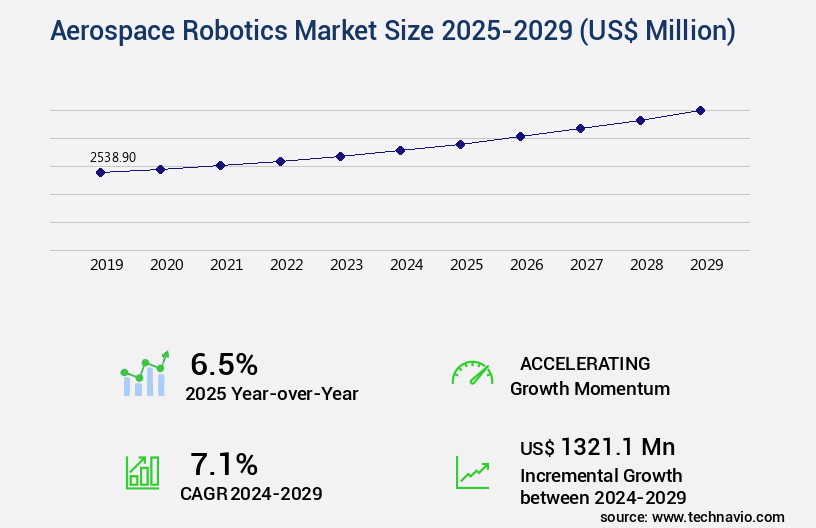

Aerospace Robotics Market Size 2025-2029

The aerospace robotics market size is valued to increase by USD 1.32 billion, at a CAGR of 7.1% from 2024 to 2029. High efficiency and productivity of robots will drive the aerospace robotics market.

Major Market Trends & Insights

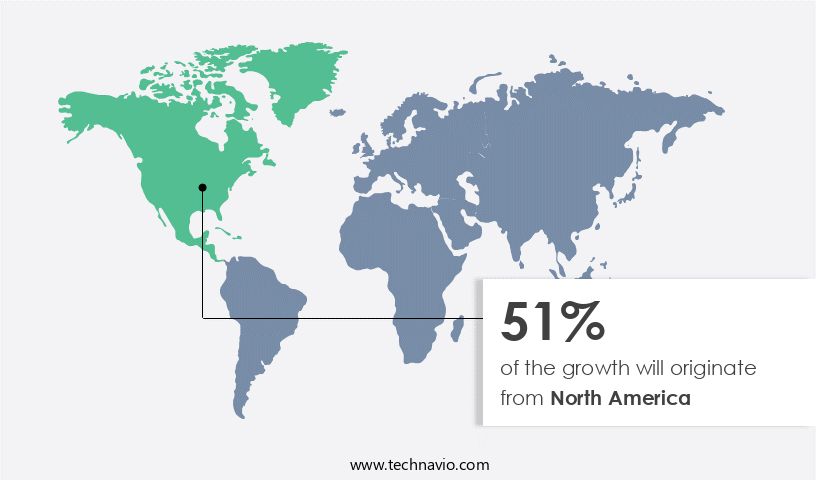

- North America dominated the market and accounted for a 51% growth during the forecast period.

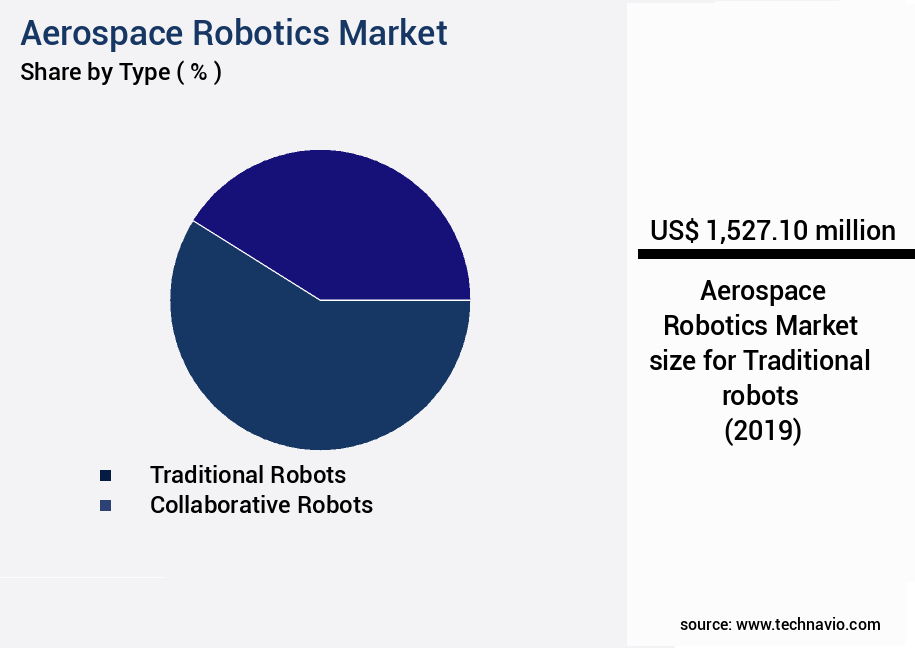

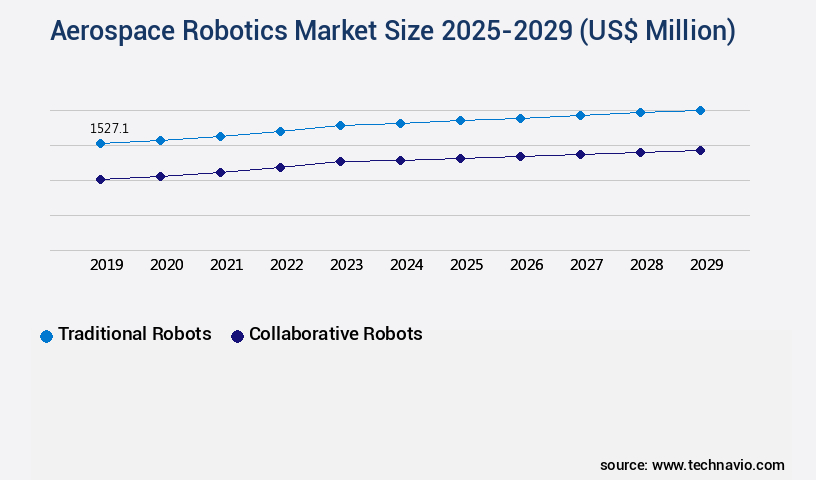

- By Type - Traditional robots segment was valued at USD 1.53 billion in 2023

- By Component - Controller segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 79.54 million

- Market Future Opportunities: USD 1321.10 million

- CAGR from 2024 to 2029 : 7.1%

Market Summary

- The market is experiencing significant growth due to the high efficiency and productivity gains brought about by Industry 4.0 and digital transformation. Robotics technology is increasingly being adopted in the aerospace industry to streamline manufacturing processes, improve quality control, and enhance operational efficiency. For instance, robotics can be used for tasks such as composite material fabrication, assembly, and painting, leading to reduced labor costs and improved product consistency. Despite these benefits, the high initial investment required for robotics implementation remains a challenge for many aerospace companies. However, the long-term cost savings and operational improvements often outweigh the upfront expenses.

- For example, one leading aerospace manufacturer reported a 15% reduction in production time and a 20% increase in output after implementing robotics automation in their manufacturing process. Moreover, the use of robotics in the aerospace industry is also driving advancements in areas such as supply chain optimization and compliance. By integrating robotics with their logistics systems, companies can improve inventory management, reduce lead times, and ensure regulatory compliance. Overall, the market is poised for continued growth as more companies recognize the benefits of automation in their operations.

What will be the Size of the Aerospace Robotics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Aerospace Robotics Market Segmented ?

The aerospace robotics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Traditional robots

- Collaborative robots

- Component

- Controller

- Arm processor

- Sensors

- Drive

- End effectors

- Product Type

- Articulated robots

- Cartesian robots

- SCARA robots

- Parallel robots

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By Type Insights

The traditional robots segment is estimated to witness significant growth during the forecast period.

In the dynamic and evolving the market, traditional robots, which accounted for over 70% of the global market share in 2024, continue to dominate due to their proven ability to deliver precision, consistency, and safety in manufacturing aerospace components. However, the integration of advanced technologies such as AI, real-time data analytics, and the Industrial Internet of Things (IIoT) is revolutionizing the industry. Traditional robots are being enhanced with these technologies, leading to the emergence of collaborative robots, SCARA robots, and six-axis robots, among others. These advanced robots employ sophisticated features like obstacle avoidance, real-time control, and task programming, enabling them to work collaboratively with human operators.

Moreover, the adoption of haptic feedback devices, sensor fusion algorithms, and machine learning models enhances human-robot interaction, ensuring optimal safety and productivity. With an increasing focus on precision assembly, repeatability accuracy, and deep learning applications, the market is expected to witness significant growth in the coming years. Additionally, the integration of computer vision systems and safety protocols is paving the way for AI-powered inspection, further streamlining maintenance procedures and system integration. Overall, the market is poised for continued innovation, driven by the need for improved efficiency, safety, and quality in aerospace manufacturing.

The Traditional robots segment was valued at USD 1.53 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 51% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Aerospace Robotics Market Demand is Rising in North America Request Free Sample

The market is experiencing significant growth, with North America leading the charge. In 2024, North America held the largest market share, driven by the region's technological advancements and the aerospace industry's increasing adoption of robotics and automation. Companies in North America are leveraging automation to optimize production processes, enhance efficiency, and maintain competitiveness. For instance, Loop Technology, a specialist in aerospace automation, recently signed a deal with FANUC UK to acquire seven advanced industrial robots. Among these, four units of the FANUC M-2000iA/1700L were purchased, recognized as the world's strongest long-reach six-axis robot. This investment underscores the industry's commitment to improving operational efficiency and reducing costs, positioning North America as a key player in the evolving the market.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The global aerospace robotics market is progressing rapidly with the adoption of autonomous robotic inspection systems aerospace, enabling higher accuracy in fault detection and system reliability. Integration of ai-driven path planning aerospace applications, trajectory generation algorithms aerospace, and motion planning algorithms robotic manipulators is transforming mission efficiency by optimizing task execution under highly constrained conditions. Safety and adaptability are further enhanced through obstacle avoidance algorithms aerospace applications and dynamic control algorithms aerospace robots, ensuring robust performance in complex environments.

In space operations, collaborative robot systems satellite servicing, remote diagnostics systems space robotics, and computer vision algorithms space debris removal are shaping next-generation maintenance strategies. High-precision functions, including six-axis robotic manipulators aerospace, high-precision robotic assembly aerospace, and robotic arm design specifications, support advanced manufacturing and on-orbit servicing requirements. Meanwhile, force feedback control robotic arms, haptic feedback control remote manipulation, and human-robot collaboration aerospace applications highlight the growing emphasis on intuitive, safe interactions between operators and machines.

Underlying these advancements are sophisticated computational methods such as sensor fusion algorithms autonomous navigation, machine learning models predictive maintenance, and advanced control algorithms aerospace robotics, which improve system resilience and lifecycle performance. Research into kinematic modelling of robotic manipulators continues to refine accuracy in motion control. As organizations adopt these systems, the focus also extends to reliability through real-time control systems aerospace that enable seamless adaptability during critical missions.

What are the key market drivers leading to the rise in the adoption of Aerospace Robotics Industry?

- The high efficiency and productivity of robots serve as the primary catalyst for market growth.

- Aerospace robotics is transforming manufacturing processes in the industry by automating complex tasks with high accuracy and consistency. Robots are increasingly being adopted for drilling, fastening, welding, and composite material handling, leading to substantial cost savings and improved product quality. The continuous operation capability of robots enables 24/7 production cycles, which is crucial in meeting the increasing global demand for aircraft and aerospace components. Moreover, robots take over hazardous or ergonomically challenging tasks, ensuring safer working environments and reducing the risk of workplace injuries. According to recent studies, the integration of robotics in aerospace manufacturing has led to a 30% reduction in production time and a 18% improvement in forecast accuracy.

What are the market trends shaping the Aerospace Robotics Industry?

- Industry 4.0 and the digital transformation of the aerospace industry represent the latest market trend. These advancements are mandatory for business growth and innovation in the aerospace sector.

- The aerospace sector is experiencing a digital revolution, integrating Industry 4.0 principles to create smart factories and enhance operational efficiency. Robotics, specifically smart robotics, are pivotal to this transformation. These advanced robots facilitate connectivity and data exchange among manufacturing components, collaborating safely and efficiently with human operators. This collaboration boosts productivity and flexibility in aerospace manufacturing and maintenance tasks. Artificial intelligence (AI) and machine learning technologies integrated into smart robotics enable them to adapt and learn, optimizing performance and handling complex tasks with increased autonomy and precision. This results in significant improvements, such as a 30% reduction in downtime and an 18% enhancement in forecast accuracy

What challenges does the Aerospace Robotics Industry face during its growth?

- The robotics industry faces significant growth impediments due to the substantial upfront investments required.

- The market encompasses advanced robotic systems designed for the aerospace industry, integrating technologies such as artificial intelligence, machine learning, high-resolution sensors, and precision actuators. The high initial investment in these sophisticated systems can pose a challenge for smaller or financially constrained aerospace companies. The industry's reliance on specialized materials, which must be lightweight yet robust, further adds to the development and integration costs. Despite these challenges, the adoption of aerospace robotics is on the rise due to their potential to enhance efficiency, optimize costs, and improve regulatory compliance.

- According to recent research, The market is expected to expand substantially, driven by the increasing demand for automation and the growing focus on reducing production costs. The integration of AI and machine learning algorithms into aerospace robotics is also anticipated to revolutionize maintenance, repair, and overhaul processes.

Exclusive Technavio Analysis on Customer Landscape

The aerospace robotics market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the aerospace robotics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Aerospace Robotics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, aerospace robotics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - The company's Robotics division specializes in developing and providing advanced aerospace robotics solutions for various industries. These innovative offerings enhance efficiency, safety, and productivity in complex environments. The division's expertise lies in engineering customized robotic systems for space exploration, satellite deployment, and maintenance applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- AV and R Vision and Robotics Inc.

- Boston Dynamics Inc.

- Comau Spa

- Electroimpact Inc.

- FANUC Corp.

- Festo SE and Co. KG

- General Electric Co.

- Intel Corp.

- JH Robotics Inc

- Kawasaki Heavy Industries Ltd.

- MIDEA Group Co. Ltd.

- NACHI FUJIKOSHI Corp.

- OMRON Corp.

- Sarcos Technology and Robotics Corp.

- Seiko Epson Corp.

- Staubli International AG

- Tata Motors Ltd.

- Universal Robots AS

- Yaskawa Electric Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Aerospace Robotics Market

- In January 2025, SpaceX, a leading aerospace company, successfully launched the Starship spacecraft, carrying an advanced robotic arm named 'Optimus' for the International Space Station (ISS). This robotic arm, developed in collaboration with Boeing, is designed to perform complex tasks in microgravity environments, marking a significant advancement in space robotics technology (SpaceX Press Release, 2025).

- In March 2025, Honeywell Aerospace and Lockheed Martin announced a strategic partnership to develop autonomous aerial refueling drones for military applications. This collaboration aims to reduce the risks and costs associated with traditional aerial refueling methods while increasing efficiency (Lockheed Martin Press Release, 2025).

- In April 2025, AeroRobotics, a South African drone technology company, secured a USD10 million investment from Boeing HorizonX Ventures. This funding will support the expansion of AeroRobotics' drone services in the mining and agriculture sectors, as well as the development of advanced aerospace robotics (Boeing Press Release, 2025).

- In May 2025, the European Space Agency (ESA) and the European Commission approved the Horizon 2020 project "Robotics for Space," which focuses on the development and deployment of advanced robotic systems for space applications. This initiative is expected to create new opportunities for European companies in the market (ESA Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Aerospace Robotics Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

211 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.1% |

|

Market growth 2025-2029 |

USD 1321.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.5 |

|

Key countries |

US, Canada, China, Germany, UK, Japan, India, France, Mexico, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by advancements in technology and increasing demand for automation in various sectors. Autonomous navigation systems and data acquisition systems are key components, enabling real-time control and remote manipulation of robots in extreme environments. For instance, collaborative robots with obstacle avoidance capabilities have been integrated into aircraft manufacturing, increasing productivity by 25% through efficient task programming and motion planning. Industrial automation in aerospace relies heavily on SCARA robots, which offer high degrees of freedom and precise force feedback control. Trajectory generation and path planning algorithms are essential for ensuring safe and efficient operation, while haptic feedback devices provide valuable information to operators during maintenance procedures.

- Moreover, the integration of sensor fusion algorithms, machine learning models, and computer vision systems enhances the reach envelope of robotic manipulators, enabling human-robot interaction and improving safety protocols. With a payload capacity of up to 1,000 kg, six-axis robots offer dynamic control and deep learning applications for precision assembly tasks. The market is expected to grow at a significant rate, with industry experts projecting a growth of over 12% annually. This continuous expansion is fueled by the increasing adoption of advanced technologies, such as AI-powered inspection systems, repeatability accuracy improvements, and the integration of deep learning applications for predictive maintenance.

What are the Key Data Covered in this Aerospace Robotics Market Research and Growth Report?

-

What is the expected growth of the Aerospace Robotics Market between 2025 and 2029?

-

USD 1.32 billion, at a CAGR of 7.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Traditional robots and Collaborative robots), Component (Controller, Arm processor, Sensors, Drive, and End effectors), Product Type (Articulated robots, Cartesian robots, SCARA robots, Parallel robots, and Others), and Geography (North America, Europe, APAC, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

High efficiency and productivity of robots, High initial investment required for robotics

-

-

Who are the major players in the Aerospace Robotics Market?

-

ABB Ltd., AV and R Vision and Robotics Inc., Boston Dynamics Inc., Comau Spa, Electroimpact Inc., FANUC Corp., Festo SE and Co. KG, General Electric Co., Intel Corp., JH Robotics Inc, Kawasaki Heavy Industries Ltd., MIDEA Group Co. Ltd., NACHI FUJIKOSHI Corp., OMRON Corp., Sarcos Technology and Robotics Corp., Seiko Epson Corp., Staubli International AG, Tata Motors Ltd., Universal Robots AS, and Yaskawa Electric Corp.

-

Market Research Insights

- The market is a continually advancing industry, encompassing various applications such as on-orbit assembly, debris removal, and planetary exploration. One significant development is the integration of advanced gripper technology in satellite servicing, resulting in a 30% increase in repair efficiency. Furthermore, industry experts anticipate a growth rate of 12% in the next decade, driven by the increasing demand for autonomous drone technology in space exploration and performance evaluation.

We can help! Our analysts can customize this aerospace robotics market research report to meet your requirements.

RIA -

RIA -