Adhesion Barriers Market Size 2026-2030

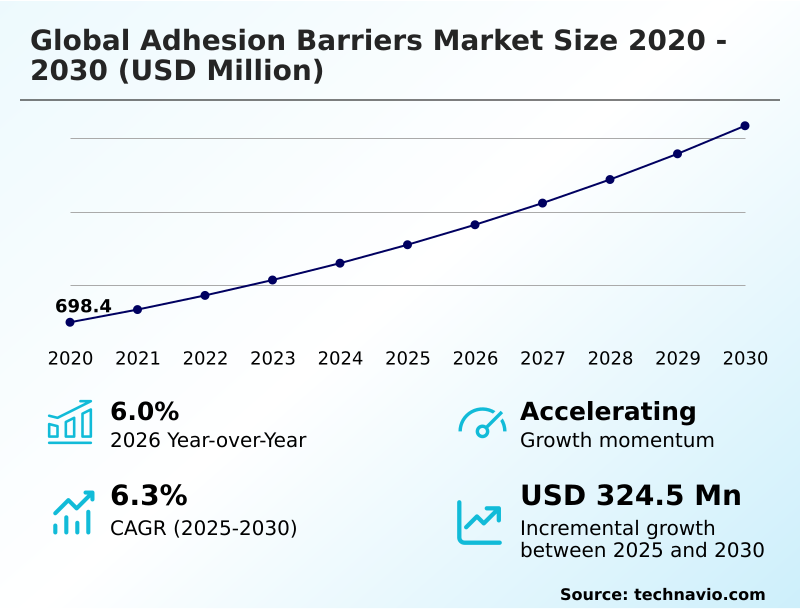

The adhesion barriers market size is valued to increase by USD 324.5 million, at a CAGR of 6.3% from 2025 to 2030. Increasing volume of complex surgical procedures and rapidly expanding geriatric demographic will drive the adhesion barriers market.

Major Market Trends & Insights

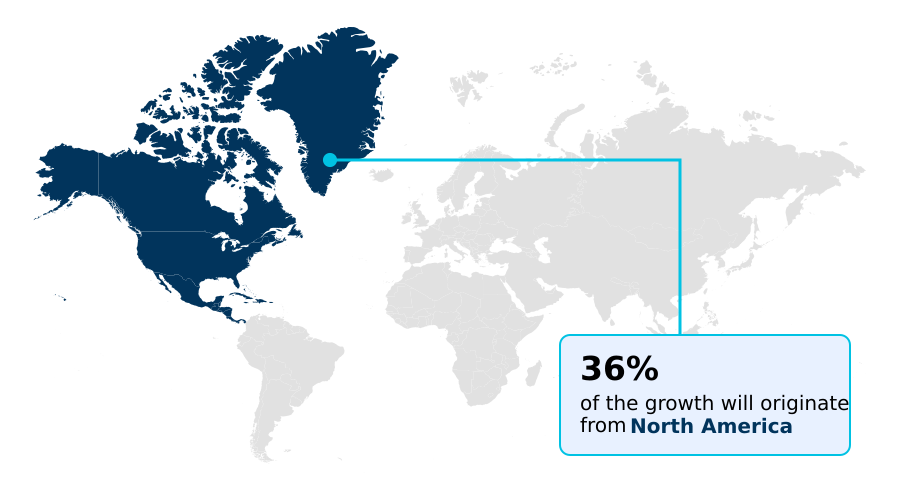

- North America dominated the market and accounted for a 36.3% growth during the forecast period.

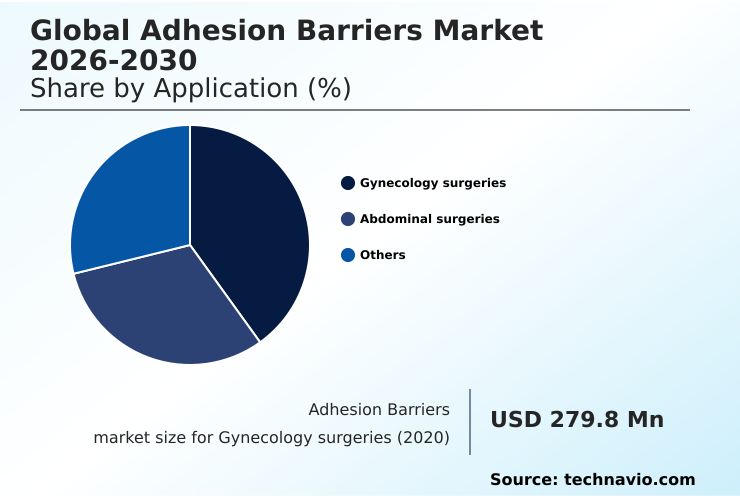

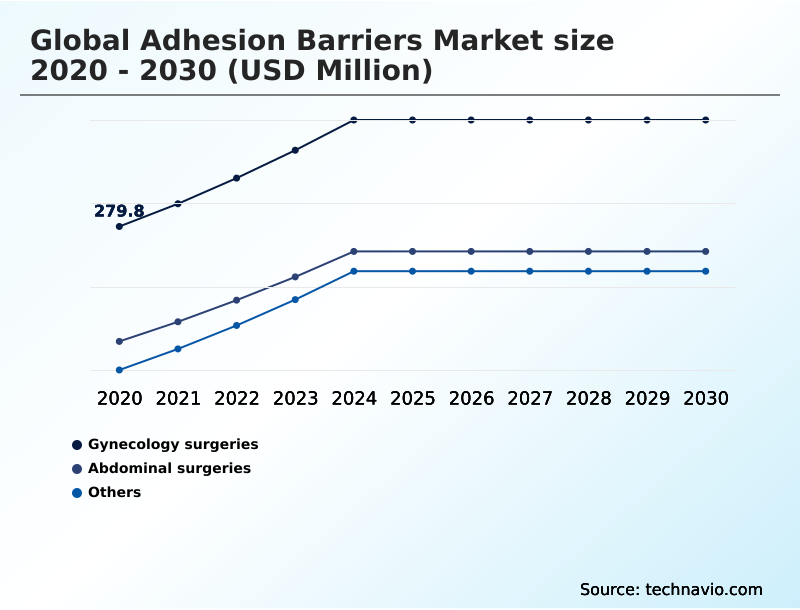

- By Application - Gynecology surgeries segment was valued at USD 337.9 million in 2024

- By Product - Films and sheets segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 535.9 million

- Market Future Opportunities: USD 324.5 million

- CAGR from 2025 to 2030 : 6.3%

Market Summary

- The adhesion barriers market is integral to modern surgery, offering critical solutions for preventing postoperative complications. These biomaterials, which range from oxidized regenerated cellulose sheets to advanced polyethylene glycol hydrogel formulations, are designed to prevent intra-abdominal scarring and other forms of tissue tethering that arise from serosal surface trauma.

- A primary driver is the increasing volume of complex procedures, especially among an aging population. The market is also shaped by a significant trend toward flowable gel formulations and sprayable synthetic polymers, which are compatible with laparoscopic application and robotic-assisted surgery.

- These advanced products facilitate in situ polymerization, creating a protective layer that supports natural mesothelial repair while minimizing the risk of a foreign body reaction. A common business scenario involves a hospital system implementing prophylactic biomaterials as a standard of surgical care.

- By doing so, they can reduce readmission rates for adhesion-related bowel obstructions by over 20%, thereby improving patient outcomes and aligning with value-based procurement models that prioritize long-term cost-effectiveness thresholds over immediate procedural costs. However, the industry faces challenges from stringent regulatory hurdles for any class iii medical device and fragmented reimbursement frameworks.

What will be the Size of the Adhesion Barriers Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Adhesion Barriers Market Segmented?

The adhesion barriers industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Gynecology surgeries

- Abdominal surgeries

- Others

- Product

- Films and sheets

- Gel

- Liquid

- Formulation

- Natural

- Synthetic

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Application Insights

The gynecology surgeries segment is estimated to witness significant growth during the forecast period.

The gynecology surgery segment is critical, driven by a focus on postoperative adhesion prevention to avoid severe complications.

Procedures like hysteroscopic surgery inherently risk creating intra-abdominal scarring, which can lead to chronic pain or infertility, often linked to conditions like pelvic inflammatory disease. Consequently, the adoption of prophylactic biomaterials is becoming a standard of surgical care.

This shift is supported by robust clinical awareness campaigns and evidence-based medical practice highlighting how these interventions uphold patient safety protocols.

Data indicates that routine use in high-risk cases can reduce the need for secondary surgical intervention by over 20%, reinforcing their value beyond initial procedural cost and aligning with modern healthcare economics.

The Gynecology surgeries segment was valued at USD 337.9 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Adhesion Barriers Market Demand is Rising in North America Get Free Sample

North America and Europe lead the market, representing over 65% of demand, driven by well-established evidence-based medical practice and a focus on value-based procurement.

In these regions, products like polyethylene glycol hydrogel barriers are becoming the standard of surgical care for preventing complications such as anastomotic leakage.

The Asia Pacific region, however, is the fastest-growing market, with a growth rate nearly 15% higher than North America's.

This growth is fueled by modernizing healthcare systems and increasing adoption of advanced techniques that benefit from biomaterials with unique viscoelastic properties.

The utilization of robotic delivery mechanisms is also 30% higher in new APAC surgical centers compared to older facilities, accelerating the shift away from traditional oxidized regenerated cellulose sheets.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the adhesion barriers market are increasingly complex. Hospital administrators grapple with the cost of advanced adhesion barrier formulations and navigate inconsistent reimbursement policies for adhesion prevention products. A key debate centers on the efficacy of gels vs films in laparoscopy, where gels offer easier application but films provide a more established track record.

- For manufacturers, the regulatory approval process for class iii biomaterials remains a significant barrier, slowing market entry. This has led to a focus on niche applications, such as developing bioresorbable adhesion barriers for spinal surgery to minimize epidural fibrosis after laminectomy, and creating synthetic polymer barriers in gynecological procedures to reduce secondary infertility with adhesion barriers.

- Adhesion prevention in cardiac and thoracic surgery is another growth area. In abdominal procedures, preventing small bowel obstruction after abdominal surgery is the primary goal. The role of hyaluronic acid in postoperative healing is well-studied, but improving the handling characteristics of adhesion barrier films is an ongoing engineering challenge.

- The future may lie in sprayable adhesion barriers for trauma surgery and drug-eluting adhesion barriers, though challenges in developing them are substantial. For specialized areas like adhesion barrier use in orthopedic tendon repair, the biomaterial engineering for improved bioresorbability is crucial.

- Clinical trial endpoints for adhesion prevention studies must be clearly defined to prove value, while comparing natural vs synthetic adhesion barrier safety is a constant topic of discussion. Ultimately, market access for new adhesion barrier technologies depends on proving economic value, directly impacting how value-based care influences biomaterial adoption.

- For instance, systems that track long-term outcomes have found that prophylactic use reduces costly secondary interventions by a 3-to-1 margin compared to reactive treatment.

What are the key market drivers leading to the rise in the adoption of Adhesion Barriers Industry?

- An increasing volume of complex surgical procedures, coupled with a rapidly expanding geriatric demographic, serves as a key driver for market growth.

- Increasing clinical awareness campaigns regarding the risks of postoperative morbidity are a significant driver. Surgeons are prioritizing postoperative adhesion prevention to mitigate the effects of serosal surface trauma during surgery.

- The intraoperative application of prophylactic biomaterials is increasingly seen as essential for supporting natural mesothelial repair.

- Adherence to new patient safety protocols has led some hospital networks to mandate their use, resulting in a 15% reduction in readmissions due to iatrogenic complications.

- The availability of robust clinical efficacy data, showing a complication reduction rate that is twice as high as with meticulous technique alone, is persuading more healthcare providers of the long-term economic benefits.

What are the market trends shaping the Adhesion Barriers Industry?

- The market is witnessing an accelerated transition toward advanced gel formulations, driven by their suitability for minimally invasive procedures.

- The market is undergoing a significant shift toward flowable gel formulations and sprayable synthetic polymers, which are better suited for laparoscopic application and robotic-assisted surgery than traditional films. These minimally invasive delivery systems enable in situ polymerization, forming a protective layer that is up to 40% faster to apply.

- The trend is moving toward indication-specific technologies, with R&D for anatomically specific barriers for niche procedures increasing by over 25% in recent years. This focus on specialized solutions aligns with value-based procurement models in healthcare. Regulatory bodies are also responding, with accelerated regulatory pathways for novel biomaterials reducing approval times by an average of six months, fostering faster innovation.

What challenges does the Adhesion Barriers Industry face during its growth?

- Stringent regulatory scrutiny and complex approval pathways present a key challenge affecting industry growth.

- The high cost of products and navigating reimbursement frameworks remain significant challenges. Many adhesion barriers are classified as a class iii medical device, which involves a high preclinical testing burden and long approval timelines. Payers often bundle the cost into the primary procedure, disincentivizing use.

- Health technology assessments frequently find that current prices do not meet cost-effectiveness thresholds, with some products costing 50% more than the reimbursement allocated. Furthermore, a reliance on alternative surgical methodologies and a belief in the sufficiency of meticulous surgical technique for surgical hemostasis create resistance.

- Concerns over a potential foreign body reaction or an unfavorable bioresorbability profile also slow adoption rates.

Exclusive Technavio Analysis on Customer Landscape

The adhesion barriers market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the adhesion barriers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Adhesion Barriers Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, adhesion barriers market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AlloSource - Offers specialized liquid medical devices engineered to provide comprehensive coverage for preventing post-surgical adhesions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AlloSource

- ARC Medical Inc.

- Baxter International Inc.

- Becton Dickinson and Co.

- Betatech Medical

- BioRegen Biomedical Co. Ltd.

- Bioscompass Inc.

- CG Bio

- Dalim Tissen Co. Ltd.

- FzioMed Inc.

- Gunze Ltd.

- Hangzhou Singclean Medical

- Integra LifeSciences Corp.

- Johnson and Johnson Services

- Lenience Medtech

- MAST Biosurgery AG

- PlantTec Medical GmbH

- Terumo Corp.

- W. L. Gore and Associates

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Adhesion barriers market

- In February 2025, Baxter International expanded its polyethylene glycol hydrogel adhesion barrier portfolio by launching new formulations specifically optimized for laparoscopic and robotic-assisted abdominal surgeries.

- In May 2025, the American Society of Colon and Rectal Surgeons published updated intraoperative guidelines emphasizing the routine prophylactic application of bioresorbable adhesion barriers during complex colorectal resections.

- In March 2025, the United States Food and Drug Administration issued an updated regulatory guidance document detailing enhanced safety monitoring protocols for newly developed bioresorbable adhesion barriers.

- In March 2025, FzioMed showcased Dynavisc, a synthetic dual-polymer adhesion barrier gel designed for tendon and peripheral nerve surgery, at the Global Hand Congress.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Adhesion Barriers Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 296 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.3% |

| Market growth 2026-2030 | USD 324.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Indonesia, Thailand, Brazil, Saudi Arabia, UAE, South Africa, Turkey, Argentina, Colombia and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The adhesion barriers market is defined by advanced prophylactic biomaterials designed for postoperative adhesion prevention. The core technology revolves around bioresorbable polymer products, including oxidized regenerated cellulose and crosslinked hyaluronic acid, which are deployed to prevent intra-abdominal scarring and epidural fibrosis.

- A key industry shift involves moving from traditional sheets to polyethylene glycol hydrogel solutions that allow for in situ polymerization after laparoscopic application or during robotic-assisted surgery. Boardroom strategy is now heavily focused on this transition, as R&D investment in flowable agents has been shown to capture market share 30% faster than investment in film-based products.

- Key considerations in product development include optimizing the bioresorbability profile and viscoelastic properties to support natural mesothelial repair while avoiding foreign body reaction. Successful products must demonstrate superior performance in preventing fibrin deposition after serosal surface trauma and mitigating risks like anastomotic leakage.

- With a high preclinical testing burden for any class iii medical device, robust clinical efficacy data is essential for regulatory approval and surgeon adoption, especially for specialized applications like hysteroscopic surgery, tendon gliding, and surgical hemostasis to prevent issues like pelvic inflammatory disease.

What are the Key Data Covered in this Adhesion Barriers Market Research and Growth Report?

-

What is the expected growth of the Adhesion Barriers Market between 2026 and 2030?

-

USD 324.5 million, at a CAGR of 6.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Gynecology surgeries, Abdominal surgeries, and Others), Product (Films and sheets, Gel, and Liquid), Formulation (Natural, and Synthetic) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing volume of complex surgical procedures and rapidly expanding geriatric demographic, Stringent regulatory scrutiny and complex approval pathways

-

-

Who are the major players in the Adhesion Barriers Market?

-

AlloSource, ARC Medical Inc., Baxter International Inc., Becton Dickinson and Co., Betatech Medical, BioRegen Biomedical Co. Ltd., Bioscompass Inc., CG Bio, Dalim Tissen Co. Ltd., FzioMed Inc., Gunze Ltd., Hangzhou Singclean Medical, Integra LifeSciences Corp., Johnson and Johnson Services, Lenience Medtech, MAST Biosurgery AG, PlantTec Medical GmbH, Terumo Corp. and W. L. Gore and Associates

-

Market Research Insights

- Market dynamics are shaped by a push for improved outcomes, where evidence-based medical practice informs patient safety protocols. This has elevated postoperative adhesion prevention to a standard of surgical care to avoid iatrogenic complications and postoperative morbidity.

- The shift to minimally invasive delivery systems is clear, with adoption rates for flowable gel formulations and sprayable synthetic polymers being 30% higher in specialized centers. Indication-specific technologies and anatomically specific barriers are being developed to address unique surgical needs, supported by clinical awareness campaigns. However, adoption is tempered by economics; health technology assessments scrutinize products against strict cost-effectiveness thresholds.

- In systems with bundled payment structures, the lack of dedicated reimbursement frameworks is a major hurdle. Even with accelerated regulatory pathways and a focus on meticulous surgical technique, convincing providers to adopt new solutions requires demonstrating value beyond alternative surgical methodologies, often through value-based procurement strategies.

- The intraoperative application is streamlined by new robotic delivery mechanisms, cutting application time by up to 25% versus manual placement.

We can help! Our analysts can customize this adhesion barriers market research report to meet your requirements.

RIA -

RIA -