Enjoy complimentary customisation on priority with our Enterprise License!

The advanced high strength steel market is is forecast to increase by USD 13.26 billion at a CAGR of 11.15% between 2022 and 2027.

The market's expansion hinges on various factors, notably the surging demand for Advanced High-Strength Steel (AHSS) within the automotive sector, driven by its lightweight properties and enhanced safety features. Furthermore, the thriving global construction industry presents lucrative opportunities for AHSS applications due to its structural integrity and durability. AHSS offers distinct advantages over conventional steel, including superior strength and formability, further propelling its adoption across diverse industries. With AHSS emerging as a preferred material, manufacturers are poised to capitalize on its potential to revolutionize structural design and meet evolving industry standards.

To learn more about this market research report, Download Report Sample

This report extensively covers market segmentation by grade type (dual phase steel, complex phase, transformation-induced plasticity, and others), end-user (automobile, construction, aviation and marine, and others). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021. The advanced high-strength steel (AHSS) market is witnessing significant growth, driven by increasing demand for lightweight and high-performance materials across various industries. With a focus on reducing environmental effects and improving efficiency, AHSS finds applications in diverse sectors like rail coach building, automotive parts, and solar panel roofing systems. Its mechanical properties and tensile strength make it ideal for manufacturing lightweight components, facilitating weight reduction in vehicles, especially electric and hybrid vehicles. Additionally, stringent regulations on GHG and CO2 emission levels are accelerating the adoption of AHSS in the manufacturing sector and aerospace industry. As iron ore prices fluctuate, AHSS offers a cost-effective solution while maintaining superior performance, driving its adoption in various vessel manufacturers and AHSS grades.

The market share growth by the dual-phase segment will be significant during the forecast period. It is a class of materials that includes dual-phase (DP steels). Low- to medium-carbon having between 5% and 50% volume fractional martensitic islands that are scattered across a soft ferrite matrix is known as ferrite-martensite dual-phase . There may also be bainite and retained austenite components in addition to martensite; these are typically formed when greater edge stretch formability is sought. Dual-phase have a wide range of strength and ductility due to these changes in microstructure. It is well known have a high energy absorption capacity. These features make it extremely desirable for automotive applications, especially when combined with a cheap production cost.

Get a glance at the market growth analysis contribution of various segments Request a PDF Sample

The dual-phase segment was valued at USD 5.79 billion in 2017 and continued to grow by 2021. It has a high-strain redistribution capacity due to their high-strain hardenability. This translates to better drivability and mechanical qualities (yield strengths) of the completed item that are higher than the blank. In addition, offer a key advantage over traditional HSLA-type materials in the form of bake hardening. The bake hardening effect is an increase in yield strength brought on by the curing temperature of the paint bake cycle, which results in enhanced temperature aging. Such wide benefits are expected to drive the growth of the segment in the global AHSS market during the forecast period.

Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.The advanced high-strength steel (AHSS) market is experiencing significant growth due to its versatility and wide range of applications. With increasing concerns about environmental effects and stringent steel industry regulations, there is a growing demand for third-generation steel that offers superior performance while reducing carbon emissions. AHSS finds extensive use in various sectors, including rail coach building and solar panel roofing systems, where its high strength low alloy steels play a crucial role. Moreover, AHSS contributes to weight reduction in automotive parts, particularly in electric and hybrid vehicles, thanks to its exceptional mechanical properties such as yield strength and tensile strength. As iron ore prices fluctuate, companies like Tata Steel are investing in AHSS to mitigate costs while ensuring the production of high-quality steel with minimum tensile strength GHG and CO2 emission levels.

Market Driver

The growing demand in the automobile industry is the key factor driving the global advanced high-strength (AHSS) market growth. The market refers to the production and sale of Type AHSS, which exhibits high yield strengths ranging from 700 to 2,000 N/mm2. These steels are primarily used in various end-use industries, including automotive, aviation, construction, and energy, due to their superior mechanical properties and enhanced corrosion resistance. The global AHSS market is projected to grow significantly during the forecast period, driven by the automotive industry's demand for lightweight and fuel-efficient vehicles. AHSS are used extensively in automobile manufacturing for body panels, chassis, fuel tank guards, and other components, contributing to weight reduction and improved consumer safety. In emerging economies, domestic requirements and economic growth fuel the demand for AHSS in the construction industry, commercial sector, and residential sector, creating employment opportunities and boosting the steel industry. Despite production costs and raw materials' price fluctuations, including iron ore, the market is expected to be restrained by governments' investments, support, and rules and regulations, as well as safety norms and carbon emissions concerns. Advancements in steel grade’s minimum yield strength and their weldability continue to drive market growth. Growing innovations and the rising demand for fuel-efficient and lightweight vehicles are expected to drive the demand in the automobile industry during the forecast period.

Market Trends

The increasing use of secondary AHSS is the main trend driving the growth of the market. Secondary are high-strength steels, which have strength and durability similar to that of AHSS. The market is experiencing significant growth due to increasing environmental concerns and the rise in renewable energy sources, particularly in the power generation sector. The share of renewables in global electricity generation with wind energy being a major contributor. In the context of AHSS, this market is driven by its type, end-use industry, and region. The automotive industry is a major end-user, with AHSS being used for body panels due to its superior mechanical properties, including high-yield strengths, formability, weldability, and corrosion resistance. The construction industry, commercial sector, and residential sector also utilize AHSS due to its weight reduction capabilities, toughness, and safety norms compliance. The markets for AHSS are spread across regions, with emerging economies such as China, India, and Brazil showing significant growth due to domestic requirements, economic growth, and consumer demand for a luxurious lifestyle. The forecast period for the AHSS market is expected to be influenced by production costs, raw materials, and iron ore prices, as well as government investments, rules and regulations, and safety norms in the steel industry. However, governments' support through investments and rules and regulations are expected to drive the market forward. The steel industry is also making advancements in steel grades to meet the evolving needs of various end-use industries.Therefore, with the growing shift to reduce carbon emissions, the demand for secondary steel is expected to rise during the forecast period.

Market Challenge

The volatile prices of raw materials are a major challenge to the market growth. Crude is produced from iron ore using blast furnaces or electric arc furnaces. Every year, around 1.5-1.8 billion tons is produced from 2-3 billion tons of iron ore globally. In the past few years, the prices of iron ore have witnessed major fluctuations, which has affected the prices of crude steel and finished steel products. Although the demand for steel is increasing in the automotive, construction, marine, aviation, and other industries, the fluctuating prices of raw materials are hampering the growth of the steel market.

Moreover, the fluctuating prices of iron ore are attributed to the mining disruptions in Australia and Brazil. Such disruptions reduce iron ore production, and subsequently, the prices increase. The disruptions have also reduced the import rate in China as the shipments from both Australia and Brazil have decreased significantly.Governments, investments, and support through rules and regulations in the steel industry aim to ensure safety norms, reduce carbon emissions, and foster advancements in steel grades. In addition, owing to revised environmental policies, China is expected to restrict its production, which will increase the prices of iron ore and steel. Therefore, the increase in the prices is expected to limit the growth of the global market during the forecast period.

Customer Landscape

The Market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth and forecasting strategies.

Market Customer Landscape

Vendors are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Arcelor Mittal - The company offers advanced high-strength steel such as SIRIUS 310S, UR 317LMN, VIRGO 39, UREA 310 MoLN.

The report also includes detailed analyses of the competitive landscape of the market and information about 15 market players, including:

Qualitative and quantitative analysis of vendors has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize vendors as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize vendors as dominant, leading, strong, tentative, and weak.

For more insights on the market share of various regions Request PDF Sample now!

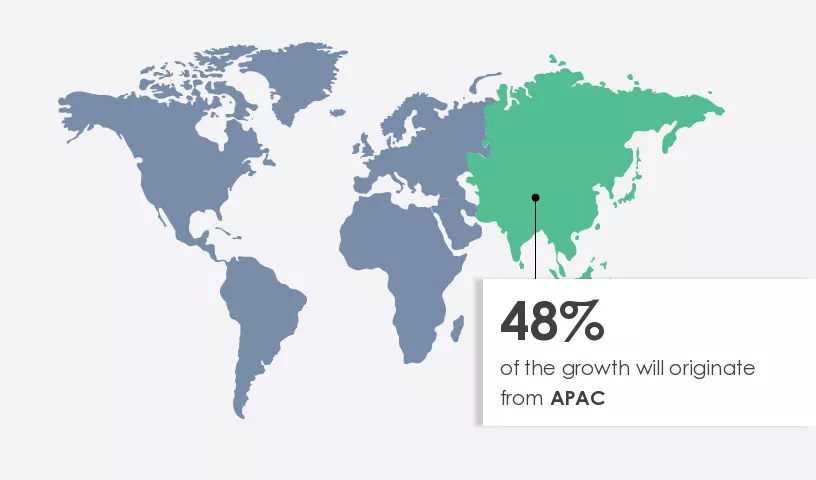

APAC is estimated to contribute 48% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. APAC is the leading construction market, owing to the rapid industrialization and infrastructural developments in the region. Government investments are increasing in the region, specifically in China, India, Malaysia, and Vietnam, in the development of new infrastructures such as roads, residential buildings, bridges, and railways. The growing construction activities are fueling the demand for building sustainable structures.

Market Analyst Overview

The advanced high-strength steels (AHSS) market is witnessing a surge in demand owing to its pivotal role in addressing key challenges across various sectors. Third-generation steel, characterized by its exceptional mechanical properties and environmental benefits, is revolutionizing industries like automotive production and rail coach building. With the rise of electric and hybrid vehicles, AHSS is increasingly favored for its ability to contribute to weight reduction without compromising on strength. This demand is further fueled by stringent steel industry regulations and the need for carbon emission reduction. As technology companies in Silicon Valley invest in solar heating systems and roofing systems, the demand for high-strength low alloy steels and advanced high-strength steels continues to grow. H2 Green Steel and Tata Steel, among others, are actively exploring AHSS solutions to enhance manufacturing efficiency while reducing carbon emissions. Additionally, collaborations between prominent automakers and steel manufacturers like Continental Automotive are driving innovations in AHSthS specifications to meet the industry's evolving needs for lightweight components and ultra-high strength steels.

This demand has spurred advancements in third generation steel, characterized by its exceptional ductility properties and ability to withstand crash zones. Moreover, AHSS, including giga steels and dual-phase steel, is gaining traction due to its high tensile strength and metallurgical type, making it ideal for active structures and aluminum alternatives. As investment pockets continue to grow, AHSS manufacturers are focusing on nomenclature considerations and AHSS designation to meet industry standards while addressing environmental effects and promoting green field investments. These developments underscore AHSS's role as a pivotal component in engineering lightweight and high-strength solutions for various applications.

The high strength low alloy segment (HSLA) is crucial for meeting demands in both the commercial sector and residential sectors. With global automobile production on the rise and domestic requirements escalating alongside economic growth, HSLA materials play a vital role in enhancing vehicle toughness and high-yield strengths. Despite their benefits, production costs remain a significant restraint, prompting the need for support and collaboration among stakeholders to navigate through stringent rules and regulations. Safety concerns, particularly regarding automotive crashes and roof strength, underscore the importance of continuous innovation in HSLA materials. Moreover, as per capita income increases and lifestyles become more luxurious lifestyle, there's an increasing emphasis on optimizing HSLA materials to ensure both safety and affordability. By addressing these challenges and capitalizing on opportunities, the automotive industry can leverage HSLA materials to drive employment opportunities and economic growth while ensuring the safety and satisfaction of consumers.

The report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

179 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11.15% |

|

Market growth 2023-2027 |

USD 13.26 billion |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

10.42 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 48% |

|

Key countries |

US, China, India, Japan, and Germany |

|

Competitive landscape |

Leading Vendors, Market Positioning of Vendors, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ArcelorMittal SA, Baosteel Group Corp., Big River Steel LLC, China Steel Corp., Cleveland Cliffs Inc., HBIS Group Co. Ltd., Hyundai Steel Co., MSP Steel and Power Ltd., Nippon Steel Corp., Nucor Corp., POSCO holdings Inc., Rashtriya Ispat Nigam Ltd., SSAB AB, Steel Technologies LLC, Tata Steel Ltd., thyssenkrupp AG, United States Steel Corp., voestalpine AG, JFE Holdings Inc., and JSW STEEL Ltd. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get sCOVID-19 customized. |

We can help! Our analysts can customize this report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Grade Type

7 Market Segmentation by End-user

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.