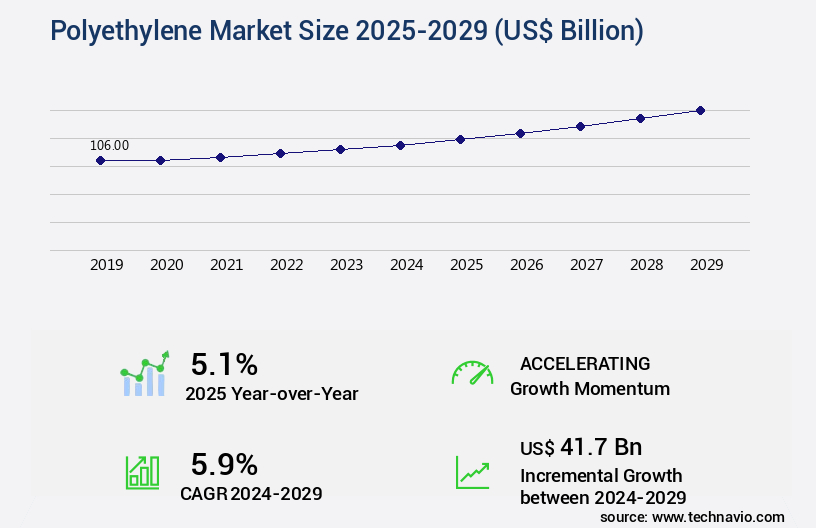

Polyethylene Market Size 2025-2029

The polyethylene market size is forecast to increase by USD 41.7 billion, at a CAGR of 5.9% between 2024 and 2029.

- The market is experiencing significant growth due to the increasing demand for polyethylene products across various sectors including packaging, construction, medical, and automotive industries. The versatility of polyethylene, which makes it suitable for various applications, is driving this trend. New developments in the utilization of polyethylene, particularly in the packaging and automotive industries, are further fueling market expansion. However, the market faces challenges from the volatility in raw material prices, which can impact the profitability of manufacturers.

- Effective supply chain management and price risk mitigation strategies are essential for companies seeking to capitalize on market opportunities and navigate these challenges successfully.

What will be the Size of the Polyethylene Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market continues to evolve, driven by the versatility and applications of synthetic polyethylene across various sectors. With a molecular structure consisting of nonpolar saturated hydrocarbons, polyethylene (PE) exhibits desirable chemical properties, including high chemical resistance and low water absorption. PE's applications span from consumer goods, such as plastic bags and packaging, to industrial polymers used in pipes, fittings, and electrical insulation. The market dynamics are shaped by the ongoing research and development in catalysts, including metallocene and Ziegler-Natta catalysts, which influence the polyethylene's crystalline arrangements and melting points. High-density PE, with its superior mechanical strength, is preferred in cable jacketing and construction materials.

Meanwhile, low-density PE, such as linear low-density PE and medium-density PE, is utilized in flexible materials like films and sheets for food packaging, pharmaceutical packaging, and agricultural nets. The PE market's continuous unfolding is also influenced by recycling activities and the demand for sustainable solutions, leading to the emergence of bio-based PE and recycled PE. As PE's applications expand, its impact on various industries and the environment continues to evolve, making it a dynamic and ever-changing market. Synthetic PE's versatility, coupled with advancements in catalysts and the increasing focus on sustainability, ensures the PE market remains an intriguing and evolving landscape.

How is this Polyethylene Industry segmented?

The polyethylene industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

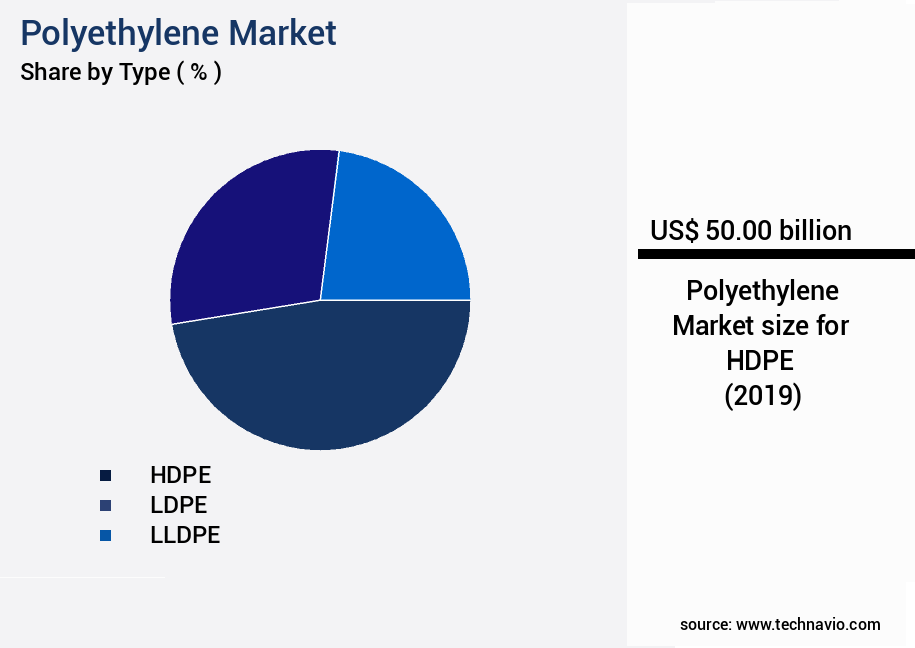

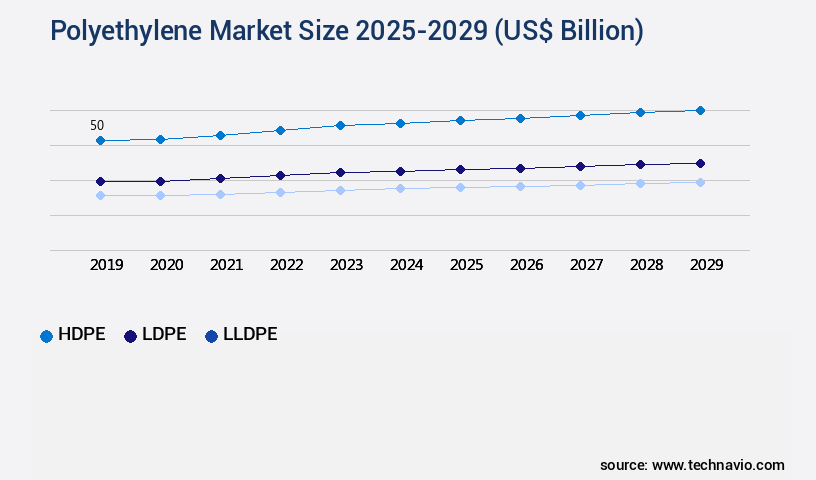

- Type

- HDPE

- LDPE

- LLDPE

- End-user

- Packaging

- Construction

- Consumer goods

- Agriculture

- Others

- Method

- Blow molding

- Extrusion

- Injection molding

- Form Factor

- Pellets

- Granules

- Powder

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Type Insights

The HDPE segment is estimated to witness significant growth during the forecast period. High-density polyethylene (HDPE), a rigid and robust type of polyethylene, is extensively used in various industries due to its superior chemical resistance and mechanical strength. HDPE's inflexible nature makes it suitable for producing bottles and containers for consumer goods, such as shampoo and milk. Its lightweight properties allow for the production of thin, yet durable materials, like HDPE foils used in food packaging for items like cookies and snacks. Additionally, HDPE is used in industrial applications, such as pipes and fittings for water and gas distribution, as well as in electrical insulation. Recycling activities have led to the reuse of HDPE materials, including milk jugs and plastic bags, which have gained popularity due to their sustainability.

The HDPE segment was valued at USD 50.00 billion in 2019 and showed a gradual increase during the forecast period. The chemical composition of HDPE is based on nonpolar saturated hydrocarbons, and its molecular structure consists of long chains of ethylene monomers. HDPE's high melting point and crystalline arrangements contribute to its desirable physical properties. Furthermore, HDPE can be modified through the addition of other monomers, such as vinyl acetate, to create copolymers with unique properties. HDPE's versatility and wide range of applications make it a significant player in the synthetic the market.

Regional Analysis

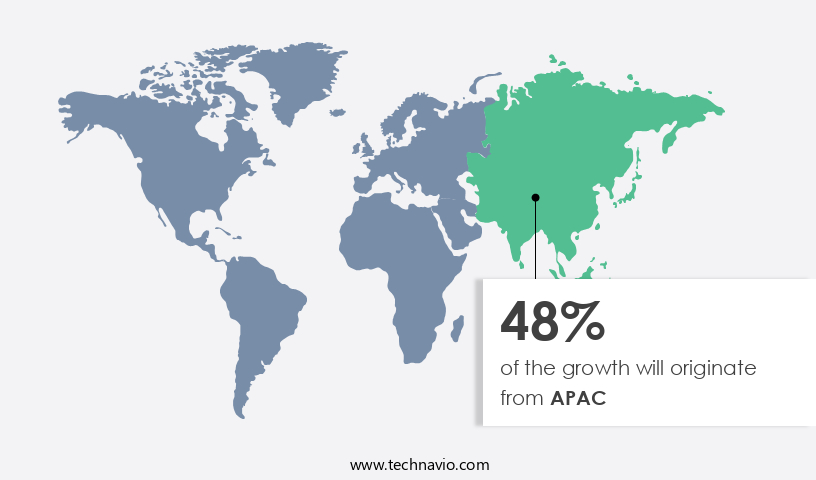

APAC is estimated to contribute 48% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

Polyethylene, a synthetic resin derived from ethylene monomers, exhibits significant market activity, particularly in the Asia-Pacific (APAC) region. Countries like India and China are major contributors to the regional the market due to the growing number of middle-class consumers. The annual per capita plastic consumption in India is estimated to be around 9.5 kilograms. This figure is anticipated to increase substantially due to population growth. In APAC, polyethylene finds extensive use in various applications, including packaging films for food and pharmaceuticals, flexible materials for automotive components, pipes for construction, and fittings for electrical insulation. Furthermore, the economic development of countries like India and China fuels the demand for polyethylene in industrial sectors.

The molecular structure of polyethylene, characterized by its linear and branched chains, offers chemical resistance and high mechanical strength. Its low water absorption and melting points make it suitable for various applications in consumer goods and construction materials. Additionally, the production of ethylene from nonpolar saturated hydrocarbons, such as aromatic hydrocarbons, is a significant factor driving the market. The use of catalysts like Ziegler-Natta and metallocene catalysts in the polymerization process enhances the production efficiency and product quality. The recycling of polyethylene through various recycling codes and activities further supports the market's growth. Cross-linked polyethylene and high-density cross-linked polyethylene are also gaining popularity due to their improved properties, such as impact strength and crystalline arrangements.

The market is expected to continue its growth trajectory, driven by the increasing demand for sustainable and eco-friendly alternatives, such as bio-based polyethylene.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is a significant segment of the global plastics industry, characterized by its versatile applications and substantial growth potential. This market encompasses various types of polyethylene, including low-density polyethylene (LDPE), high-density polyethylene (HDPE), and linear low-density polyethylene (LLDPE). Demand for polyethylene is driven by its extensive use in packaging, agriculture, construction, automotive, and electrical industries. Polyethylene's unique properties, such as its excellent chemical resistance, thermal stability, and flexibility, make it a preferred choice for numerous applications. Manufacturers continuously innovate to produce polyethylene with enhanced performance characteristics, such as improved strength, durability, and recyclability. Global trends, including the shift towards sustainable packaging and the increasing demand for Biodegradable Plastics, are influencing the market. Furthermore, advancements in polyethylene production technologies, such as single-site catalysis and metallocene catalysts, are enabling the creation of high-performance polyethylene products. Innovative applications, such as polyethylene foams, geomembranes, and 3D printing filaments, are expanding the market's reach. Despite challenges, including increasing raw material costs and environmental concerns, the market continues to grow, offering lucrative opportunities for stakeholders.

What are the key market drivers leading to the rise in the adoption of Polyethylene Industry?

- The significant expansion in the demand for polyethylene products across various sectors serves as the primary catalyst for market growth.

- The market is experiencing significant growth due to the increasing demand for plastic, particularly in Asia. Countries like India and China have the highest demand for plastics, driven by their rapidly expanding economies and industrialization. In India, the demand for plastics is particularly high in the electronics sector, which is growing at an estimated annual rate of 17%. This growth is fueled by a burgeoning customer base and advances in technology. Additionally, large investments are being made in sectors such as irrigation, power, water and sanitation management, building and construction, retail, transport, and others.

- Polyethylene, a type of synthetic resin, is widely used in various applications due to its excellent impact strength and crystalline arrangements. Medium-density polyethylene (MDPE) and low-density polyethylene (LDPE) are the most commonly used types. The recycling of polyethylene is a significant activity, with various recycling codes in place to facilitate the process. Recycled polyethylene is used in the production of new products, reducing the need for virgin materials and minimizing the environmental impact. Ziegler-Natta catalysts are used in the production of polyethylene. These catalysts enable the creation of specific crystalline arrangements, resulting in polymers with unique properties.

- Cross-linked polyethylene is a type of polyethylene that offers enhanced properties, such as improved strength and heat resistance, making it suitable for use in construction materials and other demanding applications. In conclusion, The market is driven by the increasing demand for plastic, particularly in Asia. The market is characterized by the use of various types of polyethylene, including MDPE and LDPE, and the recycling of polyethylene to reduce environmental impact. The use of Ziegler-Natta catalysts enables the production of specific crystalline arrangements, resulting in polymers with unique properties. The market is expected to continue growing due to the increasing demand for plastics in various industries.

What are the market trends shaping the Polyethylene Industry?

- The application of polyethylene is experiencing new advancements, emerging as a significant market trend. This progressive development in polyethylene technology is a noteworthy trend in the industry.

- The market has witnessed significant advancements in the production of Synthetic Polyethylene, leading to the emergence of high-performance types such as high-density cross-linked polyethylene (HDXLPE) and ultra-high molecular weight polyethylene (UHMWPE), also known as high-modulus polyethylene (HMPE). UHMWPE is gaining popularity due to its unique features, which include high mechanical strength, chemical resistance, and self-lubrication. These properties make UHMWPE an ideal choice for various industries, including cable jacketing, consumer goods, and industrial applications. UHMWPE's applications span across bearings, conveyor lines, food processing equipment, gears, marine equipment, pistons, valves, water treatment, and wear strips. Its chemical resistance, low moisture absorption, low dielectric constant, low friction coefficient, high thermal conductivity, and resistance to UV radiation make it a preferred material in these sectors.

- The increasing demand for UHMWPE in high-performance applications, such as gaskets, gear wheels, hammers, filters, and cutting boards, is a notable trend in the market. UHMWPE's superior properties have been achieved through the use of advanced catalysts, such as metallocene catalysts, which have revolutionized the production process of PE. These advancements are expected to further fuel the growth of the market, as industries continue to seek materials with enhanced performance and durability.

What challenges does the Polyethylene Industry face during its growth?

- The volatility in raw material prices, particularly for polyethylene, poses a significant challenge and impedes growth in the industry.

- The global polyethylene packaging market is influenced by the price volatility of raw materials, primarily ethylene, which is a petroleum derivative. This volatility is due to the dependence on Crude Oil prices. The increasing demand for polyethylene packaging in emerging economies further hinders market growth. Polyethylene packaging types, such as Low-Density Polyethylene (LDPE) and High-Density Polyethylene (HDPE), are subject to these price fluctuations as well. Their chemical composition and physical properties make them essential in various industries, including food packaging, pharmaceutical packaging, pipes and fittings, and electrical insulation.

- LDPE, known for its flexibility and low water absorption, is widely used in food packaging. Linear low-density polyethylene (LLDPE), an ethylene copolymer, offers improved properties and is commonly used in films and sheets. Despite the challenges, the market's growth is driven by the superior chemical and physical properties of polyethylene packaging, making it a preferred choice for various applications.

Exclusive Customer Landscape

The polyethylene market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the polyethylene market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, polyethylene market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arkema - The company specializes in providing a range of polyethylene solutions, including Kollisolv PEG 400 LA, PEG 600 LA, PEG 300, and PEG 300 G. These offerings cater to various industries and applications, showcasing our commitment to innovation and quality.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arkema

- BASF SE

- Borealis AG

- Braskem SA

- Chevron Corp.

- China National Petroleum Corp.

- China Petrochemical Corp.

- Ducor Petrochemicals B.V.

- Eni SpA

- Exxon Mobil Corp.

- Formosa Plastics Corp.

- INEOS Group Holdings S.A.

- LyondellBasell Industries NV

- NOVA Chemicals Corp.

- Reliance Industries Ltd.

- Saudi Basic Industries Corp.

- Sumitomo Chemical Co. Ltd.

- The Dow Chemical Co.

- TotalEnergies SE

- USI Corporation

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Polyethylene Market

- In January 2024, LyondellBasell Industries N.V., a leading plastics and chemicals company, announced the successful start-up of a new high-density polyethylene (HDPE) production line at its Wesseling, Germany, site. This expansion increased the company's European HDPE capacity by 300,000 metric tons per annum, strengthening its market position (LyondellBasell Press Release, 2024).

- In March 2024, INEOS Styrolution, the world's leading styrenics supplier, and SABIC, a global chemicals manufacturer, entered into a strategic collaboration to develop and commercialize innovative polyethylene products. This partnership aimed to combine INEOS Styrolution's expertise in styrenics and SABIC's capabilities in polyethylene, targeting the automotive, packaging, and electrical and electronics industries (INEOS Styrolution Press Release, 2024).

- In May 2024, Sinopec, China's largest oil and gas company, and Saudi Aramco, the world's largest oil company, signed a memorandum of understanding (MOU) to explore potential collaboration in the market. The agreement focused on sharing technology, expertise, and resources to enhance their respective polyethylene businesses and expand their market presence in China and the Middle East (Sinopec Press Release, 2024).

- In April 2025, Covestro AG, a leading polymer manufacturer, received regulatory approval from the European Commission for its new polyethylene production facility in Poland. The €1.2 billion project, which will have an annual capacity of 750,000 metric tons, is expected to commence operations in 2026, making Covestro a major player in the European the market (Covestro Press Release, 2025).

Research Analyst Overview

- The market encompasses various types, including medium-density (MDPE), high-density (HDPE), and low-density (LDPE) polymers. Each type exhibits unique physical properties, such as melting points and chemical resistance, making them suitable for diverse applications. Addition polymers derived from aromatic hydrocarbons and nonpolar saturated hydrocarbons are essential building blocks in producing these polyethylene variants. The chemical resistance of PE makes it an ideal choice for manufacturing plastic films and bags. MDPE, with its high impact strength, is widely used in the production of plastic pipes, while HDPE's superior mechanical strength is preferred for containers and geomembranes.

- LDPE, known for its flexibility, is commonly used in packaging applications. Electrical insulation is another significant market for HDPE due to its excellent chemical properties and electrical insulation capabilities. The versatility of polyethylene, with its varying densities and properties, continues to drive its demand across industries.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Polyethylene Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

254 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.9% |

|

Market growth 2025-2029 |

USD 41.7 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.1 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Polyethylene Market Research and Growth Report?

- CAGR of the Polyethylene industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the polyethylene market growth of industry companies

We can help! Our analysts can customize this polyethylene market research report to meet your requirements.

RIA -

RIA -