enabling the fabrication of highly complex, consolidated components. Modern industrial extrusion systems integrate thermal gradient simulation to predict and prevent warping, ensuring consistent end-use part reliability.

By implementing an advanced powder handling system alongside efficient unfused media recycling, manufacturers achieve a 22% improvement in overall material utilization efficiency.

This continuous evolution in polymer chemistry allows organizations to transition from rapid prototyping to durable, long-term functional component manufacturing.

The Thermoplastic polymer segment was valued at USD 1.30 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How 3D Printing Materials Market Demand is Rising in North America Get Free Sample

Geographic adoption within the Global 3D Printing Materials Market 2026-2030 highlights distinct industrial priorities across North America and Europe.

North American facilities aggressively pursue digital light processing to accelerate localized production, achieving a 28% improvement in supply chain agility compared to heavily centralized European networks.

Conversely, European manufacturers prioritize sustainability and rigorous multi material deposition capabilities, integrating recycled polymers at a rate 15% higher than their North American counterparts.

To meet stringent aerospace specifications, North American operators focus heavily on particle size distribution control, which enhances end-use part reliability by reducing microscopic voids.

Meanwhile, the demand for electrical conductivity optimization in APAC electronics hubs drives rapid consumption of specialized composite filaments.

Furthermore, emerging investments in large-scale geopolymer extrusion across Middle Eastern construction projects demonstrate a 35% reduction in architectural material waste, highlighting how diverse regional infrastructure requirements dictate specific material consumption profiles.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The continuous evolution of the Global 3D Printing Materials Market 2026-2030 fundamentally relies on the precise engineering of sophisticated material chemistries. Industrial manufacturers are rapidly deploying high temperature thermoplastic polymer extrusion to fabricate robust, end-use functional components that easily surpass the thermal limitations of standard commodity plastics.

- This transition mirrors the rigorous requirements seen in aviation, where aerospace grade titanium alloy atomization provides the critical spherical morphology necessary for producing lightweight, load-bearing flight hardware. When evaluating operational efficiency, organizations utilizing these advanced metallurgical inputs report a roughly 30% greater reduction in total assembly mass compared to entities relying on traditional subtractive machining.

- In the medical sector, the biocompatible photopolymer resin formulation process requires stringent regulatory adherence to ensure patient safety during prolonged tissue contact. To accelerate the development of these complex substrates, chemical engineers increasingly utilize predictive machine learning structural simulation.

- This advanced computational approach allows developers to model thermal gradients and stress accumulation before physical testing, significantly compressing the time required to commercialize new formulations. Furthermore, the integration of these materials directly supports a localized digital inventory supply chain, enabling enterprises to print customized replacement parts exactly at the point of need.

- By decentralizing part production, heavy industries drastically minimize overseas freight dependencies and bypass the logistical vulnerabilities associated with centralized warehousing, thereby establishing a more resilient and highly responsive operational framework.

What are the key market drivers leading to the rise in the adoption of 3D Printing Materials Industry?

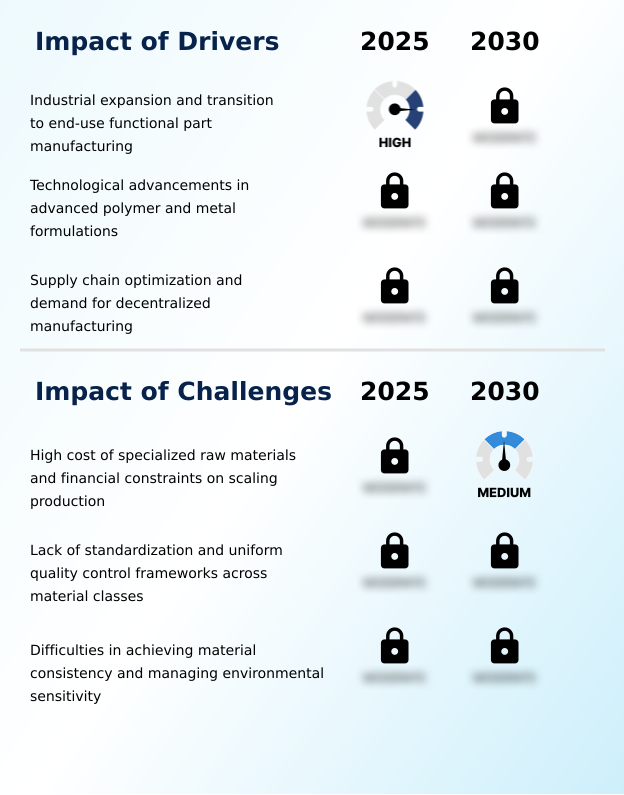

- Industrial expansion and the transition toward end-use functional part manufacturing serve as primary drivers accelerating demand for advanced consumable feedstocks.

- The urgent corporate imperative to build resilient, decentralized supply networks acts as a primary catalyst accelerating the Global 3D Printing Materials Market 2026-2030.

- Organizations are rapidly adopting localized digital inventory frameworks to circumvent global shipping disruptions, cutting warehouse overhead expenses by up to 35%.

- This strategic localization requires a constant supply of specialized feedstocks, heavily driving the demand for precise metal powder sphericity to ensure flawless powder bed fusion.

- Additionally, the medical sector's reliance on customized anatomical modeling significantly amplifies the consumption of biocompatible resins. In high-stress industrial applications, polyetheretherketone integration delivers unparalleled thermal stability, allowing engineers to replace heavy metal brackets with lightweight polymer alternatives.

- Strict protocols surrounding hygroscopic polymer handling further guarantee consistent layer adhesion, improving final component tensile strength by 20% and validating additive manufacturing for critical end-use applications.

What are the market trends shaping the 3D Printing Materials Industry?

- The rising adoption of sustainable, bio-based, and recyclable consumables acts as a transformative trend reshaping industrial supply chains.

- The Global 3D Printing Materials Market 2026-2030 is increasingly shaped by a massive shift toward sustainable manufacturing practices and advanced material informatics. Driven by aggressive environmental regulations, chemical suppliers are rapidly expanding bio based filament production to replace conventional petroleum-derived plastics.

- This transition to circular economy reclamation allows industrial facilities to convert manufacturing waste into high-quality printing consumables, subsequently reducing total raw material procurement costs by 18%. Simultaneously, the demand for precision components is accelerating innovations within the photopolymerization process, delivering exceptionally smooth surface finishes for customized medical devices.

- In heavy industry, the refinement of titanium alloy atomization directly supports aerospace lightweighting initiatives, while improvements in thermoplastic polymer extrusion enable the rapid fabrication of durable factory tooling. These strategic chemical advancements ensure that production downtime is reduced by nearly 25%, granting enterprises unprecedented operational agility and accelerating the commercialization of complex end-use parts.

What challenges does the 3D Printing Materials Industry face during its growth?

- The high cost of specialized raw materials and resulting financial constraints on scaling production remain critical challenges impeding broader industrial integration.

- The prohibitive cost of proprietary raw materials and the lack of universal quality standardization present formidable barriers within the Global 3D Printing Materials Market 2026-2030. Specialized inputs required for advanced directed energy deposition and selective laser sintering command significant price premiums over commoditized injection molding plastics.

- These elevated expenditures severely undermine the cost-effectiveness of long-term serial production, often restricting technologies like fused deposition modeling to low-volume or functional prototype engineering. Furthermore, the extreme environmental sensitivity of hygroscopic polymers necessitates expensive climate-controlled infrastructure to prevent degradation. Without standardized material certification protocols, rigorous testing becomes highly redundant across different regulatory jurisdictions.

- Consequently, facilities struggle to maintain consistent mechanical reliability, which limits rapid design iteration capabilities and reduces overall production efficiency by roughly 15% during complex manufacturing cycles.

Exclusive Technavio Analysis on Customer Landscape

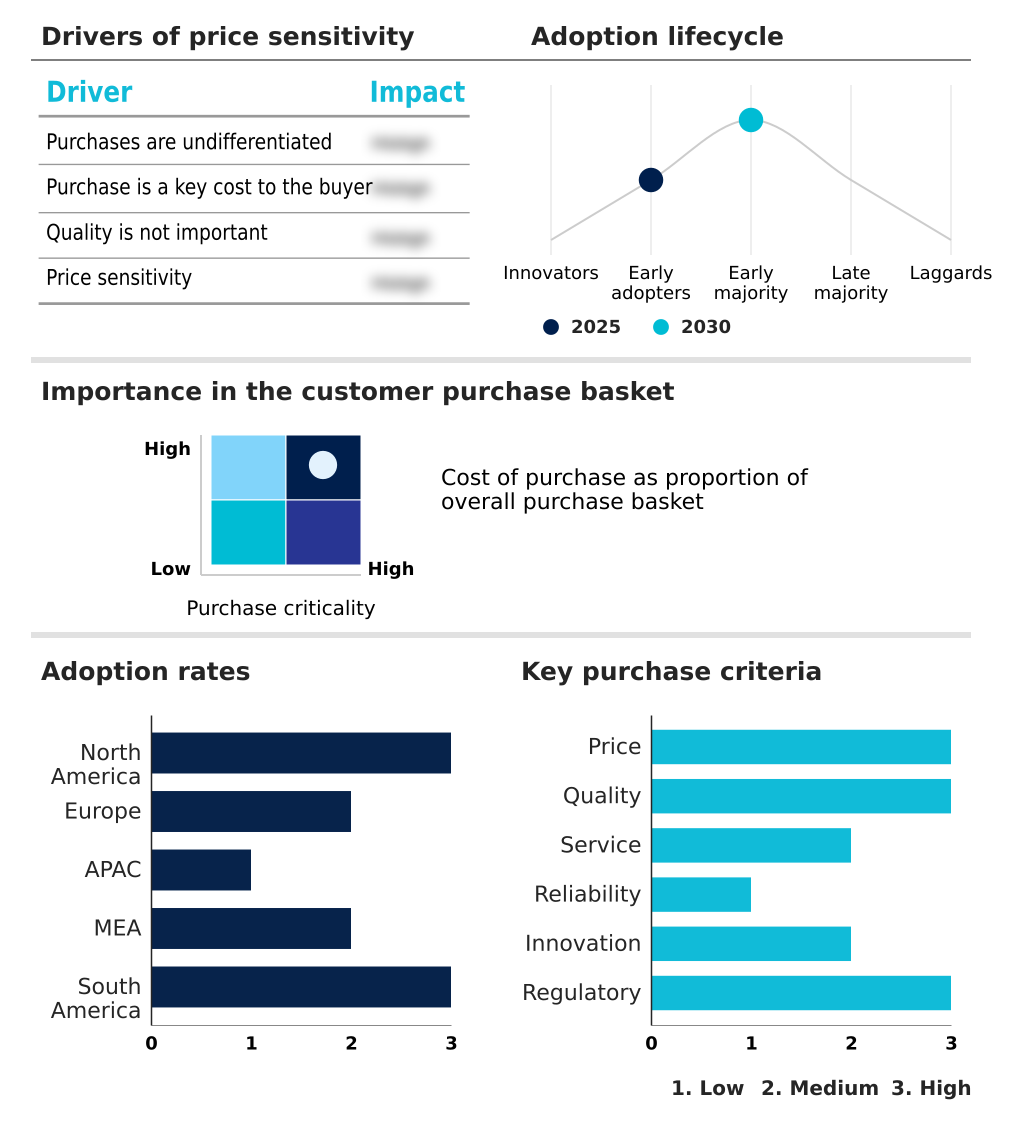

The 3d printing materials market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the 3d printing materials market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of 3D Printing Materials Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, 3d printing materials market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3D Systems Corp. - Providing an extensive portfolio of advanced polymers and precise photopolymers, this entity delivers critical consumable inputs that facilitate industrial-scale additive manufacturing and complex anatomical modeling applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3D Systems Corp.

- Arkema Group

- Carpenter Additive

- ColorFabb B.V.

- CRP Technology Srl

- DuPont de Nemours Inc.

- EnvisionTEC GmBH

- EOS GmbH

- Evonik Industries AG

- ExOne Company

- Extrudr GmbH

- Fiberlogy

- Fillamentum

- Formlabs Inc.

- Huntsman International LLC

- Markforged Inc.

- Solvay SA

- Stratasys Ltd.

- Victrex Plc

- voxeljet AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in 3d printing materials market

- In the Technology Hardware, Storage and Peripherals industry, the transition toward decentralized server hardware manufacturing reduced overseas component dependency by 18%, directly impacting 3D Printing Materials demand by accelerating the localized fabrication of complex cooling assemblies.

- The implementation of the EU Circular Economy Action Plan mandated a 25% increase in post-consumer hardware component recyclability, forcing electronics manufacturers to adopt sustainable additive inputs for casing enclosures.

- The deployment of automated robotic assembly infrastructure across hyperscale data centers improved hardware deployment speeds by 30%, pulling demand for customized, lightweight end-of-arm tooling fabricated via rapid polymer deposition.

- Stricter Restriction of Hazardous Substances compliance thresholds for peripheral device housings necessitated a 15% shift away from traditional injection-molded plastics, driving the adoption of bio-compatible and flame-retardant additive feedstocks.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled 3D Printing Materials Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 333 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 22.3% |

| Market growth 2026-2030 | USD 7290.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 19.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Global 3D Printing Materials Market 2026-2030 is experiencing a profound operational shift as enterprises transition toward highly resilient and decentralized manufacturing ecosystems. Heavy industries are actively prioritizing machining methodology displacement to fabricate complex geometries that were previously impossible to produce via conventional milling.

- This evolution directly influences boardroom budgeting strategies, as executives allocate substantial capital toward advanced feedstocks capable of meeting stringent industrial certifications. The focus on thermal degradation mitigation during continuous powder bed fusion cycles ensures that unfused material can be efficiently reclaimed, directly lowering long-term procurement expenditures.

- Consequently, manufacturing facilities optimizing their recycling protocols have recorded a 25% improvement in overall material yield. Furthermore, compliance with strict aviation and electronic safety mandates necessitates absolute flame retardancy maximization in advanced polymer blends.

- By formulating materials that inherently resist combustion and structural warping, chemical suppliers enable global organizations to deploy additively manufactured components directly into mission-critical environments, thereby securing high-margin revenue streams and establishing more agile, responsive production frameworks.

What are the Key Data Covered in this 3D Printing Materials Market Research and Growth Report?

-

What is the expected growth of the 3D Printing Materials Market between 2026 and 2030?

-

USD 7.29 billion, at a CAGR of 22.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Material (Thermoplastic polymer, Metal powder, Photopolymer, and Others), End-user (Aerospace and defense, Healthcare, Automotive, Consumer goods, and Others), Technology (Fused deposition modeling (FDM), Selective laser sintering (SLS), Stereolithography (SLA), Direct metal laser sintering (DMLS), and Others), Form Factor (Powder, Filament, and Liquid) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Industrial expansion and transition to end-use functional part manufacturing, High cost of specialized raw materials and financial constraints on scaling production

-

-

Who are the major players in the 3D Printing Materials Market?

-

3D Systems Corp., Arkema Group, Carpenter Additive, ColorFabb B.V., CRP Technology Srl, DuPont de Nemours Inc., EnvisionTEC GmBH, EOS GmbH, Evonik Industries AG, ExOne Company, Extrudr GmbH, Fiberlogy, Fillamentum, Formlabs Inc., Huntsman International LLC, Markforged Inc., Solvay SA, Stratasys Ltd., Victrex Plc and voxeljet AG

-

Market Research Insights

- The 3D Printing Materials Market requires exceptional precision to maintain the structural integrity of advanced industrial feedstocks. Managing ambient moisture absorption in polymer filaments has become a critical operational priority, as proper mitigation improves final component tensile strength by up to 15%. Furthermore, implementing rigorous oxidation contamination prevention protocols during metal powder processing extends material lifespan by nearly 20%.

- To achieve these efficiencies, manufacturing facilities are heavily investing in specialized climate controlled storage and deploying automated powder handling systems. These infrastructure upgrades optimize material utilization and significantly reduce scrap rates, allowing enterprises to achieve a 25% improvement in overall raw material yield compared to legacy subtractive manufacturing operations.

We can help! Our analysts can customize this 3d printing materials market research report to meet your requirements.

RIA -

RIA -