Aerospace Coatings Market Size 2024-2028

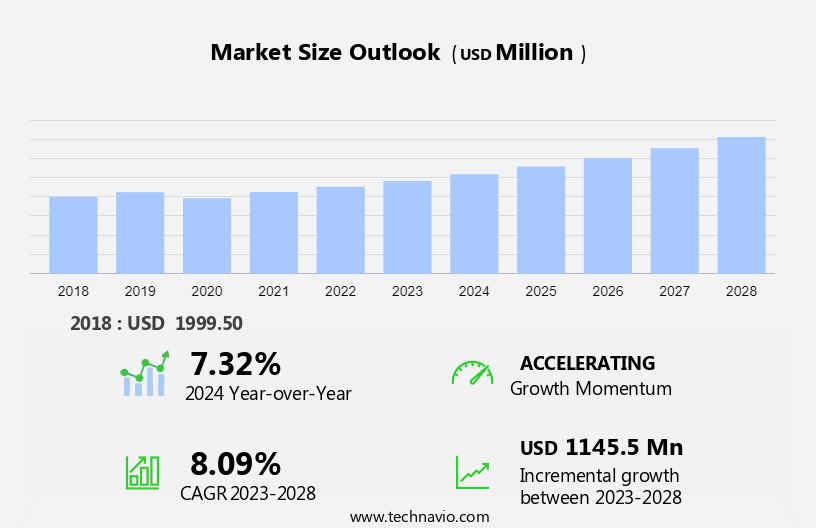

The aerospace coatings market size is forecast to increase by USD 1.15 billion at a CAGR of 8.09% between 2023 and 2028. The market is experiencing significant growth due to the increasing number of air passengers and the subsequent demand for superior aircraft components. Coating technologies, such as nano-coatings, are gaining popularity for their ability to provide enhanced protection against harsh environmental conditions. However, fluctuating raw material costs pose a challenge for market growth. Aerofleet and other fleet management solutions are integrating advanced coating maintenance systems to optimize operations and reduce maintenance costs for airline fleets. In the space exploration industry, coating processes play a crucial role in ensuring spacecraft performance and longevity.

Aerospace coatings refer to specialized coatings applied to various objects, including aircraft substrates, for both decorative and functional purposes. These coatings serve a crucial role in the aviation industry, enhancing the performance and longevity of aircraft in commercial aviation, military aviation, and general aviation. The primary functions of aerospace coatings include corrosion prevention, drag reduction, fuel efficiency enhancement, visibility improvement, and durability. Raw materials used in aerospace coatings include polymers, ceramics, and inorganic materials. The airplane maintenance company focuses on using lightweight and efficient substrates to enhance the performance of modern aircraft. The coatings are applied to various aircraft surfaces, including wings, fuselages, and engines, to improve their overall performance. In commercial aviation, passenger air travel and cargo transport rates drive the demand for aerospace coatings, while in military aviation, the focus is on durability and longevity.

Furthermore, airplane maintenance companies also play a significant role in the market, as they provide MRO (Maintenance, Repair, and Overhaul) services for the general aviation fleet. The general aviation sector also contributes to the market growth due to the increasing number of private and business aircraft. Overall, aerospace coatings are essential for maintaining the performance, functionality, and appearance of aircraft components.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Commercial aviation

- Military aviation

- General aviation

- Type

- Polyurethane

- Epoxy

- Others

- Geography

- North America

- US

- APAC

- China

- India

- Europe

- Germany

- UK

- South America

- Middle East and Africa

- North America

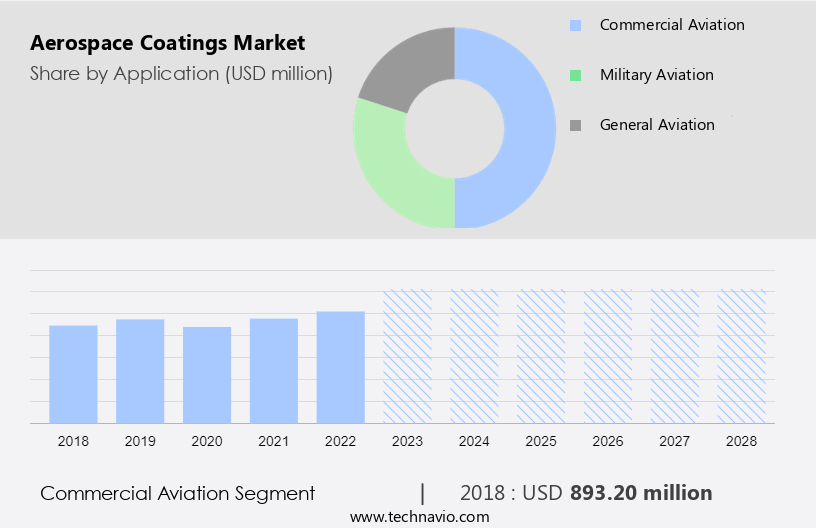

By Application Insights

The commercial aviation segment is estimated to witness significant growth during the forecast period. The market encompasses the production and supply of coatings utilized in the aviation industry, with a focus on reducing the carbon footprint of aircraft through the use of advanced, eco-friendly formulations. These coatings, primarily applied to the exterior surfaces of commercial and military aircraft, offer essential benefits such as abrasion resistance, staining resistance, and chemical resistance, ensuring the durability and longevity of the aircraft. Exposure to extreme weather conditions and ultraviolet rays during air travel necessitates the application of protective coatings on commercial aircraft. The exterior application of these coatings, predominantly polyurethane resins, safeguards against deterioration, cracking, and corrosion, thereby contributing significantly to the safety and efficiency of the aircraft.

Furthermore, in response to growing environmental concerns and increasing demand from affordable carriers and low-cost airlines, the aerospace coatings industry has witnessed a significant shift towards eco-friendly, sustainable solutions. Developing economies, particularly in the short haul sector, are expected to drive the demand for these coatings in the coming years. The defense sector is another significant end-user, with a focus on high-performance coatings offering superior resistance to harsh environments and extreme conditions.

Get a glance at the market share of various segments Request Free Sample

The commercial aviation segment was valued at USD 893.20 million in 2018 and showed a gradual increase during the forecast period.

Regional Insights

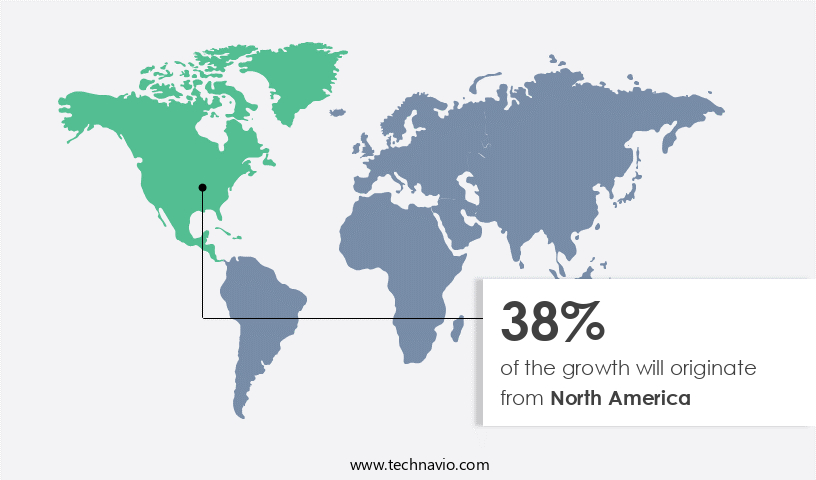

North America is estimated to contribute 38% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market is driven by the need for coatings that provide superior protection against harsh environmental conditions in the aerospace industry. North America is a leading player in this market due to its strong technological base and well-established manufacturing facilities. Aerospace coatings are essential for enhancing the performance and longevity of various aircraft components, including the airframe, engine parts, and landing gear. These coatings offer protection against corrosion, erosion, ultraviolet rays, extreme temperatures, and chemical exposure. The demand for aerospace coatings is fueled by the increasing air travel demand, particularly from affordable carriers and low-cost airlines, as well as defense spending in developing economies.

Furthermore, short haul flights in these regions are driving the market, as these flights are more susceptible to deterioration from abrasion and staining due to frequent takeoffs and landings. The carbon footprint of the aviation industry is a growing concern, and the use of high-performance aerospace coatings can help reduce the need for frequent maintenance and repairs, thereby contributing to a more sustainable industry. Polyurethane resin is a popular choice for aerospace coatings due to its excellent chemical resistance and durability.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The rise in number of air passengers is the key driver of the market. The market has experienced significant growth due to the increasing demand for air travel in both commercial and military aviation sectors. The expansion of commercial aviation, driven by the rise in business and leisure travel, and the emergence of low-cost carriers, has led to an increase in aircraft production. This, in turn, has boosted the demand for aerospace coatings, which serve both decorative and functional purposes on various objects, including substrates of nanostructure metals.

Furthermore, these coatings offer advantages such as enhanced tensile strength, corrosion resistance, and low density, leading to improved fuel consumption for aircraft. Military aviation also contributes to the market growth due to the need for advanced coatings with superior protective properties. Nanotechnology is a key trend in the aerospace coatings industry, offering potential for innovative solutions to meet the evolving demands of the aviation sector.

Market Trends

The rise in adoption of nano-coating is the upcoming trend in the market. Aerospace coatings refer to thin films applied to the surfaces of objects in the aerospace industry, enhancing both decorative and functional properties. These coatings are crucial for commercial aviation, military aviation, and general aviation applications. Nanotechnology plays a significant role in the market, with nanostructure metals and nanoparticles used for enhancing tensile strength, corrosion resistance, and reducing fuel consumption.

Furthermore, nanotechnology enables the creation of self-cleaning, thermal management, and heat and radiation resistance coatings. In aerospace manufacturing, nanoparticles, such as powdered ceramics and plastics, are used to produce coatings for aircraft engines. The ceramic particles are melted at high temperatures, around 12,632°F-14,432°F, to form a coating that offers heat insulation, while the plastic allows for the formation of tiny pores, providing elasticity.

Market Challenge

Fluctuating cost of raw materials used in aerospace coatings is a key challenge affecting market growth. Aerospace coatings play a crucial role in safeguarding aircraft from harsh environmental conditions, including extreme temperatures and corrosion. These coatings are applied to various objects, serving both decorative and functional purposes in commercial aviation, military aviation, and general aviation. The primary components of aerospace coatings include pigments, binders, and solvents.

Furthermore, among these, titanium dioxide (TiO2) is a significant raw material, contributing to the whiteness and opacity of the coating. However, the price volatility of TiO2 poses a challenge for manufacturers, as it influences the production cost and ultimately, the final product price. Nanotechnology and nanostructure metals have emerged as potential alternatives, offering enhanced properties such as increased tensile strength, corrosion resistance, and low density, which can lead to reduced fuel consumption and improved aircraft performance. Despite these advancements, the cost fluctuations of raw materials, particularly TiO2, remain a significant concern for the aerospace coatings industry.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- Aerospace Coatings Inc.

- Akzo Nobel NV

- BASF SE

- Curtiss Wright Corp.

- Henkel AG and Co. KGaA

- Hentzen Coatings Inc.

- High Performance Composites and Coatings Pvt. Ltd.

- Honeywell International Inc.

- HSH Aerospace Finishes

- IHI Corp.

- Mankiewicz Gebr. and Co.

- Metderm Treat

- Nickel Composite Coatings Inc.

- NOVARIA HOLDINGS LLC

- PPG Industries Inc.

- SOCOMORE SASU

- The Sherwin Williams Co.

- Walter Wurdack Inc.

- Zircotec Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Aerospace coatings refer to specialized coatings applied to objects, such as aircraft and spacecraft, for both decorative and functional purposes. These coatings serve various roles in commercial aviation, military aviation, and general aviation. Nanotechnology and nanostructure metals have significantly influenced aerospace coatings, enhancing their tensile strength, corrosion resistance, low density, fuel consumption, and carbon footprint. Polyurethane resin, abrasion resistance, staining resistance, chemical resistance, and protection against ultraviolet rays are essential properties of aerospace coatings. Coatings play a crucial role in exterior applications, preventing deterioration, cracking, and other forms of damage caused by air travel demand from affordable carriers and developing economies.

Furthermore, the commercial aviation sector, with its increasing fleet sizes and commercial aircraft, requires efficient aircraft, short route operations, and regulatory policies that prioritize coated aircraft. Coating maintenance, design verification tests, specifications, master files, and backlogs are essential aspects of the MRO industry. The space exploration industry also relies on aerospace coatings for spacecraft performance, space foundation organization, global space economy, commercial space sector, and space missions. High costs associated with space travel necessitate top-notch aerospace coatings that offer durability, longevity, and protection against the harsh conditions of Earth's atmosphere. Parylene conformal coatings, smart coatings, and adhesive solutions from companies are popular choices for aerospace coatings due to their advanced properties. The aerospace coatings are essential for the aviation and space industries, providing functional and decorative benefits while ensuring safety, efficiency, and cost savings. Coating technologies continue to evolve, offering improved performance, corrosion prevention, drag reduction, fuel efficiency enhancement, visibility improvement, and durability.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

175 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.09% |

|

Market growth 2024-2028 |

USD 1.14 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.32 |

|

Regional analysis |

North America, APAC, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

North America at 38% |

|

Key countries |

US, China, Germany, UK, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

3M Co., Aerospace Coatings Inc., Akzo Nobel NV, BASF SE, Curtiss Wright Corp., Henkel AG and Co. KGaA, Hentzen Coatings Inc., High Performance Composites and Coatings Pvt. Ltd., Honeywell International Inc., HSH Aerospace Finishes, IHI Corp., Mankiewicz Gebr. and Co., Metderm Treat, Nickel Composite Coatings Inc., NOVARIA HOLDINGS LLC, PPG Industries Inc., SOCOMORE SASU, The Sherwin Williams Co., Walter Wurdack Inc., and Zircotec Ltd. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -